Three Keys Why Retired Investors Should Put Maximum Focus and Weight On Dividends

Introduction

In today’s low interest rate environment, prudent long-term investors, especially those in retirement, are best served by putting maximum weight and focus on dividends. There are important reasons why I support this position, and those reasons will be the focal point of this article. However, putting maximum weight and focus on dividends does not simultaneously mean at the exclusion of other important fundamental metrics.

Prudent long-term investors, especially those in retirement, should also be paying attention to important fundamentals associated with ascertaining intrinsic value. A dividend paying company’s past, present and potential future dividend income stream can serve as an excellent barometer of fair value. In this context I am suggesting that the prudent investor start by evaluating each respective dividend paying research candidate’s historical dividend record.

At this point, I recommend first analyzing how long a company has been consecutively paying dividends in order to get a feel for management’s dividend policy and commitment. Next, it’s important to analyze the company’s record of dividend growth. When evaluating a given company’s historical dividend growth rate, consideration should also be given to the type of dividend paying company being evaluated. For example, the typical utility stock might offer high current yield, but relative to other companies’ lower historical dividend growth rates.

Finally, I believe it’s important to evaluate the company’s current yield in relation to its historical norms. A current yield that is higher than the company’s historical norm would indicate attractive valuation. Conversely, if the company’s current yield is significantly below historical norms this would indicate that the company might be overvalued. My point being that properly analyzing a company’s dividend record can be an effective way to appraise its relative investment merit. This process applies to both the appropriateness of a potential sell decision and/or the appropriateness of a potential buy decision.

Primary Arguments for Focusing On Dividends

Importantly, this article is primarily directed to retired investors, or prudent dividend growth investors interested in maximizing the income from their portfolios at controlled levels of risk. Keeping your risk under control is the most important part of that last statement.

Additionally, the principles underpinning this article apply to long-term ownership oriented investors. Focusing on dividends only makes sense when your objective is to own a business for many years to come. When your intention is to own a business for many years, even decades, short-term price volatility becomes irrelevant. In contrast, a long-term income stream that preferably is growing each year is paramount. Therefore, it makes no sense to fret about the daily gyrations of stock price. Instead, it makes better sense to focus on your income stream (your dividend) which is actually vitality important to you.

I bring this to the reader’s attention in order to clarify certain vagaries that many anti-dividend articles tend to postulate or imply. Most of the articles that I have personally come across that are negative on dividends involve warnings against concepts such as yield chasing. At other times they have a tendency to propose that dividend investing simultaneously means accepting lower total returns. Personally, I am also against investors reaching for securities that offer excessively high yields. For the most part, these tend to be risky, and therefore, may not be appropriate for conservative income seekers.

Regarding giving up total return, I reject that notion almost completely pending one important qualifier. If retired investors are choosing blue-chip dividend growth stocks, such as those found on fellow Seeking Alpha author David Fish’s CCC lists, they don’t automatically have to give up above-average total returns if they pay attention to valuation.

In truth, not all, but the majority of Dividend Champions and Contenders are high quality above-average companies. Therefore, if they are properly invested in with a disciplined valuation approach, they are quite capable of providing attractive yield, above-average growth and a high level of safety. In short, they can produce attractive and above-average total returns at reasonable levels of risk.

With the above said, my primary argument supporting focusing on dividends is based on the concepts of predictability and reliability. Dividends are a fundamental metric; typically they are paid and reported four times a year in concert with the company’s quarterly financial reports. This is in stark contrast to stock price movements and their inherent unpredictability and unreliability, which are reported virtually every minute of every trading day.

Focusing on stock price volatility can provoke the risk of making emotionally charged, and therefore, potentially irrational investing mistakes. Whereas trusting fundamentals such as a reliable and predictable dividend payment tends to be more reasoned and analytical. In the short run, stock prices are liable to go anywhere. The stock market is an auction, and as such, short run price movements can deviate from fundamental values based on emotional reactions to a piece of news, reports on the economy, or any number of exogenous events.

On the other hand, in the longer run fundamental values will prevail. When it comes to dividends, if the company is producing earnings and cash flows that cover and support the dividend payment, I believe it is more intelligent to trust that than it is fickle stock price movements. The key to the successful accomplishment of learning to trust dividends rests in the fact that you only have to contend with them once a quarter. Everything in between, especially bouncing stock prices, is just noise that you are best served to tune out.

Real-World Evidence Testing the Value of a Focus on Dividends

In the introduction I presented three key ways that focusing on dividends can assist prudent income oriented retired investors towards making sound investment decisions. With the remainder of this article I will put those three keys to the test with real-world examples. My objective is to illustrate the validity of why I believe that retired investors should put maximum weight and focus on dividends. The three keys to analyze and focus on are as follows:

- Historical record of dividend payments and increases

- Historical record of dividend growth rates

- Current yield in relation to historical norms

In order to clearly illustrate my thesis on placing maximum weight and focus on dividends, I will turn to the FAST Graphs™ fundamentals analyzer software tool and FUN Graphs (fundamental underlying numbers). I will start out by running the three keys discussed above on the S&P 500 index in order to establish a benchmark. Next I will produce examples of various types of dividend producing companies. Each of these examples will be presented based on the three keys above.

