“Negative-yield bonds now account for some €1.5 trillion of debt issued by governments in the euro area, equivalent to almost 30% of the total outstanding. Many expect even more of the global bond market to fall into negative yield territory. Half of all government bonds in the world today yield less than 1%.”

– John Mauldin

This is just not normal. The issues are global. David Rosenberg points out that nearly 90% of the industrialized world economy is presently anchored by zero rates. Wow. The race into risk assets continues but those assets are bid up and richly priced.

Evans Ambrose-Pritchard wrote, “Stephen King from HSBC warns that the global authorities have alarmingly few tools to combat the next crunch, given that interest rates are already zero across most of the developed world, debts levels are at or near record highs, and there is little scope for fiscal stimulus.”

“The world economy is sailing across the ocean without any lifeboats to use in case of emergency,” he said.

In King’s grim report – “The World Economy’s Titanic Problem” – he says the US Federal Reserve has had to cut rates by over 500 basis points to right the ship in each of the recessions since the early 1970s. “That kind of traditional stimulus is now completely ruled out. Meanwhile, budget deficits are still uncomfortably large,” he said.

The authorities are normally able to replenish their ammunition as recovery gathers steam. This time they are faced with a chronic low-growth malaise – partly due to a global ‘savings glut’ and increasingly to a slow aging crisis across most of the Northern hemisphere. The Fed keeps having to defer its first rate rise as expectations fall short.

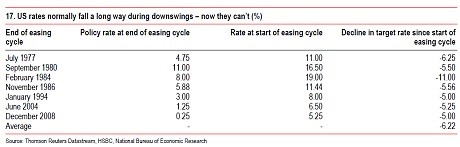

Each of the past four US recoveries has been weaker than the last one. The average growth rate has fallen from 4.5% in the early 1980s to nearer 2% this time. Oh, the problem of debt.

A quick look at past easing cycles and we can see the Fed finds itself, as my old man used to say, somewhere “between a rock and a hard place.” In the following chart, note the average decline in target rate since start of the easing cycle of 6.22%. Today we sit just next to 0.

U.S. rates normally fall a long way during downswings – now they can’t:

My personal view is that zero to negative rates will continue to drive money into risk assets. What does a European do with negative rates, a sovereign debt crisis, bank risk and lost confidence in government authorities? Smart money moves to where it is treated best and that is likely to be U.S. equities. So the aged and expensive cyclical bull can grow to be even more aged and expensive. But the snow is deep and mountain unstable. Which snowflake trips the next slide has yet to be determined.

All of this leads to what motivated me to write about in this week’s OMR. Do you remember the book by Michael Lewis titled, The Big Short? Billionaire investor Paul Singer says he has spotted the next big thing to bet against: bonds. He’s calling it “The Bigger Short.”

I’ve been actively talking about the coming default waive in HY (An Opportunity of a Lifetime Ahead – Just Not Yet). Gundlach and Bill Gross have grown more vocal on shorting bonds. So let’s look at a few highlights from a letter Singer wrote to his clients and see if we can get a better handle on just how unstable that beautifully peaceful deep mountain snow may be. I believe you’ll find the Singer notes, shared below, well worth the read.

Included in this week’s On My Radar:

- Paul Singer’s Letter – The Bigger Short

- Superpower (Indispensable America, Moneyball America or Independent America) – Ian Bremmer

- Trade Signals – Feels Like the Dog Days of Summer (Trend Positive, Sentiment Neutral, Zweig Bond Model Signals Sell)

Paul Singer’s Letter – “The Bigger Short”

Selected quotes from Singer’s client letter, “leaders abnegating their responsibilities to their citizens (in the case of presidents, prime ministers and legislators), and other policymakers (central bankers) engaging in risky, extreme and untried policies to the point where they are in way over their heads and violating (by design) the moral compact between governments and citizens that is the basis of paper money.”

“Central bankers like to protect their ‘independence,’ but that is absurd in the current context. In what sense are central bankers independent if their extreme policies just give cover to political leadership to do next to nothing to restore sustainable levels of growth? Central bank independence is a concept meant to protect the value of fiat money against grasping politicians, not to empower central bankers to pick winners and losers, allocate credit and behave as if they are fiscal authorities.”

“Today, six and a half years after the collapse of Lehman, there is a Bigger Short cooking. That Bigger Short is long-term claims on paper money, i.e., bonds,” wrote Singer in a letter to investors of his hedge fund firm Elliott Management obtained by CNBC.com.

“Bigger Short” is a play on The Big Short, the book by Michael Lewis describing how a tiny group of investors made huge sums of money for their contrarian bets against mortgage-backed securities before the collapse of the housing market in 2007 and 2008.

