“I’m not predicting a crash, I’m just saying the risk reward of going early (Fed raising rates) is better than going late.”

- Stan Druckenmiller

I spent 45 minutes this morning watching the Bloomberg interview with Stan Druckenmiller. I had a number of other things to share with you today, gathered over the course of the week, but they have been moved to the backseat. Put Druckenmiller’s comments in the important category. Often gruff, I enjoy his clear and candid way.

Outperforming Warren Buffett and most everyone else, Stan’s track record is reported to be 30% per year for 30 years (with never a down year). Let’s just say we should be interested in what he has to say.

I share my notes from the interview below but I encourage you to find some down time, grab a coffee, and watch the first 40 minutes of the interview. Additionally, you’ll see that the interview references a private presentation Stan made in January at a Ken Langone (Home Depot founder and frequent CNBC guest) sponsored event. Someone recorded the presentation and titled it “The Speech at the Lost Tree Club”. It is worth the read. You’ll find the link below.

You and I are in a tough business. It is based on probabilities and involves imperfection. The mismatch between customer expectations and practical reality is challenging. Art Cashin said, “That to survive 50 years in this business, you learn that the first thing you do when you enter a room is look for the exit sign.” It is with this thinking, along with Druckenmiller’s material, that I also share a great (short) piece on investing and risk from Ned Davis. Another grateful nod to NDR for allowing me to share it with you.

I hope you find the material helpful.

Included in this week’s On My Radar:

- Notes From the Bloomberg Druckenmiller Interview

- Speech at Lost Tree Club

Notes From the Bloomberg Druckenmiller Interview

He feels much like he did in 2004 and is more worried about looking down the road than the near term.

He sees no reason for zero interest rates:

- Why does the economy need extraordinary help.

- Retail sales are at an all-time high.

- Everything is booming except corporate capital reinvestment. That money is going into share buy backs and dividend payouts.

On where the Fed funds rate should be:

- In 2009, the Fed came up with a new version of the Taylor Rule. It said then that rates should be a -4%. Instead the Fed chose QE.

- Today that version of the Taylor Rule says that Fed funds rate should be 3 ½ %.

- If you use the traditional Taylor Rule, which said in 2009 rates should be -1%, today’s rates should be at 1.75%.

- We remain at 0%. Why?

- Strongly noting: The time has come to get us off the juice.

Every month that goes by we have more and more financial engineering. We are borrowing to buy stocks.

Stan’s fear is we won’t see a cut for 1.5 years. No confidence there will be rate hikes in June, September or by year-end.

- We’ve already met the metrics they set out.

- If you wait, the risk is worse.

- It’s a pay me know or pay me later scenario.

He is not predicting a crash or predicting doom. He is saying that as someone who practices risk reward for a living, the risk reward of the Fed moving early is better than moving late.

He was asked about Ray Dalio’s belief that we are seeing 1937 happening all over again. Duckenmiller disagrees stating the two periods are quite different:

- In 1937, stock prices and household net worth were 20% below where they were in 1929.

- Today we are at new highs in stock prices and household net worth.

- From 1929 – 1937 we had a cumulative 18% deflation.

- From 2007 to now we’ve had a cumulative 16% inflation and the Fed’s favorite measure of inflation has never been below 1% since 2007.

- Unemployment was over 14% in 1937. It is currently 5.5% today.

On deleveraging he answers that there is NO deleveraging. We have re-leveraged from an already high 2008 level. World debt has grown $57 trillion – McKinsey Report.

- In 2000: World Debt to GDP was 245%

- In 2007: World Debt to GDP was 269%

- Today World Debt to GDP is 290%

- We are doubling down in terms of debt.

He was asked about corporate credit – the host speaking favorably about corporate balance sheets. Druckenmiller responds with a firm NO and adds:

- Corporate credit in 2007 was $3.5 trillion and is now $7 trillion

- We are not talking about good quality debt here

- High yield loans in 2007 were $800 billion and are $1.4 trillion now

- Covenant lite loans which were $100 billion then are $500 billion now at a $300 billion run rate

- 28% of debt back then was B rated. Now 71% is B rated

- The risk of a credit event is extremely high

His style of investing is he can change his portfolio within 24 hours.