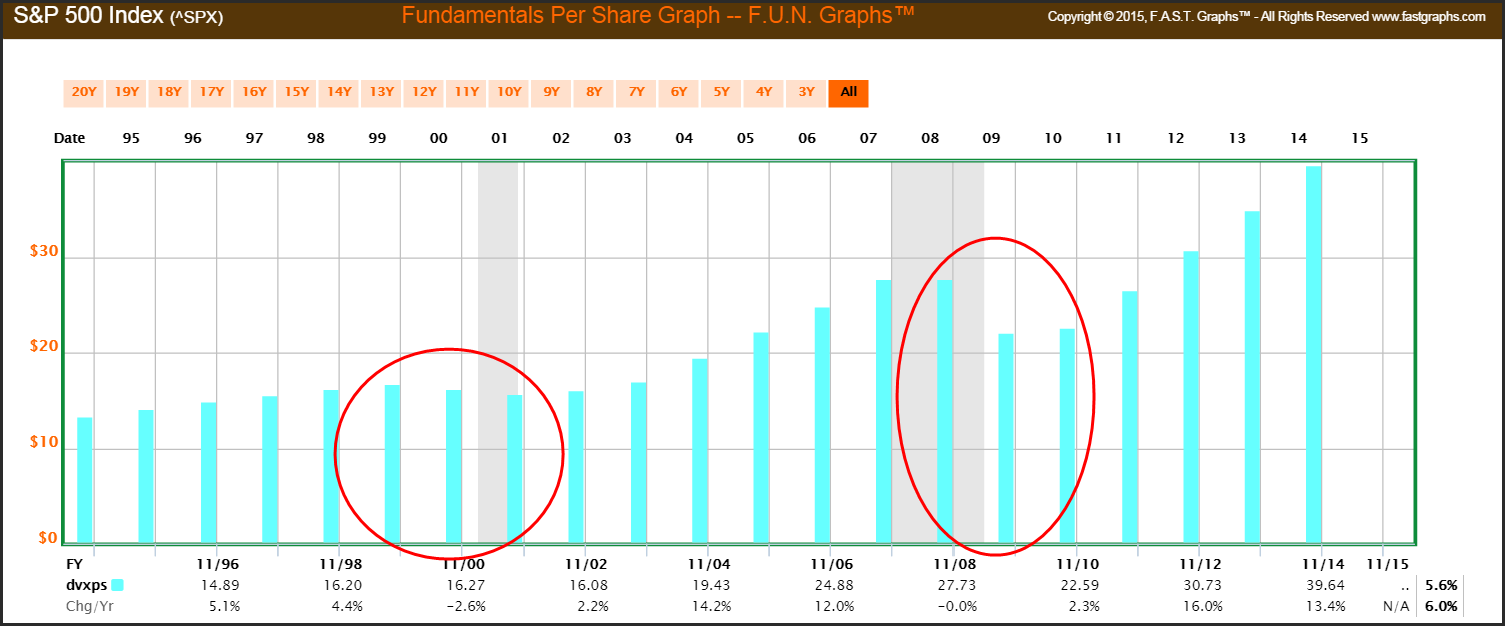

S&P 500 index

When evaluating the historical dividend record of the S&P 500 we discover that dividends were cut during both the 2001 and 2008 recessions (see red circles). Otherwise the dividend record of the S&P 500 has been consistently increasing. Nevertheless, retired investors invested in the S&P 500 index would have experienced reductions in their income, as well as significant drops in stock price during both recessions.

However, it should be interesting to note that coming in to the 2001 recession the S&P 500 was significantly overvalued. In contrast, the Great Recession of 2008 was more severe, and in that case, both stock price and dividends followed dropping earnings.

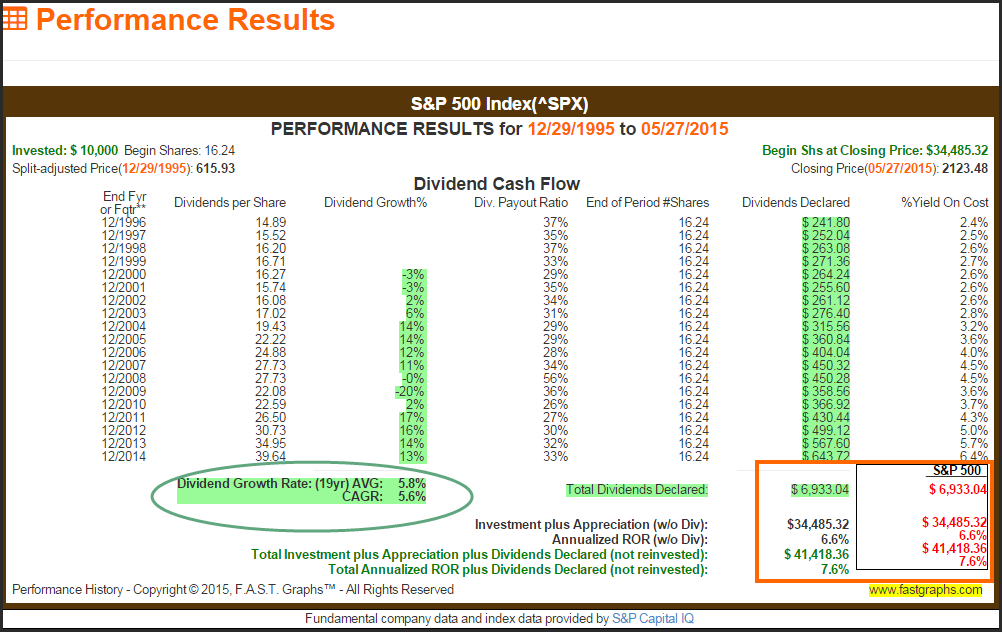

When evaluating the dividend growth rate of the average company as represented by the S&P 500, we discover that the average company grew their dividends at a 5.8% average and a 5.6% compound annual growth rate (CAGR). Therefore, in spite of the 20% dividend income drop during the Great Recession, index investors would have seen their dividend income generally increase.

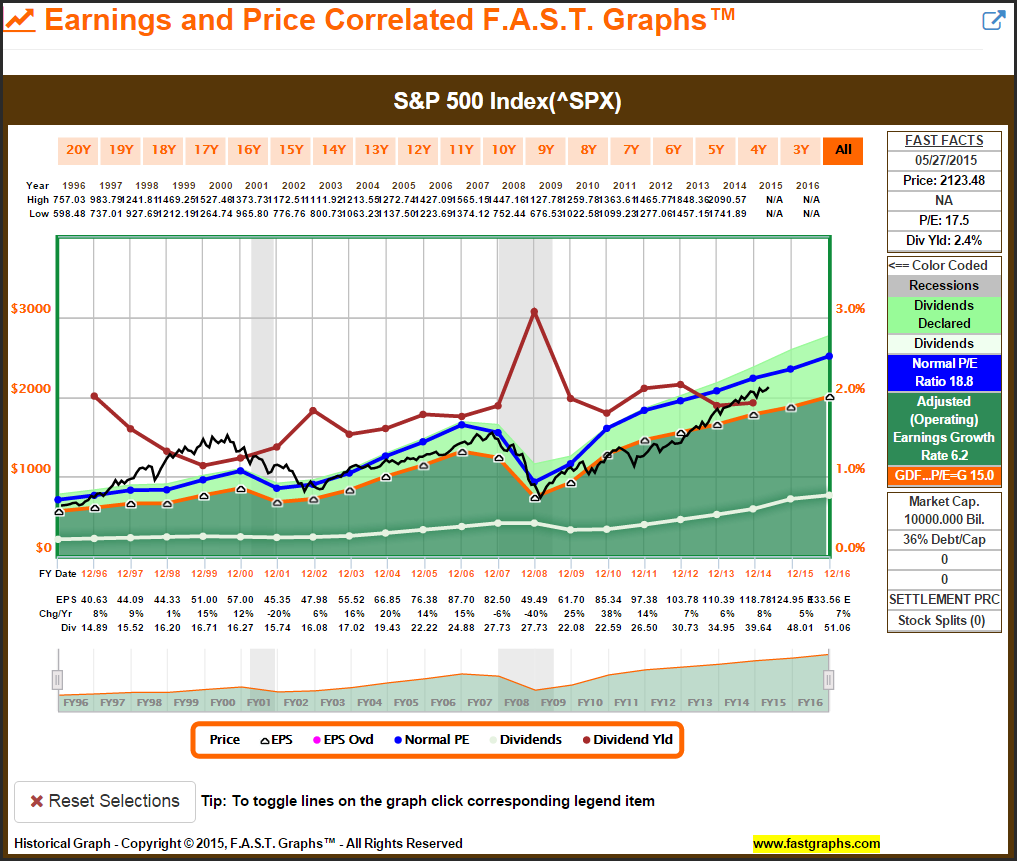

On the next graphic I present a complete earnings and price correlated FAST Graph with dividends on the S&P 500. Additionally, in order to evaluate the historical normal current yield, I have overlaid the annual dividend yield (burgundy line) and added the yield scale to the right of the graph. The value of the dividend yield line is that it represents an inverse of valuation based on price. When the yield is high, valuation is low, and vice-versa. Therefore, as we will also see with the examples of individual companies below, an above-average dividend yield is a great indicator of an investment opportunity, and vice-versa.

