“Academics operate with an expression called recency. It basically means that we, as humans, assign greater relevance and importance to more recent events than we do to more distant ones. When equities delivered exorbitant returns during the great bull market of 1982-2000, it became the norm to expect double digit returns from equities, despite the fact that equities had rarely delivered such high returns before the 1980s.”

- Niels Jensen, Absolute Return Partners, March 2015

At the beginning of each month, I like to look at a series of valuation metrics: Median PE, Price to Sales and Price to Operating Earnings. Let’s look at them today.

The logic, of course, is simple. When expensively priced, reduce exposure and reduce return expectations. When inexpensively priced, overweight exposure and increase return expectations. Oh! but to be patient – that’s the hard part.

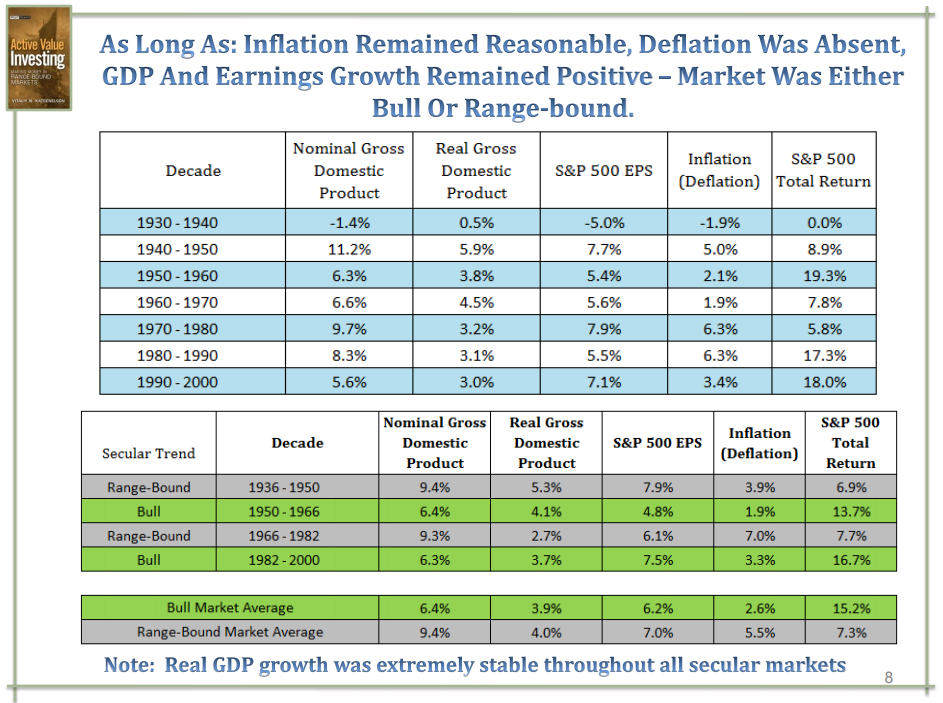

Niels Jensen is a long-time friend, hedge fund manager and CMG partner and writes what I think is a must read quarterly client letter. I thought he did an outstanding job in his most recent piece talking about unrealistic investor expectations. Niels highlighted the the following chart with the intent in helping his clients get a sense of the historical returns for each decade since 1930 (show this one to your clients). The objective is the remove recency bias.

Looking at the S&P 500 Total Return decade by decade (far right column) might be a good starting point in helping clients set reasonable return expectations. I’m not sure about your individual clients but I know from experience that return expectations tend to change based on recent gains or losses.

Source: Vitaliy Katsenelson Source: Absolute Return Partners – Tigers in Africa

Missing in the data is the “lost decade” of returns from 2000-2009. That decade achieved a total return of just -0.99% – the first negative decade in the series (including the 1930s). Overall, from 1930-2009 the annualized return with dividends was 9.37%. Source: Calculator

According to my friends at Ned Davis Research, Inc., during the average buy-and-hold stock market, an investor spends 77% of his or her time recovering from cyclical downturns in the market. 77% of the time – that’s telling. It’s in the mathematics of loss. Remember that it takes a 100% gain to overcome a 50% decline.

