I’m sure you remember my friend Mr. Market. He was introduced to me a few years after I entered the business of investment advice via Ben Graham’s book The Intelligent Investor, and for most years since I have found him to be quite fair and reasonable. Whether I wanted to sell or buy any one of the thousands of securities available to the public, he would make an intelligent opinion of its value and proceed to close the deal at that price. However, Mr. Market’s decisions can be affected by irrationality and moodiness. At times he will be brilliant and worth our undivided attention. On other occasions he may be completely off-base in his opinions.

As with any long-standing friend, we know his strengths and his weaknesses. We know Mr. Market lives in a short-term world. He has to constantly work hard to set a respectable price minute by minute, day by day. This is his greatest strength; it also is his greatest weakness. He does not have the luxury of planning for his long-term future.

Knowing that Mr. Market has had decades to develop his short-term skills, we have come to recognize that our only advantage over Mr. Market is time, and with this knowledge, we build and maintain our portfolios. However, this approach does come with a price, which is measured in dollars over a very short-term period. At times this price can be so unbearable that our human weaknesses take over, and some of us succumb to the lure of trying to beat Mr. Market in the day by day race, hoping to maximize short-term rewards. Others give up, and swear off owning any and all stocks, bonds, and other securities available in the marketplace.

As a long term value investor our portfolio returns can, at times, pay this price in the short-term for being a bit different. Over the past few months our lack of owning bonds in our conservative accounts has held back our relative returns. In addition, our ownership of large and powerful companies whose products are sold around the world have seen price declines due to the strength of the US dollar. We will take a little time in this letter to discuss these. In addition, I want to share with you my thoughts on why it can be difficult to be a value investor and earn the excess returns a value strategy offers.

Bonds

Bonds and other income bearing securities have been the preferred investments for both individuals and financial institutions for decades. There is a perfectly acceptable reason for this. When you own a bond, you are promised an interest payment for the use of your money and are promised that your principal will be repaid at some future date.

Mr. Market is adept at setting the market rate of interest. He bases these rates on the ability of the borrower to repay the principal in the future, the expectation of future inflation, and in the short-term, the amount of buyers willing to lend their money relative to the amount of borrowers in need of a loan. As the lender, or the owner of the bond, the largest reward, if not the only reward, will be the interest paid to us in a check. Because of this, we want to own bonds when we are completely satisfied with the interest rate paid until maturity.

Most of us know that Mr. Market sets prices for common stocks, and we recognize that at times he has been quite silly in his pricing. Some of us have first-hand experience with this, as fifteen years ago he was pricing technology “ideas” for millions, if not billions of dollars. What many of us do not realize is that Mr. Market can be just as silly when he prices bonds. I believe today he is truly showing us this side with the pricing of fixed income securities. Let’s see if you agree with me based on some of his recent actions around the world.

In early April the Swiss government sold a bond with a negative interest rate that will mature in 2025. Let me explain this with a little story. As you know, our office is just upstairs from the lending department of one of our local banks. Last week I went downstairs to visit with my local banker, who was all ears when I wanted a loan for one million dollars ($1,000,000). This is the deal I offered him: “If you lend me this money I promise to pay you back $950,000 in ten years. Of course there will be no interest paid on the loan and if for some reason I die in the next ten years you will receive nothing.” Do you think my banker would give me the $1,000,000 under those terms? Of course not, yet the Swiss government had no problem at all obtaining a loan from Mr. Market under very similar terms.

