The economy slowed in the first quarter, reflecting a variety of restraints. Most of these should give way, leading to stronger growth in the second quarter. However, Federal Reserve officials and financial market participants will want to see proof.

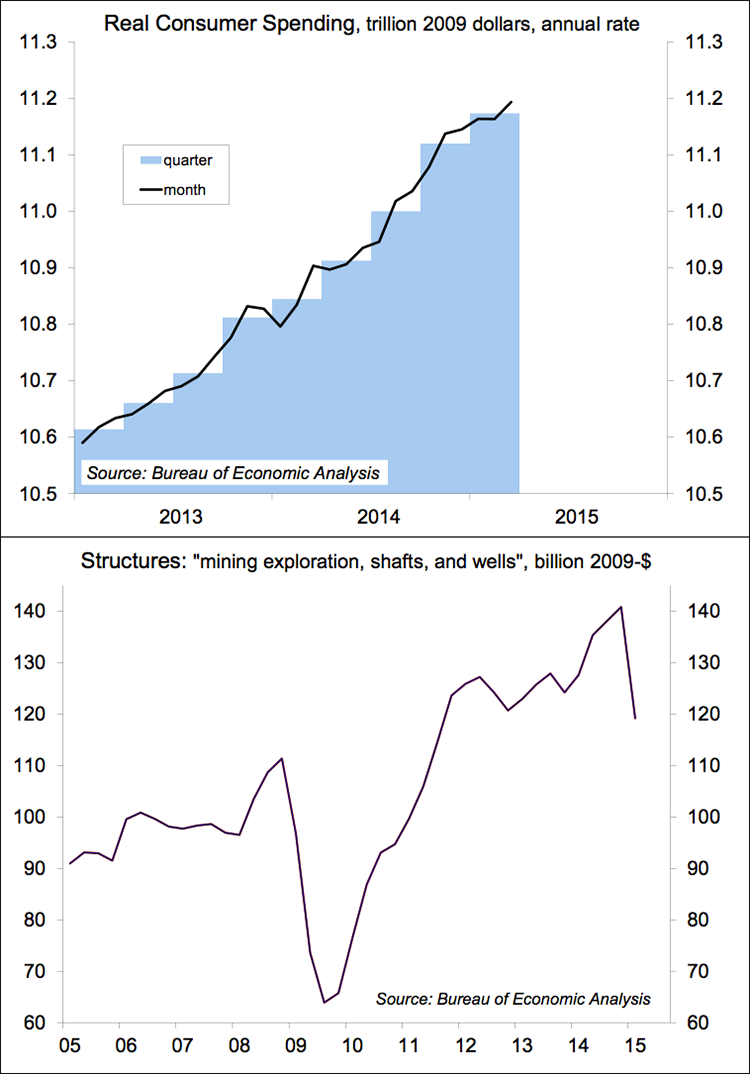

Inflation-adjusted consumer spending, which accounts for 70% of Gross Domestic Product, rose at a 1.9% annual rate in the advance estimate for 1Q15, not bad considering that the 4Q14 pace was +4.4%. Personal income was flat in March, but inflation-adjusted disposable income rose sharply in the quarter, which should provide support for spending in 2Q15.

The contraction in oil and gas drilling pushed investment in business structures lower. These figures will be revised, but they currently suggest more to come in the second quarter.

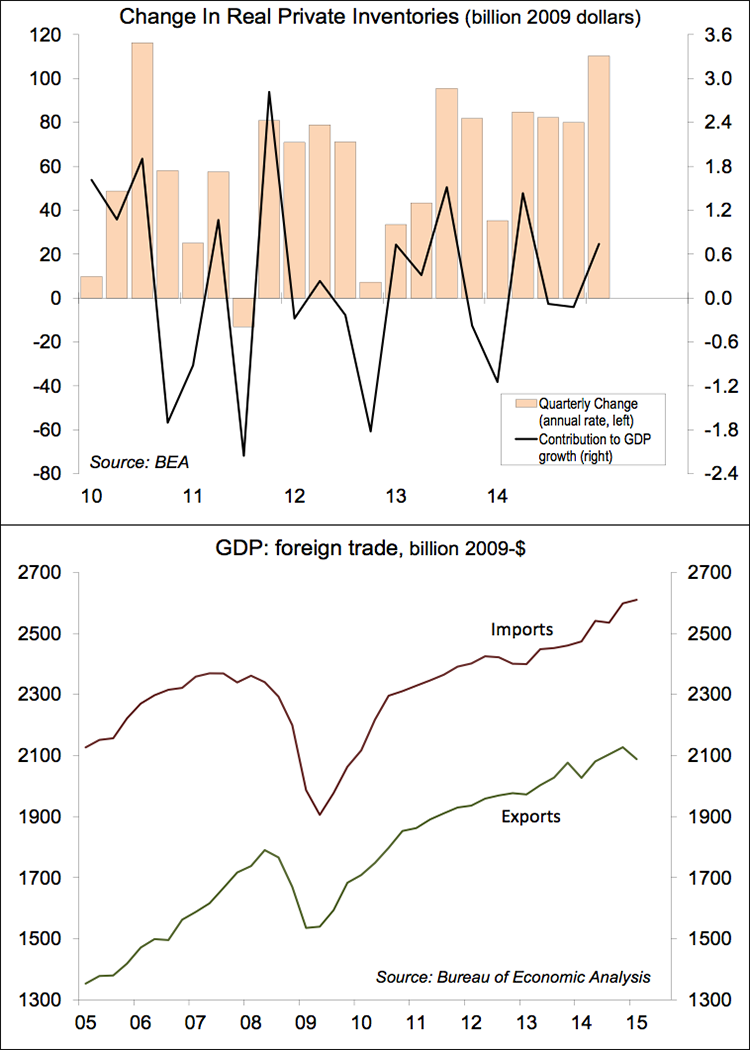

Inventories rose more than expected in 1Q15. While the total may be revised lower, the inventory-to-sale ratio is relatively high and suggests that we may see a correction in production for the second quarter (and a moderate drag on GDP growth).

The stronger dollar had a negative impact on foreign trade in 1Q15. However, West Coast port delays (the impact of which continues to be reported) make it difficult to say how much of the wider trade deficit was due to the dollar, how much was weak growth abroad, and how much was port issues (in addition, the monthly figures are normally choppy). The port delays likely had a bigger impact on imports, which have a negative sign in the GDP calculation.

Putting the pieces together, the data suggest a pickup in consumer spending in 2Q15, but further restraint in business fixed investment, a moderate inventory correction, and a further drag from foreign trade. GDP forecasts for the second quarter ought to be coming down (from early forecasts of 3%+).

In its monetary policy statement, the Federal Open Market Committee recognized the first quarter slowdown, but pinned that on “transitory factors.” That still leaves the Fed on track to begin raising rates later this year. However, officials will want to see evidence of a second quarter pickup in growth and, more importantly, further improvement in labor market conditions.