My two cents is that many investors expect 9% to 11%; yet, we currently live in a world of 4% to 5%. If you are an older dog like me, you’ll remember your clients expecting 18% per year or more in the late 1990s and 2000. My client, Roberta, left CMG in December 1999 after I grew her account 30% over the prior two years. She was ultra-conservative and positioned accordingly.

The problem, of course, was that 30% paled in comparison to the 51.4% the S&P 500 gained in 1998-1999 or the 159.14% the NASDAQ gained over those two years. She told me she was going to a Merrill Lynch broker and was investing in “safe stocks”. Her $1 million account fell to less than $500,000. Had she stayed, that same $1 million would have grown to over $1.3 million. It is tough to compare a conservative bond strategy to stocks, but I showed her the forward return probabilities back then and I wrote frequently about a technology bubble. Unfortunately, that didn’t help. She was in her mid-60s then. Safe stocks. Right.

As a quick aside: Do you remember those NASDAQ gains in 1998 and 1999? An interesting data point is that more than three quarters of all the money invested in Fidelity mutual funds was concentrated in their technology funds. The NASDAQ crashed some 75% by mid-2002 and has only just recently crossed back above 5000. It took about 15 years to get back to even but who was really able to ride that bumpy ride back. The bigger question is: Who took advantage of the buying opportunity that crash created?

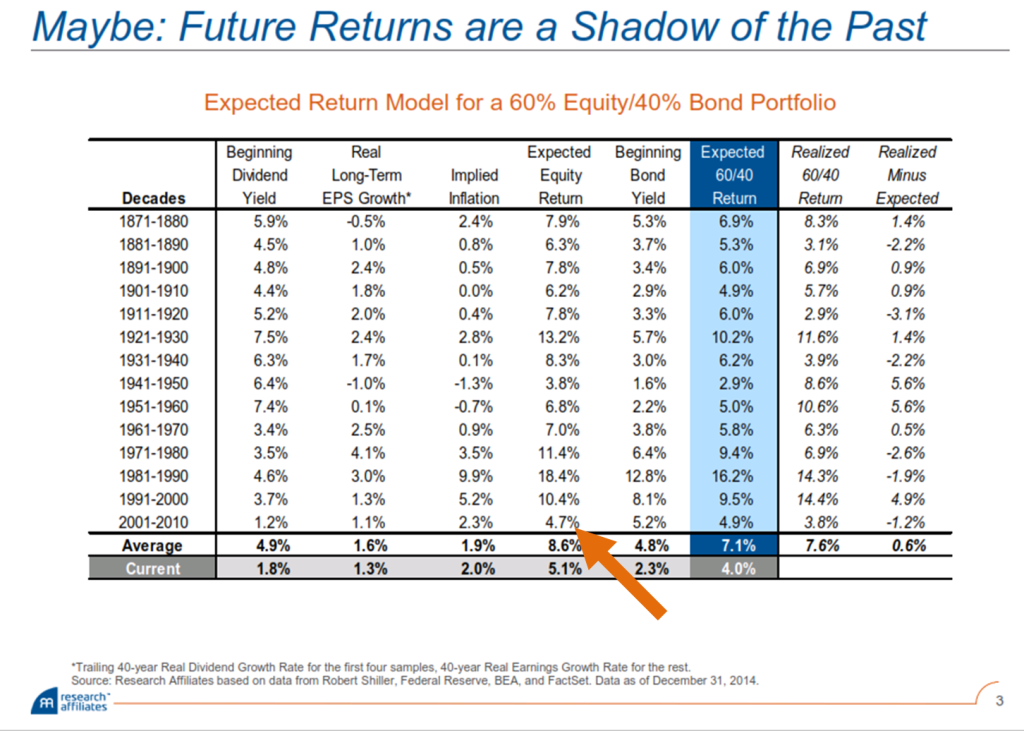

I believe we can get a good fix on what forward returns will be. Take a look at the following from Rob Arnott’s shop. His research shows that by knowing the beginning dividend yield, EPS Growth and Implied Inflation, one can fairly accurately predict the Expected Equity Return over the coming 10 years.

Though the data doesn’t perfectly align to the above decade chart, it is close enough in my book. Take a look at the Expected Equity Return for the 2001-2010 10-year period of time. In 2001, the expected forward 10-year annual return was 4.7% per year (orange arrow next chart). Not 9%, 11% or the 18% many were hoping for. The actual compounded annual growth rate or return, using the source calculator for the S&P 500 Index was just 1.36%.

