One of the most common mistakes that I see common stock investors make is failing to formulate the important distinction between a company and its publicly traded stock. There are many great companies out there with fabulous stories surrounding their wonderful businesses. As a result, it can be very easy to fall so much in love with a great company that you can’t resist investing in the stock even when the valuation is extreme.

Often when a company’s business is doing well, its stock becomes popular with investors. Pundits tend to like popular stocks and often write glowing reports and reviews about the company and how well its business is doing. Ironically, for the most part what is written about the business itself may be true and accurate. Writers will talk about things like how the company is increasing sales and earnings, how it has low debt and strong cash flows, improving margins and returns on equity or invested capital and the list goes on. And since all these accolades and positives about the business (the company) might actually be true, investors can get quite excited about investing in the company’s stock.

On the other hand, even when business is strong, a company’s stock price can get ahead of its fundamentals. When that happens, no matter how strong the business is, the stock enters the realm of becoming a risky and poor long-term investment opportunity. However, it’s important to acknowledge and understand that when a stock has momentum, its price can continue to run over the shorter term. But eventually, the day of reckoning must, and will, come. When it happens, you don’t want to be the greater fool holding the bag.

Additionally, it is an indisputable fact that the stock market often mis-appraises companies at least over short periods of time. History is full of examples such as the tech bubble that ran from the mid-1990s to 2000 where we saw high profile technology companies trading at obscenely high P/E ratios (valuations) of 200 times earnings or more. And of course, it wasn’t long before the bubble burst and the stock prices of those same high profile tech stocks literally collapsed.

Consequently, I can’t believe the notion that the stock market is efficient, nor do I believe that everything that can be known about a stock is always factored into the price. However, I do believe that the market is continuously seeking efficiency. Therefore, when a stock is being improperly valued based on fundamentals, you can be sure that it will eventually and inevitably move back towards its intrinsic value in the longer run. The exact timing is an unknown, but common sense dictates that nosebleed valuations cannot hold forever.

Finally, the primary reason that it’s important to make the distinction between the company and the stock is actually very straightforward. The operating results generated by the business behind the stock, is something that management has some control over. In contrast, the market price that Mr. Market applies to the shares of its stock is not directly controlled by the company’s management. In short, management can run the business poorly or well, but they have virtually no control over the stock market and the price (or value) it places on their shares.

