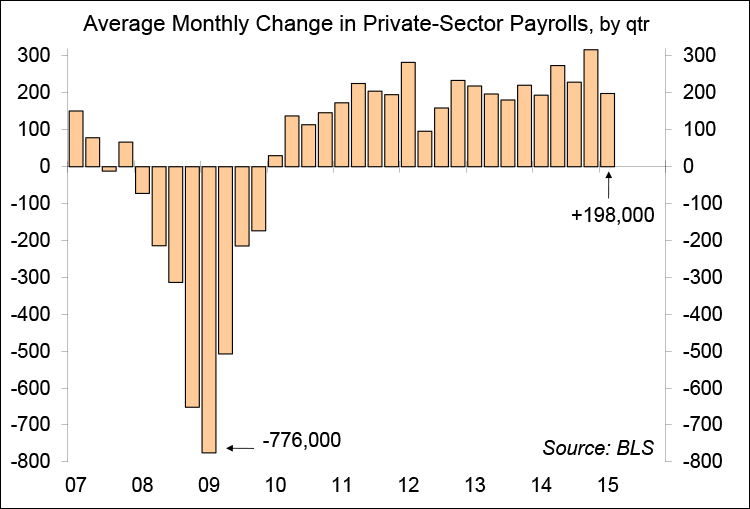

The nonfarm payroll data for March were disappointing. Job growth was substantially less than expected and figures for the first two months of the year were revised lower. These data fit in with the general theme of other recent economic reports. Growth slowed in the first quarter, reflecting bad weather and the negative impacts of a stronger dollar and lower oil prices. Growth is still widely expected to pick up in the spring, but for investors, that may begin to feel more a matter of faith.

Payrolls advanced by 126,000 in the initial estimate for March, about half the expected gain. Simply looking at the payroll graph suggests that we may be seeing a statistical moderation. There’s a fair amount of statistical uncertainty in the payroll figures. The monthly estimate is reported accurate to ±105,000 (for those of you who stayed awake in your statistics class, that is a 90% confidence interval). It’s not unusual to see the payroll figures bunch a bit higher or lower than the underlying trend. In other words, a strong quarter of payroll growth is often followed by a softer quarter. That doesn’t mean that job growth has necessarily “slowed.”

The impact of the weather can seem a bit quirky in the payroll reports. The payroll survey covers the pay period that includes the 12th of the month. That can vary from firm to firm (depending on whether workers are paid weekly or semi-monthly). The BLS noted that the survey period dodged the bad weather in February, but was not so lucky in March. The household survey, which covers the week of the 12th, showed that 328,000 people could not get to work due to bad weather in February, compared to a 387,000 average over the 10 previous Februarys. In March, 182,000 could not get to work due to bad weather, versus a 150,000 average over the past 10 years). So we went from better-than-normal weather in February to worse-than-normal weather in March. That may explains some of the shortfall in payrolls for March. Note that these are unadjusted figures from a different survey and are not directly comparable to the nonfarm payroll data, but suggest that we may see a weather-related rebound in April payrolls.

The stronger dollar and the decline in oil prices have both positive and negative effects on the economy. It’s likely that the negative effects are showing up more quickly than the benefits. The decrease in energy exploration is seen in the drop in mining payrolls (-11,100 in March, -11,100 in February, -7,400 in January). While perhaps devastating to local economies (these are high-paying jobs that are being lost), it is tiny on a national scale (about 0.02% of total payrolls). Even accounting for multiplier effects, the impact on total payrolls is small. The bigger impact from the retreat in energy exploration will come in capital spending. Note that the stronger dollar has hit corporate profits. Corporate profits are a key driver of capital spending and new hiring. This will show more at larger firms. Unlike the official BLS data, the ADP estimate of private-sector payrolls provides a breakout by size of firm. The March report showed a sharp slowing in job gains at large firms, but continued strength in hiring for small and medium-sized firms.

Job growth has been strong over the last year (over 3.1 million, or 2.3%). Combined with the increase in purchasing power from lower gasoline prices, consumer spending should be picking up. Consumer spending accounts for 70% of Gross Domestic Product, so the benefits of lower gasoline prices should offset the negative effects of the stronger dollar.

The general theme of recent data reports should make Fed policymakers less inclined to raise short-term interest rates this summer. The Fed is still justified to plan for policy normalization and to return to “business as usual” in June (that is, considering whether to raise rates on a meeting-by-meeting basis). However, the monetary policy outlook will depend critically on the upcoming economic data and signs of a spring awakening.

(C) Raymond James