A 10-year time frame is one thing but zeroing in on what returns might be over the next year or so is far more challenging. I take a crack at that too this week with another great valuation chart from NDR (hint: the result is negative over the coming 3 to 24 months).

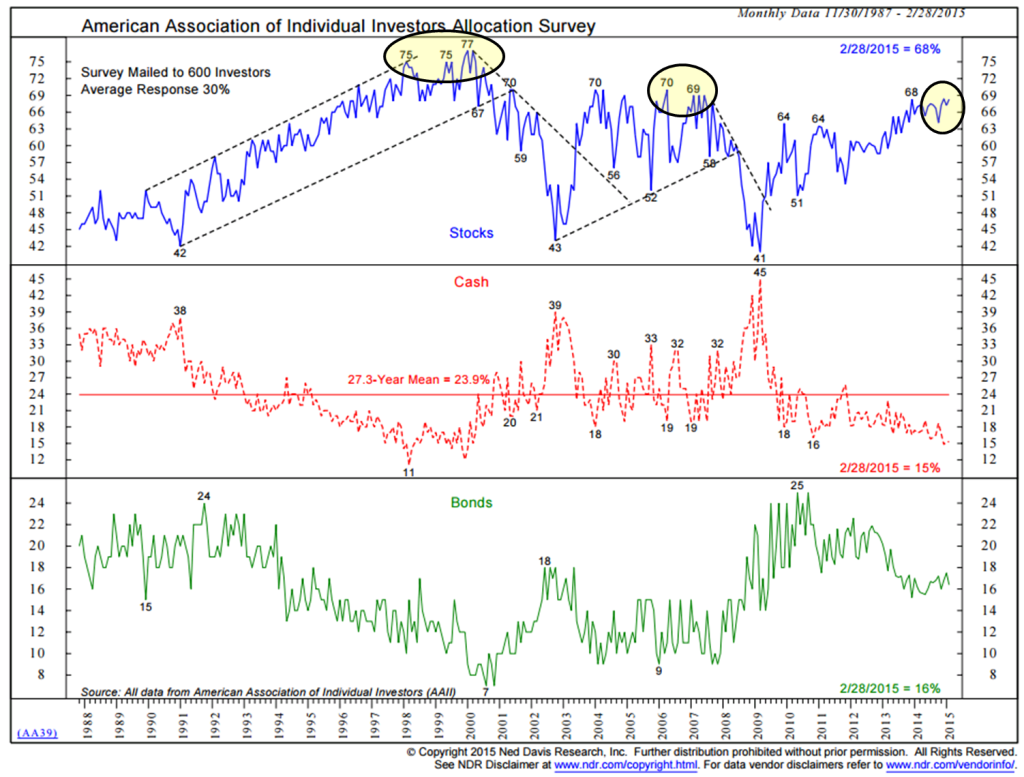

Let’s also take a look at what has been driving the market higher. Some argue that individual investors are still on the sidelines. I don’t think so and I show evidence that they are almost as fully invested as they were at the 2000 and 2007 market peaks. So if they are nearly “all-in”, who’s been pushing up prices? I include a note from Art Cashin this week – it is corporations buying their shares back and taking on more debt to do so.

So let’s dive in. It prints long but reads fast.

Included in this week’s On My Radar:

- Buyback Fever – Corporate Repurchases Continued at a Blistering Pace

- Individual Investors Are Nearly All-In and So Are the Pros

- Valuations Are High

- My Thoughts on Risks

- Trade Signals – Sentiment Turns Negative, Trend Remains Bullish

Buyback Fever – Corporate Repurchases Continued at a Blistering Pace.

Here’s a bit from Bloomberg (courtesy of Art Cashin’s March 3, 2015 letter):

“Stock buybacks, which along with dividends eat up sums of money equal to almost all the Standard & Poor’s 500’s earnings, vaulted to a record in February, with chief executive officers announcing $104.3 billion in planned repurchases. That’s the most since TrimTabs Investment Research began tracking the data in 1995 and almost twice the $55 billion bought a year earlier.