“Central bankers have chosen, and doubled down on, a palliative (super-easy money and QE), which is unprecedented and extreme, and whose ultimate effects are unknowable,” wrote Singer of governments stimulating markets, in part through the purchase of bonds.

Singer has long been a critic of mainstream economic policy, particularly taking on high debt to spur financial recovery.

“Asset prices are skyrocketing because of massive public-sector purchases. The tinkering and experimentation that characterizes each round of novel central bank policy leads to more and more complicated unwanted consequences and convolutions,” Singer wrote. “Central bankers are, in our view, getting ‘pretzeled’ by all this flailing, yet they deliver it with aplomb and serene self-confidence. Are they really taming volatility with their bond-buying, or just jamming it into a coiled spring?”

That makes for risk that many don’t see, according to Singer.

“Bondholders … continue to think,” he wrote, “that it is perfectly safe to own 30-year German bonds at a yield of 0.6 percent per year, or a 20-year Japanese bond (issued by the most thoroughly long-term-insolvent of the major countries) at a little over 1 percent per year, or an American 30-year bond at scarcely above 2 percent per year.”

The opportunity, then, is to short bonds.

Our view is that central bankers have chosen, and doubled down on, a palliative (super-easy money and QE), which is unprecedented and extreme, and whose ultimate effects are unknowable. To be sure, the collapse in interest rates all along the curve, and a bull market in equities, “trophy real estate” and other assets, has had some effect on job creation. However, the effect is indirect, and in our opinion the benefits of complete reliance on monetary extremism are overwhelmed by the negatives and the risks. To begin with, such policies are inefficient in actually creating jobs and growth, and they worsen inequality: investors prosper and the middle class struggles. The goal of leaders of developed nations and their central bankers should be more or less the same: enhanced growth and financial stability. But somehow the principal policy goal of both has become to generate more inflation. Both extreme deflation (credit collapse) and extreme inflation (which forces citizens to forego normal economic activities and become traders and speculators in a desperate attempt to keep up with the erosion of savings and value) are threats to societal stability, and we don’t actually think there is much to choose from between those extremes. But central bankers are completely focused on erasing any chance of deflation, and the tool to do so – currency debasement – is certainly near to hand. Therefore, the likelihood of deflation is highly remote. By contrast, the central bankers’ universal belief that inflation is easy to deal with if it accidentally overheats is arrogant and not supported by the historical record.

Furthermore, we fail to comprehend how owners of claims on money (that is, bondholders) can continue to ignore the fact that the goal of generating more inflation is aimed precisely at reducing the value of their capital. Central bankers obviously do not understand that the modern financial system is almost impossible to “manage,” and is fundamentally unsound as currently structured and leveraged. Given that reality, why should bondholders believe that central banks are capable of creating just enough inflation, and not a farthing more, in their current quest to rebubble-ize the world? We also question why bondholders believe that if inflation bursts its dictated boundaries despite central bank scolding, that policymakers can indeed, as a former Fed chairman and now immodest citizen blogger and incoming hedge fund advisor (Ben Bernanke) has said, cure it in “10 minutes.” We call to your attention the hand-wringing and agonizing now underway about raising U.S. policy rates by 25, 50 or 75 basis points over the next few months. Imagine the caterwauling in global financial markets if inflation surprises everyone on the upside and the right policy rate should be 2%, 4% or higher. Given the fragility of the financial system and its still-extreme leverage, even a few points of inflation and a few hundred basis points of increase in medium- and long-term interest rates could cause a renewed financial crisis.

You don’t need a weatherman to know which way the wind blows (according to Bob Dylan), but bondholders nevertheless continue to think, up to basically this moment, that it is perfectly safe to own 30-year German bonds at a yield of 0.6% per year, or a 20-year Japanese bond (issued by the most thoroughly long-term-insolvent of the major countries) at a little over 1% per year, or an American 30-year bond at scarcely above 2% per year.

Asset prices are skyrocketing because of massive public-sector purchases. The tinkering and experimentation that characterizes each round of novel central bank policy leads to more and more complicated unwanted consequences and convolutions. Central bankers are, in our view, getting “pretzeled” by all this flailing, yet they deliver it with aplomb and serene selfconfidence. Are they really taming volatility with their bond-buying, or just jamming it into a coiled spring?