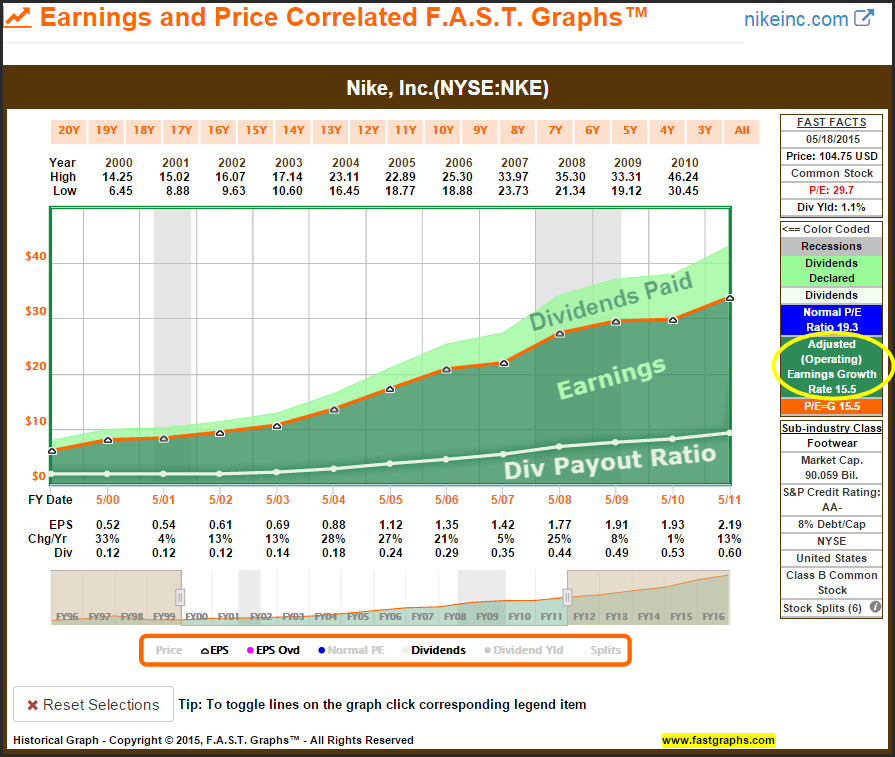

Nike’s Exceptional Operating History

As the following earnings and dividends F.A.S.T. Graphs™ on Nike for fiscal years 2000-2010 vividly reveals, Nike the business performed exceptionally well. Earnings growth was very reliable and consistent, and averaged over 15% per annum. Nike’s dividend over that time frame also followed suit, averaging 15% growth and a similar compound annual growth rate (CAGR) of 14.5%.

The above graph clearly supports the undeniable reality that Nike was a wonderful and superbly run business over this timeframe. Importantly, Mr. Market recognized Nike’s superior business results to the extent that it was willing to generally apply an above average valuation to their shares. As the following graph depicts it was quite common to see Nike trading at a P/E multiple of 19-20 (normal P/E ratio of 19.3, depicted by the blue line on the graph) or higher over this timeframe. I refer to this as a “quality premium valuation,” and Nike has historically been a quintessential example, and arguably deservedly so.

However, the same graph also reveals short periods of time when Nike’s stock price was valued below its normal premium, and conversely, short periods when it was priced higher than its normal premium. This offers clear evidence that the market has not always been efficiently pricing Nike shares.

Lessons on Valuation

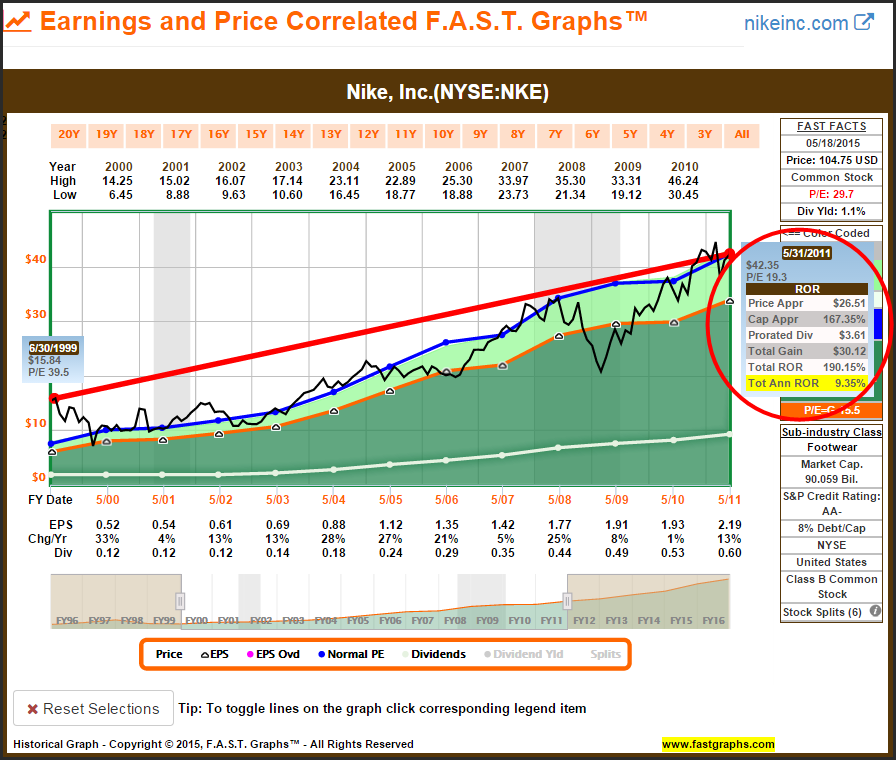

By taking advantage of the return calculation functionality of F.A.S.T. Graphs™ we can run calculations and then analyze and evaluate the impact that valuation has had on long-term returns. With my first example I calculate the long-term performance when investing in Nike at the very beginning of the timeframe and at the highest valuation that the stock traded at over this period of time.

Here we discover something quite remarkable. Even if you invested in Nike at its worst possible valuation, you would have still achieved very attractive long-term returns exceeding 9% per annum. This calculation suggests that within reason you cannot overpay for a great business and lose money, as long as you’re willing to hold it long enough. On the other hand, few investors can show such fortitude once the company’s stock price starts falling, as it did from the summer of 1999 to the spring of 2000 in the case of Nike. That kind of stock behavior will typically cause most investors to turn an unrealized loss into a realized one by selling out.

