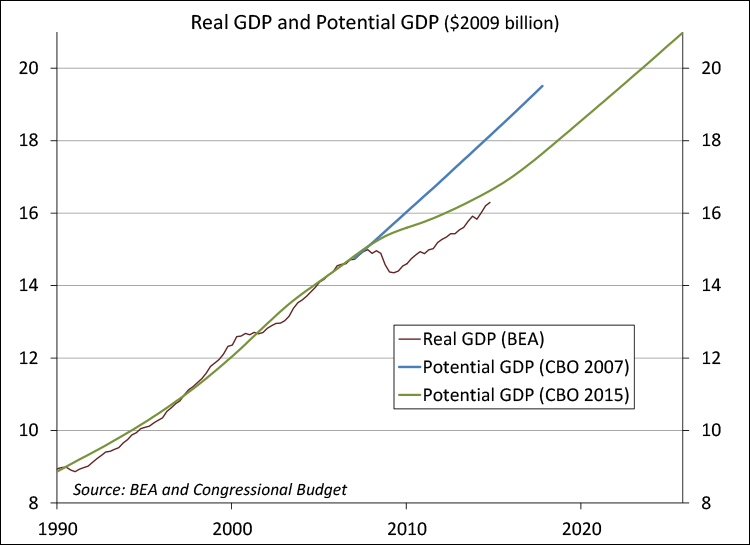

The good news is that the output gap, the difference between real Gross Domestic Product and its potential, has narrowed. The bad news is that’s largely because potential GDP has declined. The big question now is whether the economy is on a permanently lower track. The answer is not so clear.

We like to say that the 2008-09 economic downturn was not your father’s recession. It was more like your grandfather’s depression. This was not the typical Fed-induced recession. This was a collapse of a housing bubble combined with a huge deleveraging within the financial system. More than eight years after the initial downturn and nearly six years into the economic recovery, the borrowing situation appears to be in better balance. That doesn’t mean that everything is okay, but we are on better footing and poised for improvement.

It’s an odd fact that GDP growth has averaged about 3% per year over the last several decades. Through that time, we’ve had variations in labor growth (increased female labor force participation in the 1960s, 70s, and 80s) and changes in productivity growth. This trend may go back well before the turn of the last century, as suggested by some historical analysis (GDP, as a concept, did not exist back then). GDP deviated from the trend during the Great Depression, but returned to it after World War II. There is no good theoretical reason to expect 3% GDP growth over a long period of time. Output is equal to labor times the productivity of that labor. Why would labor growth and productivity growth sum to 3% on average?

Potential GDP can be defined to be the level of economic activity consistent with steady inflation (2%) over time – not too hot, not too cold. There are some challenges in forecasting it. The standard approach is to project labor input (considering population growth and the removal of current slack) and apply that to an estimate of productivity growth. Estimating the amount of slack in the labor market isn’t terribly difficult, but there are uncertainties. Population growth is slowing, so the longer-term trend in labor input should be slowing accordingly. The estimate of productivity growth will depend on the pace of capital investment. The main reason that the Congressional Budget Office’s projection of potential GDP has come down in recent years is that business fixed investment has been subdued through most of the recovery.

The key question is whether the lower track in potential GDP is permanent or secular (persisting over an indefinitely long period). One can imagine a scenario where population growth slows further (Europe is turning Japanese and the U.S. may not be far behind). This is a very important issue. At 1% GDP growth, the economy will be 34% larger in 30 years. At 3%, it will be 143% larger. Even a 0.5% difference in long-term growth will matter a lot for the outlook for the standard of living and for funding government entitlement programs.

Secular stagnation is not simply a concern for the U.S. In the analytic chapters of its World Economic Outlook, the IMF reports that “potential output growth across advanced and emerging market economies has declined in recent years.” For the advanced economies, the slowdown in potential GDP began well before the financial crisis, but the pace should pick up “as some crisis-related effects wear off (yet will still remain below the pre-recession trend). For emerging economies, the slowdown happened after the crisis. However, the slowdown in potential GDP for emerging economies is likely to continue, as their populations age and productivity slows as they “catch up to the technology frontier.” China has had phenomenal growth over the last few decades, but may have a tough time meeting current (lower) growth targets.

Investors tend to focus on the short term, but they would be wise to pay attention to the debate about the long term.

(c) Raymond James