IN THIS ISSUE:

1. How Concerned Are Americans About Climate Change?

2. The Weakest US Economic Recovery in Generations

3. US Economy Continues to Disappoint in Most Reports

4. Ahead of Tax Time, Some Interesting Rasmussen Surveys

Overview

The combination of topics for today’s E-Letter might seem unusual, and it is – the economy, the environment and income tax time. How do those fit together? They don’t really, but I think you will find today’s discussion on each to be interesting.

The economy has been in a slow recovery for the past five-and-a- half years. It’s the weakest post-recession rebound in generations. The Commerce Department’s latest revision of 4Q GDP shows that nothing much has changed. Meanwhile, winter economic reports for retail sales, manufacturing and capital investment point to a weaker 1Q, perhaps only around 1% growth in GDP.

Today we will look at several recent economic reports, most of which were (you guessed it, unless you didn’t read last week’s E-letter) disappointing. That includes last week’s final Gross Domestic Product report for the 4Q, Gallup’s Economic Confidence Index and February durable goods orders and housing starts.

I also want to share with you some of the latest interesting polling results from Rasmussen Reports that I think you’ll find very interesting, especially regarding how most Americans feel about the IRS – given that income tax day is just two weeks away.

But before we get to those topics, I want to share with you the findings of a couple of new Gallup polls which gauge Americans’ concerns about the environment and global warming. With so much alarmist rhetoric out there, you would think that the environment would be near the top of most Americans’ worry list. Let’s take a look.

How Concerned Are Americans About Climate Change?

With back-to-back severe winters in the US, climate scientists and environmental activists are warning louder than ever about global warming or “climate change,” as they now prefer to call it. Given the intensity and frequency of the warnings, you would think that the environment would be a top concern for most Americans. Yet the latest Gallup Environment Surveys taken in early March prove otherwise.

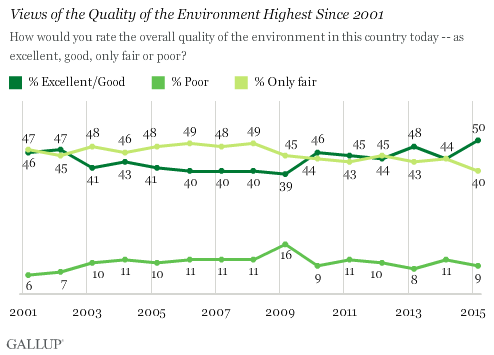

One of the questions asked of over 1,000 adults (age 18 or over and in all 50 states and DC) was: How would you rate the overall quality of the environment in this country today – excellent/good or fair or poor? Now before you look at the chart below, think of which of the three categories you would select, and which one you would think most other people would pick. Now take a look.

Did you think that 50% of survey respondents would answer “Excellent/Good,” the largest selection of the three? Did you think that 90% would answer Excellent/Good or “Fair”? And finally, did you expect that only 9% would select “Poor”? I didn’t!

As you can also see, the percentage selecting Excellent/Good has increased significantly since the low in 2009. The percentage selecting Poor has declined significantly since the high in 2009. This is despite the increasingly shrill warnings from some climate scientists and environmental activists, including President Obama.

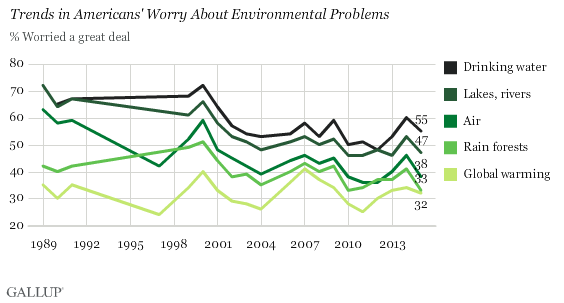

In a separate survey, Gallup asked Americans about specific environmental threats they worry about, ranging from global warming to polluted drinking water to pollution of rivers, lakes and reservoirs toair pollution to the loss of rain forests, etc.

Again, before you look at the chart below, think about which of the five specific threats worry you the most, and which one the least. Now take a look.

What this chart tells us is that the only significant point about the public’s concern over global warming is that it has gone essentially nowhere over the last 25 years. This is rather remarkable given that the environmentalists have waged perhaps the most expensive public relations campaign ever over the same period.

In doing so, they have had significant help from the public school system, the universities, an infinite parade of celebrities, think tanks and an entire major political party – the Democrats. Yet most Americans are considerably less worried today over most environmental threats.

My main point today is that even though the shrieking from the environmentalist crowd is getting louder, Americans are becoming more positive about the quality of their environment and less concerned about the threats.

