IN THIS ISSUE:

1. Atlanta Fed Predicts Zero Growth in the 1Q

2. March Unemployment Report Was a Stunner

3. Implications For the Federal Reserve Rate Hike

4. What if the Official US Unemployment Rate is Wrong?

5. Measured Risk Portfolios WEBINAR on April 8

Overview

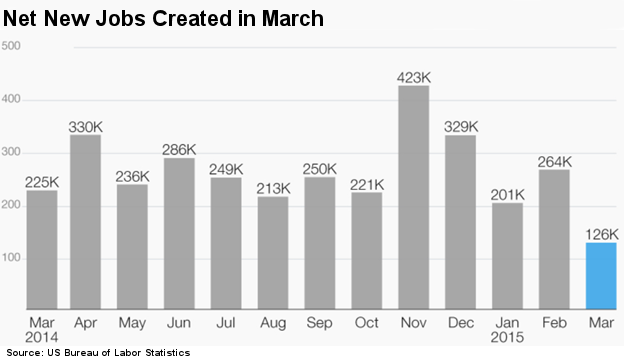

Last Friday’s unemployment report for March was a stunner, no doubt about it. After 12 consecutive months of new job creation above 200,000 per month, the Labor Department reported that only a meager126,000 new jobs were created in March.

Theories abound as to the cause of the huge drop-off in new jobs last month, but the default reason cited, once again this year, is the severe winter weather. While bitter winter weather is a factor, questions arise as to whether this could be a sign of worse things to come in the US economy.

We will focus today on the latest disappointing unemployment report and examine what the internals of the latest missive might mean for the economy, and for the Fed’s timing of its first interest rate hike.

Following that discussion, I want to shift our sights to a new study which suggests that the government’s official unemployment rate, currently 5.5% is significantly lower than reality. This new study concludes that the real unemployment rate in America today is somewhere between 7% and 9% or even higher. I think you’ll find this discussion compelling.

But before we get to today’s main topic on the latest unemployment report, I want to briefly share with you a new and disturbing economic forecast from none other than the Federal Reserve itself.

At the end of March, the Federal Reserve Bank of Atlanta released a new forecast for US GDP growth of0.0% for the 1Q. This surprising new forecast from the Fed itself has sparked a spirited new debate on the subject of where the US economy is headed this year.

Atlanta Fed Predicts Zero Growth in the 1Q

The research department of the Federal Reserve Bank of Atlanta has been less optimistic on the trajectory of the US economy this year than most forecasters. The Atlanta Fed issued its first estimate of 1Q GDP in early February at only 1.9% growth. That was well below the February economists’ consensus estimate of 2.5% or better.

Not long after, the Atlanta Fed pared its estimate of 1Q growth back to only 0.8%. And most recently, after another spate of disappointing economic reports, the Atlanta Fed has cut its latest growth forecast to zero(0.0%). There were very few reports on this in the mainstream media.

This report from within the Fed itself, along with last Friday’s shocking report on the lack of new jobs created in March, virtually assures that the Fed will not raise interest rates anytime soon, as I have predicted for months.

March Unemployment Report Was a Stunner

The weakening US economy spilled into the job market in March as employers added only 126,000 net new jobs – the fewest since December 2013 – snapping a streak of 12 straight months of gains above 200,000. The Labor Department said Friday that the unemployment rate remained at 5.5% in March.

Friday’s jobs report raised uncertainties about the world’s largest economy, which for months has been the envy of other industrialized nations for its steadily robust hiring and positive GDP growth. American employers appear wary about the economy, especially as a strong dollar has slowed US exports, home sales have stagnated and cheaper gasoline has yet to unleash more consumer spending.

Some of the weakness may prove temporary, since another unseasonably cold March followed a brutal winter that slowed key sectors of the economy. You may recall that the economy rebounded strongly in the 2Qand 3Q of last year, before slowing again in the 4Q.

Last month’s subpar job growth could make the Federal Reserve less likely to start raising interest rates from record lows in June, as some have been anticipating. The Fed may decide that the economy still needs the benefit of low borrowing costs to generate healthy growth. I continue to maintain that the Fed won’t raise rates until September, if at all this year.

Government bond yields fell sharply after Friday’s disappointing jobs report. The yield on the US 10-year Treasury note fell to 1.84% on Friday from 1.90% before the unemployment report. As this is written, the 10-year yield is back up to 1.90%.

Last month, the manufacturing, building and government sectors all shed workers. Factories cut 1,000 jobs, snapping a 19-month hiring streak. Construction jobs also fell by 1,000, the first drop in 15 months. Hiring at restaurants plunged from February. The mining and logging sector, which includes oil drilling, lost 11,000 jobs.

The federal government also shed jobs in March. In addition, the Labor Department revised down its estimate of job gains in February and January by a combined 69,000.

Wage growth in March remained modest. Average hourly wages rose 7 cents to $24.86 an hour. That marked a year-over-year pay increase of just 2.1%. But because average hours worked fell in March for the first time in 15 months, Americans actually earned less on average than they did in February. Tepid pay increases have been a drag on the economy since the Great Recession ended nearly six years ago.

Many Americans remain out of the labor force, partly because many Baby Boomers are reaching retirement age. The labor force participation rate – the percentage of Americans who are either working or looking for work – fell in March to 62.7%, tying the lowest rate since 1978.

Job growth had been healthy for more than a year before March. Yet the streak of strong hiring, along with cheaper gasoline, hasn’t significantly boosted consumer spending.

Implications For the Federal Reserve Rate Hike

The Fed signaled last month that it would be cautious in raising rates from record lows. The Fed has yet to rule out a June rate hike, but many analysts expect the first increase no earlier than September. In part, that’s because Fed officials have revised down the range of unemployment they view as consistent with a healthy economy to 5.0%–5.2% from 5.2%–5.5% previously.

