"We've gotten used to thinking of a zero interest rate as normal—it's far from normal."

- Fed Vice Chairman Stanley Fischer

I wrote a piece in Forbes this week titled “Rate Hike Ahead, Bond Model Says Sell”. The gist of the piece is about a tug of war between opposing views on the direction of interest rates. The outcome of this contest will enrich some and demoralize others.

Trend evidence suggests that rates are moving higher. As you may know, we rebuilt a model with the help of our friends at Ned Davis Research that the late great Marty Zweig created in the mid-80s. It signaled this week that the trend in rates has changed, suggesting it is best to shorten maturity exposure. I share a few ideas in the Forbes piece.

I’m not sure just how valuable a 10-year Treasury paying 2.10% is to a portfolio. Yet the total return would be very nice indeed should rates fall to 1% by year end. Conversely, because the starting place is low, the risk of loss is exponentially elevated than if rates were at, say, 4%. I conclude that now, more than ever, is the time to have a tactical process in place that can help you manage your duration exposure.

Included in this week’s On My Radar:

- Rate Hike Ahead – Zweig Bond Model Says Sell (Shorten Maturity Exposure) – Forbes by Steve Blumenthal

- Don’t Fight the Fed or the Tape – Updated Chart

- Trade Signals – Sentiment Neutral, Trend Bullish, Zweig Bond Model “SELL” Signal

Rate Hike Ahead – Zweig Bond Model Says Sell (Shorten Maturity Exposure) – Forbes by SB

In addition to the Zweig Bond Model chart (and process description), there is a great chart we’ve recently updated that shows just how much money is gained or lost for every 1% move in interest rates, i.e. should rates move from 2% to 3%, 3% or 4%... or 2% down to 1%. Feel free to share that chart with your clients if you find it helpful/relevant.

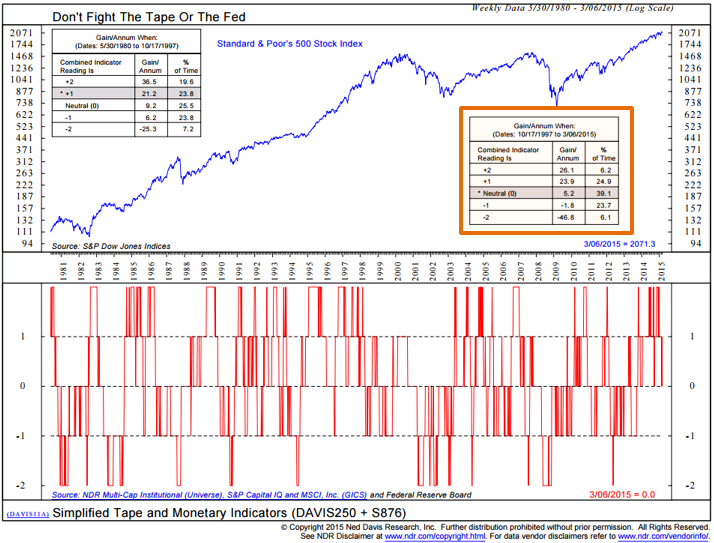

Don’t Fight the Fed or the Tape – Updated Chart

Along the same lines, let’s take a look at one of my favorite charts.

Here is how to view the chart:

The chart's upper clip plots the Standard & Poor's 500 Stock Index weekly close. The chart's bottom clip plots the Simplified Tape and Monetary Indicators. These indicators are a combination of NDR's Big Mo Multi-Cap Tape Composite (DAVIS250) and the 10-Year Treasury Yield percentage (S876).

The current reading is “0”. As evidenced by the S&P 500 gain per annum based on composite indicator levels (Orange Highlighted Box), this indicator supports the notion that we should not Fight the Tape or the Fed.

NDR's Big Mo Multi-Cap Tape Composite Model was created to give a composite reading on the technical health of the broad equity market. The model aggregates the signals of over 100 component indicators and generates a reading between 0% and 100%, reflecting the percentage of the component indicators that are currently giving bullish signals for the S&P 500 Index. The model provides a single summary reading of the U.S. stock market's technical health based on historical analysis of many trend and momentum indicators. Chart S876 illustrates when 10-week Treasury Yields are historically lower than their 70-week linear regression, the S&P 500 has produced larger gains.

The combined indicator can produce a score from -2 (both indicators bearish) to 2 (both indicators bullish). When these two indicators are used in conjunction, they produce a historically strong timing indicator. Source: NDR

In short, it is a systematic and disciplined weight-of-evidence approach that identifies the stock market’s technical health. Please refer to the disclosure language at the bottom of this email. Past performance cannot guarantee future performance.

The deteriorating in the Don’t Fight the Fed or Tape Model and the Zweig Bond Model, for that matter, is largely coming from the recent rise in interest rates.