Even with 10-year Treasury yields holding below 2.1 percent, economic growth trailing forecasts and earnings estimates deteriorating, the stock market snapped back last month as companies announced an average of more than $5 billion in buybacks each day. That’s enough to cover about 2 percent of the value of shares traded on U.S. exchanges, data compiled by Bloomberg show.

Records show that companies have bought over $2 trillion of their own shares since the low of 2009. They are on a pace to spend about 95% of their earnings on buybacks and dividends.

No wonder we’re at new highs.”

As I mentioned, the probability of a pickup in global capital flows, fueled by an advancing sovereign debt crisis and distrust for government debt, and piggy backing record corporate share buy-backs, could further propel the market higher. We’ll see.

Individual Investors Are Nearly All-In and So Are the Pros

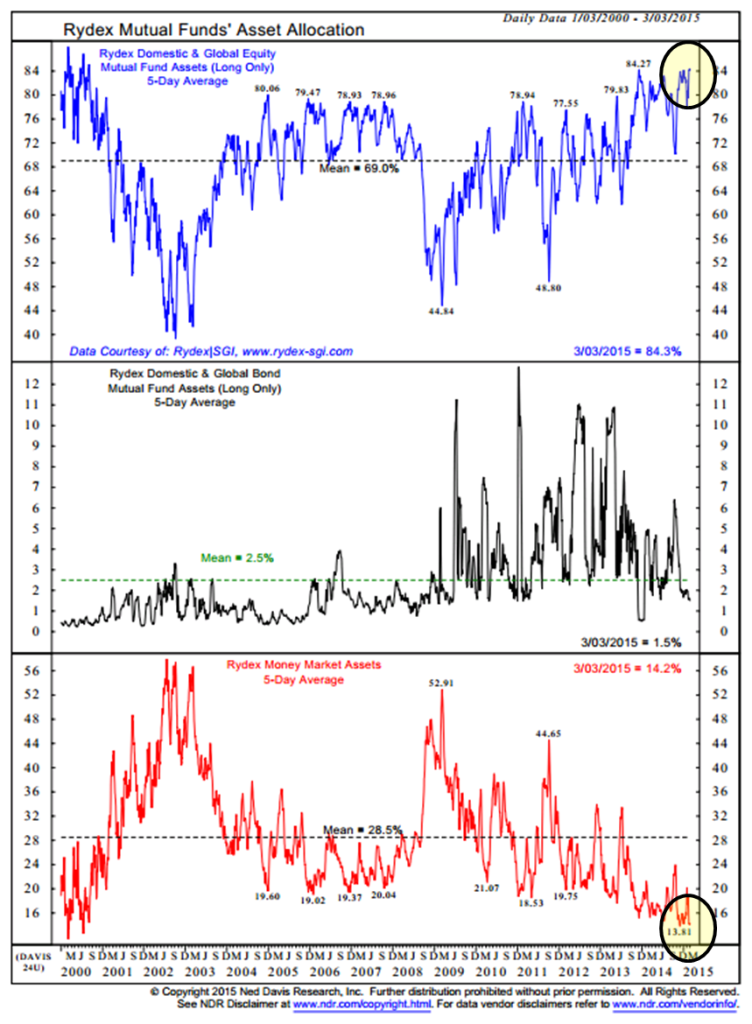

I really like this next chart. It tracks money allocated in Rydex Mutual Funds. A lot of professional investors use these funds. Note the yellow circle in the upper right. It shows us that 84.3% of the money in Rydex Funds is allocated to Domestic and Global Equity funds. It was 79% in 2007. Also note the record low level of money market assets (yellow circle bottom right). As is the case with individual investors, the pros are also nearly all-in.

