This past week Germany sold five-year debt at a negative yield for the first time in history. Read, wash, rinse and repeat. A negative yield for the first time in history. The problem globally is unmanageable debt. An investor gets to pay Germany money for five years to hold his money. Come on – we are living in highly unusual times.

That investor could decide that an investment in a five-year U.S Treasury note paying 1.38% is a better deal. Think about the implications of a major developed market player paying negative rates. Think about it in terms of global capital flows. What does is say about growth, risk, desperation?

Would you invest your money in German paper earning a guaranteed negative return or would you invest in a U.S. Treasury note earning a positive 1.38%? For now, advantage U.S. dollar. Money will flow to where it is treated best. I wrote about the problem in Forbes in a piece titled Creative Destruction and Managing the Risk of Global Debt.

Global QE is running out of runway. Debt has increased, not decreased. Twenty countries have cut interest rates in 2015. It is an all-out global race to debase. Today let’s take a look at the hard evidence signaling slowdown. My personal view is that slowdown would not be as much of a problem if valuation measures were low. They’re not: by just about every measure the market is overpriced, overbought and over believed.

What can you do? I share a simple and disciplined rules based way for you to stay invested in the market’s primary trend. Over the near term, the U.S. equity market may be driven higher by the favorable global capital flows. That is my current view; however, with risk high, it is important to remember that bear markets happen and it is likely that one is in our not too distant future.

Stay in line with the primary trend, stay alert and remember that bear markets create outstanding investment opportunities. Now is not the time to be complacent.

Included in this week’s On My Radar:

- Putting Declining Sales Estimates In Context – From GaveKal

- Equity Valuations, Recessions and Market Declines

- 13/34-Week EMA and Big Mo (“The Trend Is Your Friend”)

- Trade Signals – Sentiment Turns Negative, Trend Remains Bullish

Putting Declining Sales Estimates In Context – From GaveKal:

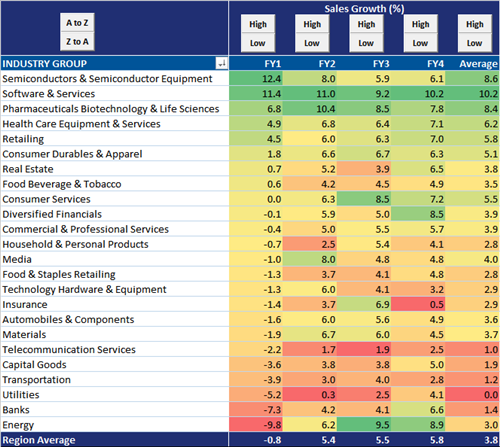

Today, let's look at sales estimate data from an equal-weighted, industry perspective. There are 24 industries in the MSCI World Index. Currently, only 9 of the 24 industries are expected to have positive sales growth in the next fiscal year. In fact, the MSCI World Index on average is expected to have sales decline by 80 basis points over the next fiscal year (FY1). Two industries stand out in terms of their optimistic sales growth expectations. Semiconductors & Semiconductor Equipment is expected to grow sales by 12.4% over the course of the next fiscal year. Software & Services is expected to grow sales by 11.4%. The growth rates for these two industries are nearly twice as high as the industry with the third highest expected sales growth rate.

Energy continues to have the lowest expected sales growth over the next year. The Energy industry is expected to have sales decline by 9.8% over the next fiscal year. However, analysts currently expect sales to bounce back in a few years as Energy has the highest expected sales growth (9.5%) in three years and the second highest expected sales growth in four years. Therefore, if Energy sales do not rebound (or rebound as strongly) it would seem there is further downside for the Energy industry ahead.

