“Everyone has to think about what will happen to their wealth when interest rates change direction.”

– Peter Briger, CEO and Co-CIO of Fortress Investment Group

“By 2020, 70% of assets will be held by retirees and pre-retirees.”

– Salim Ramji, BlackRock’s Global Head of Corporate Strategy

Place those two quotes front of mind. The primary need of investors is shifting and the risk dynamics has changed. Gone are those wonderful defined benefit plans. This is the first generation of retirees retiring with control of their financial assets. That’s good news for your advisory business, yet, with zero bond rates and 10-year forward returns for equities in the 2% to 4% range, the challenges loom large.

The 65 year old is less concerned with performance relative to the S&P than the 45 year old. Income generation and capital preservation prevails. The number one question for many investors will be: how to generate a steady amount of income?

Several weeks back I attended an ETF Strategist event hosted by BlackRock. The 70% data came from that conference. BlackRock suggested that advisors focus on creating outcomes that provide income generation, capital preservation and inflation protection. I agree and, reflecting on the quote above, “everyone has to think about what will happen to their wealth when interest rates change direction.” Indeed. I see two outcomes: one good, one bad. It comes down to planning, client education and positioning.

So today, let’s continue the discussion started last week as I share with you more of my notes from the Strategic Investment Conference. Gundlach’s view is rates likely bottomed. There was much agreement on a coming corporate default wave. India was a common positive investment theme. I hope you find the information valuable and helpful in your work with clients.

Before we jump in, as a quick aside, high yield debt has been front and center in the news lately. This is a space I have particular expertise. As a follow-up to a piece I wrote for Forbes titled, Junk Bonds Are The Investment Opportunity Of A Lifetime, Just Not Yet. I’m going to present some ideas on May 20 on how to position high yield in your portfolio to both participate in further gains and risk protect in a way that puts you in the favorable position to take advantage of a coming once in a lifetime buying opportunity. I believe it presents within the next few years.

Included in this week’s On My Radar:

- Jim Bianco, President of Bianco Research

- Jeffrey Gundlach, CEO and CIO of DoubleLine

- Ian Bremmer, President of Eurasia Group

Jim Bianco

Jim began his presentation with a quote from the great Charlie Munger:

“I’m convinced that everything that’s important in investing is counter intuitive and everything that is obvious is wrong.”

This quote sets me off on a short detour. No wonder it is so hard at times to work with individual investors. A long-time client (with me since 1985) called last week with several hundred thousand to invest. He told me how his friend is making a killing in dividend stocks and he wants to get into something that will make him big money. It’s obvious to my long-time friend that it is time to buy into stocks. I sense return envy and a market top. Thirty years and far too many knocks on the head tells me I’ve seen this story before. Risk is high.

Advisors are telling me about how tough the calls are today – everyone comparing their broadly diversified portfolios to the S&P 500. Investor or speculator? Which one does the client want to be? Can’t be both and few are good at the latter.

Ok – back on track. Here are some of the notes that struck me as important from Jim’s presentation:

- He is not in the recession camp, not in the growth camp but in the “below average camp”

- A “C” grade at best for corporate revenues and earnings. Nothing great

- Today, even forward PE is high at 17. Not good when you are getting a decline in earnings and revenues