The weak hiring last month could give them further pause. Chair Janet Yellen has stressed that even when the Fed begins raising rates, it will do so only very gradually. A Fed rate hike would suggest that the economy is improving. Yet the economy has weakened in the first two months of 2015, in part because of the tough winter.

Factory orders have been mixed, having dropped sharply in January before ticking up modestly in February. Cheaper oil has led energy companies to halt orders for pipelines and equipment, hurting manufacturers. At the same time, the strengthening dollar has made American-made goods costlier abroad, thereby cutting into exports.

Job growth over the last year has yet to ignite a larger boom in consumer spending. McDonald's, Wal-Mart, the Gap and other major employers have announced raises for their lowest-paid employees. But those pay raises are staggered and don’t affect all workers, so they are unlikely to fuel significantly faster wage growth.

The economy has disproportionately added lower-paying jobs in the retail and restaurant sectors since the economic recovery began in mid-2009. Adding jobs in the lowest-paid industries can suppress average hourly wages, even when employers are rewarding cashiers, waiters and sales clerks with small pay bumps.

The rise in lower-paying jobs hasn’t been enough to boost home sales. Housing prices have surged faster than wages since 2012, when the real estate market bottomed.

The likelihood of a strong spring rebound likely hinges on hiring by retailers and restaurants. But bars and restaurants added just 8,700 jobs in March, compared with 66,000 in February. Retailers stayed close to their 12-month average by adding 26,000.

The one bright spot in March was the continued reduction in the number of people that have been unemployed for 27 weeks or more. During the 16 months since Congress refused to renew extended unemployment benefits, long-term unemployment fell by 36.9%, as compared to the 21.8% decline seen during the prior 16-month period.

Other than that, the March jobs report was a real bummer.

What if the Official US Unemployment Rate is Wrong?

Judging by the official unemployment rate alone, the American economy would seem to be getting back on track. The US unemployment rate fell to 5.5% back in February 2015, from 10% just after the Great Recession ended in early 2009.

But what if these figures are hiding an uncomfortable reality about the economy? This is the conclusion reached by two highly respected economists, David Blanchflower of Dartmouth College and Andrew Levin of the International Monetary Fund, in a new paper published on March 19.

Blanchflower and Levin argue that the way the US calculates its unemployment figure obscures a significant amount of slack in the labor market, and that, if computed more accurately, the true unemployment rate in the US could be as high as 7% to 9%.

Speaking at an event about full employment at Johns Hopkins University in March, Levin argued that the official definition of unemployment is far too narrow. The US Bureau of Labor Statistics defines the unemployed as the percentage of the total labor force that is unemployed but actively seeking employment.

That means the unemployment figure misses out on two important groups of people: First, those who are working part-time because they can’t find a full-time job, a group the authors refer to as the“underemployed,” and those who have given up actively looking for work but might return to the workforce again given the right incentives, which they call the “hidden unemployed.”

Essentially, this calculation means that a drop in the unemployment rate isn’t always a good thing. For example, Levin and Blanchflower point out that the unemployment rate fell sharply in 2010 and 2011 because many people gave up looking for work. Because of how the Labor Department calculates unemployment, that took them out of the labor force and therefore out of the ranks of the officially unemployed.

If we add in the underemployed and the hidden unemployed, Levin and Blanchflower calculate, the ranks of the US unemployed would swell by the equivalent of 3.3 million full-time workers to over 10 million. I have written about this disparity in the numbers often in the past.

The authors argue that this hidden glut of surplus workers is the reason that America’s economic recovery over the past few years hasn’t yet resulted in widespread prosperity. Their paper presents statistical evidence that the large ranks of underemployed and hidden unemployed continue to weigh on wage growth.

As an example, let’s assume that an employer is looking to add a new full-time position. But rather than looking for someone who is already working full-time, this employer can look among the millions who are working part-time because they can’t find full-time work. And many of these applicants may be so desperate to leave part-time status, they may be willing to accept lower full-time pay. This is another reason why wages have stagnated.

The highlight of Levin and Blanchflower’s paper is their calculations of what the “real” unemployment rate should be, which really brings the issue into focus. Depending on how you calculate the figures, the authors estimate that the US has the equivalent of an additional 1.9-3.9 million unemployed people. Based on those figures, the true unemployment rate in the US would be somewhere between 7.4% and 9.4% today, rather than the official 5.5%.

That figure has important consequences for America’s monetary planners. Obviously, The Fed uses the unemployment rate as an important indicator of how and when it should stimulate the economy to guide it toward a path where inflation and employment growth are stable. Based on the unemployment rate of 5.5%, many believe the time is drawing near for the Fed to raise historically low interest rates, in order to avoid over-heating the economy.

But as Levin, Blanchflower, Ben Bernanke and other prominent economists argue, the time for monetary tightening appears to be still very far off. If the true unemployment rate really is 7.4%, the low end of the professors’ calculation, then the Fed would not be inclined to raise rates anytime soon.

Given their findings, it’s not hard to see why Levin and Blanchflower call a tighter monetary policy“premature” and “a serious mistake.” They argue the Fed should wait to tighten interest rates until inflation has accelerated and labor market slack has diminished.

So when would this happen? Given the economy’s current rate of growth of about 250,000 nonfarm jobs added per month on average in the last year, Levin and Blanchflower project that the employment gap might be eliminated toward the end of next year.

But if the economic recovery starts to decelerate, perhaps due to the strong dollar, higher oil prices, or weaker export markets, the US recovery could take much longer than that to close the gap. Altogether, these figures imply a slower policy tightening path than the Fed may have had in mind.

Best regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.