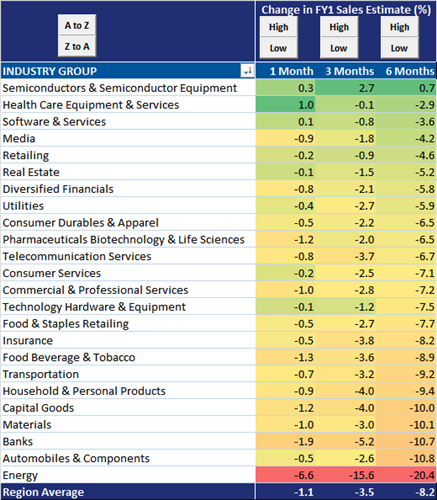

The aggregate estimate of sales in USD has been declining significantly over the past six months. This is a good spot in our data to identify the effect that a stronger dollar is having on sales estimates for global companies. For example, over the past six months the USD level of projected sales has declined by 10.8% for the Automobiles & Components industry. Similarly, the projected level of sales for the Bank industry has declined by 10.7% over the past six months. Overall, only 1 out of 24 industries have experienced a rise in their FY1 projected sales over the past six months. That industry is the Semiconductors & Semiconductor Equipment industry and their USD level of sales has only increased by 70 basis points.

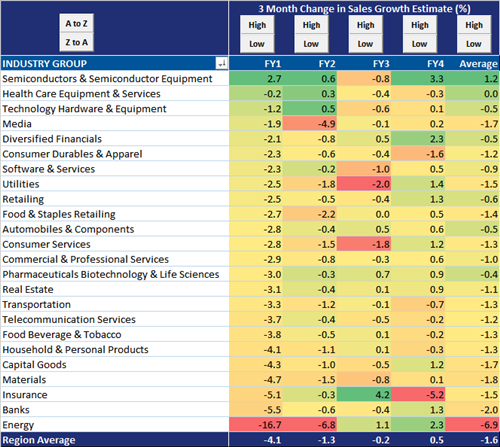

Next let's look at the three month difference in FY1 estimated sales growth rates. Let's look at the Media industry. Currently, the three month difference in FY1 sales estimates for the Media industry is -1.9%. The current growth rate in FY1 sales estimates according to the first table is -1%. This means that three months ago the FY1 sales estimate growth rate for the Media industry was 0.9%. Again, only 1 out of 24 industries has experienced a positive increase in their expected sales growth rate for next year.

GaveKal goes on to say,

Over the past six months, only 17% of all MSCI World companies have experienced a positive FY1 sales revision and no industry has had a majority of companies experience increasing revisions.

Globally, this is not a healthy picture. The point here is that when valuations are high (as they are today) and sales and earnings are deteriorating the risk of price decline is much higher. Source

