“The secret to my success is that I buy when everyone else is selling and I sell when everyone else is buying.”

- Sir John Templeton

There were several charts that caught my eye this week. The first is a chart that tells us the likely annual return for the S&P 500 Index will average just 2.25% over the next ten years. Many valuation measurements support a period of probable low future returns, but this particular data is different – it looks at the percentage of household equity ownership.

Think of it this way: It looks at how much potential buying demand there is for stocks from households. When fully invested in stocks there is less available demand to drive prices higher. When under invested the opposite is true. You’ll see that the data shows that returns are higher after periods of low ownership and lower after periods of high ownership.

There were just two prior periods of higher equity ownership than where we sit currently. One was the market peak in March 2000 and the other in October 2007. Unfortunately today, the percentage of household equity ownership is approaching the level reached at the market peak in 2007.

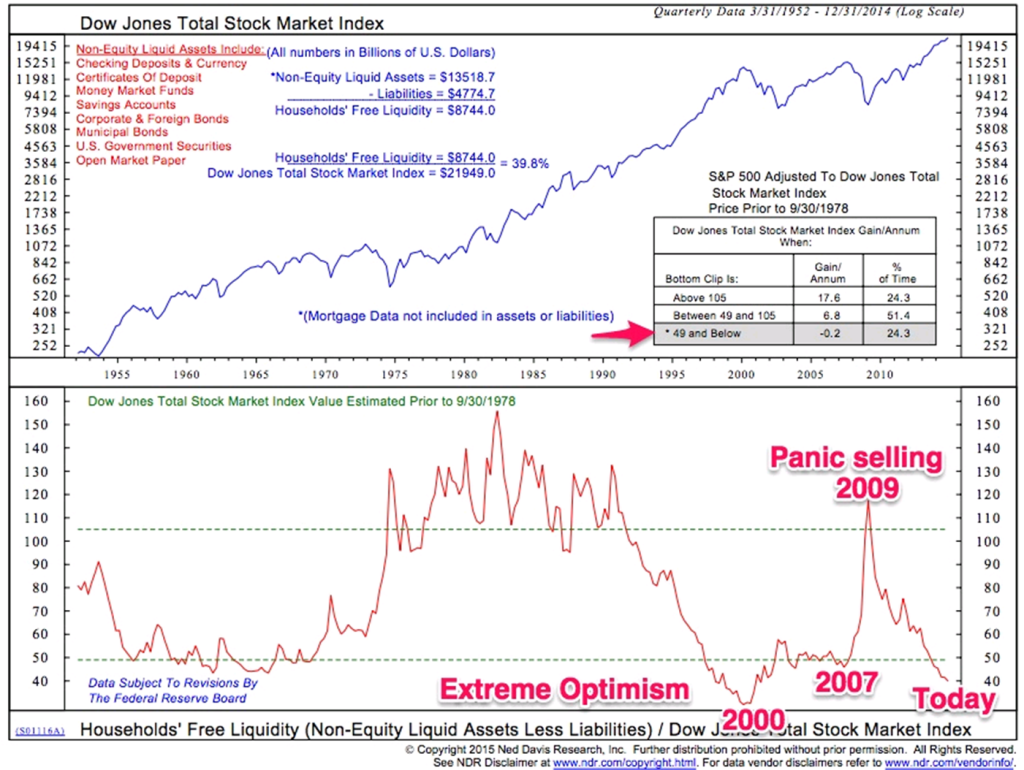

The second chart I share looks at non-equity liquid assets. The idea here is to see how much free liquidity is available to buy stocks. If you ever have wondered if investors buy and sell at the wrong time this shows that data in real time. Let’s call it “investors behaving badly”. Show the chart (below) to your client the next time his emotions look to overtake logical reasoning. The great Sir John Templeton’s wisdom rings in my head.

Finally, I asked Ned Davis Research if I could share with you a recent research piece that Ned shared with his institutional clients like CMG. In it Ned takes the research on their popular “Big Mo” (Momentum) indicator back to 1929. As you’ll see, it remains modestly bullish at present.

Given the high level of household ownership and high current market valuations, risk is elevated. I believe that now is the time to be focused on risk management and become more tactical in approach. I share some ideas today.

This week’s post is short. I hope you find it helpful.