Something he learned from George Soros: When you see it, bet big.

Big bets he sees today:

- Flipping of monetary policy created a textbook opportunity in currencies: The negative deposit rate in the EU, the EU going into QE and the US ending QE. He has never seen a major currency trend last less than two years. We are ten months into it. Dollar higher. Euro lower.

- Another big bet is Japanese and European equities.

- Has new ideas he’s flirting with – is pretty optimistic on crude prices.

- Also sees one other wild card. China’s stock market is up 140% in six months on record volume and record breadth. As day follows night six months down the road, we are in a full-blown strong economy. He is opining on the transmission mechanism of the market to the economy – market goes up, wealth goes up, the economy goes up.

He believes Europe’s economy has actually turned and is looking better.

He believes the Euro could get into the 80s. Stating, that would be about the average move for a currency when they get into a big trend. The big currency moves when in motion generally see something like a 50% to 55% move which would target an 80 handle on the Euro. Don’t forget it was at 82 in 2000.

I really enjoyed his comments around the dollar and the economy:

- Effects the strong dollar could have on the US economy. He finds no correlation between the level of the dollar and the direction of the dollar on the effect on the economy – after a study for a better part of 40 years. He can find no correlation to the level and direction of the dollar to the economy.

- It is true that has a negative effect on corporate earnings; however, that is very small compared to the impact a strong dollar has on the consumer who is 70% of the economy as it gets a big purchasing boost in a stronger dollar.

- He does see correlation in a strong dollar to a strong economy but can’t say if it is because a strong economy causes a strong dollar or a strong dollar causes a strong economy. No evidence.

- What is true is that it is negative for corporate earnings. But noted that corporations are a very small part of the economy relative to the 70% that is the consumer and a strong dollar benefits the consumer.

He cited the following supporting the above:

- The dollar went from 80 to 160 by June 2008. Under a dollar theory, shouldn’t we have been going into an economic boom? He recalls the economy sunk sharply shortly after.

- When he was at Soros, the Yen declined from 78 to 147 vs. the dollar between 1995 and 1996. Japan did not experience great economic growth because their currency went down 50% to 60%.

- He has been looking at this for a long, long time; he can’t find the evidence that a currency has that big of an effect on economic activity.

He touched on the student loan problem: stating it is very reminiscent of the housing boom. Bill Ackman thinks it is the biggest risk we face. Druckenmiller doesn’t see it getting paid back. He is somewhat concerned about the student loan problem and generally agrees with Bill.

One mistake he made in the past was getting emotional about investing. Nice to hear that from one of the great traders.

I’m tried to hit all the important points but click here for the full piece.

Speech at Lost Tree Club

When clients and friends ask me for investing advice, I ask them if they are an investor or a speculator. What I’m trying to do is see what process best suites who they are inside. Put an investor (let’s call this category broad based asset allocation) “all in” on a few speculative bets and failure is sure to occur. Broadly diversify the speculator and a similar personality/expectation mismatch is sure to occur.

Great speculators have the conviction to stick with a bet when it is not working. Most also have a risk management process to limit loss. No one hits 100%. I have heard it said that broad diversification is the only free lunch in the investment business. To that I agree. Sure wish I had a 10% allocation to Druckenmiller’s hedge fund over the last 30 years.

The Druckenmiller speech at Lost Tree Club is readable and enjoyable. You get a chance to get into the mind of one of history’s greatest investment speculator. All I can say is read it, file it and reread it again another day. It is both enlightening and enjoyable. Link to the full piece here.

Sage Words from Ned Davis – Compounding Returns and Making the Trend Your Friend

Excerpts from Ned’s piece,

“My philosophy in making money and how the trend fits into that is my subject today. I basically believe that most people get rich by compounding interest and probably the best investment to compound is the stock market. Stocks have returned 10% per annum, almost double most other investments.

So the main key to getting wealthy is to compound investment returns. And long-term investing in stocks has certainly been one of the best choices. But one must also find a method of investing that one can live with – that meets one’s psyche. It’s important to understand the market does not go up constantly over time.

I’ve also learned this about compound returns. If you buy something at $100, and it goes to $50, that is a 50% loss, but it will take a 100% advance to just get back to even. So when asked how to make money, Warren Buffett said he had two rules: “Rule #1 – Don’t lose money. Rule #2 – Don’t forget Rule #1.”