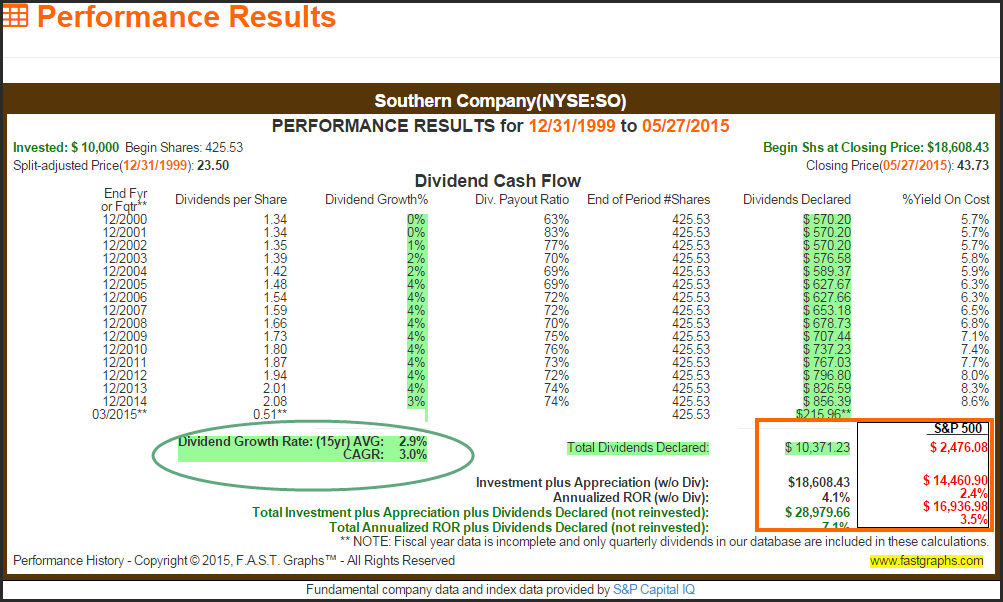

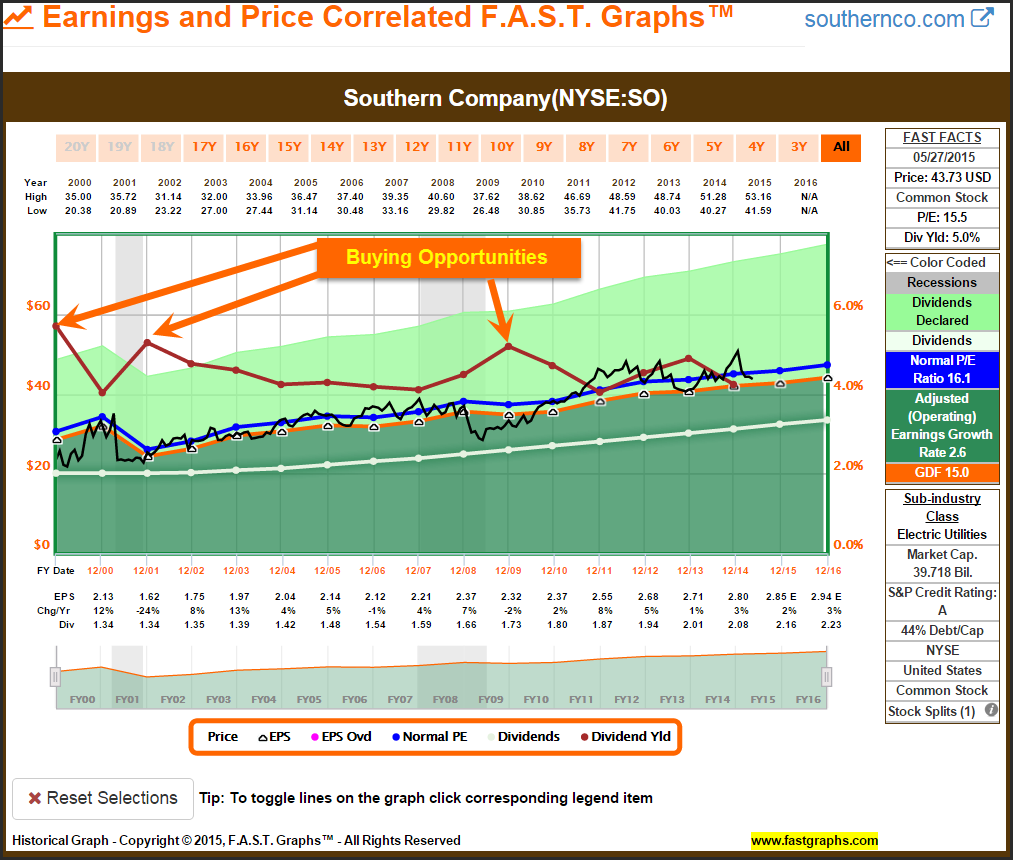

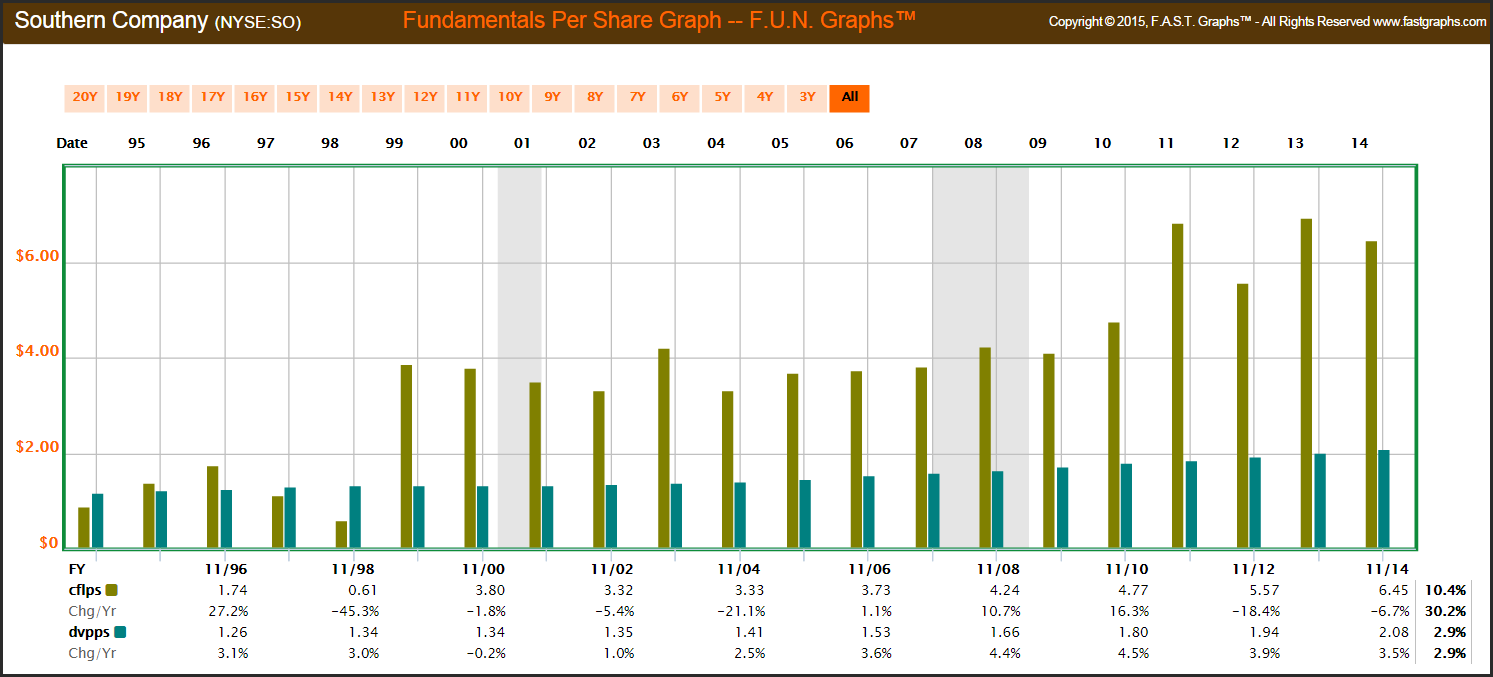

Southern Company

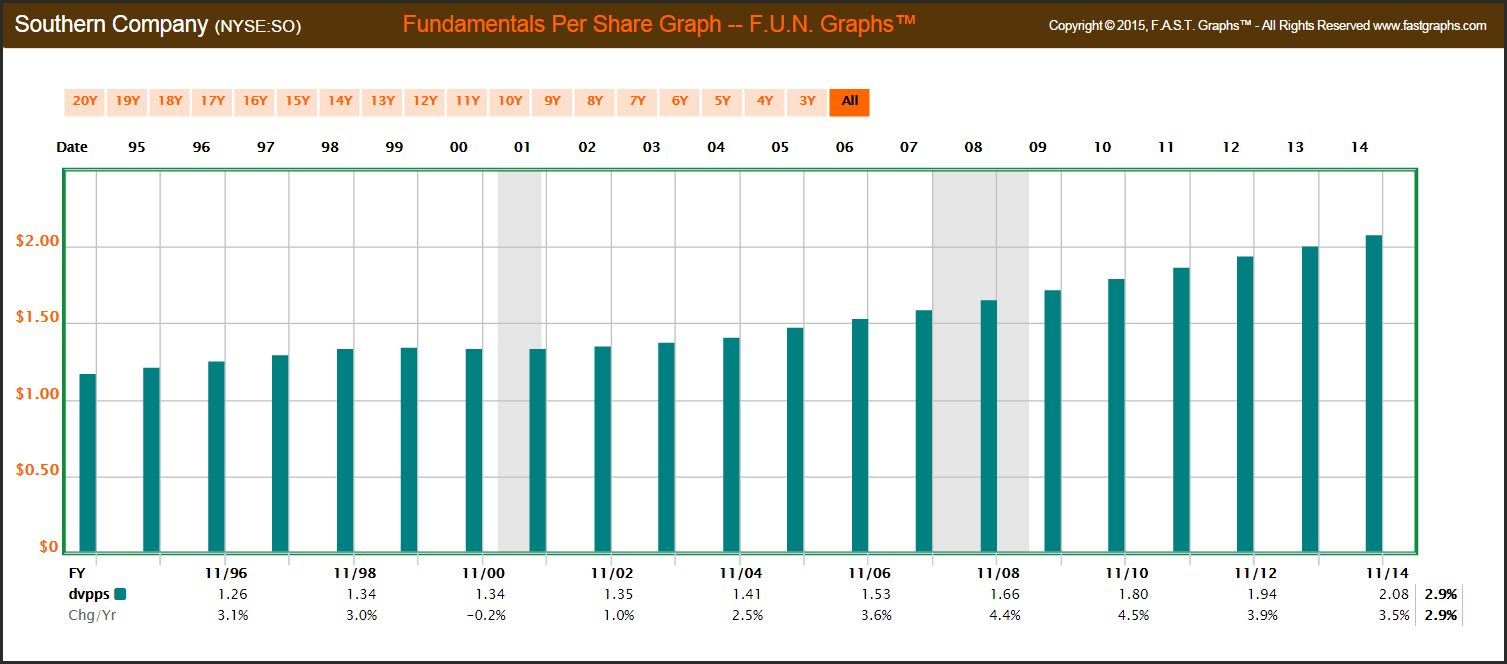

My first individual example looks at Southern Company (SO), a high-profile utility stock. Utility stocks generally provide the advantage of above-market yield, but that yield advantage is compromised by typically lower rates of growth.

In spite of lower growth, the following annual dividends paid FUN Graph on Southern Company supports my position on the calming effect of placing maximum weight and focus on dividends. While stock prices even for a low-growth utility stock are volatile in the short run, annual dividends are more predictable and reliable. Even during both recessions, the retired investor’s annual income either remained steady or increased.

Although the dividend growth rate for Southern Company was lower than the dividend growth rate of the S&P 500 index, the yield advantage produced significantly more total cumulative dividend income. It is interesting to note that Southern Company’s above-average dividend yield enabled it to significantly outperform the S&P 500 index on a total return basis. This provides supporting evidence of the power and protection of dividends, even for a low-growth utility stock.

Even though Southern Company is a low-growth utility stock, an analysis of its historical normal dividend yield proves illuminating. Clearly the optimum time to invest in a utility stock is during periods when the current yield is above historic norms.