Let’s move on to some economic analysis.

The Weakest US Economic Recovery in Generations

The economy has been in a slow recovery for the past five-and-a- half years. It’s the weakest post-recession rebound in generations. The Commerce Department’s latest revision of 4Q GDP shows that nothing much has changed, as I will discuss below, even though there was some brief optimism last year when 3Q GDP hit 5%. But that didn’t last.

Meanwhile, winter economic reports for retail sales, manufacturing and capital investment point to a weaker 1Q, perhaps only around 1% growth in GDP. And Wall Street is talking about a possible profits recession, with expectations of a 2-3% drop in corporate earnings for the first half of 2015.

Globally, things are even worse. Europe, Japan, and Russia are all in recession or near it, and all are flirting with outright deflation. China’s formerly red-hot economy is also faltering. Japan doubled-down on quantitative easing late last year, while Europe started QE in a big way this year. Financial risks have definitely heightened.

In light of all this, the stock markets are struggling so far this year. Investors are nervous, as well they should be. Outflows from equity mutual funds and ETFs this year are the heaviest they’ve been since early 2009 at the depth of the Great Recession.

Historically, after deep recessions, the economy comes roaring back with GDP growth of 4-5% or more. But as we all know now, this time is different. By some calculations, GDP is 10% – or nearly $2 trillion – below its long-term trend, and overall jobs are lagging by 8 to 10 million.

Government entitlement transfers pay people not to work. Family breakdown has created a poverty trap for the lowest economic groups. Upward mobility is lagging, so fewer people are moving to where the jobs are. And the government has attacked the high-end movers and shakers with tax hikes and overregulation.

Unfortunately, a damaging business psychology prevails within the current administration that has led to more businesses closing down than starting up – for the first time in US history. The Obama crowd believes success must be punished and that redistribution is the way to solve inadequate growth and income inequality.

With that said, let’s look at some of the latest economic reports.

US Economy Continues to Disappoint in Most Reports

The Commerce Department reported last Friday that 4Q GDP was up 2.2% (annual rate), unchanged from the previous estimate in February. The pre-report consensus was for an increase to 2.4%, so the report was considered another disappointment. For all of 2014, GDP rose by 2.4%.

The overall picture last quarter was mixed, with consumers spending at the fastest pace in several years, but with business investment decelerating and government outlays falling. As a result most estimates for growth in the 1Q of 2015 have been trimmed to a range of 0.9% to 1.4%.

The government also reported that after-tax corporate profits fell at a 1.6% rate in the 4Q, as a strong dollar dented the earnings of multinational corporations. For all of 2014, profits dropped 8.3%, the largest annual drop since 2008.

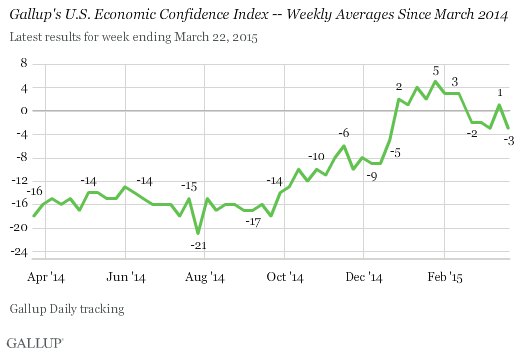

Gallup’s Economic Confidence Index, which had been rising since last August as gas prices fell, has been trending lower this year. That is a reflection of slower than expected growth so far in 2015 and decreasing expectations for the rest of this year.

Orders for American-made durable goods unexpectedly dropped in February as manufacturers absorbed the damage inflicted by a rising dollar and slumping energy production. Demand for goods meant to last at least three years declined 1.4% after a 2% gain in January. The pre-report consensus called for a rise of 0.3%.

Elsewhere, housing starts tumbled in February. The cold, snowy weather was the main reason since the declines were much deeper in the Northeast and the Midwest regions, as compared to the South and the West regions where the cold weather was less of a factor.

Housing starts in February fell to 897,000 units (annual rate), down from 1.081 million in January. The pre-report consensus was for 1.041 million units. In addition to the weather, many locally-based homebuilders have been restrained by difficulty in obtaining construction loans.

