The question of whether the Fed would abandon the “patient” language should have not been an issue, but the financial press always tries to generate some level of tension. However, while the Federal Open Market Committee appeared to move closer to tightening monetary policy, it indirectly signaled that it would likely be much less aggressive.

In its policy statement, the FOMC noted that economic growth has “moderated somewhat.” In her press briefing, Chair Yellen cited slower growth in household spending, weaker export growth, and a subdued recovery in housing. The Fed’s outlook is “not a weak forecast,” said Yellen. The Fed is still expecting above-trend growth. However, the outlook is less optimistic than it was three months ago.

| Federal Reserve’s Summary of Economic Projections: | ||||

|---|---|---|---|---|

| 2015 | 2016 | 2017 | long run | |

| Real GDP (4Q/4Q) | 2.3-2.7% | 2.3-2.6% | 2.0-2.4% | 2.0-2.3% |

| Dec Projections | 2.6-3.0% | 2.5-3.0% | 2.3-2.5% | 2.0-2.3% |

| Unemp. Rate (4Q) | 5.0-5.2% | 4.9-5.1% | 4.8-5.1% | 5.0-5.2% |

| Dec Projections | 5.2-5.3% | 5.0-5.2% | 4.9-5.3% | 5.2-5.5% |

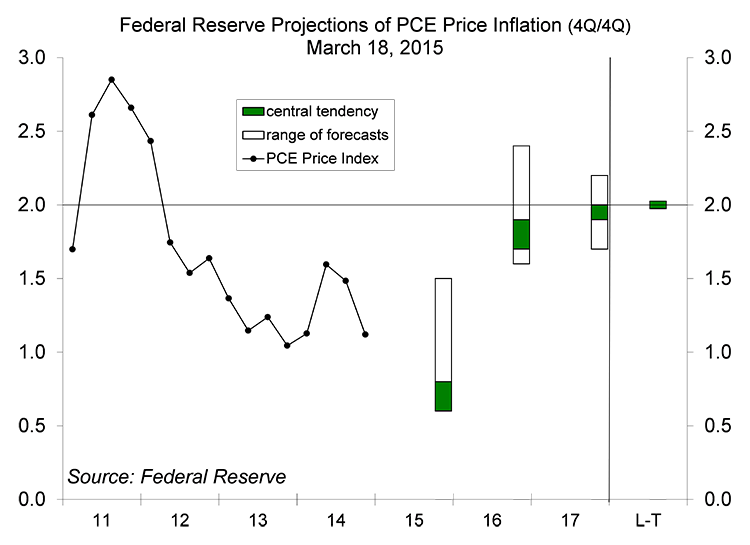

| PCE Price Inf. (4Q/4Q) | 0.6-0.8% | 1.7-1.9% | 1.9-2.0% | 2.0% |

| Dec Projections | 1.0-1.6% | 1.7-2.0% | 1.8-2.0% | 2.0% |

| Core PCE Infl. (4Q/4Q) | 1.3-1.4% | 1.5-1.9% | 1.8-2.0% | |

| Dec Projections | 1.5-1.8% | 1.7-2.0% | 1.8-2.0% | |

*These are central tendency forecasts, which exclude the three lowest and three highest forecasts of the Fed governors and 12 district bank presidents.

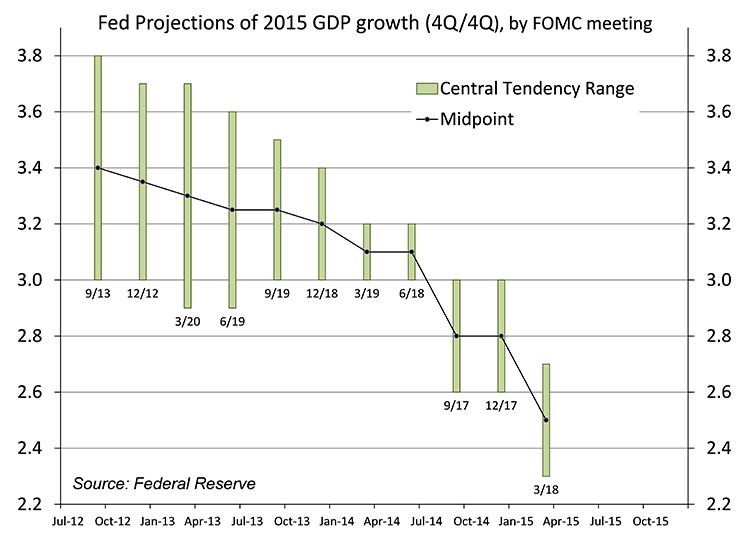

Downward revisions to the growth outlook are nothing new. Expectations have typically been revised down in recent years.

The Fed also revised lower its inflation outlook. The drop in oil prices has had a huge impact on headline inflation driving the year-over-year pace to around 0%. Lower oil prices also feed through indirectly to core inflation over time. The strong dollar has led to declines in import prices, which have restrained inflation, Yellen noted, “and will likely continue to do so in the months ahead.” At the same time, officials see these impacts as “transitory.” Yellen repeated that, before raising short-term interest rates, Fed officials want to see further improvement in the job market and be “reasonably confident” that inflation will move back to the 2% goal. That should happen as the job market strengthens and transitory inflation impacts fade, but Yellen indicated that there was no precise definition of “reasonably confident.” Fed officials will remain focused on the job market, wages, and inflation expectations.

While the dots in the dot plot continued to suggest no clear consensus on the timing and pace of rate hikes, they did generally move down, implying that most Fed officials expect the initial rate hike to arrive after the June policy meeting and further rate increases are expected to arrive more slowly.

In recent weeks, the Fed funds futures market had priced in a slower policy outlook than most Fed officials. However, while Fed officials have now revised their policy outlooks down, so too has the market, which still expects rate hikes to come much more slowly than even the most dovish Fed officials. The fixed income and currency markets were encouraged by the less aggressive Fed policy outlook, but the Fed is still moving toward raising rates at some point. Short-term interest rates will still have to rise at some point. The data will dictate when.

*When the Earth laps Mars (which is on an outer orbit around the Sun), it appears to travel backward in the night sky. In a much better analogy, the Financial Times described the Fed’s action (appearing to move toward tightening while actually expecting to be less aggressive) as “moonwalking.”

(c) Raymond James