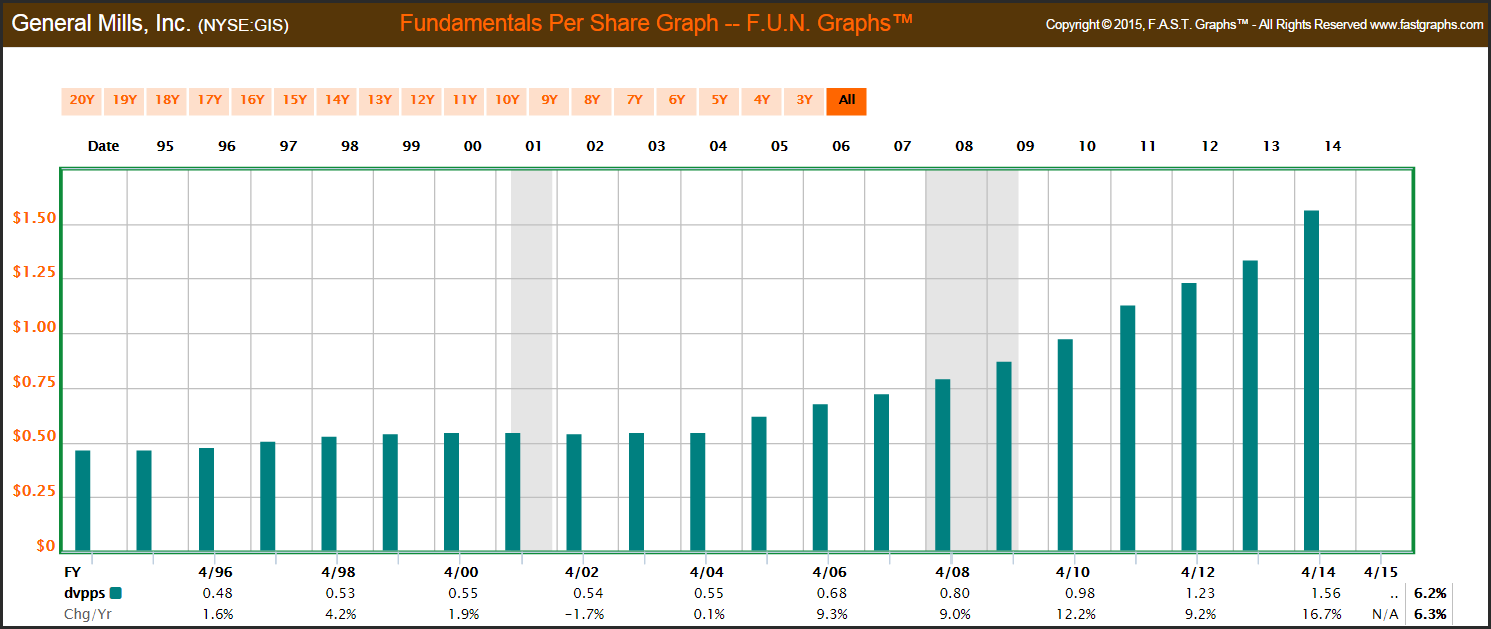

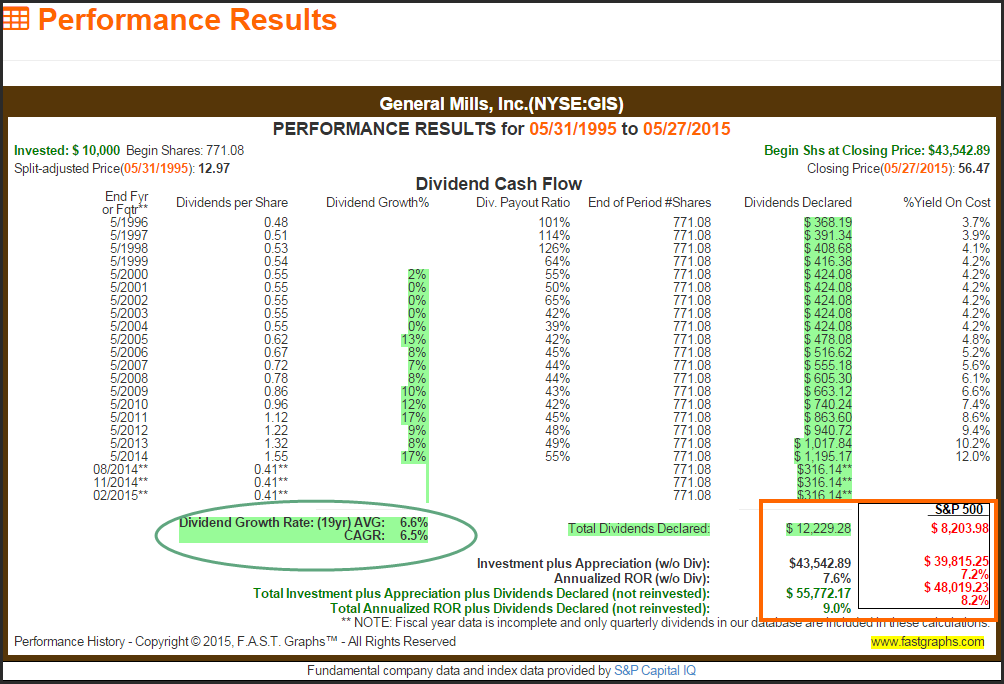

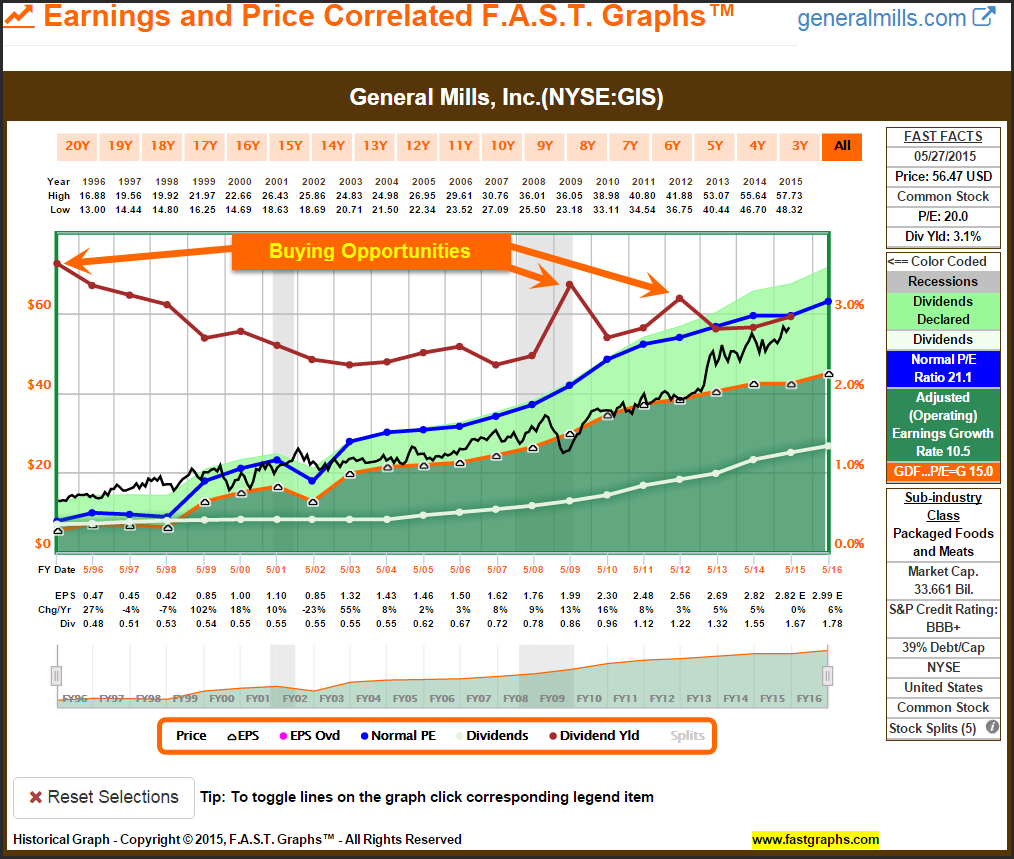

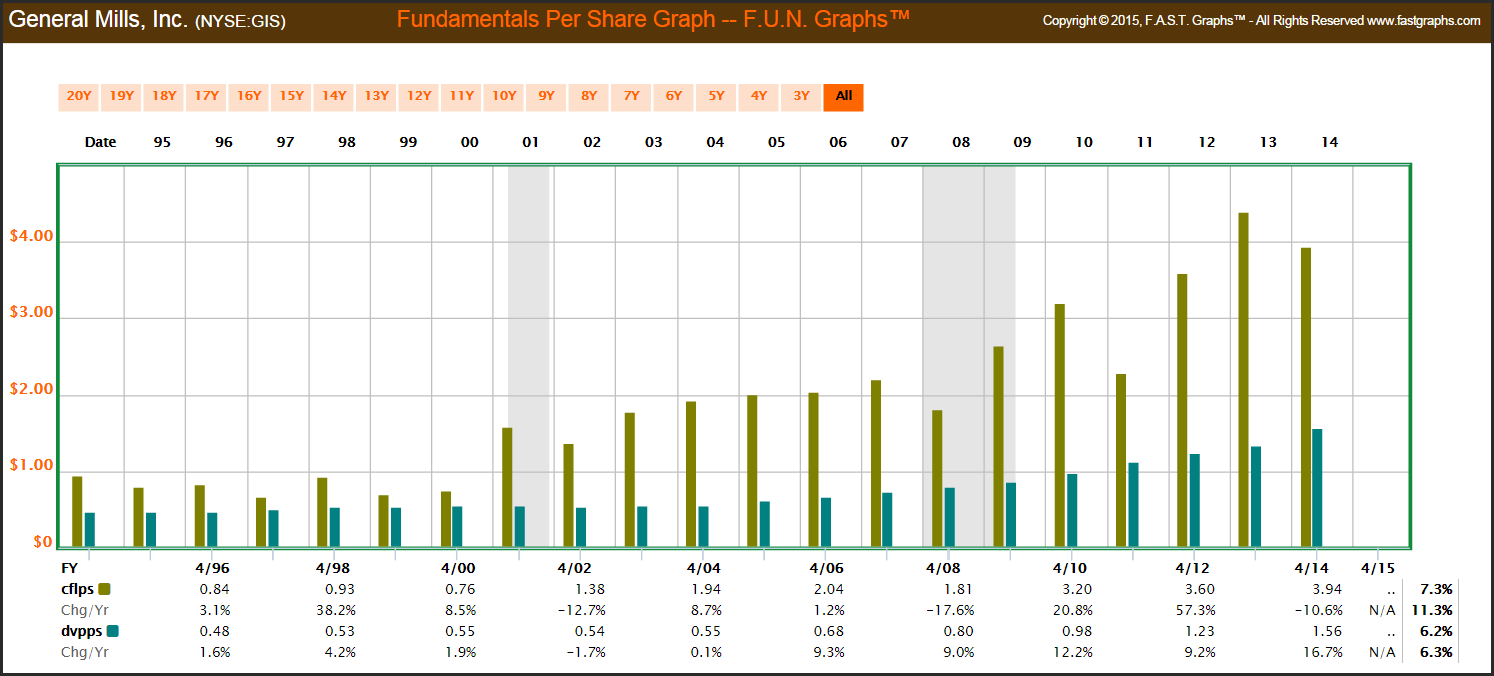

General Mills, Inc.

With my second example I review General Mills (GIS), a Dividend Contender that has raised its dividend for 10 – 24 consecutive years. Although General Mills is widely-recognized and carries an investment grade credit rating of BBB+, it is not in the same class as my next example AAA rated Johnson & Johnson. However, that is precisely why I chose it as one of my examples.

General Mills did modestly reduce their dividend during the recession of 2001 by a penny per share, but that was hardly an interruption in shareholder income. Otherwise, focusing on General Mills’ income stream versus its stock price movement should have kept long-term shareholders calm and collected.

General Mills has grown their dividend on average by 6.6% and a comparable compound annual growth rate of 6.5%. This is slightly higher than the S&P 500 index, and it should be noted that General Mills has consistently offered investors a higher current yield. Consequently, higher cumulative dividend income and capital appreciation resulted in a higher total return than the index. This supports my statement that dividend growth stocks are capable of producing above-average long-term total returns for their shareholders.

Note: S&P 500 values are different than above due to the fact that the timeframe measured is based on General Mills’ fiscal year ending in May.

Going through the exercise of evaluating General Mills’ historical annual current yields provides interesting insights. We discover that General Mills’ current yields were highest during fiscal years 1996, 1997 and 1998. However, the interesting part is that this is also a time when valuation was high. A closer examination reveals that this was a time when General Mills was paying out in excess of 100% of their earnings. This should have been a matter of concern for prospective investors at that time.

However, after fiscal year 1999, General Mills was once again paying out an appropriate portion of earnings and their current yield normalized. The above normal current yield seen during the Great Recession of 2008 indicated a great buying opportunity.