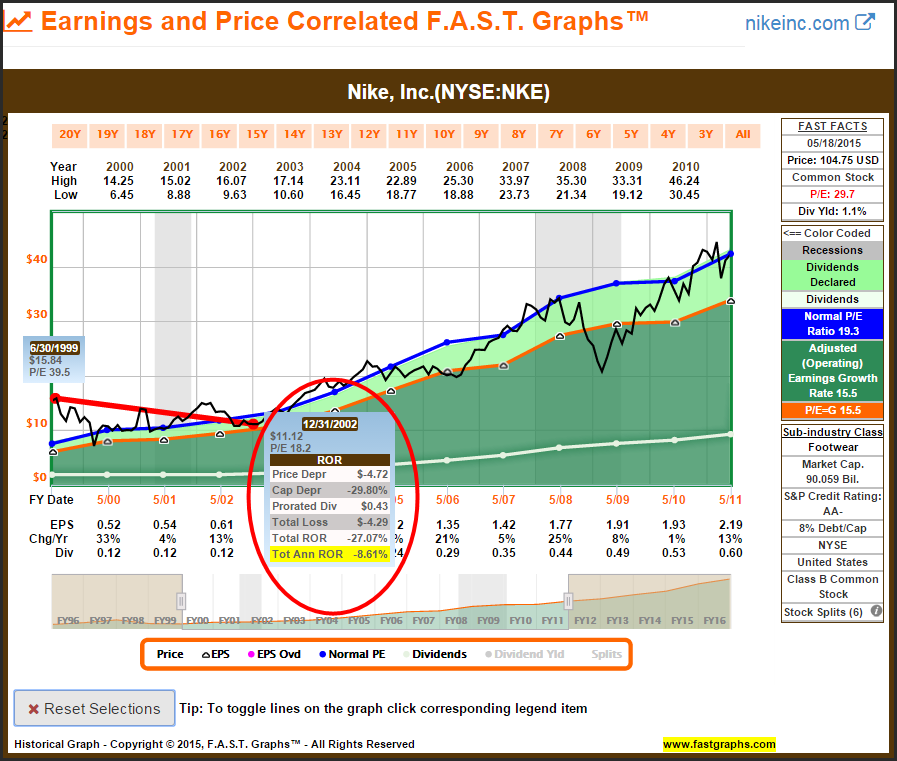

On the other hand, with this next calculation I again purchase Nike at its highest valuation, but this time I run my calculation only out to calendar year-end 2002. That is more than three calendar years later, and up to that time buy-and-hold investors would have suffered a 27% loss of principal or a total loss of 8.61% annually. This calculation adds further support to the question: Would investors be willing to continue holding Nike after suffering such extended losses over such an extended period of time in order to eventually achieve the long-term returns depicted above? Personally, I doubt that many would.