Mr. Market made another loan last week. This time the loan was to the government of Mexico. Being a neighbor to Mexico, I know a couple of things about the country. First, it has unfortunately had a history of not paying obligations in a timely manner. Second, some Mexican citizens have not been too happy with their government or with their lives in Mexico, and have chosen to leave their homeland for greener pastures. In contrast to the Swiss bond, there is some doubt in regards to whether interest will be paid by Mexico or whether the principal will be repaid when the loan matures. Of course Mr. Market took this into consideration when he lent Mexico funds, and he decided it was a good idea to charge some interest. He decided to charge Mexico 4.2%. Some of you may think this is not so bad. After all, we can’t get that much interest here in our town. But in order to get the 4.2%, Mr. Market had to agree that Mexico would not repay the principal for 100 years. That silly Mr. Market… doesn’t he know that everyone who borrowed these funds will be dead before the promised repayment date? Do you really think the great grand babies of the borrowers will be saving their money to repay this debt ten decades from now?

Mr. Market’s loans to Switzerland and Mexico are not the only demonstrations of his silliness. He has lent trillions of dollars to nine other countries around the world at a ten year repayment date with the sole requirement of an interest payment of less than ½ of 1% (0.50%) per year. This is the equivalent of being paid $5.00 a year for every $1,000 borrowed. Belgium, Finland, France, Germany, Netherlands, Sweden, Switzerland, Czech Republic and Japan have gladly borrowed money from Mr. Market for almost nothing.

It’s true that the bond market has produced some pretty good returns over the past thirty years, and some will say that owning bonds provides the benefits of diversification, or that Mr. Market is always correct and smarter than all of us. Although not owning intermediate or long-term bonds over the past couple of years may have minimized the total returns earned on our balanced accounts, I have no desire to participate with Mr. Market by lending my own money or your money under the current terms he is offering.

Mr. Market will come to his senses on interest rates at some time in the future. When he does, I can only hope for the millions of people who have invested their savings in bonds and other fixed rate securities that the transition is gradual. However, in the past, Mr. Market has not taken his sweet time correcting prices.

The Large and Powerful

We have felt some of Mr. Market’s manic corrections over the past six months, as the share prices of many of the great companies of America that do business around the world experienced dramatic swings. Mr. Market’s price corrections had to do with the value of one currency over another. How one currency is valued relative to another may be an unfamiliar concept to you. For our purposes, just think in terms of your dollars and what they will buy. When shopping, what your dollar will buy varies with the quantity or quality of what you are seeking. Take sweet corn as an example. Growing up in Iowa, it was a great pleasure having sweet corn on the cob abundantly available in late spring and early summer. You could buy a dozen ears of the best tasting corn in the world for just a little bit of money. Later in the year, after the season ended, corn on the cob was not only expensive, but almost impossible to find. If the farmer could charge these fall prices in the springtime, he would certainly be rich.

Think of your dollars as ears of corn. Beginning seven years ago, our own federal reserve produced trillions of dollars and sent them off to the world’s markets. Just like cheap corn on the cob, the world feasted on cheap dollars, buying the equivalent of a dozen ears of corn for just a little bit of their money. Yet the American farmers who grew the corn were able to earn a profit as if they were selling all corn at fall prices.

Global corporations based in America took advantage of this. They built factories and distribution systems to sell products and services to people around the world, who paid for everything with their own currency, be it the euro, yen, etc. American corporations were able to sell products that were cheap for the buyer and also highly profitable to the seller. This profit was realized when the American company adjusted foreign sales into US dollars.

Since the middle of last year, the value of the dollar has strengthened. People around the world who have had the luxury of buying American goods and service at springtime prices are now having to pay a higher price. Because of that, American companies are struggling to sell the same amount of items, and are also not able to charge fall prices. This reduces their profits, which is realized when the American company adjusts their foreign sales into US dollars.

Today it takes about 25% more foreign currency to buy the same amount of American produced goods and services as it did just a year ago. Think of yourself and what you would do if the price you paid increased 25% in less than a year? I am sure you would make adjustments. Mr. Market’s reaction to this change was to reduce the share price of these great American based global companies. But as always, Mr. Market’s price reduction went a little overboard. With his short-term focus, he failed to take into account the fact that these great companies have handled the change in value of currencies for decades. He may be correct today, but he gives little credit to the value of time. With time, the benefits of providing goods or services to the 7+ billion people in the world versus the 300+ million people who call America home will add greater and more sustainable profits for the owners of these great businesses. Mr. Market will ultimately recognize this.