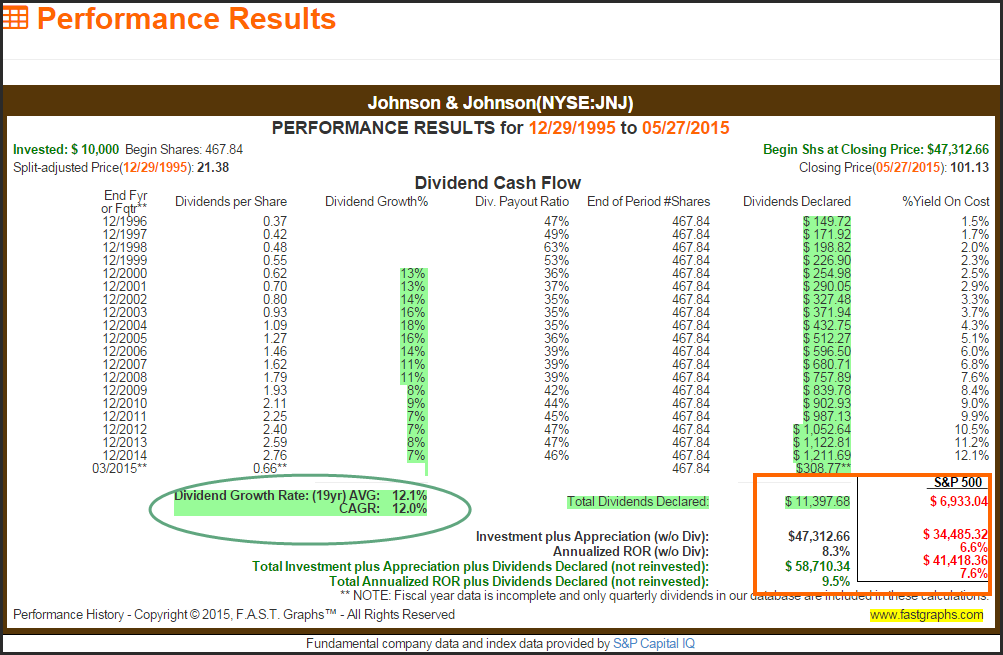

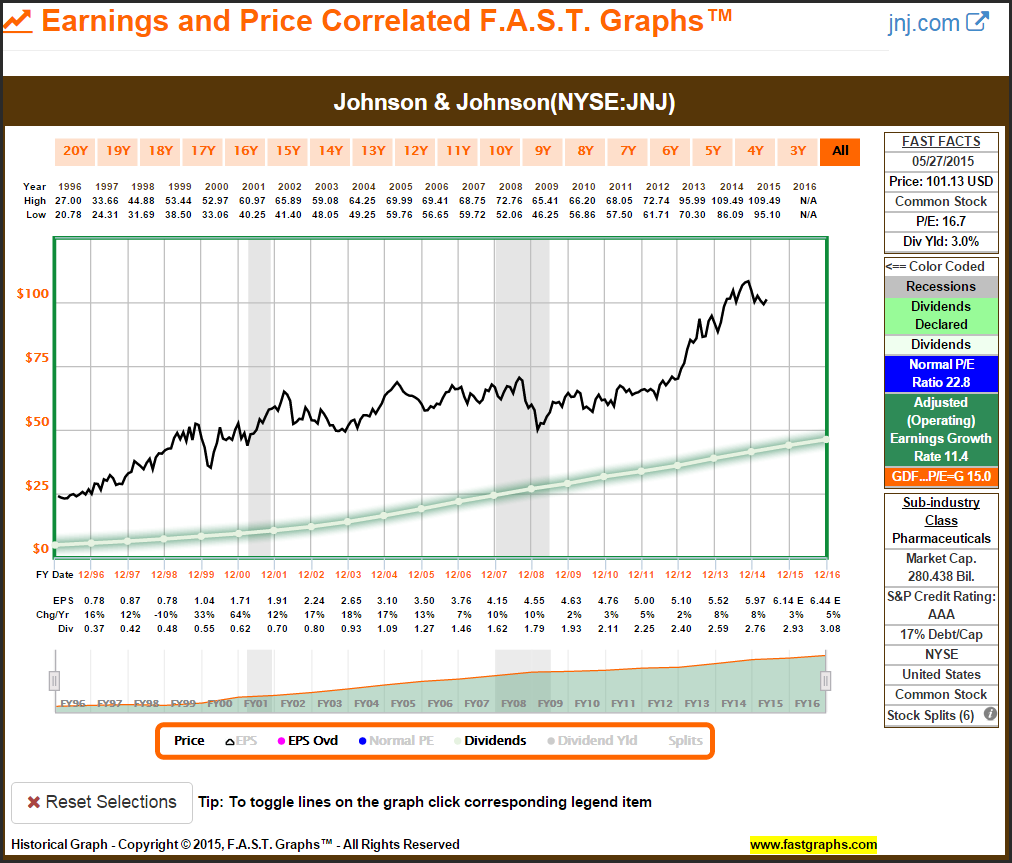

Johnson & Johnson

Johnson & Johnson (JNJ) is highly regarded as the best dividend growth stock to own by many dividend growth investors. A quick glance at its historical dividend record shows why AAA rated Johnson & Johnson is so highly rated. The consistent growth of Johnson & Johnson’s dividend supports my thesis that retired investors should place maximum weight and focus on dividends. As I will illustrate later, historically you could not overpay for Johnson & Johnson and lose money in the long run. The company’s impeccable dividend record is the primary reason.

Johnson & Johnson is a quintessential example of a perfect buy and hold dividend growth stock. The company’s long-term average and compound annual dividend growth rates clearly support the power and importance of a great dividend record. It’s important to note that dividends were a significant component of Johnson & Johnson’s total return outperformance versus the S&P 500.

In spite of my statement that you cannot overpay for Johnson & Johnson and lose money in the long run, it is still prudent to focus on its current yield relative to historical norms. Clearly, the optimum times to invest in Johnson & Johnson were during those times when its current yield (the burgundy line) was highest.

