“Earnings don’t move the overall market; it’s the Federal Reserve board. And whatever you do, focus on the central banks and focus on the movement of liquidity. Most people in the market are looking for earnings and conventional measures. It’s liquidity that moves markets.”

-Stan Druckenmiller

Included in this week’s On My Radar:

- David Rosenberg

- Peter Briger

- Lacy Hunt

David Rosenberg

My notes from David’s presentation:

- We are in the weakest economic growth cycle of all time.

- Working age population growth is vanishing – a big part of the growth story is demographics.

- However, while growth is weak, the expansion is the 6th longest at 69 months.

- The average expansion is approximately 40 months dating back to the year 1857.

- David believes this expansion will exceed the record 120 months expansion in the 1990s citing that even though we are at 69 months, we have lower rates and more capacity to grow.

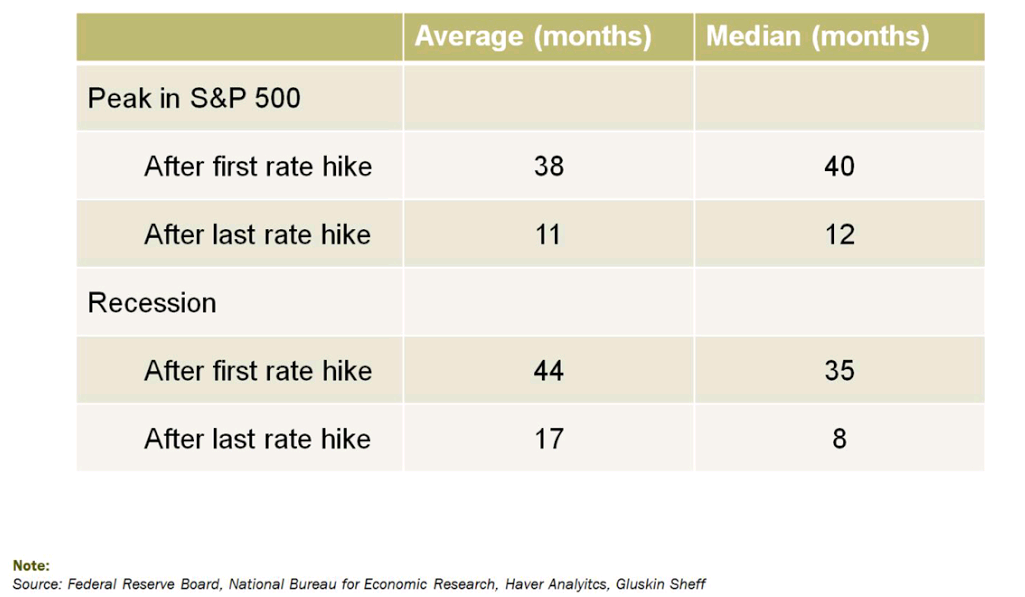

- An important point: Bull Markets and Economic Expansions End after the Tightening Cycle – Not when the Fed begins to tighten. This chart shows the Bull Market’s peak 38 months after the first hike and 11 months after the last. Recession’s begin 44 months after the first and 17 months after the last.

- The Fed rate hike doesn’t bring an end to economic expansion or a bull market.

- It is when the Fed tightens so much that they invert the yield curve and recessions start.

- All the bad stuff happens after the last Fed rate hike.

- This one will end too but may not end until 2018.

- On profit recession discussion: if you strip energy out of the S&P 500, profits are actually up. Energy earnings are down 64%.

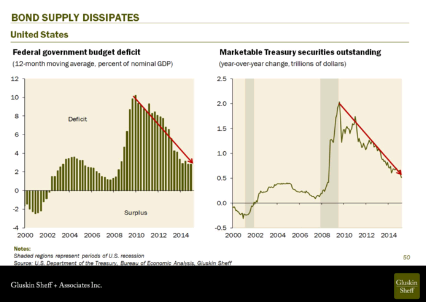

- Central banks are gobbling up the Treasury supply. Note the drop in marketable Treasury securities outstanding from $2 trillion to $700 billion.

- Loved this comment from David – “entities out there are buying bonds because they have to but you don’t. Bonds are unattractive – don’t buy.”