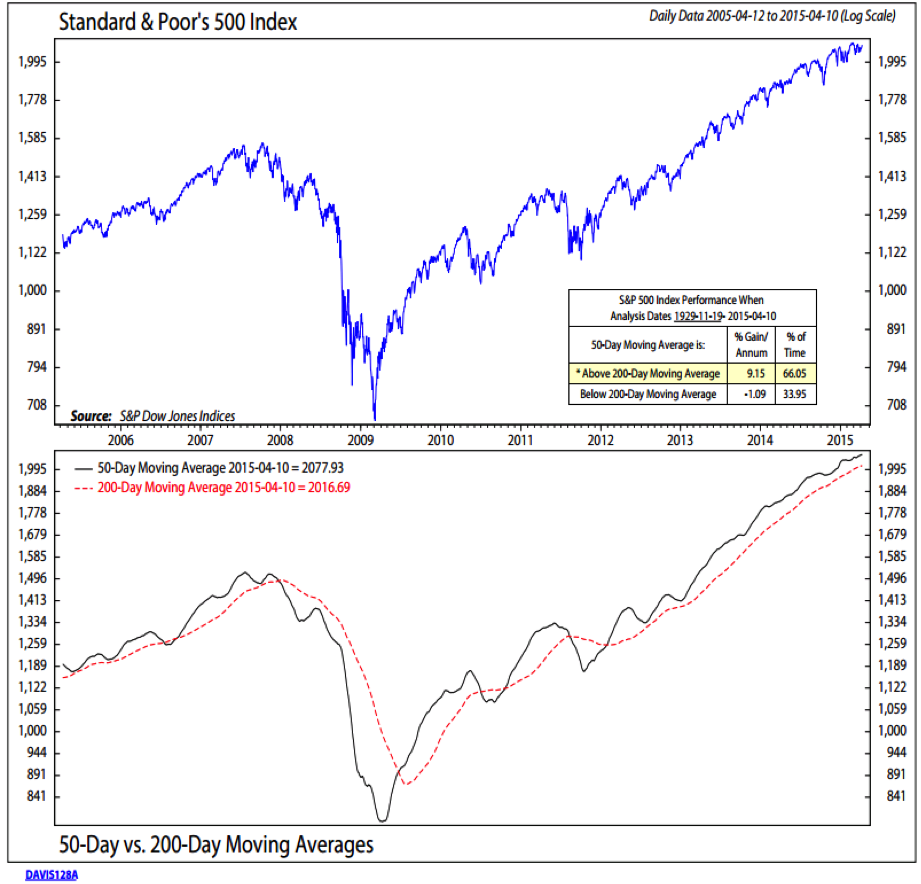

I don’t like to take big losses. For me, this means the trend is your friend or “don’t fight the tape.” As one example of this, note chart DAVIS128A (below). Here, we’ve calculated how the market performed whenever the 50-day smoothing of the trend goes above the 200-day smoothing. We used data going back to 1929 and all the net gains in stock prices came when the trend was upward as measured by this simple trend formula. The results are based upon price alone and do not include dividends or interest earned when out of stocks. The reason this indicator worked is that it lets profits run, but cuts losses short, a great money management rule.