A Problem for Value Investors

Outperforming Mr. Market in the short-term is close to impossible. Those of us who practice a value approach to investing, however, have seen some success in the long run. The evidence of this success is abundant and shared willingly by most of its practitioners, the most famous of whom is Warren Buffett. It is surprising that the documented history of value investing has shown that it has consistently produced a rate of return over and above the market indices for the last nine decades, yet it is still frowned upon by many investors world-wide. There has to be a reason for this. My own anecdotal reason is plain and simple. It is just too hard for most people to pay the psychological price of being a successful value investor.

I will share with you an example of a company we recently sold. First, please note that due to regulatory oversight in place to protect you and anyone who may read this, I need to remind you to read our disclosures, which are printed at the bottom of this letter. I also must mention that this example includes the results of an investment that worked out for us, but as you are aware, this is not always the case. Also, because the future is completely unknown and can vary wildly from the past, no one should draw any conclusion that our results from this example can be replicated and be equally successful in the future.

Now, with that said, I’d like to review our investment in Kohl’s Corporation. Because time is a factor in measuring investment success, those of us who purchased shares of Kohl’s early on and owned them for a longer period of time might only view their investment performance in the position as average. However, those who purchased the position a year or so ago might view the shorter term investment performance as exceptional. Either way, for our learning purposes, this example covers the safety of buying low, the patience needed for effective value investing, and demonstrates how Mr. Market can change his mind quickly.

Kohl’s Corporation (KSS) operates a chain of department stores in all states but Hawaii. For the most part, they sell brand-name and private-label clothing, footwear and accessories to women and their families. Over the last ten years they have been pretty successful, earning an average return on equity of 15.5%, a return on invested capital of a little over 12%, and have grown their book value at a little over 8% a year. They began paying dividends in 2011 and have increased the payment per share from $1.00 to an expected $1.80 this year. The company is considered financially sound with a financial strength rating of A+ from Value Line.

Kohl’s seems to be a fine company managed by a competent team, although there might not be anything that jumps out and excites you about it. Of course Mr. Market was fully aware of this and afforded Kohl’s a market price that we at Anderson Griggs believed was a little less than fair. So why then would we invest? Looking back I could use selective memory, but instead I will tell you that our primary driver was in maintaining a diversified portfolio. We want to own a representative group of all major economic sectors, and at the time we were a bit shy on our ownership of companies in the consumer discretionary sector. Kohl’s is a member of this sector, and their share price was cheap enough to provide us with a little safety and an expected return that was acceptable.

Here is a simple equation that I have found helpful in explaining your returns:

Investor Returns = (Future Earnings x Market Multiples) + Dividends

This is simple enough, but what will be the future earnings and dividends? And most importantly, what will Mr. Market set as the price? Of these variables, future earnings and dividends are under the control of the economy and company management. Mr. Market sets the multiple of these earnings at what he believes is correct.

The ability to forecast each of these variables on its own is subject to large errors, as all of us know. With skill, the accuracy of estimating future earnings for the next year or so is close enough to be used with a margin of error. The dividends tend to be set by boards who seldom, if ever, for a financially sound company, will change the current dividend payment without a great deal of warning. The market multiple is the largest and most important variable of the three, yet it is the one variable that is next to impossible to predict with any accuracy. The best we can do is use history and regression to the mean to guide us. Because all three of these variables are important and each will add or subtract from your returns, we do not base a purchase or a sale on one alone, but attempt to estimate all three.