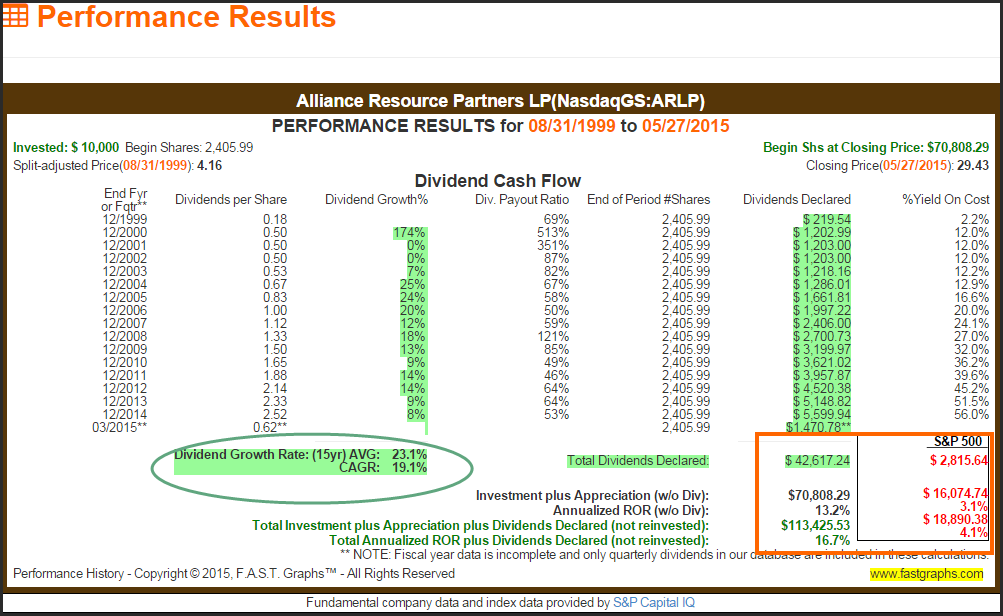

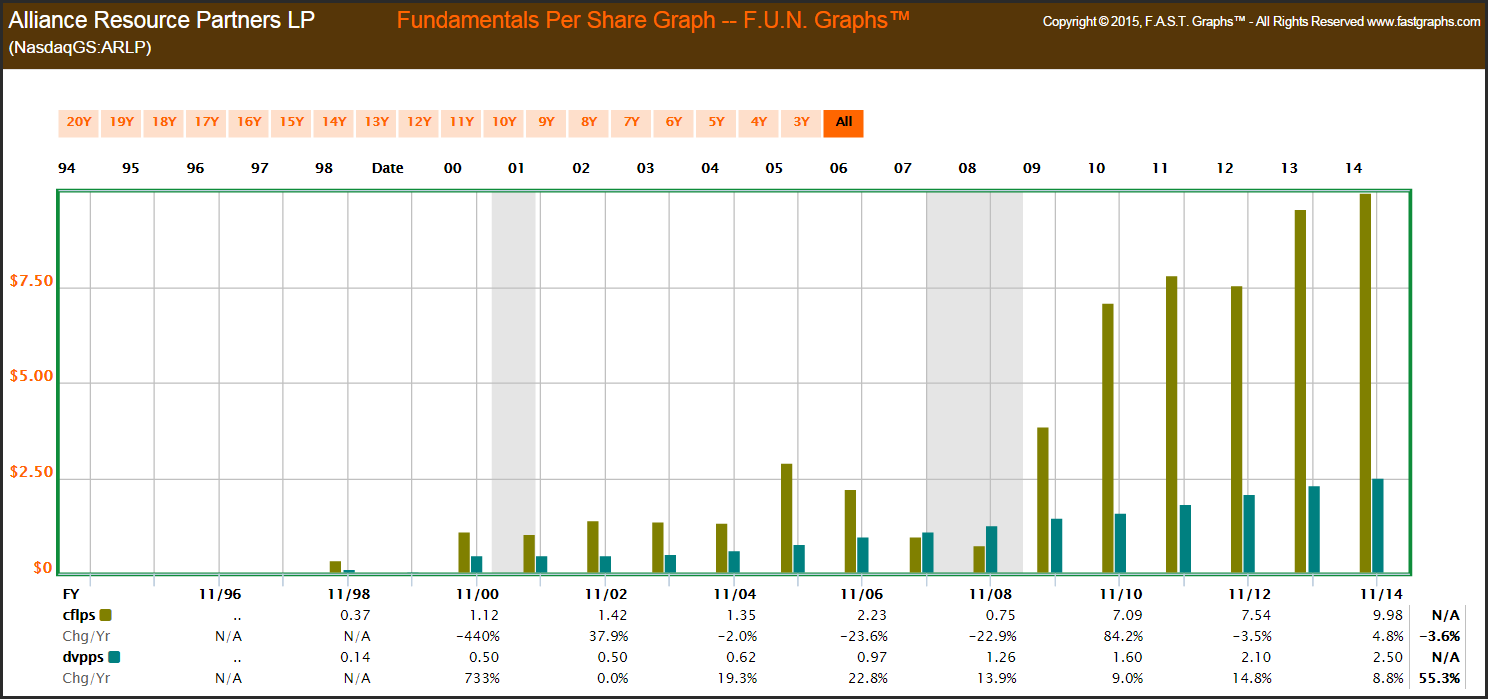

Alliance Resource Partners

With my final example I offer Alliance Resource Partners (ARLP) as an example of a high-yield higher risk dividend growth stock. As mentioned above, chasing yield can be dangerous and Alliance Resource Partners’ recent stock price history validates that admonition. However, this article is oriented to the power and protection of dividends, and Alliance Resource Partners represents a good example of how a solid dividend record can benefit investor shareholders focused on income.

In spite of all the controversy surrounding energy in general, and coal in particular, this master limited partnership has produced an impressive dividend distribution history. If you focused on this company’s stock price volatility, you could get very nervous. On the other hand, if you put maximum weight and focus on its dividend, you would be less inclined to fret or worry.

There is no comparison to the long-term returns Alliance Resource Partners’ shareholders have enjoyed relative to the S&P 500 index. Total cumulative dividend income has dwarfed the average company, and in spite of its recent drop in stock price, so has long-term capital appreciation. Even with a higher risk dividend growth stock like Alliance Resource Partners, the importance and protection of dividends cannot be denied.

As we have seen with all the previous examples, a higher than historically normal current yield represents a great buying opportunity. It is interesting to note that these great buying opportunities were during times when short-term price performance was at its worst. As Warren Buffett so eloquently put it, “be greedy when others are fearful” works extremely well when your focus is on dividends.

Are the Dividends Covered and Secure

As previously stated, in the longer run fundamental values will prevail. When it comes to dividends, if the company is producing earnings and cash flows that cover and support the dividend payment, I believe it is more intelligent to trust that, than it is fickle stock price movements.

The following FUN Graphs on each of the examples presented in this article present cash flow per share (cflps) and dividends paid per share (dvpps). I believe these graphs speak loudly to the point made above about dividends being reliable and predictable. When a company has ample cash flow to support the payment of a dividend, shareholders can be confident that dividends will continue.

Summary and Conclusions

Retired investors should put maximum weight and focus on dividends because they are more reliable and predictable than fickle short-term stock price volatility. Stock price movements are not always rational, and in truth and fact, that is true most of the time over the short run. In contrast, dividends are a pure function of the company’s operating results, and as such, a fundamental metric.

Consequently, I contend that stock price movements, especially in the short run, cannot be trusted. In contrast, consistent and predictable growing dividends can be analyzed and evaluated by reviewing a company’s financial statements. The following graphics depict the company’s historical stock price and dividend for each example company in this article. Since a picture is worth a thousand words, I suggest the reader reflect on how nervous and unpredictable the stock price line (black line) is in contrast to how consistent the dividend line (the green shaded line) is.

Disclosure: Long GIS, JNJ, ARLP at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.