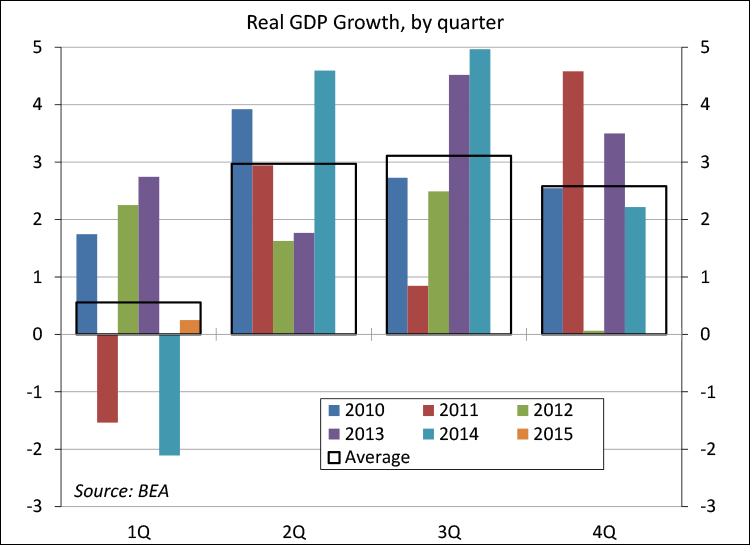

The current economic expansion is rapidly approaching its six-year anniversary. Contrary to popular belief, the likelihood of entering a recession does not depend on the age of the expansion. However, there are other issues. In this recovery, average growth in the first quarter of the year has been well below the average of the other three quarters, leading to some doubts about the quality of the seasonal adjustment. Looking ahead, the government will introduce two new gauges with the annual benchmark revisions in late July.

Economic activity has strong seasonal patterns related to the weather, the school year, and holiday shopping. Estimates of Gross Domestic Product are adjusted for seasonal differences, or rather, their components are adjusted (usually by the agency providing the source data). By design, seasonally adjusted data should not display signs of seasonal variation (that is, there should be no residual seasonality).

Clearly, first quarter GDP growth in recent years has been lower, but is that truly significant? Economists at the Fed’s Board of Governors say no. Economists at the San Francisco Fed say yes, and properly adjusted, GDP growth for 1Q15 would have been 1.8%, rather than the 0.2% reported in the advance estimate. Yet, any statistician can tell you, five observations are not enough on which to base any meaningful analysis. In other words, nobody knows. Post-recession seasonal patterns may have changed. The housing collapse and mortgage debt overhang could have led to permanent changes in spending habits. Financial deleveraging may have led to longer-term distortions in the credit system. We won’t know for sure until a lot more time has passed. The government does alter the seasonal adjustment over time. However, seasonal adjustment problems will balance out over the course of the year. One can simply look at year-over-year changes.

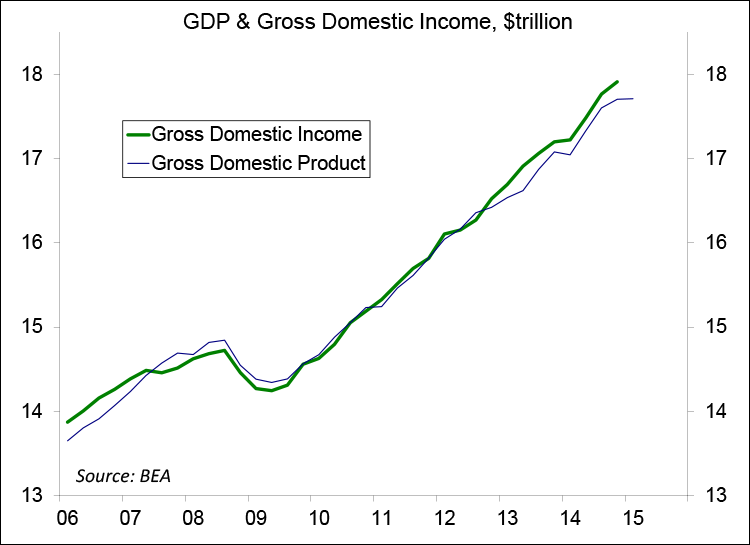

In Econ 1, students learn the aggregate economic activity can be measured as output or income. While most people are familiar with GDP, may are unaware of GDI. These two measures often differ from quarter to quarter and each has its advocates. In July, the Bureau of Economic Analysis will introduce a new measure, which is simply the average of the two.

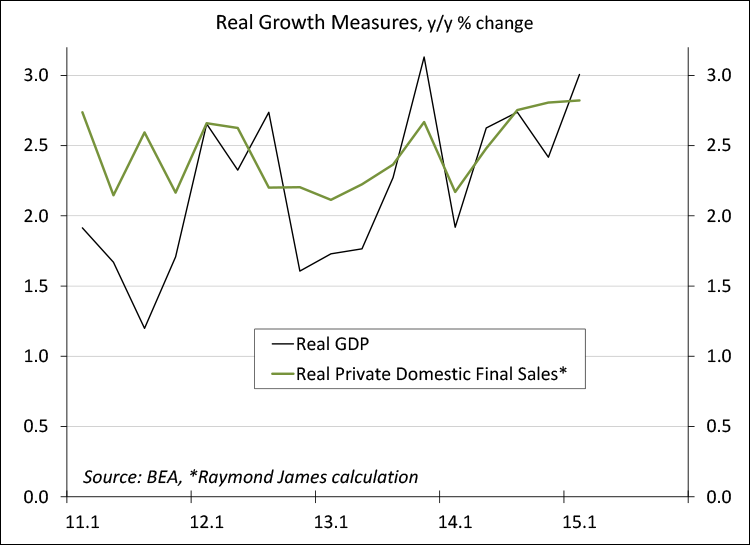

Financial market participants place way too much emphasis on the headline GDP growth figure. Consumer spending and business fixed investment are key, accounting for more than 80% of GDP. However, net exports, the change in inventories, and defense spending account for more than their fair share of volatility and can whip the headline GDP growth figure around from quarter to quarter. In July, the BEA will introduce Final Sales to Private Domestic Purchases, which will be a better gauge of underlying demand and be a lot less choppy than GDP.

Questions about the seasonality of GDP growth help highlight the fact that investors should consider the broad range of economic data, not just one figure.