Our original purchase of Kohl’s was in the spring of 2011 at average price of about $51.00. Here were our expectations:

Trailing Earnings at time of purchase: $3.23 Expected Earning 12 months forward: $3.69 Expected Dividend: $1.00 Earnings Multiple Range Past 10 Years: 13.37 – 21.58 Simple 10 year Average Multiple: 17.48

Using our equation, our potential upside results 12 months into the future at the time of our original purchase were:

$3.69 (Expected Earnings) x 17.48 (Average 10 year multiple) = $64.50 - $51.00(purchase price) = $13.50 (Capital Gain) + $1.00 (Dividend) = $14.50. As a percentage of purchase price: 28.43%

Using our equation, these were our potential downside results 12 months into the future:

$3.69 (Expected Earnings) x 13.37 (Low 10 year multiple) = $49.34 - $51.00 (purchase price) = -$1.66 (Capital Loss) + $1.00 (Dividend) = -$0.66. As a percentage of purchase price: -1.29%

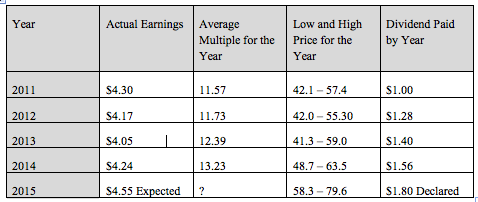

This is the actual results and share price range:

We held on, because Mr. Market never offered to buy our shares at what we considered a fair price. In a portfolio of 40 to 50 companies, on average 70% of your holdings will have similar results as this example. In most cases the current market price will be below your purchase price at some point. Company earnings will vary more than we expect. Because Mr. Market assigns a value to a company based on factors that will unfold in the future, we will sell our positions when those forecasts are rosy and he is pricing the company for future perfection.We sold all of our shares on April 2nd at $79.06, at 18.64 times trailing earnings of $4.24, or 17.37 times expected earnings of $4.55. Every year for the first three years we owned shares of Kohl’s, the market price was both below and above our purchase price. This year by year share price volatility was not a concern, as it was close to the normal fluctuation of market prices every year, which is approximately 30% between the high and low prices.

Holding a company whose market price is below the purchase price for a number of years is often too hard for people. We feel dumb hanging on. We only feel good if we are doing the same thing as everyone else, which means we should sell when prices are down. Of course, this also means that selling when the price is going up is just as wrong. Instead we should be buying when the price is going up like everyone else. In other words, to feel good we should sell low and buy high, because that is what everyone else is doing. Yet greater success comes from buying low and selling high, the very actions that provide so many opportunities to make us feel bad. Earning the value premium sounds easy, yet in practice most of us do not have the mental strength necessary to actually keep it.

On February 27th, Warren Buffett held a meeting with Dr. George Athanassakos of the Ivey Business School of Western University and his MBA and HBA students in Omaha, Nebraska. Buffett was asked, “What are some common traits of good investors?” Part of his answer was: “Toughness is important. There is a lot of temptation to cave in or follow others but it is important to stick to your own convictions. I have seen so many smart people do dumb things because of what everyone else is doing.”

Anderson Griggs & Company, Inc., doing business as Anderson Griggs Investments, is a registered investment adviser. Anderson Griggs only conducts business in states and locations where it is properly registered or meets state requirement for advisors. This commentary is for informational purposes only and is not an offer of investment advice. We will only render advice after we deliver our Form ADV Part 2 to a client in an authorized jurisdiction and receive a properly executed Investment Supervisory Services Agreement. Any reference to performance is historical in nature and no assumption about future performance should be made based on the past performance of any Anderson Griggs’ Investment Objectives, individual account, individual security or index. Upon request, Anderson Griggs Investments will provide to you a list of all trade recommendations made by us for the immediately preceding 12 months. The authors of publications are expressing general opinions and commentary. They are not attempting to provide legal, accounting, or specific advice to any individual concerning their personal situation. Anderson Griggs Investments’ office is located at 113 E. Main St., Suite 310, Rock Hill, SC 29730. The local phone number is 803-324-5044 and nationally can be reached via its toll-free number 800-254-0874.

(c) Anderson Griggs