Quantitative Easing Comes to the Eurozone

March 6, 2015

It is said that imitation is the sincerest form of flattery. If so, the Federal Reserve should take a great compliment from the succession of central banks that followed it into aggressive quantitative easing (QE). The European Central Bank (ECB) will become the latest addition to this parade later this month.

Success is by no means assured. The ECB program, at least for now, is modest compared to what was done in other regions. The fabric of markets, institutions and households in the eurozone differ from the United States in ways that may limit the effectiveness of QE. Nonetheless, there are some common threads to programs across countries that bode well for the eurozone. And early returns are encouraging.

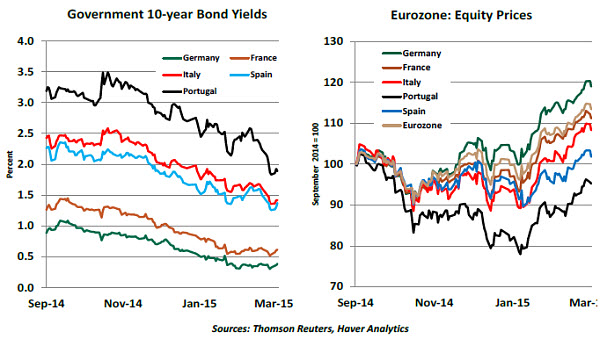

A review of how QE operates will help assess prospects for the ECB’s initiative. Its direct effect is to lower long-term interest rates. Studies of the QE programs in the United States and the United Kingdom have concluded that the effort did have a tangible role in reducing borrowing costs. Sovereign interest rates across the eurozone (with the exception of Greece) have fallen sharply so far this year, especially for the peripheral countries.

In theory, this should prompt additional leveraging, supporting spending and investment. The power of this influence may be blunted a bit in the eurozone, for two reasons. First, U.S. firms get about 70% of their financing from the debt capital markets and only 30% from banks; in the eurozone, those percentages are nearly reversed. Eurozone banks have been limited by the need to rebuild capital after the financial crisis. Bank lending growth in the eurozone is now positive, but balance-sheet health and size remain a critical focus for financial companies.

In addition, eurozone households, corporations and governments are trying to reduce their leverage, which may constrain the willingness and ability to take advantage of lower interest rates. The opportunity to refinance debt at advantageous rates will, however, be helpful to eurozone fiscal authorities, many of whom are laboring to meet debt and deficit targets.

A second way that QE works is through the “portfolio rebalancing channel.” As the central bank takes bonds out of general circulation, investors have to turn to other asset classes. And as those other asset classes gain momentum, allocations may be altered further. Eurozone equities have performed very well since the beginning of the year, thanks in part to signals that QE was coming.  Wealth effects on spending follow asset price gains, adding to consumption momentum. But wealth effects are not easy to measure and may vary based on the kind of wealth created and the behavioral characteristics of the underlying population. A greater fraction of U.S. households owns shares than is the case in Europe, and saving rates are more than double there. The impact of ECB QE on spending may, therefore, be quite a bit more modest.

Wealth effects on spending follow asset price gains, adding to consumption momentum. But wealth effects are not easy to measure and may vary based on the kind of wealth created and the behavioral characteristics of the underlying population. A greater fraction of U.S. households owns shares than is the case in Europe, and saving rates are more than double there. The impact of ECB QE on spending may, therefore, be quite a bit more modest.

The initiation of QE had mixed effects on the U.S., U.K. and Japanese currencies. The eurozone is certainly hoping to expand its collective exports, and its currency has weakened since QE became more of a certainty in January. But while much of the focus has been on the correction of the euro versus the U.S. dollar (18% over the past 12 months) the trade-weighted euro is cheaper by only 10% over the same interval.

With a host of central banks joining the easing parade, it may be difficult for eurozone policy- makers to engineer an extended competitive devaluation. The attraction of eurozone products also depends on some of the structural reforms of labor, corporate and tax policies that have been very slow to progress.

