IN THIS ISSUE:

1. US Economy Disappoints Analysts’ Expectations Badly

2. CitiGroup’s Economic Surprise Index Ranks US Lowest

3. US Most Disappointing in Developed World vs. Forecasts

4. Despite Plunging Rig Count, US Oil Production Still Rising

5. Oil Companies Face High-Interest Junk Bonds or Bankruptcy

Overview

Today we will talk about an economic indicator that I have not written about before, which is compiled and reported monthly by CitiGroup, the American multinational banking and financial services corporation headquartered in Manhattan.

The report is known as the CitiGroup Economic Surprise Report. It is an interesting indicator in that it measures how actual economic reports exceed or fall short of their pre-report expectations, or“consensus” as we call it.

CitiGroup compiles the Surprise Report each month, not only for the US but also for other regions of the world, including the Eurozone, China, Asia and others. We will look at this particular indicator today since most US economic reports this year have come in below expectations, whereas in late 2014, most exceeded the consensus.

What does this tell us about the future? Most analysts conclude that the recent downward trend in the Surprise Report means that the US economy is slowing down, perhaps significantly. I tend to agree. Yet some others maintain that the report tells us little, if anything, about the direction of the economy. That’s what we will talk about today.

Following that discussion, we’ll turn our attention to the latest developments in the oil patch. Given the collapse in oil prices over the last year, the number of working oil rigs has plummeted by almost 50%. Yet very surprisingly, daily oil production and our level of above-ground crude inventory have continued to increase rapidly.

The question is, how can the rig count drop by almost half, yet daily oil production has continued to soar? The answer may surprise you. Let’s get started.

US Economy Disappoints Analysts’ Expectations Badly

Of late, there is one economic indicator that is really making the rounds: CitiGroup’s US Economic Surprise index. The Surprise Index merely looks at a variety of monthly economic reports and ranks them on the basis of whether they were better or worse than the pre-report consensus.

This index gauges how US economic data performs relative to expectations on a rolling three-month basis. A reading of 0 means that the last three months’ worth of data were on balance in-line with Wall Street estimates. The index climbs into positive territory when economic data is better than expected, and it goes negative when data disappoints.

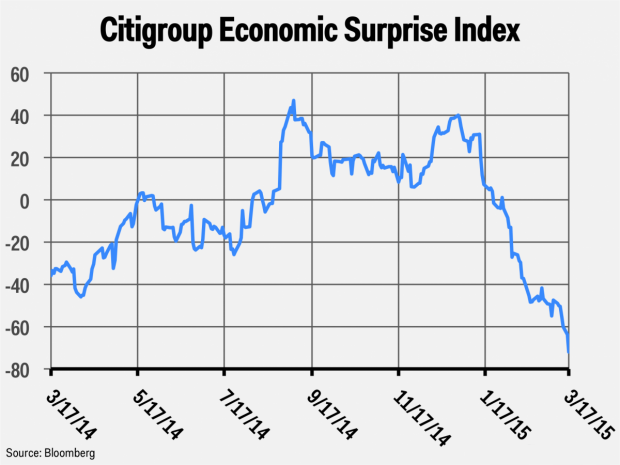

On the surface, this would not seem to matter to most of us, but if we drill down deeper, the Surprise Index can lead us to clues as to where the economic trend is headed. So let’s start by looking at a chart.

Now let’s be clear as to what this chart shows. The Surprise Index merely shows how the various economic reports exceeded or disappointed the pre-report expectations average. It does not necessarily represent whether the overall economy is headed up or down. However, I do think this index can be useful in spotting upcoming trends, particularly when it changes direction.

Simply put, US economic reports, on balance, exceeded the pre-report consensus in the second half of last year. Then the Index plunged sharply lower beginning in January. What that means is that most of our monthly economic reports have fallen below analysts’ average pre-report expectations. This is not a good sign for our economy.

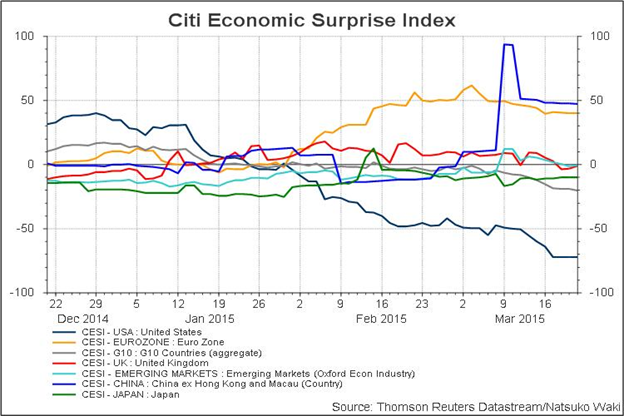

Now let’s look at another chart on the same subject. This chart shows how the US economy has faltered recently in terms of CitiGroup’s Surprise Index, which compares the US to the Eurozone, the G-10 countries, the UK, China, Japan and emerging nations. Take a look.

The US has gone from the leader in late 2014 to the laggard so far this year. That is a huge drop in less than six months. How could this happen? Again, this is just a function of how many of our economic reports have come in below the pre-report consensus.

Currently the US Economic Surprise Index is at levels not seen since 2008, when America was in the deepest recession since the Great Depression. Again, this doesn’t mean that the economy is anywhere near as bad as it was then. But whether it’s a slowdown caused by the harsh winter or something else, relative to where economists thought we would be, the US economy is missing by a large margin.

This also doesn’t mean that all sectors of the economy are disappointing. One notable exception to the disappointment is jobs. The economy added 295,000 jobs in February and 1.3 million over the last four months, a reflection of a healthier labor market in which the unemployment rate has fallen to the lowest level in almost seven years.