Valuations Are High

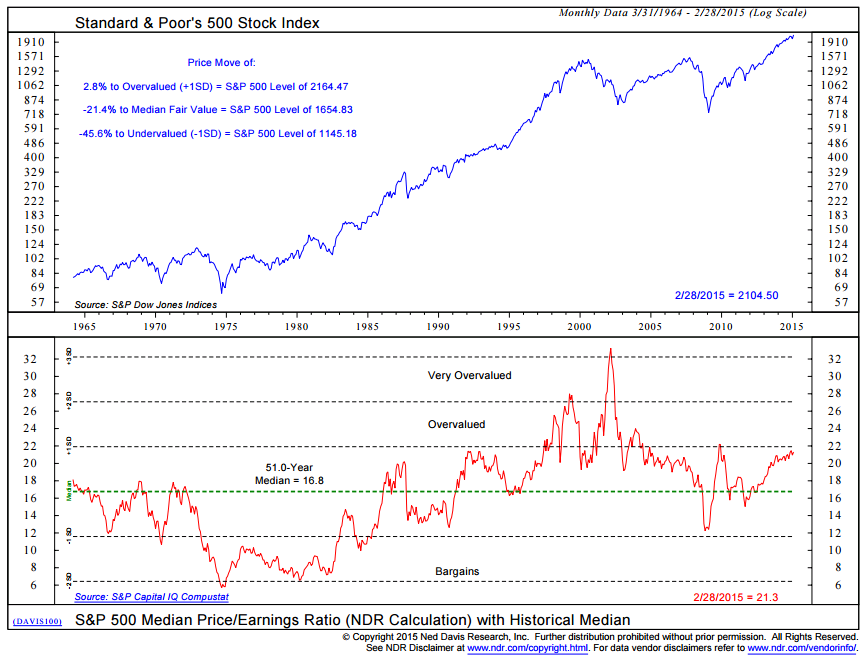

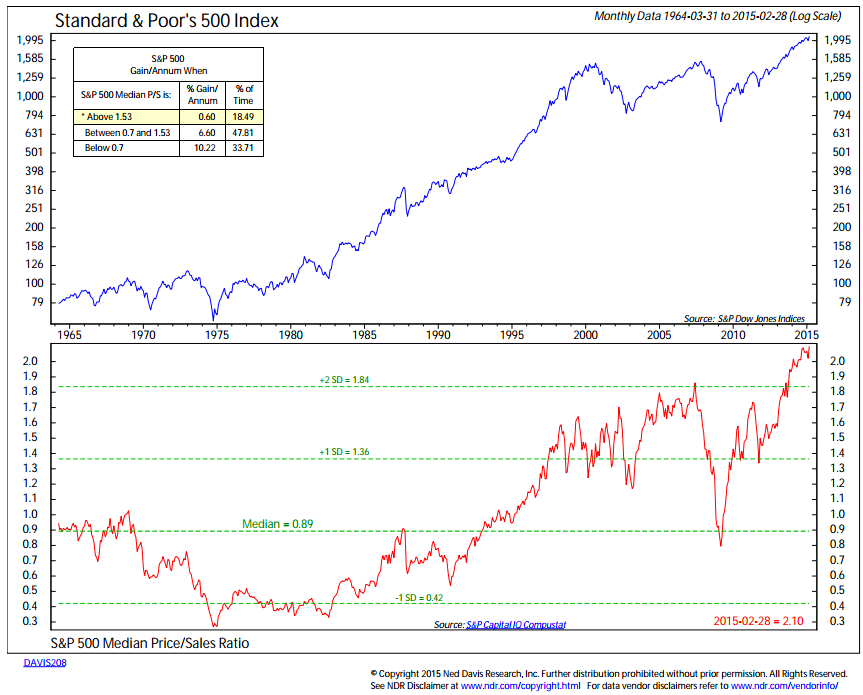

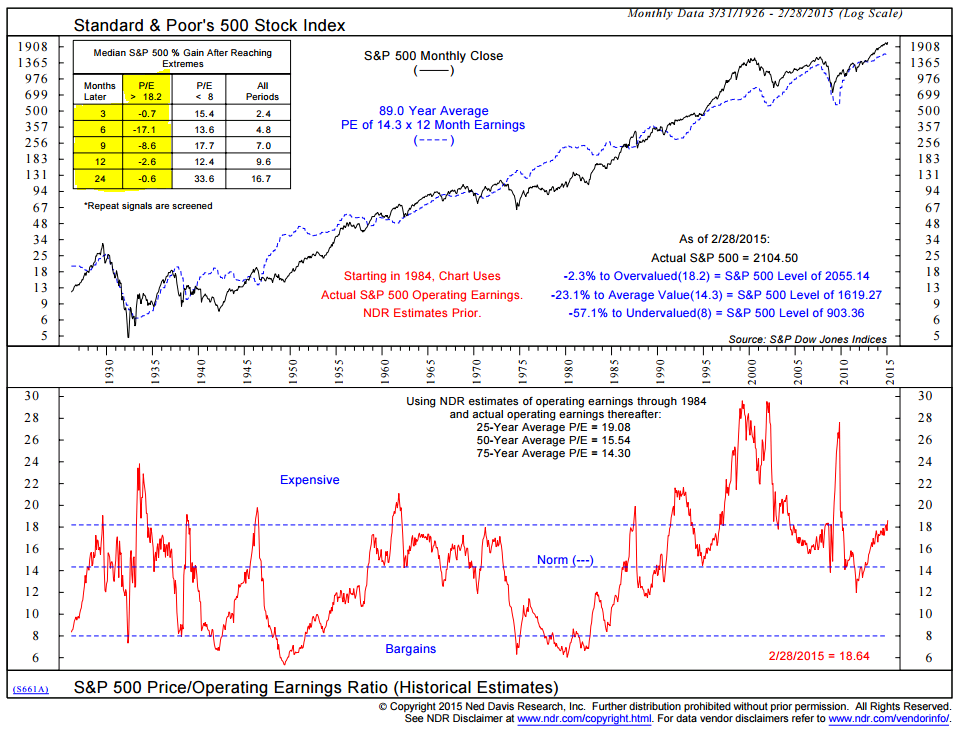

Let’s take a look at Median PE, Price to Sales and Price to Operating Earnings.

Median PE

Median Price to Sales

Price to Operating Earnings

I highlighted the returns that followed periods when the Price to Operating Earnings Ratio was above 18.2. Shown are 3, 6, 9, 12 and 24 months later. Also note how well the market did when the ratio was less than 8.

One final look at Valuations (in the above charts the data is based on actual reported earnings and not over hyped Wall Street Analysts’ estimates).