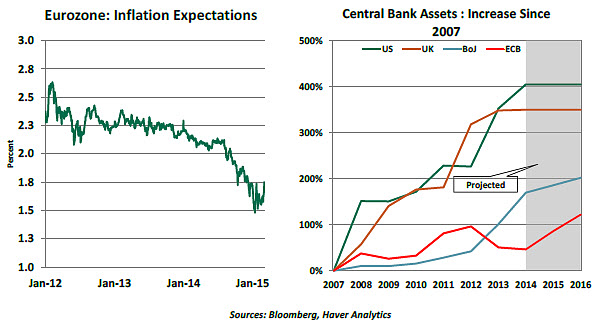

Finally, QE can favorably affect the psychology of economic actors. This is a more intangible benefit, but its immediate impact in the eurozone has been to arrest expectations for falling inflation.

The ECB will face some logistical challenges as it undertakes quantitative easing. The size of the program is more than twice the amount of net new borrowing done by eurozone governments last year, so acquiring assets may be more challenging that it has been for other central banks. Filling the quota of German debt will present a particular hurdle; Germany is only scheduled to issue about €15 billion of new long-term debt this year, while the ECB’s outline calls for €140 billion of German bond purchases over the next 12 months.

Longer-term, the prospective size of the ECB program remains modest compared to what was done in other markets. Given the depth of the challenges faced, it seems quite possible that the ECB may need to extend bond buying well beyond the September 2016 checkpoint offered by Mario Draghi. Given the rancor that attended the program’s launch, securing support for an extension may be problematic. And at some point, an exit strategy will be needed.

Longer-term, the prospective size of the ECB program remains modest compared to what was done in other markets. Given the depth of the challenges faced, it seems quite possible that the ECB may need to extend bond buying well beyond the September 2016 checkpoint offered by Mario Draghi. Given the rancor that attended the program’s launch, securing support for an extension may be problematic. And at some point, an exit strategy will be needed.

In spite of all these theoretical and practical problems, the ECB’s decision to initiate QE in the eurozone was the right one. Over time, better growth in the eurozone will be the best way to compliment the efforts of the Federal Reserve and secure a solid global expansion.

Strong U.S. Jobs Report, but Wage Growth Remains Subdued

The labor market continues to send a signal of strengthening fundamentals. The headline numbers are more-than-impressive, with a lack of wage growth as the only missing piece.

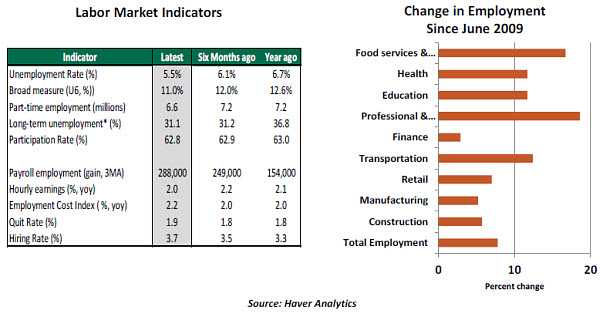

The unemployment rate dropped to 5.5% from 5.7% in February. This is the upper bound of what the Fed considers as full employment (5.2%-5.5%). The broad measure of unemployment (U-6), which includes workers marginally attached to the labor force and those working part-time for economic reasons, declined to 11.0% from 11.3% in January.

The participation rate edged down one notch to 62.8% in February, but a nearly flat trend has prevailed during the past 12 months. Part-time employment has fallen during seven of the last eight months and is at its lowest since October 2008. The share of long-term unemployment declined to 31.1% from 31.5%.