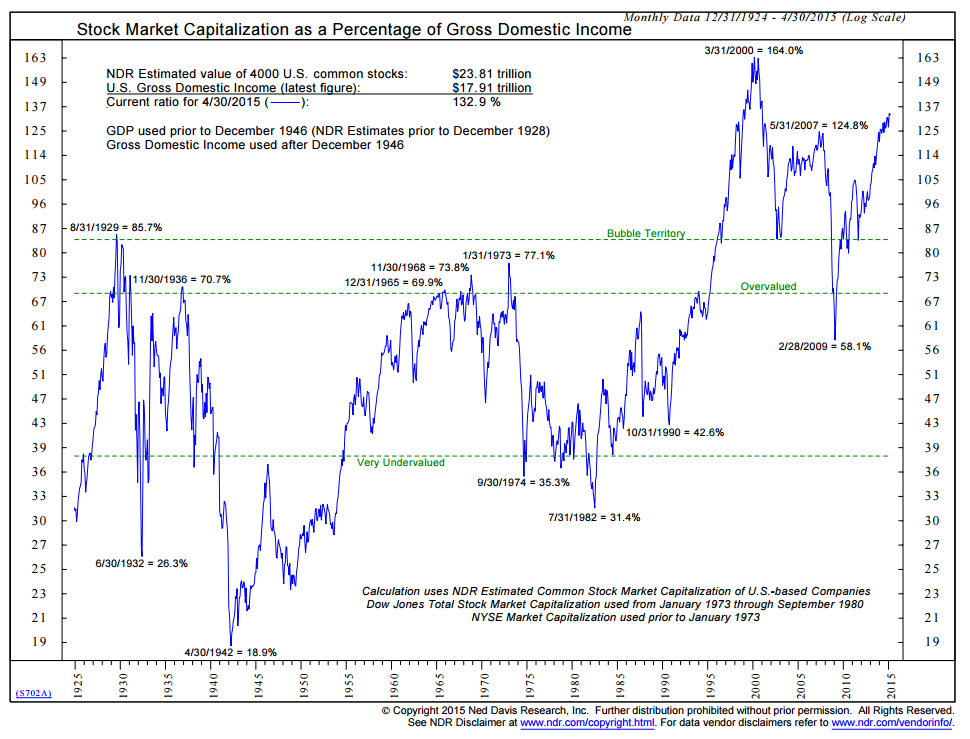

- Warren Buffett’s valuation measure, stock market cap as a percentage of Gross Domestic Income, near 140% is very high

- 1974-2008 real GDP tracked CBO’s (Congressional Budget Office) real potential GDP

- 2008-present there is a big gap between the real number and CBO’s estimate

- Something is holding back the economy

- QE might be the problem and not the solution

- Jim is telling Fed officials to raise rates now

- He believes that the Fed’s third mandate is investment market stability (SB here: Munger’s quote echoes in my head)

- Jim’s personal interpretation of the Fed’s duel mandate, forget just inflation and employment, he believes it is, “everything and whether the market throws a fit when the Fed acts”

- This is a meaningful point in my view: Jim stated that “the Fed funds futures chart shows that the market has not priced in a higher Fed rate move this year.” It will be a shock to the system if we get one.

- To this point he added, “as long as there is a gap between market expectation (the Fed funds futures level) and the Fed’s projection of rates (dot plot) the Fed won’t raise rates

- Jim restated the Fed’s third silent mandate – investment market stability

- The market is moving further away from a rate hike, not expecting one soon

- On oil: we are producing too much relative to demand and said that demand from oil ETFs like “USO” has supported oil futures prices

- He believes market participants see $100 oil again. Too many speculative bulls out there… no wall of worry – don’t buy oil (he suggests)

- There is roughly $40 billion lined up waiting to buy distressed energy companies

- Saudis see opportunity to step on the gas and break the back of the frackers

Ian Bremmer on the Geopolitical Environment

Ian is one of my favorite geopolitical analysts. I’ve followed him for years and enjoy his direct and candid view. Here are some of my notes from his presentation:

- He and his team see “unstable and they see dangerous”

- There are more refugees than at any point since WWII

- Dealing with a well-funded ISIS and growing Al Qaeda strength

- The world is experiencing geopolitical destruction. It is going to get worse

- Why is this happening: America is a large part of the reason why

- We do not want to step up for our allies like we have in the past

- Ask any American ally what they think about our foreign policy – you won’t get good answers (even from Canada)

- Europeans are another big part of the why

- The Brits put up the Heisman to us on the China Bank

- Not many noticed that the Netherlands hired a Chinese company (one led by China’s military) to build out their internet infrastructure (SB again – NSA fallout. )

- Russia is a part of the why

- First to be clear, Russia is in decline

- Putin won’t change his path. We are hitting him, his oligarchs, planes, apartments and bank accounts

- If there is a black swan out there, it is Putin showing us not to mess with him. Something big.