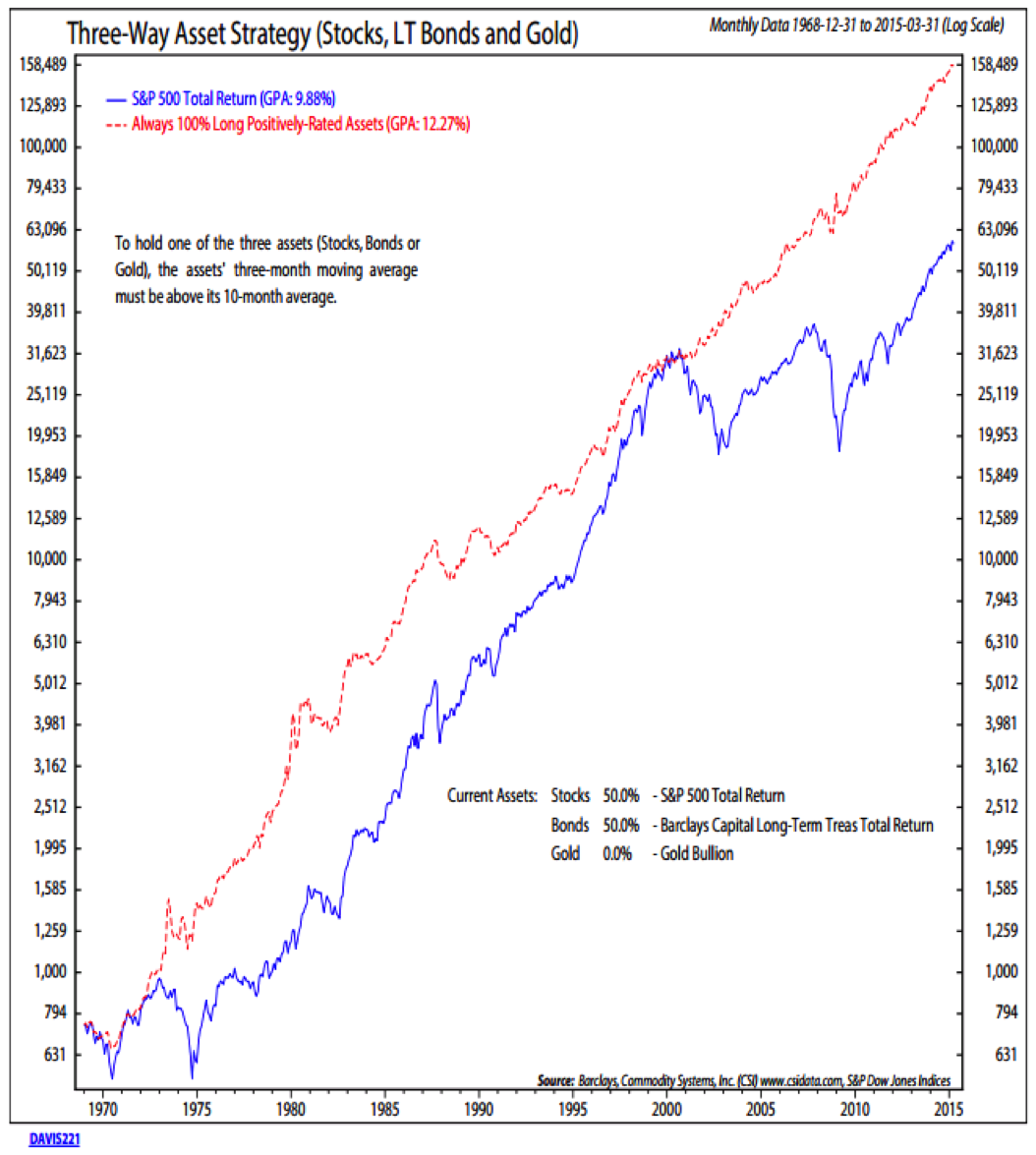

But I also like to diversify. I think it cuts risks. So I don’t just want to be limited to compounding stock returns. The next chart illustrates the returns one could have enjoyed using a similar formula as DAVIS128A, but using it to allocate a portfolio among stocks, bonds, and gold. Just being in these three investments during uptrends has beaten the record of just being long stocks (DAVIS221, below).

This indicator starts in 1968 because that is when gold started trading freely. Why did this indicator work? As I learned in Economics 101, prices are determined by supply and demand. And prices are also the equilibrium points of supply and demand. Thus, if prices are rising, demand must be greater than supply, and I want to be in. To not lose money, I hedge my risks when we get into downtrends.”

While Ned examples a 50-day over 200-day moving average crossover (and it has done a good job keeping one on trend), I favor the Big Mo indicator and a 13-week over 34-week moving average crossover. The overall message is to have a plan and the discipline to stick to the plan. I post risk management ideas each week in Trade Signals. Coincidentally, I wrote about diversification and better understanding uncorrelated returns in Wednesday’s Trade Signals post. Let me know what you think.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM: Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456. Please read the prospectus carefully before investing. The CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA. NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, or the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

© CMG Capital Management Group, Inc.

© CMG Capital Management Group