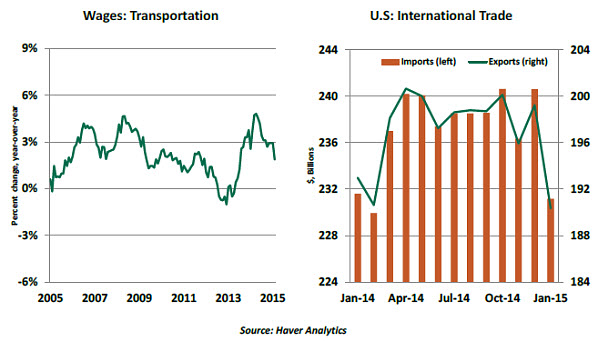

Nonfarm payrolls rose 295,000 in February, putting the three-month moving average at 288,000. By major categories of employment, job gains were strongest in the leisure and hospitality sector; professional and business services; construction; health care; and transportation. Employment in the oil-and-gas industry fell, reflecting energy-sector layoffs, a minor setback in an otherwise solid overall employment trend.

Average hourly earnings increased 0.1%, translating to a muted 2.0% year-to-year increase. One of the most-pressing questions is why wages have failed to accelerate despite a visibly strong improvement in employment. The mix of jobs (high- versus low-paying) created during the recovery is one of the reasons for tepid wage growth. The leisure and hospitality industry (inclusive of food services and drinking places) shows one of the largest increases in employment by industry during the nearly six-year recovery.

Average hourly earnings increased 0.1%, translating to a muted 2.0% year-to-year increase. One of the most-pressing questions is why wages have failed to accelerate despite a visibly strong improvement in employment. The mix of jobs (high- versus low-paying) created during the recovery is one of the reasons for tepid wage growth. The leisure and hospitality industry (inclusive of food services and drinking places) shows one of the largest increases in employment by industry during the nearly six-year recovery.

The other reason is that many establishments were unable to reduce wages during the Great Recession due to downward wage rigidity. Research shows that industries that were unable to reduce wages during the downswing accumulated the most “pent-up wage cuts” and show relatively slow wage growth. There are signs that this trend is changing, with companies such as Wal-Mart increasing compensation for their lowest-paid employees.

This is the last jobs report before the March 17-18 Federal Open Market Committee (FOMC) meeting. The Fed most likely will modify its current forward guidance and use new language in place of being “patient” to raise the policy rate. Although the tone of the February employment report is strongly positive, better inflation and wage numbers are essential for the Fed to consider tightening monetary policy. We continue to believe that such evidence should emerge by the September FOMC meeting.

Docked

The Fed is waiting for robust wage gains in order to be confident about the labor market’s underlying fundamentals. Aggregate employee compensation data have yet show a solid pickup after nearly six years of economic growth. However, there are employers facing demands for higher wages that have caused some distortions in the economy. A case in point is the months-long West Coast dockworkers strike to secure better compensation and working conditions.

The labor standoff at 29 West Coast ports commenced in the latter part of 2014 and increased in severity this year. After a good deal of acrimony and negotiation, a temporary agreement was struck. Unofficial details of the 5- year deal indicate a 3.0% increase in wages, generous health insurance coverage and a substantial pension package.  The West Coast ports handle roughly 45% of U.S. trade, with imports accounting for a larger share than exports. A sharp drop in imports and exports resulting from the strike at these ports helped narrow the trade deficit in January; it is nearly certain to reverse soon. A smaller trade gap is a positive for headline gross domestic product (GDP). At the same time, a decline in inventory accumulation — if consumer demand is assumed to advance — is a negative for GDP.

The West Coast ports handle roughly 45% of U.S. trade, with imports accounting for a larger share than exports. A sharp drop in imports and exports resulting from the strike at these ports helped narrow the trade deficit in January; it is nearly certain to reverse soon. A smaller trade gap is a positive for headline gross domestic product (GDP). At the same time, a decline in inventory accumulation — if consumer demand is assumed to advance — is a negative for GDP.

The net effect is very much uncertain but will consist of the impact on different economic sectors. Exports of perishables would have to be written off, and supply bottlenecks affect production of other goods and services. Respondents to the February Institute of Supply Management’s factory survey noted some of these challenges. Income loss of workers involved in the labor dispute translates into other spillover effects.

Besides these short-term distortions to economic data, the more-important story is whether compensation packages of the sort negotiated by the dockworkers will become more widespread.