- On deflation – “we don’t have deflation.”

- On inflation – “inflation is running close to 2.5%. There is more inflation beneath the surface than meets the eye.”

- The risk/reward is in stocks – not bonds. Bonds don’t have the coupon protection. The only opportunity is for capital gains and you are buying at extremely low yields.

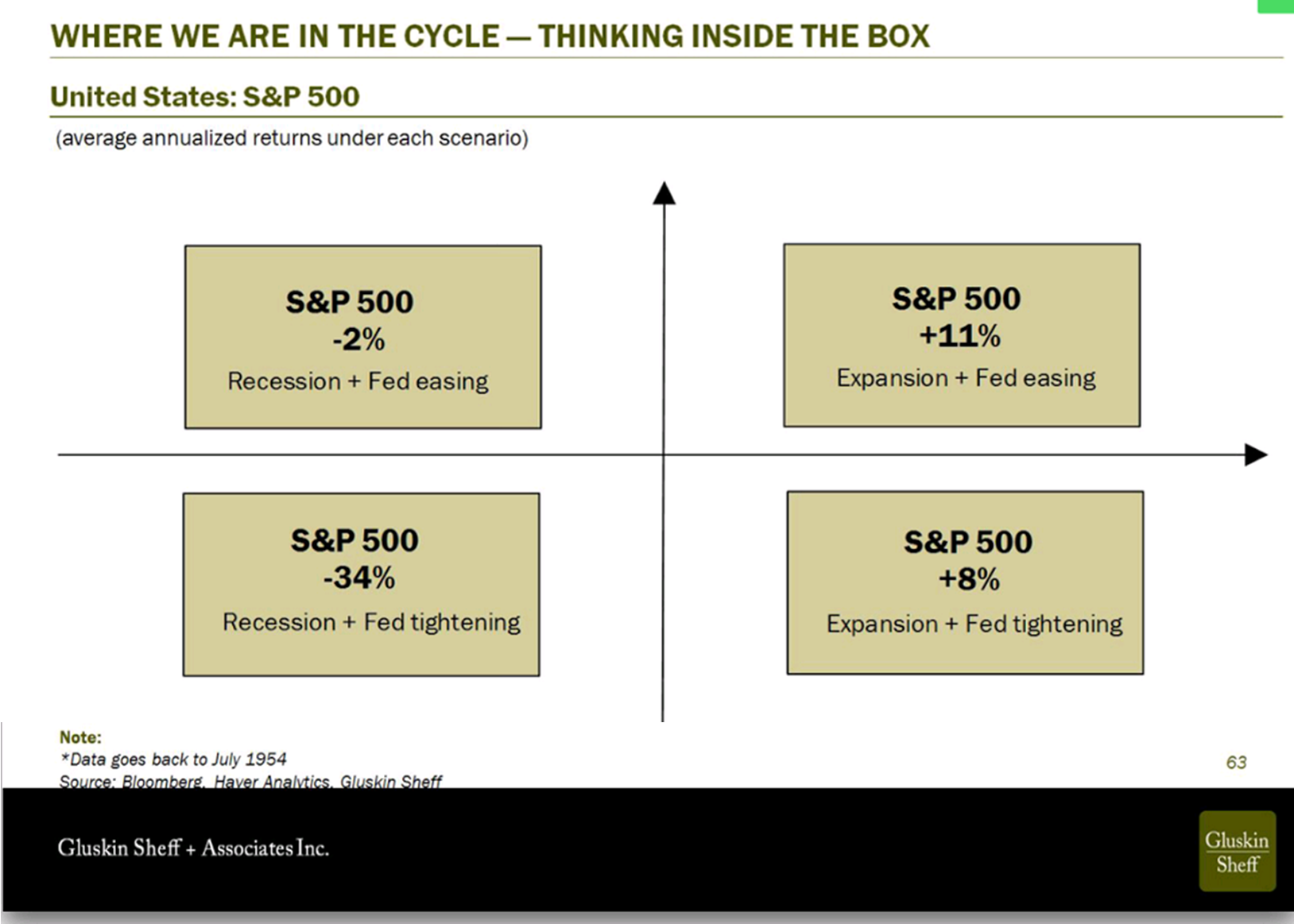

- Liked this next chart: S&P 500 returns broken down into four quadrants. We are somewhere between the two right quadrants (Fed likely to tighten soon).

