The data reports for April suggest that the second quarter’s anticipated rebound from a weak 1Q15 will fall far short of expectations. We could get revisions, figures for May and June could be a lot stronger, but at face value, the economy has disappointed. However, the Fed is still on track to begin raising short-term interest rates later this year. We should come away with a better understanding of how the Fed sees the situation when the central bank’s two top officials speak later this week.

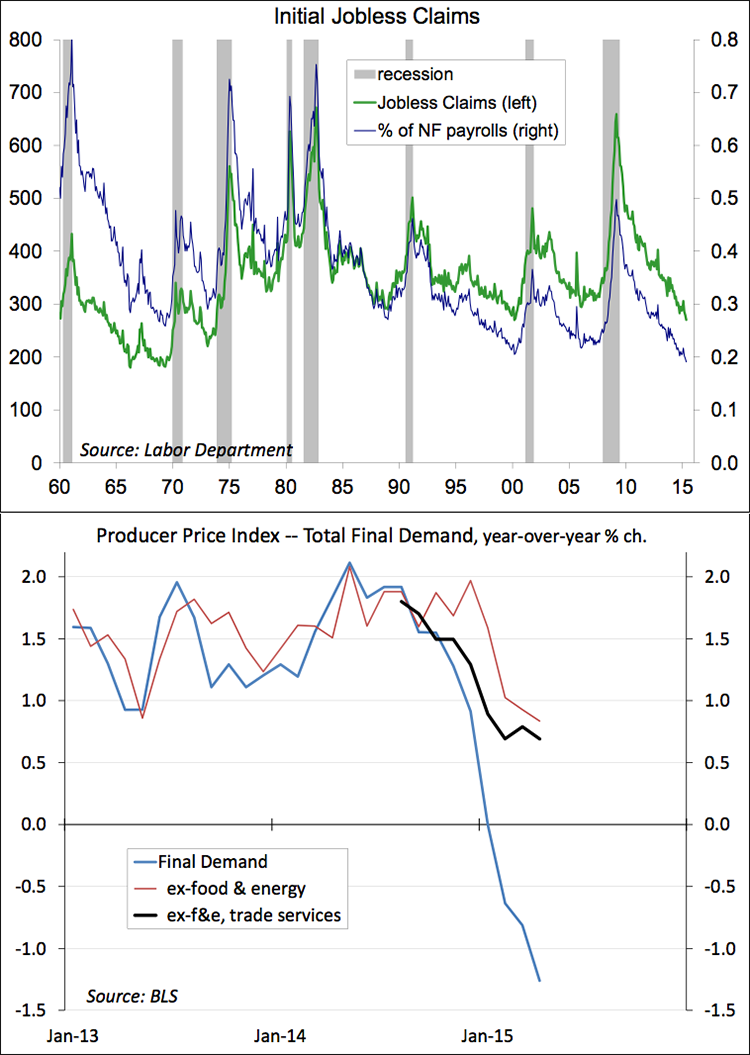

Not all of the news is bad. Weekly claims for unemployment benefits have been trending at a remarkably low level in early May. It’s hard to dismiss the low trend as being due to seasonal adjustment difficulties (which aren’t much of an issue in May). Jobless claims are near at a record low as a percentage of nonfarm payrolls. Yet, job losses really haven’t been an issue in recent years. The real concern is job creation. Recent data suggest that hiring at small and medium-sized firms is still going strong. However, hiring at large firms has slowed to a crawl. The key question is whether that’s temporary.

April consumer price figures will be reported at the end of the week. However, the Producer Price Index and the report on import prices suggest continued disinflationary pressures. There’s very little inflation in “stuff.” Inflation in consumer services is running at a moderate pace. Although there were some supply-chain disruptions related to delays at West Coast ports, manufacturers are generally not seeing the type of bottleneck production pressures that would push inflation higher. Of course, the labor market is the widest channel for inflation pressure. While wage increases have remained relatively lackluster, a decrease in productivity has contributed to an increase in unit labor costs (the labor expense per unit of output). Productivity figures are often erratic and unreliable, but weak productivity growth is a major concern. If firms can’t pass higher unit labor costs along, they will eat into corporate profits. Uncertainties in the productivity outlook, here and abroad, are unlikely to be settled anytime soon.

Where does this leave the Fed? In its April 29 policy statement, the Federal Open Market Committees recognized that the economy slowed in the first quarter, but it pinned that on “transitory factors.” In other words, officials viewed the first quarter softness as temporary. The data reports that have arrived since then (a drop in unit auto sales, soft retail sales, disappointing industrial production, and declining consumer sentiment) point to a subpar pickup for the economy in April and GDP growth in the second quarter is likely to be a lot softer than was anticipated at the time of the Fed policy meeting.

Despite disappointing growth in the first half of the year, Fed officials are still likely to expect conditions that will warrant an initial hike in short-term interest rates later this year. Why would the Fed tighten? The focus is on the job market. We are likely to see more slack taken up in the months ahead. The Fed has to consider where the economy will be 12 to 18 months from now. Monetary policy will still be very accommodative even after the first few rate hikes. There’s no need for the Fed to hit the brakes, but officials do need to take the foot off the gas at some point. Still, Fed officials have emphasized that the pace of tightening after the first rate increase is a lot more important than the timing of the initial move. Fed officials have indicated that that pace will be very gradual.

Later this week, we should gain a lot more insight into how the Fed sees things. Vice Chair Fischer will speak on the euro area on Thursday (some implications for long-term interest rates and exchange rates). On Friday afternoon, Fed Chair Yellen will speak on the economic outlook. Market participants may eye an early exit ahead of a three-day weekend, but Yellen should provide an up-to-date view of how the Fed sees things.

RIP B.B. King – The thrill, indeed, is gone.