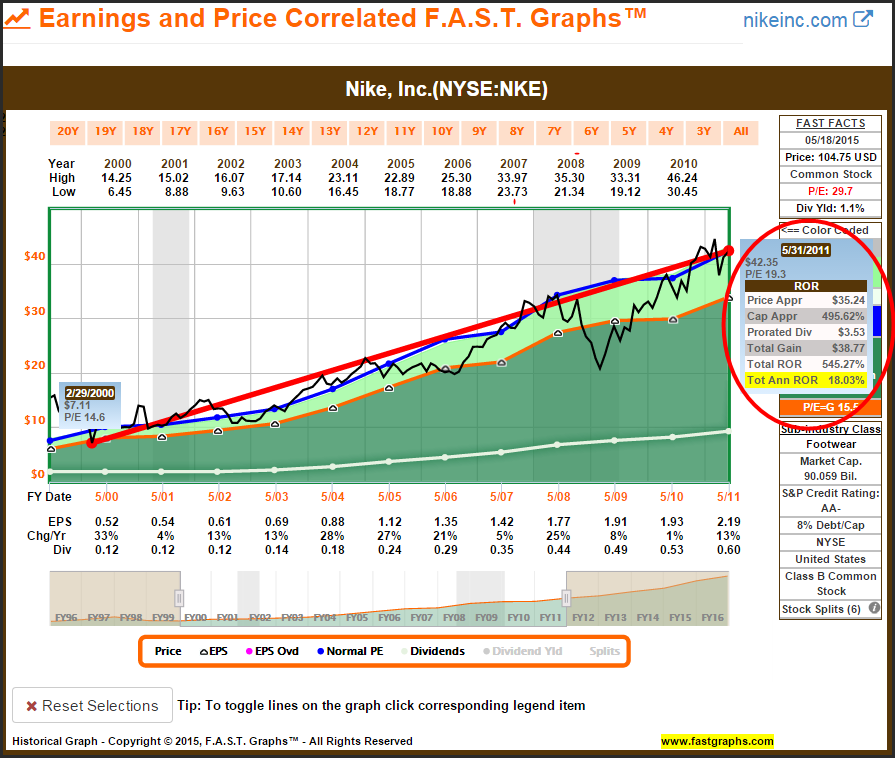

With my next example I calculate the returns that a patient investor that was only prudently willing to invest when fair value was manifest would have achieved. In this case, the prudent investor would only have had to wait approximately 7 months to find this superb company trading at fair value (the price touching the orange earnings justified valuation line).

What’s truly fascinating about this is the reality that doing so would double the compound annual long-term return from approximately 9% to 18%. Even more interesting is the fact that this prudent behavior would have only caused this investor to miss out on less than a dime’s worth of total dividends per share over the long run. And of course, they would have been saved from the more than three years of angst and worry caused by the falling stock price reverting to the fair valuation mean.

I believe this analysis clearly supports and validates not only the importance, but the great benefits of paying attention to valuation before investing in stocks. Succinctly stated, valuation matters a lot.

What If Anything Has Changed to Justify Nike’s Current Valuation?

What If Anything Has Changed to Justify Nike’s Current Valuation?

With this next earnings and price correlated graph I extend the timeframe to current time. Here we immediately are presented with vivid evidence that Nike’s stock valuation has changed dramatically starting in the spring of 2013 (red circle). Since that time, Nike’s valuation has greatly exceeded the long-term historical normal valuation that the market had previously applied (the dark blue line on the graph). To me, this immediately poses a vitally important question. What if anything about the business has changed to justify Nike’s current valuation?

Let’s examine the facts to see if this higher valuation is justified. If this higher valuation is justified it would be logical to assume that we would see significantly accelerated improvements in important fundamentals. For example, we should expect to see rapidly increasing revenues, earnings and/or dividend growth - to name just a few important fundamental metrics. Common sense dictates that there must be some important and powerful fundamental catalyst to support Nike’s higher valuations.

Importantly, if there hasn’t been any material improvement or change with Nike’s fundamentals, then we must assume that the market has been recently improperly valuing the stock. If that is the case, then we can also further assume that Nike’s elevated stock price is emotionally driven rather than fundamentally based. The problem with emotionally driven valuations is that they can be quite fickle, whereas fundamental values are more permanent and reliable. Therefore, let’s examine some of the important underlying fundamentals to see if we can see any significant improvements.

