Fed Chair Janet Yellen signaled that officials will likely alter the forward guidance at the March 17-18 policy meeting. However, altering this guidance (the conditional commitment to keep short-term interest rates exceptionally low) is not the same as signaling that a rate hike is imminent, as Yellen made clear. She did indicate what would lead the Fed to start tightening. The Fed needs to see further improvement in the job market, it must expect even more improvement in the job market on top of that, and it has to be “reasonably confident” that inflation will move toward the 2% objective.

The Fed has relied on two extraordinary policies to provide support to the economic recovery in recent years. One is quantitative easing, the outright purchases of Treasuries and mortgage-backed securities to help push long-term interest rates lower. The other is the forward guidance. By making a conditional promise to keep short-term interest rates low for some period of time, the Fed puts downward pressure on long-term rates (long-term rates can be thought of as a series of short-term rates). The forward guidance doesn’t cost the Fed anything, making it an attractive tool to use when faced with the zero lower bound (on short-term interest rates).

Initially, the forward guidance was based on a specified time period, but some Fed officials worried that that was too vague. The Fed shifted to economic thresholds. However, as the unemployment rate approached its threshold, something had to give, and the Fed went back to a time-based directive, promising to keep rates low for “a considerable time.” That language proved useful, but as the Fed began to make plans for policy normalization, it was clear that the phrase would have to change. This created a dilemma for Fed policymakers. The financial markets could misinterpret a change in the language. Minutes from the 2014 FOMC meetings reflected a lot of anxiety among Fed officials about changing the phrase. In the mid-December policy statement, the Fed replaced the “considerable time” phrase, saying that it could“be patient” in deciding when to begin raising rates. At the same time, the Fed said that the change in language did not represent any change in the policy outlook. Thus, the Fed changed the language, but kept the sentiment, seemingly having it both ways. However, market participants soon began to speculate on when the “patient” phrase would go, believing that such a change would signal a likely rate hike at the next meeting. Yellen sidestepped that trap in her monetary policy testimony to Congress. The patient language is expected to go. However, Yellen emphasized that the change would not necessarily signal that rates would be raised within a couple of meetings. It only meant that the Fed would begin to consider the possibility of rates hikes.

The Fed is still going to rely on some forward guidance. Specifically, the Fed has indicated that short-term interest rates may remain below normal “even after employment and inflation are near levels consistent with our dual mandate.”

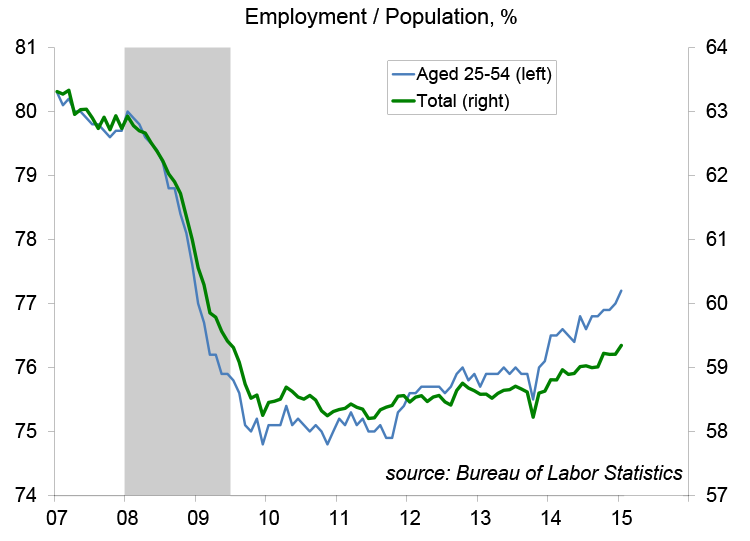

No surprise, the job market will play a key role in when the Fed begins to tighten. We’ve seen significant progress. However, as Yellen testified, “we’re not there yet.” Job conditions will have to improve further before the Fed considers raising rates, but it also must have sufficient momentum to improve further.

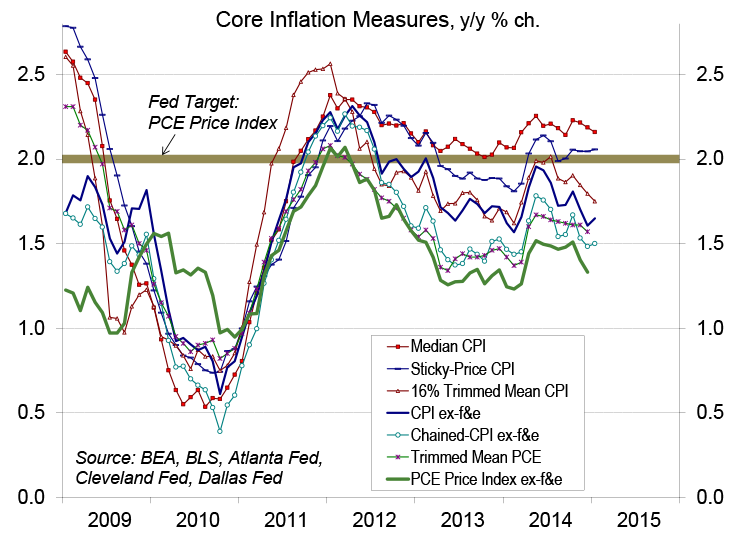

The Fed will also need to be “reasonably confident” that inflation will move back toward the 2% goal. What exactly does that mean? Fed officials are likely to differ in their views, and they’ve not done a good job in forecasting inflation in the last few years. Yellen is likely to require more substantial evidence.

Putting it all together, given the low near-term trend in inflation, most Fed officials are likely to fall into the later-rather-than sooner camp. The bigger uncertainty will be the speed of adjustment once rate hikes begin. That will be data-dependent.

(c) Raymond James