- We are going to see a much more assertive Russia

- S. has shown very little thinking around this

- The question is not if but what is Putin going to do?

- Russia in decline creates much more geopolitical instability

- Lastly, the rise of China is a big part of the why

- They are the only country that has a coherent global geopolitical strategy

- Asia Infrastructure Bank, Development Bank and Asia Bank

- It is impossible to look at the Middle East and see anything good

- Saudi’s recent leader change is a message

- No one is more hurt by an Iranian deal than the Saudis

- No more reform. The focus is on security

- They feel that no one is going to help them

- He believes Iran is likely to get a deal done with the U.S. giving it an 80% change

- Noted that Iran has cheated on every inspection. It’s a bad deal, they are going to continue to cheat, but not doing a deal is worse for the U.S. in his view

- Israel is unhappy but will they strike? He says no

- Jim believes the U.S. doesn’t want to do as much in the Middle East. A trend we’ll see more of. It is bad for the Middle East but he’s not so sure it is bad for the U.S. (SB: personally I have a different view)

- Israel and Saudi Arabia know we are pivoting away from the Middle East

- We spent billions on Iraq, made regime change and the country fell apart

- Other places, like Libya, the U.S. didn’t play a key role and the nation fell apart

- He said he has had meetings with every head of state. The biggest problem for the U.S. is our allies don’t trust us – He was consistently asked these key questions:

- What do you guys want?

- Who are you?

- Where do you stand?

- Relative to the geopolitical environment in most of the world, the U.S. looks good

- He believes this favors U.S. investment

- Brazil – corruption is being attacked. He expects that when the current president gets voted out, there will be a favorable investment environment in Brazil

- He is bullish on Asian economies

- Impressed with what Narendra Modi has done in India. Sees big growth

- Buy India. India’s growth has surpassed China’s and will continue to surpass it by a wide margin

- China understands they need to expand fast – there is a strong sense of urgency

- Japan has a strong leader in Abe. Delighted to see a single united government again

- He concluded his remarks by circling back to Russia stating, “if you press the Russians into a corner, Putin is going to bite you.”

On that depressing note, let’s jump to Gundlach.

Jeffrey Gundlach

There are three things Jeffrey won’t sell: He is bullish on India’s stock market (by the way, a consistent theme at the conference), bullish on his absolute return fund and bullish on his hedge fund.

Here are selected notes:

- You have to take risks. He presented on those he believes are worth taking and not taking

- Bonds in Europe are in short supply. The central banks own most of them and the financial institutions must own them. He suggested:

- Not buying negative interest rate yielding bonds is a good idea

- Sovereign debt issuance has turned negative in Japan, UK, Europe and the U.S.

- Fed Policy is on the stage – “Don’t be a block head.” Implying Don’t Fight the Fed

- He noted that the Fed blinked relative to the dollar strength (SB here: I agree and here is what it means in English. If they raised the Fed funds rate, the dollar would have rocketed higher causing a potential major crisis much like the one in 1998. Recall the current estimated $9 trillion in foreign-based U.S. dollar owed debt. A higher dollar means crisis for those borrowers – dollar up 30%, they owe 30% more, up 50%… you get it. So much for those attractive low U.S. interest rates several years ago. The Fed blinked)

- Here is a good one: The market nor the U.S. economy will respond well to a Fed rate hike

- Bond market participants’ probability of a Fed hike?