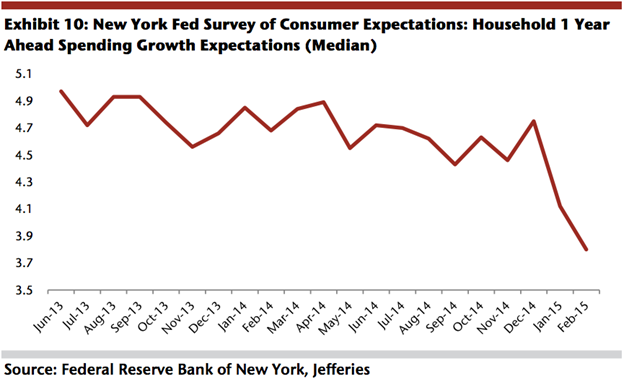

Finally, as most readers know, consumer spending makes up apprx. 70% of GDP. Given that, it is always important to gauge the forward expectations of US consumers. With the plunge in gas and energy prices since last summer, US consumers have more cash in their bank accounts.

But as I have discussed in recent weeks, many American families have chosen to save most of that cash rather than spend it. The following chart may explain in large part why consumers are being so cautious.

It is obvious that American consumers are troubled by what they see as the future of the economy and jobs, despite the improvements in the labor market in recent months. It is my opinion that consumers are also troubled by what they continue to see coming out of the Obama administration in terms of more and more onerous regulations.

While not directly related to the economy, I think consumers are also really scared by President Obama’s unyielding quest to strike a nuclear deal with Iran, despite lopsided polls showing huge public disapproval. Whatever the reasons, consumer expectations have gone into a nosedive since the end of last year. This is definitely not a good sign for the economy.

Ahead of Tax Time, Some Interesting Rasmussen Surveys

With April 15 just two weeks away, millions of Americans and their tax preparers are busy getting ready to pay Uncle Sam what they owe. I am a subscriber to Rasmussen Reports so I see dozens of polls every week. Rasmussen significantly increases its polling around tax time, and I thought it would be interesting to look at some of the latest samplings as we approach April 15.

Americans are slightly ahead of last year’s pace when it comes to filing their income taxes. A new Rasmussen Reports national telephone survey found that 55% of American adults have already filed their income taxes, up from 51% who had done so by this time last year.

Some 32% have yet to file but plan to do so by the April 15 deadline. Another 5% plan to get an extension on their tax return, while 9% are not sure what they’ll do.

47% of adults now expect they’ll get a refund this year, up from 43% in February, while 20% expect to owe the government money. Some 20% predict that they will break even, while 13% are not sure.

An estimated 70% of Americans will file their 2014 tax returns electronically this year, up slightly from 68% in 2013 and 63% the previous year. Only 18% will file by mail, while 12% are undecided.

In another set of polling, Rasmussen found that the IRS has a growing PR problem. 50% of likely US voters don’t trust the IRS to fairly enforce tax laws. On the other hand, 31% do trust the IRS to enforce the laws fairly, but 19% are not sure.

Some 64% of Republicans and 56% of Independents don’t trust the IRS – whereas only 32% of Democrats feel that way. 50% of all voters surveyed view the IRS unfavorably, with 25% very unfavorable. This is actually an improvement over last year.

Surprisingly, 40% of all voters have a favorable opinion of the IRS, but that includes only six percent (6%) with a very favorable one. This, too, is an improvement over March of last year when just 34% viewed the IRS favorably and 58% did not. Not sure how that happened.

Men, especially those age 40 and over, are more likely to distrust the IRS than women and younger voters are. 69% of political conservatives do not trust the IRS to fairly enforce tax laws. Just 39% of moderates and 34% of liberals agree.

Interestingly, Rasmussen found that government employees are just as likely as those employed in the private sector to distrust the IRS.

The IRS definitely has some serious taxpayer service issues. The head of the IRS acknowledged recently that it has answered or returned less than half of taxpayer telephone calls in the last year because of its relatively new responsibilities policing Obamacare – this despite adding over 16,000 new agents for Obamacare alone.

The IRS definitely has some serious taxpayer service issues. The head of the IRS acknowledged recently that it has answered or returned less than half of taxpayer telephone calls in the last year because of its relatively new responsibilities policing Obamacare – this despite adding over 16,000 new agents for Obamacare alone.

The IRS’ image problems also stem in part from the lingering questions over its targeting of Tea Party and other conservative groups. Most voters have said in surveys since the agency’s rogue activity was first disclosed in spring 2013 that it was criminal and politically motivated. 58% said it’s likely that President Obama and/or his top aides were aware of the IRS’ actions.

Most voters also think it’s likely that the IRS deliberately destroyed e-mails about its investigations of Tea Party and other conservative groups to hide its criminal behavior. Two-out-of-three voters believe IRS employees involved in these investigations should be jailed or fired, or both.

Have a great rest of the week!

Very best regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.