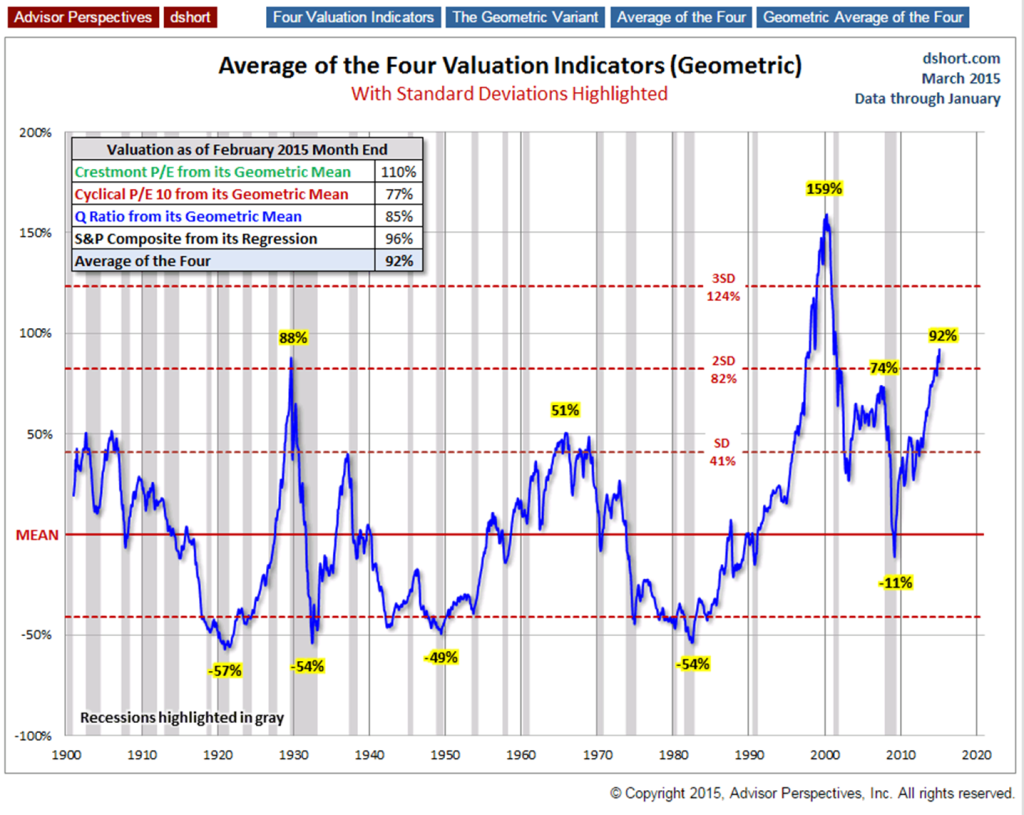

Average of the Four Valuation Indicators – via Doug Short’s blog

Last month, the average of the four valuation indicators was 86% overvalued. It is 92% overvalued through February.

I shared the next chart with you last week. In the “We are here” line, insert 92%. We are now two months at more than 2.5 standard deviations above the mean and just one prior period spent more than one month that far above fair value (as measured by mean). That was the March 2001 to November 2001 period. If you were an odds maker, what would you be thinking? I know what I’d think. “Rut Ro Rastro” Channeling my inner Astro – do you remember Astro from The Jetsons cartoon? – ok…somebody get me some meds.

Also, I thought this next chart was very clever.

Here is a scatter graph with the market valuation on the vertical axis (log scale) and interest rates on the horizontal axis. I’ve included some key highlights: 1) the extreme overvaluation of the tech bubble, 2) the valuations since the start of last recession, 3) the average P/E 10 and 4) where we are today.

Source: Doug Short blog (I find his site to be a chart geek’s dream land)

{kind=link}

My Thoughts on Risks

The problem in the world is excessive debt and it cannot be rectified unless you have either a hyperinflation or a hard debt deflation like the 1930s.

Corporations have taken advantage of borrowing at ultra-low rates and have used that money to purchase their stock. Financial engineering at its best. Yet earnings are in decline here and globally. A concerning combination. Call me crazy, but I’m of the belief that an inflight of fresh new capital (a global rush to dollars/safety) may propel U.S. stocks even higher.

With negative interest rates in Europe and a Fed edging ever closer to lifting U.S. rates (expectations are for June or September), the advantage goes to the U.S. dollar with U.S. assets the beneficiary of global capital flows. That’s my thesis for now as we watch the equity market step higher.

Remember the card game called Acey Deucey? You are dealt two cards and you split them. The dealer would then flip a third card. If that card number fell in-between your two cards, you’d win the pot. If you lost, you’d have to double the amount of money in the pot and the turn would move to the next player. The best combination was an Ace and a 2 (or deuce). This gave you the best odds to win but nonetheless a risk it was and nerves were tested – especially the bigger the pot grew.

It kind of feels a bit like Acey Deucey today except we are holding a 5 and a 10. As much as I know about global currency flows, valuation, supply and demand dynamics, and human behavior, I can’t help but wonder what it is that I don’t know. We live within a highly complex system with many moving parts.

Risk is high and the bet may pay off but recessions happen (often two times each decade) and when the bubble is fully inflated, the bear market declines are at their greatest. Similar to 2000 and 2007, now is the time to have a stop-loss or hedged risk management game plan in place.

I was interviewed on a radio program last week and the host asked, “What keeps you up at night?” I think, globally, we need to face the hard reality of unmanageable debt. It involves restructure (some form of default) which means underfunded pensions will become more underfunded and it means banks will take hits, investors will take hits and economies will slow.

In the meantime, all of this is confusing to individuals as they, not living in our professional investment world, have their other important interests. But lack of education and planning can prove painful – like it did to Roberta. Far easier to feel good and project yesterday’s returns forward. It is just so emotionally difficult to stay disciplined.

When valuations are high (like today), history tells us to expect very low forward 10-year returns. The bigger challenge, and coming opportunity, is for both of us to prepare our clients for a period of high forward 10-year returns. Their confidence to invest will be challenged so some advance prep work is required. It rarely feels like an opportunity during -40% bear market declines (times of stress).

Follow the valuation charts to assess risk and opportunity. Use a risk management or hedged process (like Big Mo or 13/34-Week EMA – see Trade Signals). It is time to be tactical and know that a period of low valuations and high potential forward returns will present itself again. Seek gains but with a plan to risk protect. Patience and risk management today will lead to greater opportunity tomorrow.