- 60% say a hike by December

- 30% say by September

- 10% by June

- Gundlach – the Fed will wait for a few consecutive periods of strength

- On currencies: currency trends usually last ten years. The current trend likely started in 2011 or 2008. He believes ultimately the dollar goes higher. Current support is at 93

- Amazing weakness in commodities – not just last summer through today, but last four years to today

- Gold is unchanged over the last four years in dollar terms but doing well in other currencies

- He advises to hold gold

- I felt that one of the more interesting charts showed Core CPI in the U.S. against Core CPI in Europe

- The core CPIs are completely the same if you calculated both using the same inputs (the U.S. has a higher weighting on housing)

- In short, core CPI has declined in both countries from 2011 to present. Very little core inflation at 0.60%. Using the U.S. calculation, core CPI is 1.6% in the U.S. reflecting a bit more inflation but nothing like the 2.5% in 2011 and the trend is down

- He noted that nominal GDP seems to be a great predictor in forecasting interest rates (he favors a seven year moving average) and noted that nominal GDP might just be flattening out which would mean that interest rates will flatten out too

- Some question whether there is manipulation in the CPI data. He noted the Billion Prices Index (something I have written about in the past) showing the high correlation of CPI to that index. The Billion Prices Index scans the internet and tracks actual prices of billions of items. Pretty cool. Anyway, little sign of inflation and prices appear to be in decline

- History shows that every time the Fed tightened the yield curve inverted. (SB – recession has followed every invert). Again, it is flattening now

- Technically it looks like the 10-year Treasury rate has bottomed. The 2-year bottomed in 2011, the 5-year in 2012 and the 10-year at 1.38% in 2012

- He noted that the 10-year could not take out the 1.38% low in January

- The 30-year did take out the 2.45% 2012 low dropping to 2.22% on January 31, 2015; however, we quickly went up to 2.85% then to 2.50% and that rate is now moving higher

- Similar to all of the money that poured into U.S. equities at the top of the market cycle in March 2000 (my comment), January 2015 was the best month ever for inflows into bond funds. A top?

- On high Yield: “everything you know about HY is wrong”

- None of us have experienced a secular rate rise (something that he believes might happen in a few years from now)

- He believes interest rates will rise: first gradually, then suddenly

- If Treasurys go to 8%, then HYs are going to 14%, 16%, 18% or higher

- He doesn’t believe the Fed is tightening soon – so there is some time

- The HY maturity cycle picks up significantly in 2018 – that’s the coming stress point

- Also, the Fed’s refinancing needs are set to balloon in 2018-2019

- He sees a storm coming in 2018-19

- This will become an important theme

It really helps me to hear the views of some bright economists, political analysts and investment managers with true skin in the game. It challenges my thinking and I believe keeps me on my toes. I hope it does the same for you.

A quick note on Kyle Bass. He asked to keep his presentation private. I feel comfortable sharing that he touched on the progress he is making in challenging what he believes to be out of control manipulation by the pharmaceutical industry in regards to patent protection. Did you know that it is illegal for Medicare to negotiate drug prices? I didn’t. Blame both Bush and Obama and a very powerful lobby.

He mentioned that the U.S. could save $300-$700 billion per year over ten years if we paid the same prices Canada now pays for the very same drugs. Even more if we paid what Norway pays. I have not looked into those numbers.

Shorting Bunds might be the “trade of a lifetime”. If you’ve watched what has happened to Bund yields over the last week or so, someone is on the right track. Not so easy to do as the futures markets have their own set of complications. Great timing is required. Ultimately, I think their banks are in trouble but for now I still find myself in the Don’t Fight the Fed and Global Central Banks camp.

A final few notes on the conference. It was outstanding. India and China were central themes. I’m going to do some more research – I’m sure my mother-in-law is looking for a new idea having exited the short Yen trade. I left out other notable presenters: Grant Williams and Raoul Pal (some great ideas on stock selection), Stephanie Pomboy, Paul McCulley, David Zervos from Jeffries. This piece is getting too long so I’ll see if I can weave some central ideas into next week’s piece.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, or the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site.

© CMG Capital Management Group, Inc.

© CMG Capital Management Group