Sometimes inflection points take a while to actualize, even when they are long overdue. For example, the unsustainable dotcom stock boom went on and on in the late 1990s, with the American stock market PE passing its all-time historical high in 1995, before topping out in March 2000 at a level twice the previous 1929 and 1972 peaks. All it would take at the present time for a collapse in developed-country bond markets to begin is a loss of confidence in paper money, central bankers or political leadership. Any combination of these could occur due to the market’s fear or projection of future increased inflation, which could bring about or accompany a self-reinforcing cycle of securities depreciation and other asset price and or wage/cost appreciation. Or perhaps a bond market collapse could ensue as part of a currency crisis in which one or more of the major currencies suffer an unexpected precipitous decline. Up to now, bond markets have acted more like puppets on a string. It would be a large and unpleasant surprise, shaking a lot of assumptions, if bond markets softened as QE continue to build and expand globally.

Current conditions are extraordinary. There has been no global deleveraging since the great financial crisis; in fact, worldwide debt has experienced a further massive increase in the last six years. Long-term entitlement programs have not been pared down to accommodate reality. Derivatives have not lessened in complexity and have actually grown in global size. Moreover, the financial statements of global financial institutions have not moved from opacity to transparency. The ingredients for a renewed financial crisis are in place, as is a possible “surprising” transformation of money debasement into highly-visible inflation.

A good or great trade is not created by just the prospect of a big move in a direction. The ability of investors to engage in a superior risk/reward profile, and to finesse the question of when the expected move will occur, is what separates “just-ok” trades from great trades. It is the extreme overpricing of bonds, and the universal confidence (unjustified, in our opinion) of investors in central banks and in the current mix of perceptions about what is safe and what is not, that makes the “Bigger Short” into possibly a great trade. To be sure, while a great trade is not a guarantee, at current prices the bond markets of Europe, the U.S., the U.K. and Japan present precious little future reward and a great deal of risk. No investor’s actuarial requirements or investment return goals can possibly be met by today’s long-term bond interest rates, but investors are holding them nonetheless because they have been making money on their bond holdings persistently and seemingly inexorably for the last few years. The day when their perceptions are challenged and they change their minds, only to find that the exit door has been blocked by everyone else doing an about-face at the same time, is going to be one heck of a day for those who have positions in bonds, whether long or short.

The Big Short was compelling pre-2007 because the pricing aberration in a specific type of debt was so huge that it didn’t cost much to wait for the trade to go right (the precise timing being impossible, as usual). We became interested in The Big Short when we saw data that subprime mortgages were defaulting at high rates even while house prices were rising. Today, the “Bigger Short” is in a much larger marketplace, so it can be undertaken in whatever size one can stomach, and the cost of effectuating it during the waiting period is really low. However, the power of the herd on the current upward bond price stampede is beyond anyone’s control, so one can lose money waiting for the trade to work out.

In terms of directional trades representing extremes of value, the “Bigger Short” is in a rare category. It is certainly not riskless, because nobody can predict how much staying power policymakers can have when they are unconstrained and have a theory (as unnerving as their theory is), and when citizens are passive and complicit in what we regard as central bankers’ risky policies. Of course, not every trader or investor is in a position to actually short bonds, but our reasoning is equally applicable to the decision of whether or not even to continue owning medium- and long-term bonds at today’s prices and yields.

This analysis is not just about one of the more interesting asymmetries of risk and reward in market history. Rather, it is about leaders abnegating their responsibilities to their citizens (in the case of presidents, prime ministers and legislators), and other policymakers (central bankers) engaging in risky, extreme and untried policies to the point where they are in way over their heads and violating (by design) the moral compact between governments and citizens that is the basis of paper money. Central bankers like to protect their “independence,” but that is absurd in the current context. In what sense are central bankers independent if their extreme policies just give cover to political leadership to do next to nothing to restore sustainable levels of growth? Central bank independence is a concept meant to protect the value of fiat money against grasping politicians, not to empower central bankers to pick winners and losers, allocate credit and behave as if they are fiscal authorities. Certainly the Fed’s “dual mandate” to pursue both monetary stability and maximum employment ought to be replaced with a single mandate to focus on financial and price stability. It doesn’t matter that the other major central banks are engaging in similar practices (QE and ZIRP or NIRP) despite lacking a maximum-employment mandate of their own; eliminating the dual mandate would still be an important symbolic act aimed at pushing back against the arrogance of the Fed and forcing the President and Congress to face up to their responsibilities for optimizing growth and sustainable employment.

The central bankers of the developed world are the architects and enablers of a policy mix whose most powerful result is to further enrich the already well-off, which is clearly posing a challenge to the social fabric of the developed world. It is possible that this situation could worsen if central bankers, frustrated by their economies’ refusal to dance to their incessant piping, step up the pace of their bond-buying and possibly convert it to more direct forms of money-printing, which at some point is certain to ignite the inflation that they have been trying merely to kindle. Don’t fall out of your seats if inflation then burns right through the finely-tuned “target” and keeps on going. If this happens, we all may find out whether they indeed can, or have the courage to, stop inflation in “10 minutes.”