Most everything else, though, is disappointing. This month alone, personal income and spending, manufacturing (as measured by the Institute for Supply Management), auto sales, factory orders, and retail sales have all come in weaker than expected.

The surprise shortfall in the US doesn't necessarily mean the world’s largest economy is in dire straits. It’s just falling short of elevated expectations which may be due to earlier optimistic forecasts for growth in 2015 that have since been revised lower. Whatever the reasons, the US has seen the most disappointing economic reports, relative to forecasts, of any of the countries tracked by CitiGroup.

Federal Reserve Chair Janet Yellen made no mention of the US economy faltering in her congressional testimony in late February. In fact, she cited an “overall improvement in the U.S. economy and the U.S. economic outlook,” boosted by lower oil prices. However, the Fed changed its tune at the latest policy meeting last week and acknowledged that “economic growth has moderated somewhat.”

The statement also indicated the Fed will not raise the Fed Funds rate until it sees “further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term.” [Emphasis mine.]

In conclusion, it remains to be seen if the US economy is headed for another slump. But we have clearly seen a drop in retail sales over the last three consecutive months, as I pointed out last week. Nevertheless, most forecasters still believe the economy will grow by 2.5-3.0% this year, despite the fact that the US Surprise Index has disappointed more than any other country in recent months.

Despite Plunging Rig Count, US Oil Production Still Rising

Given the fact that crude oil prices plunged from above $100 per barrel to below $47 as of last week’s close, you would expect that a lot of drilling rigs would be shut down and oil production would decline, perhaps sharply. Yet US oil production continues to rise.

It’s true that many rigs are being idled. As of early March, only 866 rigs were still active in the US, down almost 50% from October, when they peaked at 1,609. Oil drillers are shutting down their least productive rigs. Yet with only slightly more than half of their rigs still working, crude oil production continues to rise.

There’s a dirty little secret most people outside of the oil industry don’t know: Many small to midsize producers have no way to service their debt except by selling oil. Therefore, most are continuing to bring oil to market as fast as they can (but also as cheaply as they can, using only the most efficient rigs).

In fact, the cheaper oil becomes, the more oil these producers have to bring to market to service their debt. Hence, production may continue to surge. In fact, we now have 450 million barrels on hand, versus an available physical storage capacity of 521 million barrels in the US.

Some indication of how serious the situation is can perhaps be garnered from the surprise announcement last Friday that the US government will buy five million barrels of oil for the Strategic Petroleum Reserve. Just a year ago, the Department of Energy caught oil markets off guard with a “test sale” of five million barrels of oil from the Strategic Petroleum Reserve. Thus, the government has gone from selling oil to being a buyer of reserve oil, in one year.

It will have little effect, in any case. While five million barrels may sound like a lot of oil, it represents only one week’s additional inventory surplus, or half a day of production. Unless the government decides to buy this much oil every week, we’re looking at a continued pile-up of four to seven million barrels of surplus oil per week.

If that continues, we might be just 10 weeks away from hitting the absolute storage limit of 521 million barrels. As we approach that limit, oil prices could fall, perhaps precipitously, and some producers will default on their debts, a process that has already begun.

Oil Companies Face High-Interest Junk Bonds or Bankruptcy

The oil price crash is taking a growing financial toll on companies throughout the oil industry, forcing some into bankruptcy and others to issue expensive junk bonds to stay afloat.

The rise in junk bonds and bankruptcies is the latest sign of stress in the petroleum sector as US crude prices linger around $45 a barrel, down nearly 60% since last summer. Low prices depress profits and pinch balance sheets, especially for smaller companies, which can be heavily leveraged.

On March 17, shale producer Quicksilver Resources filed for bankruptcy protection for its US operations after missing a bond payment. Earlier bankruptcies include a March 3 filing by Cal Dive International, which installs offshore pipelines and platforms.

And energy firms are now the top issuers, by a wide margin, of junk bonds, which require them to pay much higher interest rates than conventional bonds.

On March 5, Gulf Coast oil producer Energy XXI issued $1.45 billion in new bonds that pay a steep 11%, and plans to use the money in part to pay other lenders. Energy XXI had previously warned it would not be able to make payments if oil prices stay low.

The issuance of high-yield energy company bonds surged by about $30 billion in the first two months of the year. That was far more than any other sector, according to Fitch Ratings.

While the number of bankruptcies has so far been limited, that number is almost certain to soar if oil prices remain below $50-$60 per barrel. “You need oil prices to be lower for longer before you see a tidal wave of bankruptcies,” said David Pursell, managing director at Tudor, Pickering Holt, an energy investment bank in Houston.

One wrinkle is that to continue to win financing, companies have to keep producing and selling oil, which keeps downward pressure on crude prices. The International Energy Agency last week warned that, despite the sharp fall in crude prices, US supply “so far shows precious little sign of slowing down.”

Fitch Ratings said that it expects oil output to fall off in the second half of the year, slowly pushing up prices. Nevertheless, Fitch warned that it “believes energy default rates will push above the historic average,” in part because many companies that jumped into the shale business are relatively low-quality borrowers.

And finally, there is still the risk that oil prices could fall significantly lower. Some forecasters are convinced – what with production continuing to increase – that crude prices are destined to fall to $30 or below. Commodities maven Dennis Gartman predicts that crude prices will fall even lower than that by the end of this year.

The growing risk of more bankruptcies in the oil patch is yet another reason I recommended last week that investors reduce equity exposure, hedge long positions or consider some of the actively managed strategies that I recommend.

As always, past performance is not necessarily indicative of future results.

Wishing you well in these crazy markets,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.