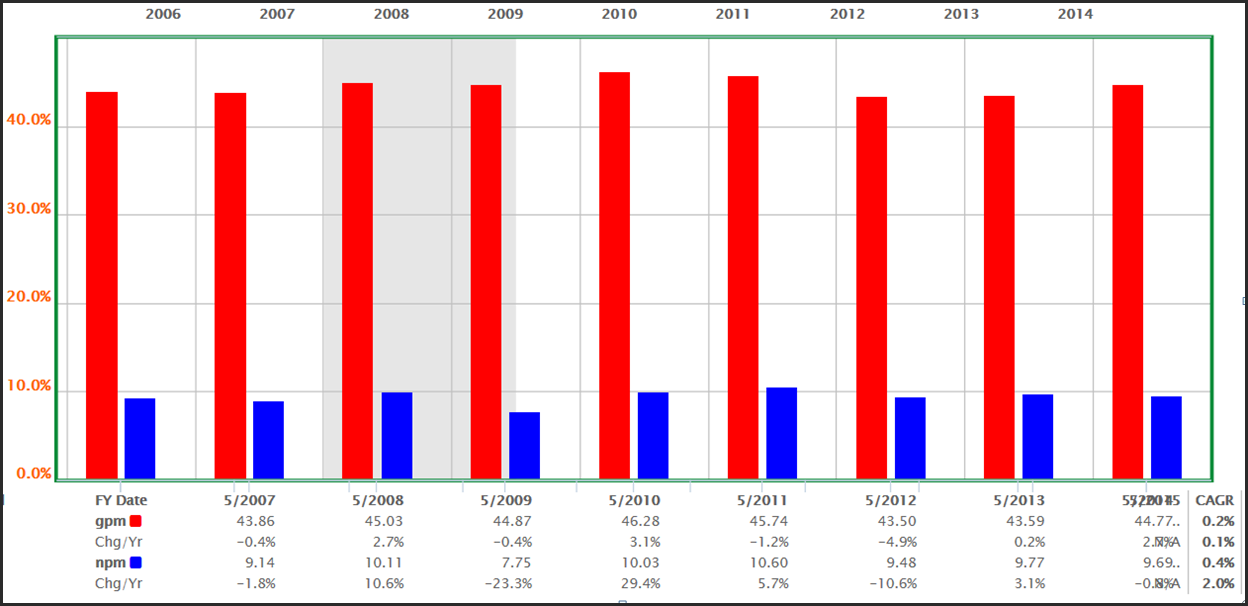

Gross Profit Margin/Net Profit Margin

Utilizing the soon-to-be-launched new and improved FUN Graphs (fundamental underlying numbers) let’s first examine Nike’s gross (gpm) and net profit margins (npm). Here we see a continuation of operating consistency and excellence, but not much in the way of a major change or improvement.

Return On Equity/Return on Invested Capital

When we examine Nike’s returns on equity (roe) and return on invested capital (roi), we again see great consistency. However, once again there is no abnormal or significant improvement in recent years, just more of the same.

Revenues and Earnings Before Interest and Taxes

Nike’s revenues (rev) continue to increase as they historically have, and revenue growth for fiscal year ending in May, 2014 was strong, but again nothing unusual for this great company.

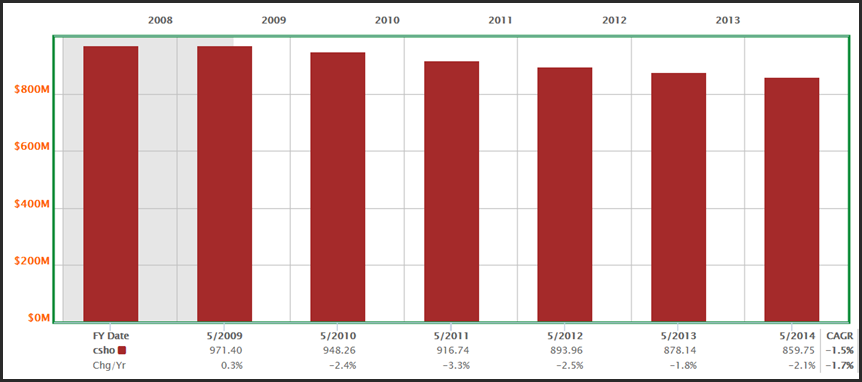

Share Buyback Activity

There is one fundamental that I consider a negative, and that is Nike’s recent share buyback activity. As I indicated in my recent article, share buybacks can be a good thing when stock valuations are low, and they can be a bad thing when valuations are high, as they clearly are with Nike today. Consequently, I find Nike’s recent share buyback activity a concern. Reducing common shares outstanding (csho) with Nike’s stock valuation so high could lead to a future destruction in shareholder capital.

Future Expectations for Nike’s Earnings

Next, let’s examine Nike’s recent past and potential future earnings growth to see if we can find anything about Nike’s operating results that have made the company so much more valuable. I am confident that earnings growth is one of the most important drivers of long-term results, and the above graphics correlating Nike’s historical earnings and price relationship validate my confidence. In the long run, price follows earnings. More importantly, the historical rate of change of earnings growth is the primary long-term determinant of total return.