- “When you are in a recession, start to bail” out of the market.

- “The U.S. has never been shocked into a recession by another country.”

- Concluded that it is a slow motion recovery that gets no respect. Noting that “inflation is the end game and it will be in our future. Central banks will ultimately get what they want.”

Peter Briger – CEO and Co-CIO Fortress Investment Group

Many years ago I ran a large structured trade. We borrowed money from a Wall Street bank and synthetically created a note. Underlying that note was a leveraged allocation to approximately 20 different non-correlating hedge funds. It was a great trade but we closed it at the end of 2007 concerned with the leverage in our note and the leverage in the system.

One of our allocations was to a bright hedge fund manager named Peter Briger. Peter ran and continues to run the credit group at Fortress. Prior to Fortress, he ran a credit group at Goldman Sachs for 15 years. He is one of the reasons I made the trip to this conference. He is super smart and an extremely disciplined investor. When my old friend Jon Sundt introduced Peter to the room, he said he told his wife that if anything happens to me, whatever you do, never sell our family’s investment in Peter’s fund. Unfortunately, we closed our investment with Fortress when we closed our structured trade.

With that, following are my notes from Peter’s presentation:

- This lead quote pretty much says it all, “I’m not raising money. Frankly, I’m pretty confused.”

- “We invest when the opportunity is good.”

- “The world seems very strange and very manipulated. Very hard to draw conclusions.”

- He noted his job is to walk into distressed situations and walk out with a bag of money.

- “Today, all the easy money has been made.”

- “Central banks are sitting around and trying to buy up all the bonds in their respective markets.”

- He said he should title this talk “Credit Sucks.”

- Liquidity is very high. It is easy for companies to get financed. While it is really hard to get a loan from a commercial bank, it is very easy to get a loan from the capital markets.

- He is “sure that we’ll see a high default rate over the next three years – especially on the corporate side.”

- The best investment opportunities are in high default environments and commercial banks under duress. Thinks we get high defaults but in this period of highly regulated banks (Dodd-Frank), he doesn’t see banks under as much duress as in prior periods.

- “Not saying that banks are not going to blow up again – that’s a certainty. It’s just going to take longer this cycle.”

- “Everyone has to think about what will happen to their wealth when interest rates change direction.”

- “The whole world is expensive right now” and added, “nobody in this room would want to buy bonds at 0% real interest rates.”

- Overall, he sees economies muddle along and banks deleveraged.

- Difficult to “fight the global Fed” and a strong worldwide banking system.

- In his personal account, he is trying to figure out the best way to short long-term sovereign debt. He said he wants to figure out how to short it without getting screwed. (On this note, my two cents is to buy puts on a foreign bank ETF or directly short the ETF or underling foreign bank stocks, but it is too early in my view for that trade as Draghi is just beginning European QE.

Lacy Hunt (with Q&A lead by the great Gary Shilling)

As one of my favorite sources of insight, Lacy didn’t disappoint. Overall, he thinks that high debt means slow growth and sees nothing that changes that story. He is an economist who is a money manager. He remains 100% invested in 20-year Treasury bonds and his current view is that the yield on the 30-year Treasury bond will drop to 1 ½ % or 2% and when we get there, were are going to stay there for a long time.

Here are my notes:

- From history’s many examples of high debt periods, all of which show economic slowdown, there are six periods of high indebtedness similar to today.

- In short, we don’t get normal economic growth.

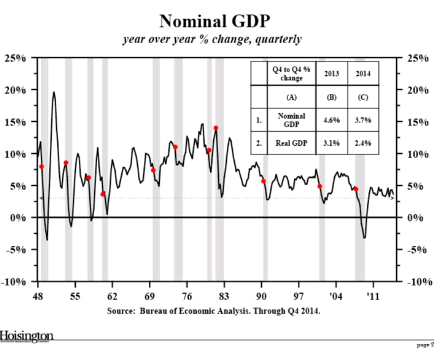

- Nominal GDP is the best measure of growth according to Lacy as it is the broadest and most complete measure of economic activity. He noted that the economy can go up, but it can’t stay up. The last five years are below all other peaks since 1948 (chart below).