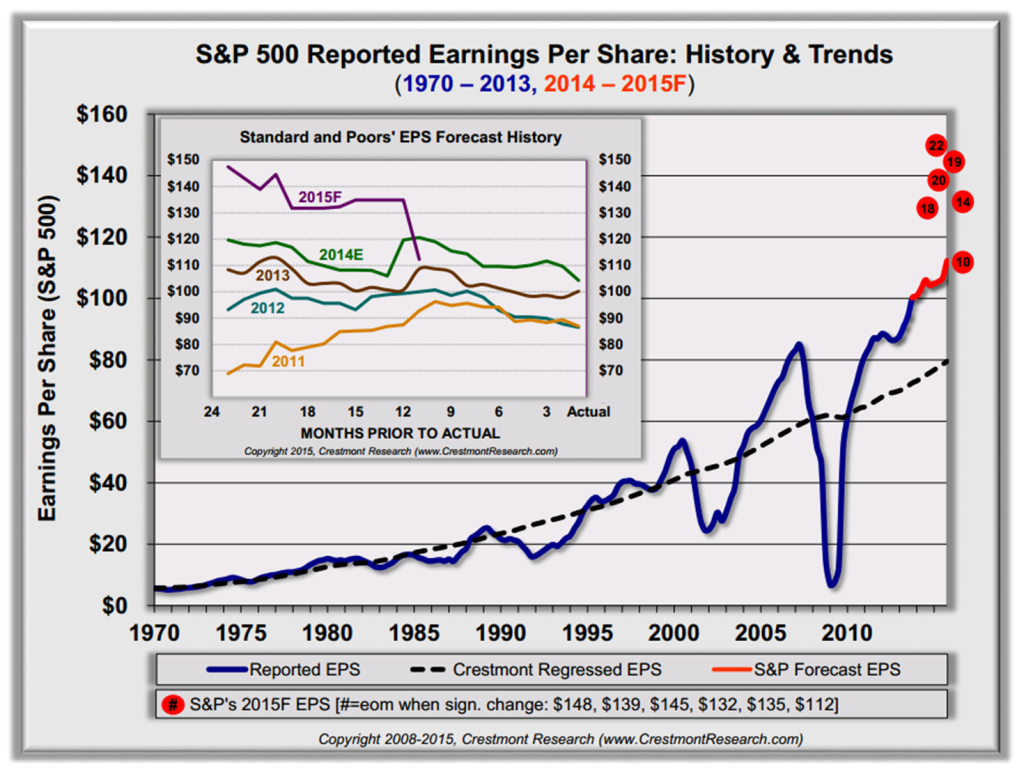

While sales are declining, earnings expectations are being adjusted lower. It becomes a problem when the E in PE is reduced making PE valuations even higher. I found this next chart from Ed Easterling to be meaningful:

SEE SIGNIFICANT CHANGE IN 2015 EPS FORECAST – Source

This graph presents both (1) the historical trend for actual reported earnings per share (EPS), including a forecast by Standard & Poors, and (2) an inset graph presenting the historical record for S&P’s forecast over the past five years. To put the historical trend and future forecast into perspective, the graph includes Crestmont’s assessment of the long-term baseline trend for EPS. Crestmont’s baseline also puts into perspective whether current and forecast EPS are above or below the long-term trend for EPS.

Note: red dots are included with numbers that reflect the month number (e.g., 2=Feb.); this provides a view of the history of recent EPS forecasts. Also, the inset graph reflects S&P’s EPS forecasts for recent years; forecasts begin about two years in advance and proceed until the year is finalized.

Given the overbought, aged and expensively priced U.S. stock market, now is the time to have a plan to risk protect your gains.

Equity Valuations, Recessions and Market Declines

I think Doug Short does some outstanding work. You can follow his research here. The following is from his Feb 25 blog post.

“When I initiated the dshort web page in late 2005, one of my routine topics was equity valuations, initially inspired by Nobel laureate Robert Shiller's book,Irrational Exuberance, the second edition of which was published earlier that year. I gradually expanded my focus from his cyclically adjusted price-to-earnings ratio (CAPE) to include Ed Easterling's Crestmont P/E, Nobel laureate James Tobin's Q Ratio and my own monthly regression analysis of the S&P 500.

About three years ago I began posting a monthly update featuring an overlay of the four. Here is a chart that shows the average of the four valuation indicators from a mean regression.

Last week I had a fascinating conversation with Neile Wolfe of Wells Fargo Advisors, LLC. Based on the underlying data in the chart above, Neile made some cogent observations about the historical relationships between equity valuations, recessions and market prices:

- High valuations lead to large stock market declines during recessions.

- During secular bull markets, modest overvaluation does not produce large stock market declines.

- During secular bear markets, modest overvaluation still produces large stock market declines.

Here is a table that highlights some of the key points. The rows are sorted by the valuation column.

Beginning with the market peak before the epic Crash of 1929, there have been fourteen recessions as defined by the National Bureau of Economic Research (NBER). The table above lists the recessions, the recession lengths, the valuation (as documented in the chart illustration above), the peak-to-trough changes in market price and GDP. The market price is based on the S&P Composite, an academic splicing of the S&P 500, which dates from 1957 and the S&P 90 for the earlier years (more on that splice here).

I've included a row for our current valuation, through the end of January, to assist us in making an assessment of potential risk of a near-term recession. The valuation that preceded the Tech Bubble tops the list and was associated with a 49.1% decline in the S&P 500. The largest decline, of course, was associated with the 43-month recession that began in 1929. Note: Our current market valuation puts us between the two.

Here's an interesting calculation not included in the table: Of the nine market declines associated with recessions that started with valuations above the mean, the average decline was -42.8%. Of the four declines that began with valuations below the mean, the average was -19.9% (and that doesn't factor in the 1945 outlier recession associated with a market gain).

