Job growth remained strong in February, leading financial market participants to believe that the Fed will begin to raise short-term interest rates sooner (June) rather than later (September) and, more importantly, at a faster pace than thought earlier. The report is only one item that the Fed will consider when it meets to set monetary policy (March 17-18).

Nonfarm payrolls rose by 295,000 in February, a 3.86 million seasonally adjusted annual rate over the last four months. This is an extraordinary pace, one consistent with a sharp decline in unemployment. The unemployment rate did decline in February, but that was partly due to a decrease in labor force participation. The employment/population ratio was flat versus January, up only half a percentage point over the last year. Something’s not right with this picture.

Normally, one would put more weight on the payroll data, which are periodically benchmarked to actual payroll tax receipts (and revisions to the payroll data tend to be relatively small). Payroll estimates count jobs, not people, and an increase in multiple jobholders could overstate the payroll figure. However, the household survey asks about multiple jobs: 4.9% of employed people had more than one job in February, down slightly from 5.0% a year ago. The number of multiple jobholders rose by 58,000 over the last 12 months. In comparison, nonfarm payrolls rose by about 3.3 million.

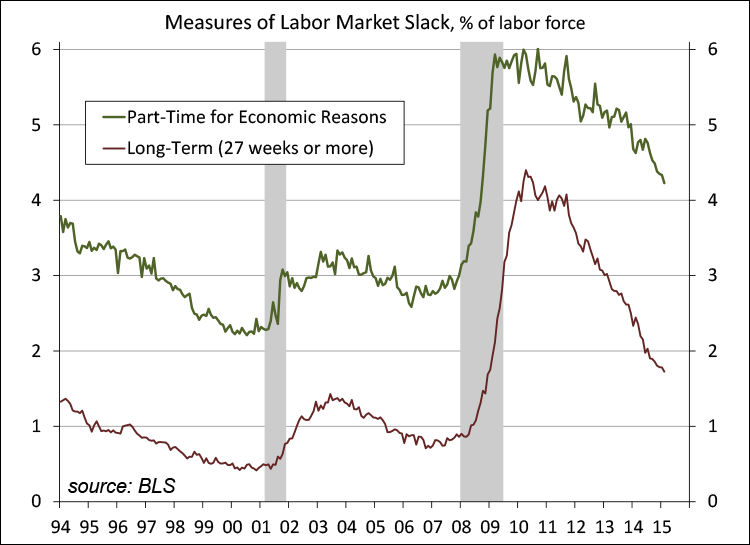

The employment/population ratio suggests that there is still a lot of slack in the job market. Other measures, including the percentage of people working part-time for economic reasons and the long-term unemployment rate also suggest that slack is being taken up, but that a large amount remains. Note that the number of people working part time because that was the only thing available has begun to trend lower.

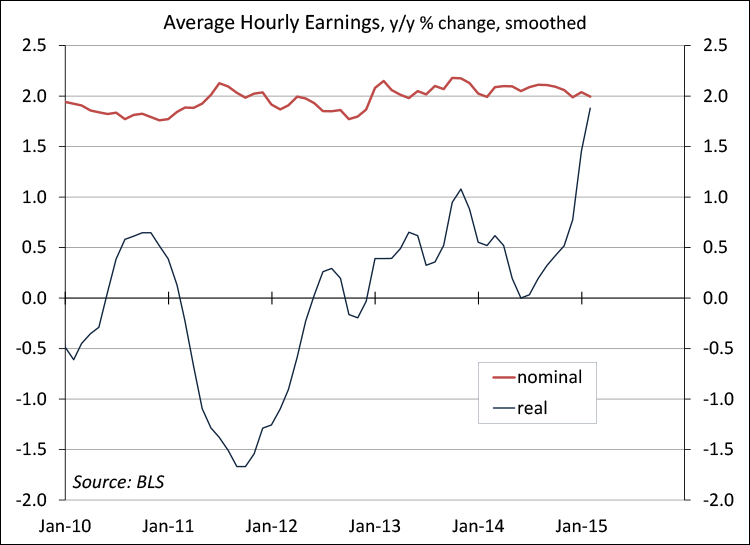

Average hourly earnings rose modestly in February, still at a lackluster pace (+2.0%) year-over-year. Faster wage gains are being seen for certain high-skilled positions, but there is no evidence of a broad-based acceleration in labor compensation. As slack disappears, one would expect to see faster wage growth. Productivity figures are choppy and unreliable, but the trend over the last year suggests a noticeable slowdown in output per worker. That could explain some of the lackluster pace in wages, but it’s most likely evidence of slack.

Nominal wage growth has struggled to keep pace with inflation in recent years. Most of the growth in consumer spending has come from job gains (the typical worker is running just to stay in the same place). However, the sharp drop in gasoline prices into January reduced inflation to about 0% year-over-year, boosting real earnings growth sharply. Combined with the recent strong pace of job growth, real consumer spending growth should be significantly higher in the near term. We may not see that in the February data, but is should be much more apparent in the figures for March and April.

(c) Raymond James