Honestly, I feel I failed Roberta. I wish I was able to keep her on plan. I guess with experience, we gain great conviction in our process. I do hope I’m able to help the next Roberta.

Trade Signals – Sentiment Remains “Excessively Optimistic”, Trend Bullish

Included in this week’s Trade Signals:

- Cyclical Equity Market Trend: The Primary Trend Remains Bullish for Stocks

- Volume Demand Continues to Better Volume Supply: Bullishfor Stocks

- Weekly Investor Sentiment Indicator:

- o NDR Crowd Sentiment Poll: Extreme Optimism (short-term BEARISHfor stocks)

- o Daily Trading Sentiment Composite: Extreme Pessimism (short-term BEARISHfor stocks)

- The Zweig Bond Model: The Cyclical Trend for Bonds Remains Bullish

Click here for the full piece.

Personal note

The five boys are out shoveling and it sure is beautiful outside. About a foot of new snow and three of the five got the much prayed for “school is cancelled for today” phone call. Not so lucky for thing two and thing three but a two hour delay eased the pain.

Warm weather can’t come soon enough. If you are in the south or the west, smile and take in the warmth. And please send some our way!

The knee is on the mend, the Philadelphia Flyers won a big game last night (struggling to make the playoffs) and tomorrow is opening day for my favorite MLS soccer team – the Philadelphia Union. I’m looking forward to a cold Victory Hop Devil IPA, a cheesesteak, and a “W” for the home team.

Hoping you have plenty of shovel-ready helpers in your house and a warm fire inside. Come on spring!

Have a great weekend!

With kind regards,

Steve

Stephen B. Blumenthal Founder & CEO CMG Capital Management Group, Inc.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM: Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456. Please read the prospectus carefully before investing. The CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA. NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, or the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

Cashin’s – UBS disclosure:

Opinions expressed herein are subject to change without notice and may differ or be contrary to the opinions or recommendations of UBS Wealth Management Research, UBS Investment Research or the opinions expressed by other business areas or groups of UBS as a result of using different assumptions and criteria. Full details of UBS Wealth Management Research and / or UBS Investment Research, if any, are available on request. Any prices or quotations contained herein are indicative only and do not constitute an offer to buy or sell any securities at any given price. No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness, reliability or appropriateness of the information, methodology and any derived price contained within this material. The securities and related financial instruments described herein may not be eligible for sale in all jurisdictions or to certain categories of investors. UBS AG or any of its affiliates (“UBS”), its directors, officers and employees or clients may have or have had interests or long or short positions in the securities or related financial instruments referred to herein, and may at any time make purchases and/or sales in them as principal or agent. UBS may provide investment banking and other services to and/or serve as directors of the companies referred to in this material. Neither UBS its directors, employees or agents accept any liability for any loss or damage arising out of the use of all or any part of these materials.

This material is distributed in the following jurisdictions by: United Kingdom: UBS Limited, a subsidiary of UBS AG, to persons who are market counterparties or intermediate customers (as detailed in the FSA Rules) and is only available to such persons. The information contained herein does not apply to, and should not be relied upon by, private customers. Switzerland: UBS AG to institutional investors only. Italy: Giubergia UBS SIM SpA, an associate of UBS SA, in Milan. US: UBS Securities LLC or UBS Financial Services Inc., subsidiaries of UBS AG, or solely to US institutional investors by UBS AG or a subsidiary or affiliate thereof that is not registered as a US broker-dealer (a “non-US affiliate”). Transactions resulting from materials distributed by a non-US affiliate must be effected through UBS Securities LLC or UBS Financial Services Inc. Canada: UBS Securities Canada Inc., a subsidiary of UBS AG and a member of the principal Canadian stock exchanges & CIPF. Japan: UBS Securities Japan Ltd, to institutional investors only. Hong Kong: UBS Securities Asia Limited. Singapore: UBS Securities Singapore Pte. Ltd. Australia: UBS Capital Markets Australia Ltd and UBS Securities Australia Ltd. For additional information or trade execution please contact your local sales or trading contact.

©2014 UBS Financial Services Inc. All Rights Reserved. Member SIPC.

UBS Financial Services Inc. is a subsidiary of UBS AG.

© CMG Capital Management Group