What are the Implications of Overvaluation for Portfolio Management?

Neile and I discussed his thoughts on the data in this table with respect to portfolio management. I came away with some key implications:

- The S&P 500 is likely to decline severely during the next recession and future index returns over the next seven to ten years are likely to be low.

- Given this scenario, over the next seven to ten years, a buy and hold strategy may not meet the return assumptions that many investors have for their portfolio.

- Asset allocation in general and tactical asset allocation specifically are going to be THE important determinant of portfolio return during this time frame. Just buying and holding the S&P 500 is likely to be disappointing.

- Some market commentators argue that high long-term valuations (e.g., Shiller's CAPE) no longer matter because accounting standards have changed and the stock market is still going up. However, the impact of elevated valuations -- when it really matters -- is expressed when the business cycle peaks and the next recession rolls around. Elevated valuations do not take a toll on portfolios so long as the economy is in expansion.

How Long Can Periods of Overvaluations Last?

Equity markets can stay at lofty valuation levels for a very long time. Consider the chart posted above. There are 1369 months in the series with only 58 months of valuations more than two Standard Deviations (STD) above the mean. They are:

- September 1929 (i.e., only one month above 2 STDs prior to the Crash of 1929)

- Fifty-one months during the Tech bubble (that's over FOUR YEARS)

- Six of the last seven months have been above 2 STDs

Stay tuned. Next week I'll be updating the four valuation indicators I routinely track, and preliminary indications are that February will be another month of valuation above 2 STDs.

A special thank you to Doug Short. Well done!

So what can you do? Here is something to consider:

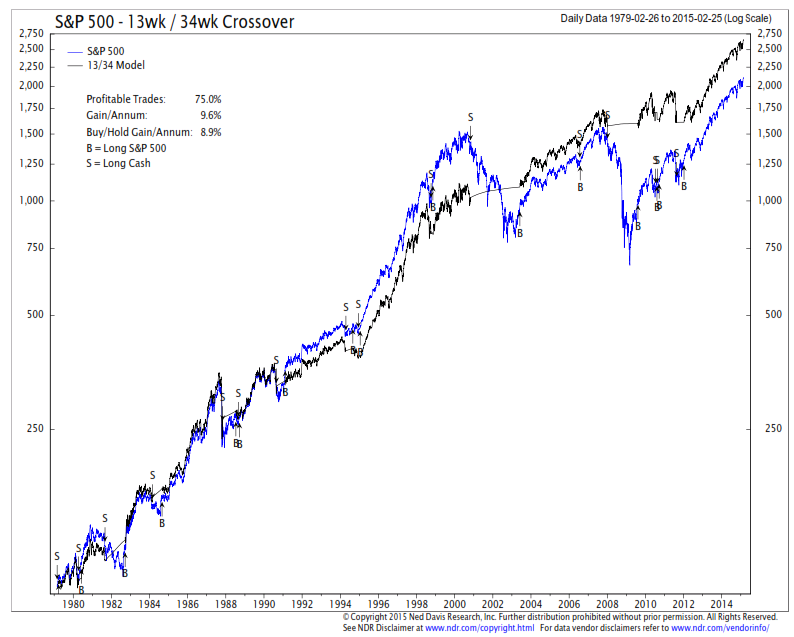

13/34-Week EMA and Big Mo

I had my friends at Ned Davis run some history on one of my favorite trend indicators. The idea it to be invested when the shorter-term 13-week trend line is above the 34-week trend line. Hedge or move to a safer ETF like “BIL” (Treasury Bill ETF) or a low volatility ETF.

Buy and sell indicators are reflected in the next chart. Note how well this simple trend indicator has done since the beginning of the bear market in March 2000. Approximately $1,000 in March 2000 grew to approximately $2,700 (black line) today for a gain of roughly 170% while approximately $1,500 (blue line) grew to $2,100 for a gain of roughly 40%.

