The Bureau of Economic Analysis will report its initial estimate of first quarter growth on April 29. There’s always a lot of uncertainty in the advance estimate, but that’s especially true for 1Q15. Of the key components of GDP, consumer spending is expected to have slowed to a more moderate pace – nothing terrible. However, business fixed investment should be soft. For business investment, as with manufacturing activity in general, it’s often difficult to distinguish a short-term slowdown from the beginning of a more significant downturn.

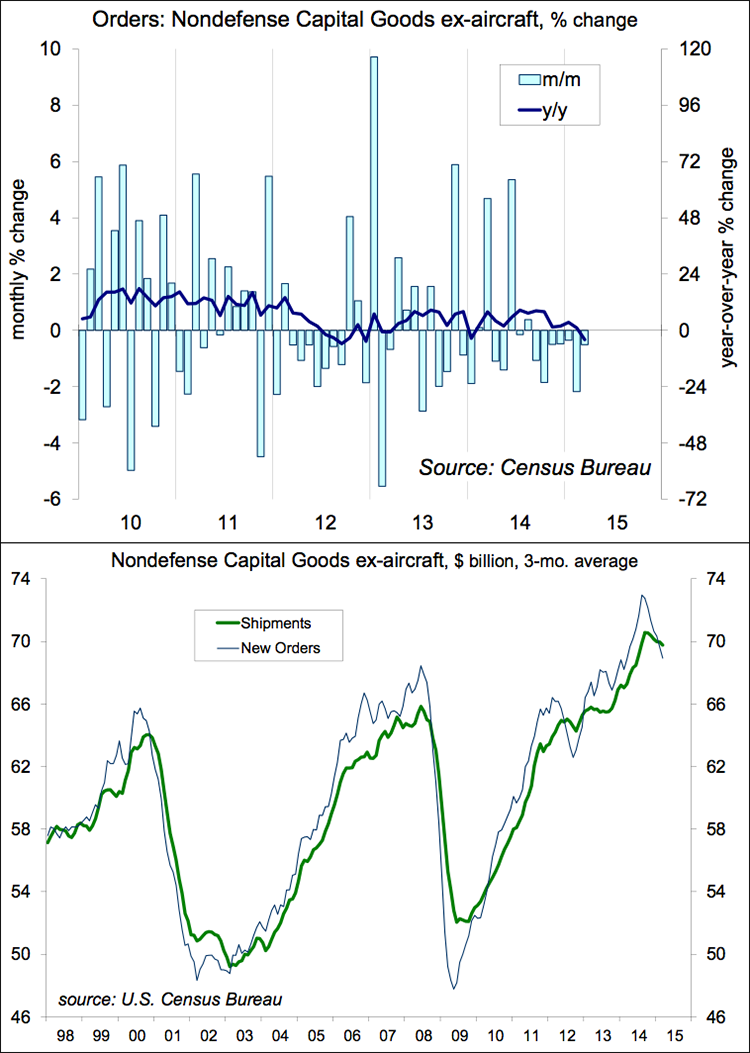

Orders for core capital goods (nondefense and excluding aircraft) have fallen for seven months in a row. This decline could be a “correction” from unusual strength in 2Q14 and 3Q14. More likely, it’s a reflection of the stronger dollar. The dollar has had a negative impact on corporate profits, which are a key driver of capital investment. The dollar has stabilized in recent weeks. If that continues, the currency impact on earnings should fade over time. There’s nothing to suggest a sharp decline in business investment similar to recent recessions.

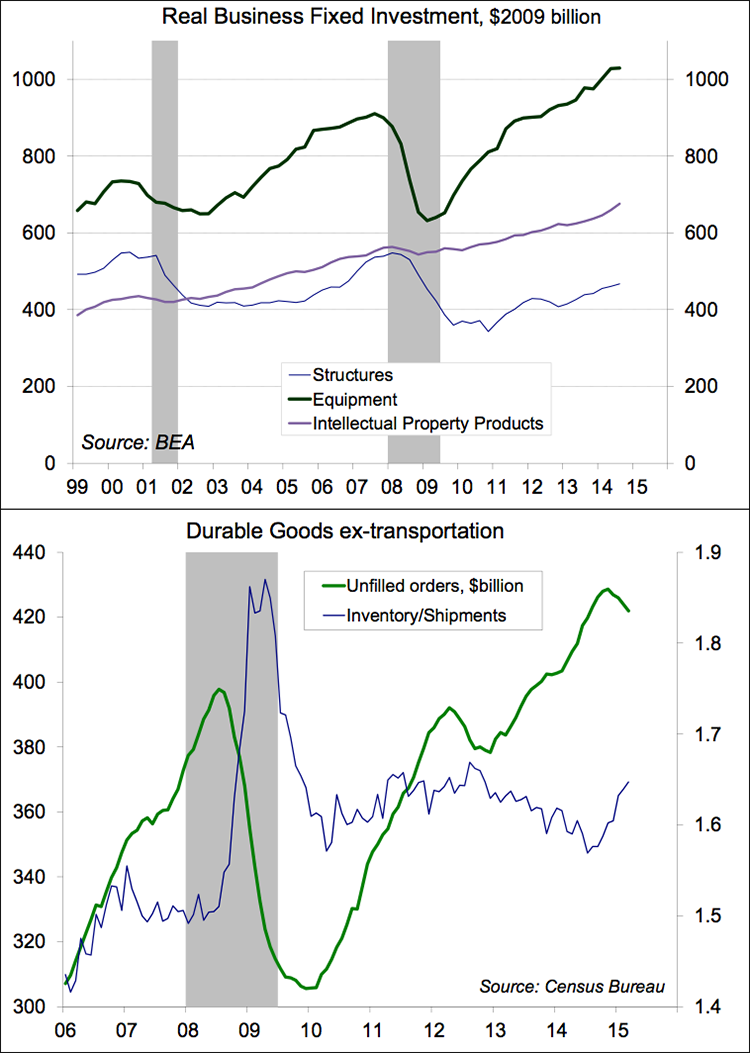

There’s a reason that it’s called “the business cycle.” Business fixed investment accounts for about 13% of GDP, but it swings sharply in recessions and recoveries. Business fixed investment includes structures, equipment, and (since 2013) intellectual property products. Structures and equipment are the more cyclical components. In recent quarters, energy exploration and extraction accounted for about 6.8% of business fixed investment (some equipment, but mostly structures) or about 0.9% of Gross Domestic Product.

Durable goods orders and shipments provide some insights into the manufacturing sector, but some gauges will tend to lead (although not always). Unfilled orders, a favorite of former Fed Chair Alan Greenspan, are an early indicator of trouble when falling. The inventory-to-shipments ratio can be used to gauge imbalances. However, the increased use of computers and scanners in inventory management and the off-shoring of inventories make the U.S. economy less susceptible to inventory cycles (compared to a few decades ago). These gauges are not yet at “danger” levels, but they bear watching.