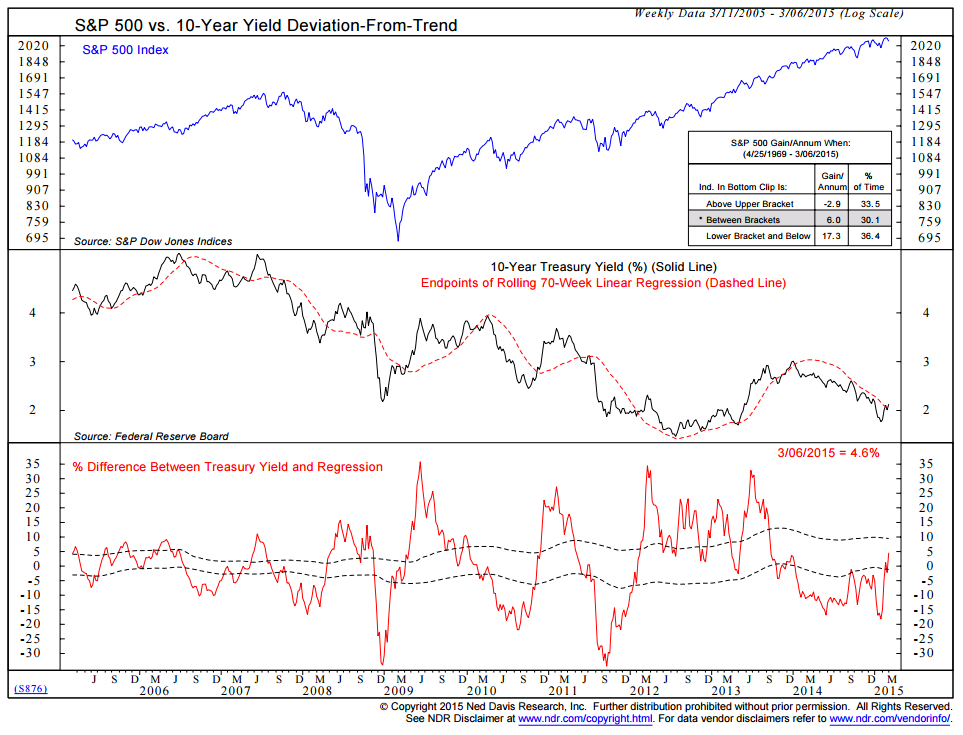

Additionally, if you are a true quant geek like me, here is chart S876 that NDR references above. All others, grab a beer and just keep moving – this one, as with too much beer, might make you a bit dizzy. Combine both at your own risk.

S&P 500 VS. 10-YEAR YIELD DEVIATION-FROM-TREND – Explained by NDR (Again, for Quant Geeks Only):

This chart uses a variation on a deviation-from-trend calculation to create an interest rate indicator for the stock market using the benchmark 10-year Treasury note yield. A traditional deviation-from-trend indicator compares the current data (in this case, the current 10-year Treasury yield) to a longer-term moving average (representing the "trend") of the data and plots the percent difference (the "deviation") between the two. In this chart, instead of a simple moving average to represent the trend, we use the weekly endpoint of a rolling 70-week simple linear regression trend-line of the T-note yield (dashed line, middle clip). That is, each week we use the last 70 weeks of data to calculate a best-fit linear regression line through the Treasury note yield data and the endpoint of the regression trend-line is plotted for that week. We then determine the percent difference between the actual 10-year yield and the endpoint of the trend-line and that difference is plotted in the bottom clip of the chart.

To determine whether a given differential should be considered high or low, we plot moving standard deviation bands around a three-year (156-week) moving average of the differential (+/- 0.4 SD above and below). By doing this, roughly a third of the time historically is spent above the upper bracket (indicating rising interest rates), a third of the time is spent below the lower bracket (falling interest rates) and a third of the time is spent between the brackets (neutral rates). The use of moving standard deviation brackets allows for longer-term shifts in the level and volatility of the indicator. Our analysis based on data from 1969 to present has found that the S&P 500 has shown sub-par returns on average when the differential has been above the upper bracket, while it has posted strong annualized gains when the differential has been below the lower bracket (neutral readings have been associated with average returns). The results on the chart reflect the full history since 1969, but only the latest 10 years of data are plotted for better visibility.

The concept behind the chart is that the rolling regression trend-line could reflect a simplistic estimate of where investors might think interest rates "should" be and incorporates the tendency for investors to extrapolate an uptrend or downtrend in rates into the future, which a simple moving average does not do. This indicator thus gives a different perspective on where current bond yields are relative to their recent trend and the results show that it has been a useful timing indicator for the stock market. Source: NDR

Personal note

I’ve been working on two new white papers that we hope to publish shortly. One is on Diversification and Correlations and the second discusses how to pull it all together and create a “Total Portfolio Solution” that targets a certain return and controlled risk objective. It has been a great deal of work and, frankly, a lot of fun. I know…Susan tells me I need to get a life.

Daughter Brie is back home for the weekend having just returned from her final spring break trip. Real life for her is set to start in May. I remember my dad pulling me aside, with my graduation hat in hand, telling me it’s all downhill from here. I’d have to say it really hasn’t turned out to be that way. The ride has been pretty great – for which I’m grateful. A big dinner is planned for tonight and I’m showing up hungry. I hope you have something fun on the weekend schedule. Wishing you the very best.

Have a wonderful weekend!

With kind regards,

Steve

Stephen B. Blumenthal Founder & CEO CMG Capital Management Group, Inc.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM: Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456. Please read the prospectus carefully before investing. The CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA. NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, or the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

(c) CMG Capital Management Group

© CMG Capital Management Group