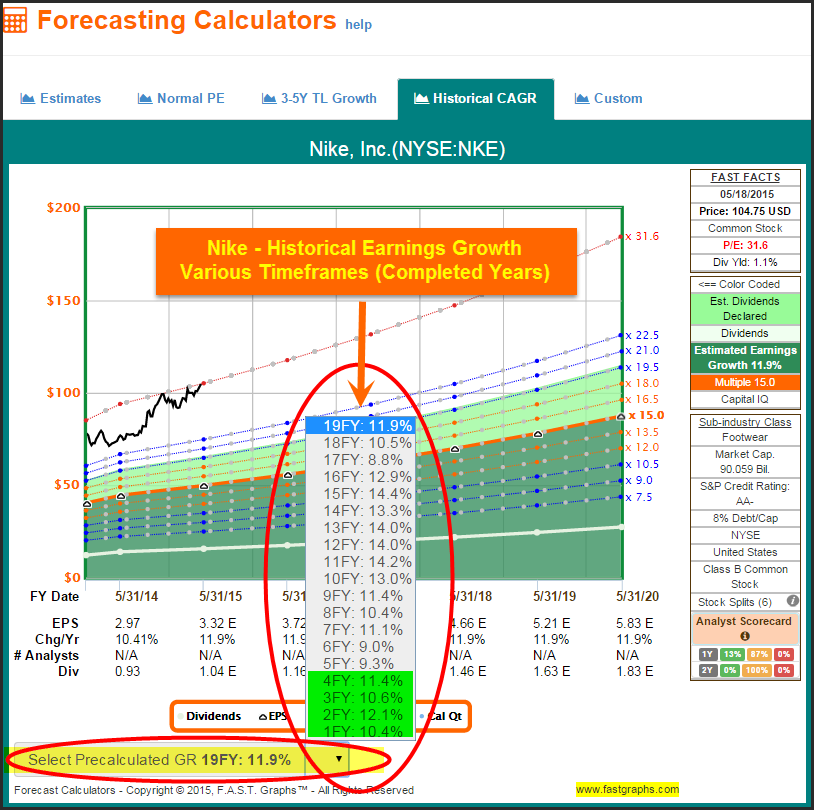

Utilizing the “Select Pre-calculated GR” (historical earnings growth rates) drop-down on the F.A.S.T. Graphs™ Historical CAGR (compound annual growth rate) forecasting calculator we can easily and quickly review Nike’s historical earnings growth rates over every period of time going back 19 years.

As we analyze Nike’s historical earnings growth rate achievements, we discover that Nike’s earnings growth rates over recent periods of time have moderately decelerated (see highlights) rather than accelerated. Nothing alarming, and recent growth has still been quite good, but no obvious catalyst or significant improvement to support Nike’s current higher valuation.

Consensus Analyst Estimates

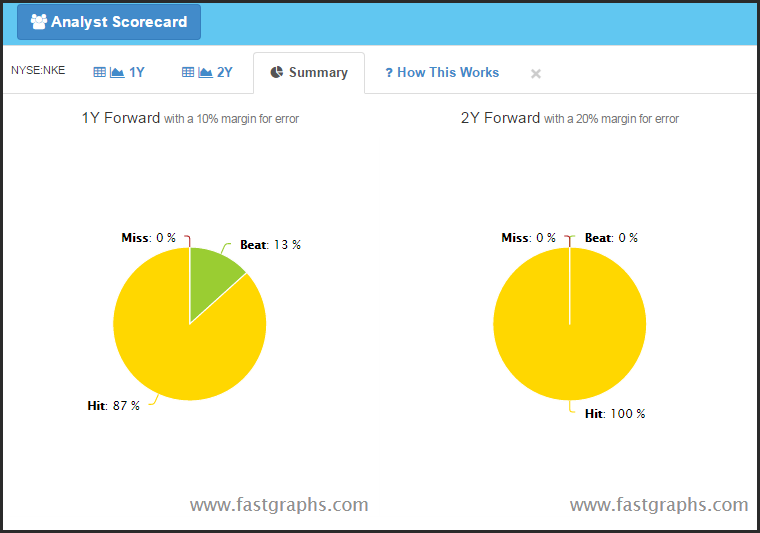

Utilizing the F.A.S.T. Graphs™ “Analyst Scorecard” we discover that the record of analysts’ forecasts one year forward and two year forward over the past two decades on Nike have been exceptional. Nike has either beat or met consensus estimates virtually 100% of the time. Consequently, as we next examine future analyst estimates, we can have some confidence that the estimates may be reasonably reliable.