Superpower (Indispensable America, Moneyball America or Independent America) – Ian Bremmer

The Singer piece was long but important so I’ll do my best to keep this section short though no less important. I wrote a few weeks back about Ian Bremmer. He is my favorite geopolitical analyst. He is out with a new book titled Superpower and I link to a summary well-crafted by good friend John Mauldin in an Outside the Box piece he shared this week. Let’s keep the following on our radars as well.

Bremmer begins, “President Obama hosts a Gulf security summit, and most Arab leaders decide not to attend. Israeli Prime Minister Netanyahu comes to Washington to address Congress on Iran over protests from the president. Britain ignores pleas from the United States and becomes a founding member of the China-led Asian Infrastructure Investment Bank, a potential competitor for the World Bank. The Obama administration gripes that the Brits are pandering to the Chinese. Russia’s Putin, like Syria’s Assad, strides across American redlines with little consequence. Beijing and Moscow announce joint military exercises… in the Mediterranean. NATO ally Turkey turns to China for new defense equipment. The Dutch go to Huawei for internet security. These are not random events.

What’s going on?

America is not in decline. Look to the strength of the dollar, US equity markets, employment levels and the economic rebound, the energy and food revolutions, and generation after generation of technological innovation. But America’s foreign policy and its international influence most certainly is in decline. Superpower or not, too many countries now have the power and self-confidence to say no to US plans.”

Click here for a short summary. I plan to read the book this weekend.

Trade Signals – Feels Like the Dog Days of Summer (Trend Positive, Sentiment Neutral, Zweig Bond Model Signals Sell)

Speaking about “The Bigger Short”, one idea to consider is to use the Zweig Bond Model Signal as a tool to get on the right side of the trend. Right now it is in a “Sell” signal. Nothing is perfect in this business so expect some false signals but it is about probability and process and this to me is a good way to stay on the right side of the trade (long or short). I believe Singer will be proven correct and he is also correct in saying one might have to wait for some time before the big payoff. Price action, as measured by the Zweig Bond Model, can help tell us a lot about supply and demand. It is my favorite indicator for shortening or lengthening bond market exposure. For more aggressive speculators, the short trade is worth considering. Consider the risks and size accordingly.

I mentioned the following in Wednesday’s post:

Sentiment is neutral and the overall trend, while aged, remains positive. The Zweig Bond Model remains in a “Sell” signal suggesting shorter-term bond exposure is favored. High yield remains the strongest bond asset category. Our CMG HY Program remains in a buy.

Click here for the updated trend and sentiment charts.

Personal note

So step forward with your equity exposure hedged and mindful of the elevated risk. Keep a close eye on the market’s primary trend. Price can tell us a lot about supply and demand. I favor Big Mo and 13/34 Week Moving Average (posted each week in Trade Signals). Include within your portfolio(s) a small handful of alternative strategies (defined as anything other than traditional buy-and-hold stocks and bonds) that demonstrate low to no correlation to stocks and bonds. Today, I believe we are in a participate but protect environment. Great opportunities present when markets dislocate. And dislocate they will. Let’s not get run over on the way to the opportunity.

Speaking of stepping forward. Tomorrow is an all-day soccer tournament for Team 6. Great name – I know. Susan and I tried to convince our boys to go with Team 6 and the Killer B’s (last name initial) but rightly so they shot that idea down. Anyway, all five of our boys play on the same township co-ed high school rec team. A small window of time and first to see them on the field together. You should see the 13 year old give the 18 year old the business. The want to win is big and it will be tested this weekend. Hopes are high and the team looks strong.

I believe a pasta meal is planned for this evening. The excitement is building and honestly it is really fun for Susan and I to see them playing on the same field together. Time is moving much too fast. I’ll see if I can share a picture next week. Hopefully with trophy in hand (or free t-shirt).

I’m in New York again next week with John Mauldin and Robert Schuster from NDR. We are meeting on Tuesday with an innovative new “smart beta” ETF company that is doing something really exciting. John just sent me a note that he has an extra pass to see George Gilder and Jim Grant do a lunch presentation on information economics at the Princeton Club. Really looking forward to both meetings. Should be fun. Chicago is on deck next June 10-11 and then back to NYC on the 17th for an Envestnet Manager forum.

So happy that summer is here. Wishing you a great weekend!

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM and the CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

© CMG Capital Management Group

© CMG Capital Management Group