- $10 trillion thrown at the problem and the Fed has quadrupled the size of its balance sheet with little overall impact.

- On wages for 70% of households: the level in this decade is below all others since 1965.

- Real GDP:

1790-1999 Real Per Capita GDP Growth = 1.9% average annual growth

2000-2014 Real Per Capita GDP Growth = 1.0% average annual growth

- The culprit is private and public debt.

- Liked this quote: “There becomes a point when the pay later overwhelms the buy now.”

- “An over-indebtedness problem can’t be overcome by piling on more debt. And we are piling on more debt.”

- 80% Debt to GDP is the level where public debt becomes a problem:

USA 110% Debt to GDP

EU 108% Debt to GDP

UK 96% Debt to GDP

Canada 94% Debt to GDP

- Important to note: “In the U.S., debt will rise by 1% per year due to Social Security requirements alone.”

- On productivity: lowest level since 1982 and below the low reached at the bottom of the great recession.

- “When productivity falters, the economy and wages and income can’t grow.”

- Monetary Policy – “the mechanisms that work in a low debt environment do not work in a high debt environment.”

- The QE money went into the Banks and the banks put it in the Reserve. There has been no growth in M2 money supply.

- Velocity of money – we are at a six decade low. “A clear sign that debt levels are problematic.”

- Same problem in Japan and the EU – velocity is declining, “the problem is too much debt.”

- On the Wealth Effect: He sees little impact on the economy. Families earning less than $150,000 per year have limited holdings in stocks. They are unable to change their lifestyle due to a wealth effect. Those earning greater than $150,000 do have holdings but they are unlikely to change their spending habits.

- No wealth effect – no evidence out there to prove the thesis.

- S. economic conditions unlikely to improve for many years to come.

In the Q&A with Gary Shilling:

- Shilling sees the 30-year Treasury moving to 2% and the 10-year moving to 1% (his targets).

- Lacy 1 ½ % on the 30-year as noted above – “When we get down there, it is going to stay low for a long time.”

- Deflation remains the greatest risk and noted the long bond rate is a great indicator of economic conditions (Fed can influence the short end but not the long end).

In summary, there were various views, but what is clear is that traditional return potential is low. Whether it’s Rosenberg’s more optimistic economic view (if you can call it that) and belief that inflation is in our future in 2018, Briger’s “credit sucks” or Hunt’s debt drag – lower long-term rates – deflation remains the greatest risk.

Personal note

As I reflect on the various views on what lies ahead (recession, inflation, default, growth), I can’t help but recall the fact that most economists get it wrong (even the great ones). I lean towards “Don’t Fight the Fed and the Tape”. It is “liquidity that moves markets” as reminded by the great Druckenmiller in the intro quote:

“Earnings don’t move the overall market; it’s the Federal Reserve board. And whatever you do, focus on the central banks and focus on the movement of liquidity. Most people in the market are looking for earnings and conventional measures. It’s liquidity that moves markets.”

As for recessions, I thought of the piece I wrote last week titled, “Recession Watch – Keep an Eye on This Chart”. For me it takes a lot of economist confusion out of the equation though it is important to take in data from some of the brightest minds amongst us.

Maybe Rosenberg is right, he titled his presentation “The Rodney Dangerfield Expansion – the economy just can’t get any respect.” Perhaps Hunt is right, “the U.S. economic conditions are unlikely to improve for many years to come.” Briger doesn’t’ see great opportunity in credit for several years (but a blow up in credit and the banks is certain). I am in that same camp seeing an opportunity of a lifetime coming in high yield bonds –just not yet.

Stay broadly diversified. Hedge your equity exposure where you can and include a number of diverse risks in your portfolio. Tactical all asset strategies, global macro strategies and tactical fixed income can help produce return, income and risk preservation.

The quant geek in me says to monitor the “recession watch” chart. It seems to me to be a highly probable and disciplined way to identify the timing of recession and take a lot of noise out of the equation.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM: Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456. Please read the prospectus carefully before investing. The CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA. NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, or the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site.

© CMG Captial Management Group

© CMG Capital Management Group