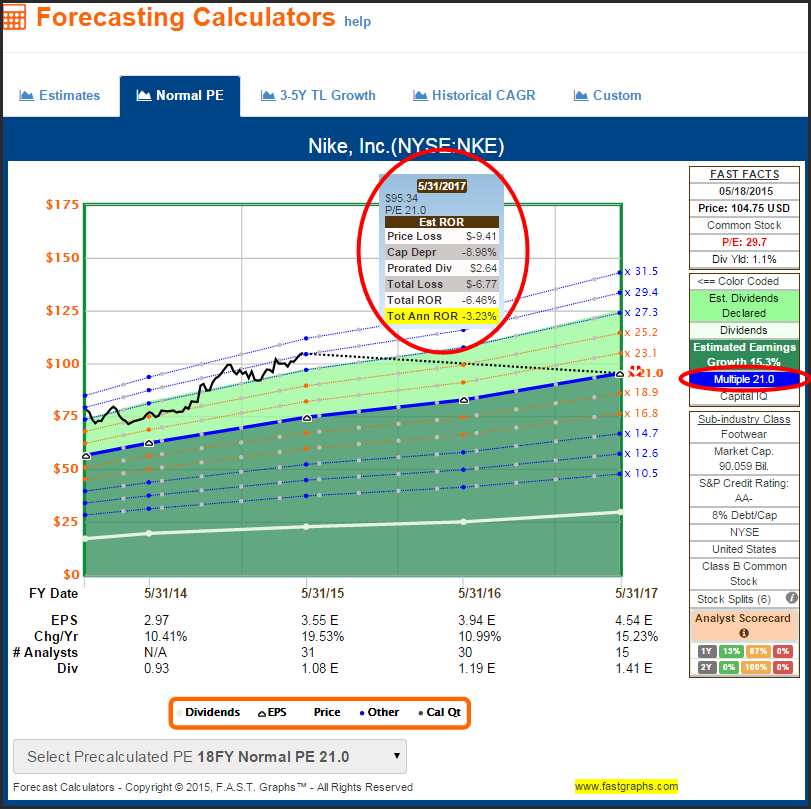

The consensus of leading analysts reporting on Nike to S&P Capital IQ expect average estimated earnings growth of 15.3% out to fiscal year-end 5/31/2017. This is a strong growth rate and slightly in excess of its recent historical average growth rates. However, if Nike were to trade at an earnings justified fair value P/E of 15.3 (P/E = earnings growth) the annual rate of loss would be almost 17% (16.76% see red circle). This represents the potential risk of holding Nike at such an elevated valuation.

Based on the same consensus earnings estimates, but assuming that Nike is awarded its normal historical quality premium valuation (P/E = 21, the dark blue line on the graph), shareholders would still be exposed to a potential annualized loss of 3.23%. Both this estimate and the one above illustrate the potential risk of holding Nike at its current high valuation.

Summary and Conclusions

Nike is and has been one of my favorite companies for a very long time. However, as a stickler for fair valuation, I have had few opportunities to find the stock at fair value. Although I don’t own Nike today, I did have the good fortune to invest in it when I found it at fair value (P/E ratio 15) in February, 2006. I held the stock until October, 2010 and enjoyed a total annual rate of return of 16%.

Nevertheless, even though Nike had only moved back to its historical normal P/E ratio of 20, like most investors the trauma from the Great Recession of 2008 was still fresh in my mind. Therefore, I was of the mindset to de-risk my stock investments. As a result, I took my excellent profits and looked for alternative high-quality dividend growth stocks with better current yields and lower valuations.

Fortunately, I found NextEra Energy (NEE) available at a P/E ratio below 13 with a current yield above 3%. Therefore, I traded my Nike with its P/E ratio of 20 and a 1.5% dividend yield for NextEra Energy. Of course, Nike has continued to advance since I sold out, and therefore, one could argue that I left a lot of money on the table.

However, my replacement investment into NextEra Energy has also performed well and only slightly less than had I held onto my Nike. On the other hand, I also believe I took a lot less risk and received a significantly higher dividend than I would have gotten with Nike. Therefore, I don’t consider selling Nike a mistake, especially considering its current high valuation.

The moral of the story is simple and straightforward. Nike is unquestionably a great company, has been for some time and probably will continue to be so in the future. However, since price is what you pay and value is what you get, I don’t believe that the stock is a good investment at current levels. As investors, it’s important to separate the company from the stock. A great company can be a risky and even a poor investment if valuation is too high, as I believe it currently is with Nike.

Disclosure: No position at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.