Recent economic data reports have reflected a slowdown in growth, but they are not disastrous. The economy continues to improve, but not so much that the Fed will rush to take away the punch bowl. That’s good news for the financial markets.

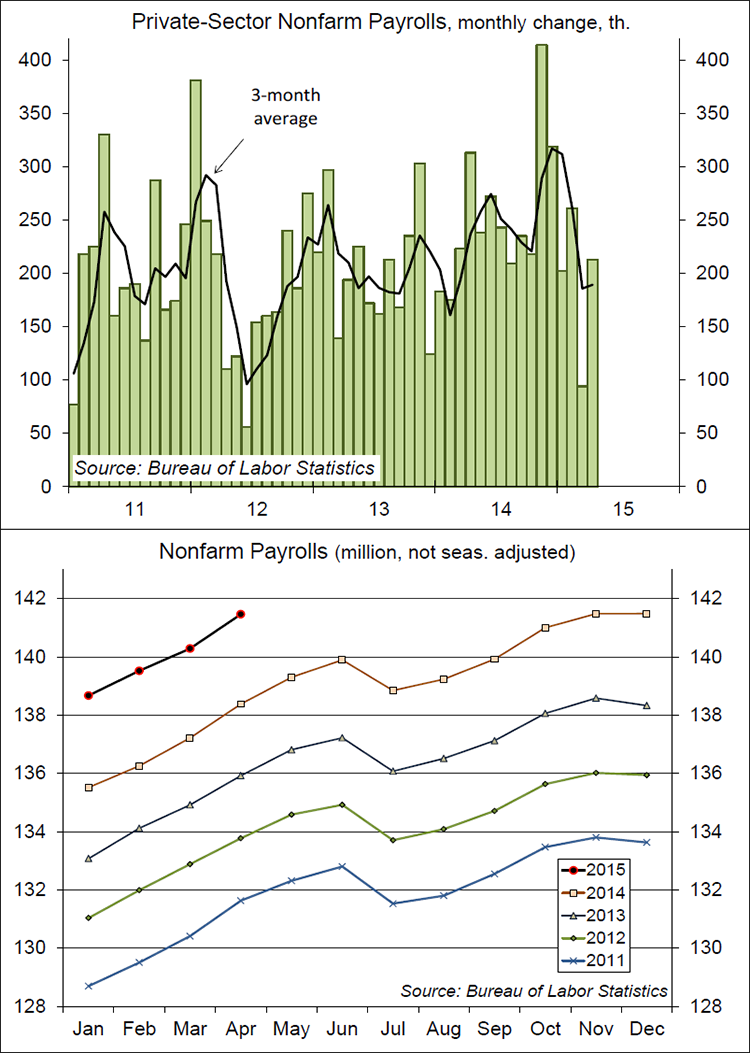

Nonfarm payrolls rose about as expected in the initial estimate for April, but figures for the two previous months were revised down. We know that the subpar payroll figure for March was a weather story. The employment report is made up of two separate surveys, one of establishments and one of households. In February, the establishment survey largely missed the major snowstorms, but bad weather hit the March survey period head on. The household survey details showed a larger-than-usual number of people who could not get to work due to the weather. Granted, the employment report’s two surveys are not directly comparable, but they give you a good idea on the weather impact. The April payroll increase largely reflected a rebound from bad weather. The average gain for the two months was 154,000 – a moderate pace.

The unadjusted figures were in line with the usual pattern. The U.S. added 1.178 million jobs in April (before seasonal adjustment), vs. 1.163 million in April 2014. The level of unadjusted payrolls is trending sharply higher relative to a year ago (private-sector jobs are up 2.6% y/y). Still, the underlying trend in seasonally adjusted payrolls has moderated. The ADP estimate shows a sharp slowing in hiring at large firms in March and April, while job gains at small and medium-sized firms have remained relatively strong. This is a contrast to the earlier years of the recovery, when large firms prospered and smaller firms struggled to improve. The gains at small firms are an important signal of a broadening recovery. The softness at larger firms likely reflects the transitional impact of a strong dollar.

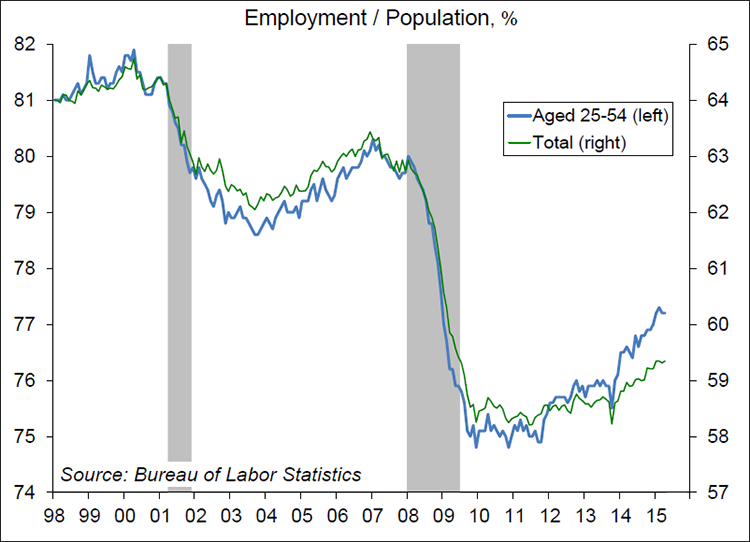

For Fed policymakers, the key issue is the amount of slack in the job market. The unemployment rate was 5.4% in April, essentially unchanged from March and down from 6.3% a year ago. However, the employment/population ratio held steady at 59.3%, up only gradually over the last year. Improvement here is more concentrated in the key age cohort (those aged 25-54), but that should broaden to teenagers and young adults over time. Average hourly earnings rose modestly in April, with the year-over-year pace remaining at a lackluster 2.2%. The continued lack of better wage growth is taken as a sign of slack.

The range of recent economic data reports is consistent with a temporary slowdown in growth. The pace should improve as the first quarter’s restraining factors (weather, West Coast port delays, the energy contraction, and the stronger dollar) wane, but some restraints have continued into 2Q15. As a consequence, the 2015 economic outlook appears softer and we’re back to “more of the same.” That is, we’re still on the road to economic recovery. We’ve made a lot of progress, but we’re nowhere near where we need to be. The continuation of this backdrop should be taken well by the financial markets.