Included in this week’s On My Radar:

- What the Percentage of Household Equity Ownership Tells Us About Probable Future Returns

- Investors Behaving Badly

What the Percentage of Household Equity Ownership Tells Us About Probable Future Returns

Here is how you read this chart. First, the blue line shows the percentage of household financial assets invested in equities. The dotted black line plots the actual rolling 10-year returns of the S&P 500 Total Return Index.

Correlation measures how closely the market’s rolling 10-year returns follow the Household Equity Percentage. A correlation of 1 is a perfect match. A reading between 0.80 and 1.0 reflects a very high correlation. You can see it visually in how closely the dotted black line follows the blue line.

The red arrow at the top of the charts shows the ownership at the market peak in 2000. The left vertical scale shows that households had 65% of their money invested in equities at the market peak in 2000. It accurately identified the 10-year period of negative returns that followed.

The smaller red arrow marks the percentage of equity ownership at the market peak in 2007. Same story.

Take a look at the green arrow at the market bottom in 2009. Great annual returns followed but were individual investors prepared to seize that opportunity? Then, fear in the air was palpable.

The orange circle shows where we are today. Expect low forward returns, be risk focused, stay tactical and patient – a better buying opportunity remains ahead.

Investors Behaving Badly

Warren Buffett says to be fearful when others are optimistic and optimistic when others are fearful. Household equity is one measure of over and under ownership. The next chart takes a look at “Household Fee Liquidity”. Think of it as available money that can be used to buy equities.

The red arrow points to the gain per annum when household liquidity is low. Not surprising – returns are low (and in this case negative). The bottom section of the chart shows where we are “today”.

There is little available liquidity today. It is lower than it was in 2007 and lower than it was in every other period except 2000. Personally, I think 2000 to be an outlier.

In regards to “investors behaving badly”, take a look at the amount of available liquidity at the market low in 2009 (“Panic selling 2009”). The sad truth, perhaps, is that the behavior of the many creates the opportunity for the few.

In the “what you can do” category, here are a few ideas as it relates to portfolio equity exposure (the point is to have a plan in place that protects you from the really big declines):

- Set a plan in place. Markets can certainly go higher.

- While the various “valuation”, “household equity ownership” and/or “free liquidity” data are helpful at identifying probable forward returns, they are less valuable risk timing tools.

- The great Paul Tudor Jones suggests a trailing 10% stop loss from the market’s high water point is prudent. Not a bad idea but needed too is a rule to get back in or remove set hedges.

- Some like a simple 200-day moving average to identify trend, some a 1% move below that MA line. Hedge or sell on negative cross. Remove hedges or rebuy back in on positive cross.

- I like a 13/34-Week Exponential Moving Average cross (see Trade Signals below for detail)

- My favorite is NDR’s “Big Mo”

I’m excited to share, with permission from NDR, Ned’s recent research piece on Big Mo.

Ned Davis on Big Mo (Momentum)

Ned has a very humble and balanced way. This past Monday, Ned took his research back to 1929 (with the help of market data from Kenneth French). I found the deeper data set encouraging. While the process has run live for many years, prior data went back to just 1980.

Here is the link to the full piece (a quick read). Click here for NDR disclosures. NDR’s is an independent research firm. If you are a professional advisor or institutional investor, you can reach out to Dan Dortona, in their Boston office, at 617-279-4860 to learn more about NDR. (Please note: I am simply an NDR client and do not get compensated in any way. Just a fan.)

Personal note

Spring here in the northeast is being ushered with another snow storm. It is peaceful watching the snow fall outside but it is getting way too old. Warmer weather can’t come soon enough. Looks more like global cooling than it does global warming.

As a crazed soccer family, the eight of us are bundling up and heading to tonight’s Philadelphia Union vs. Dallas game. The forecast is for temperatures in the high 20s. The upside is that the ice cold beer should stay ice cold. Seems a family room with a warm fire going is the better move but what the heck – we are going for it.

Here is to hoping that this is the last snow storm. I’m ready to see some flowers. Come on spring!

I hope you find this week’s post both interesting and useful.

Have a great weekend!

With kind regards,

Steve

Stephen B. Blumenthal Founder & CEO CMG Capital Management Group, Inc.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM: Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456. Please read the prospectus carefully before investing. The CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA. NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, or the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

© CMG Capital Management Group