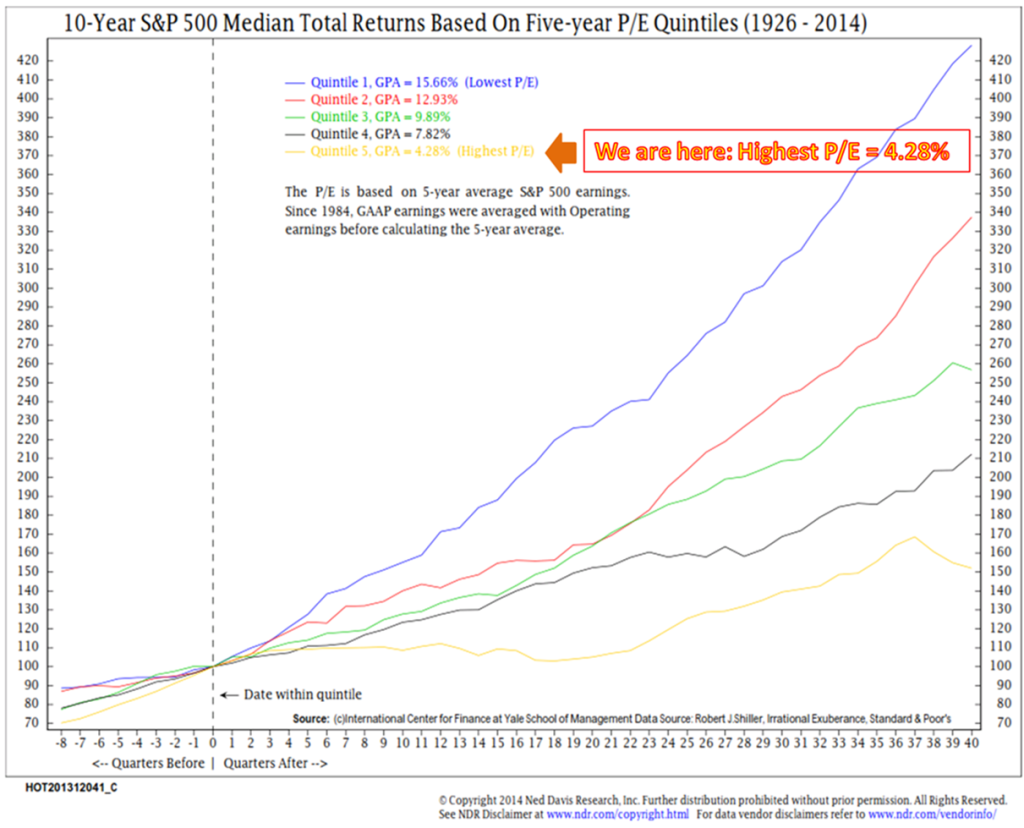

It didn’t do as well in the great bull market (1982 – 2000); however, over both secular cycles, the overall return was pretty good. Frankly, I personally believe that there are periods of time when it is less important to risk protect your equity exposure. PE valuation quintiles can help you identify when risk is low vs. high.

As shown in the chart below, increase equity exposure when PEs are low (Quintiles 1&2) and decrease equity exposure when PEs are high (Quintile 5). The next chart plots historical Median PE data from 1926 to 2014. Simply, it sorted historical/actual Median PEs into five segments and then looked at the return that was gained over the subsequent ten years. When Median PE was high (Quintile 5 – yellow line in the chart), the return for the following ten years was a low 4.28%. When low, the returns were much greater. Quintile 1 (lowest P/E) offered the best returns at 15.66% per year.

I believe PE valuations can help us identify periods of high and low risk; however, it is important to note that PE is a poor timing tool. Thus, stay invested when the trend is “your friend” and hedge when it turns bearish. 13/34-Week EMA is one tool that’s done a pretty good job at identifying the market’s primary trend.

My personal favorite weight of evidence trend indicator is NDR’s Big Mo. We have been working with NDR to create a CMG tradable version that will give us daily signals vs. weekly signals and our work is nearly finished. I’ll share more with you on this shortly. In the meantime, you can see the current Big Mo indicator in Trade Signals (below).

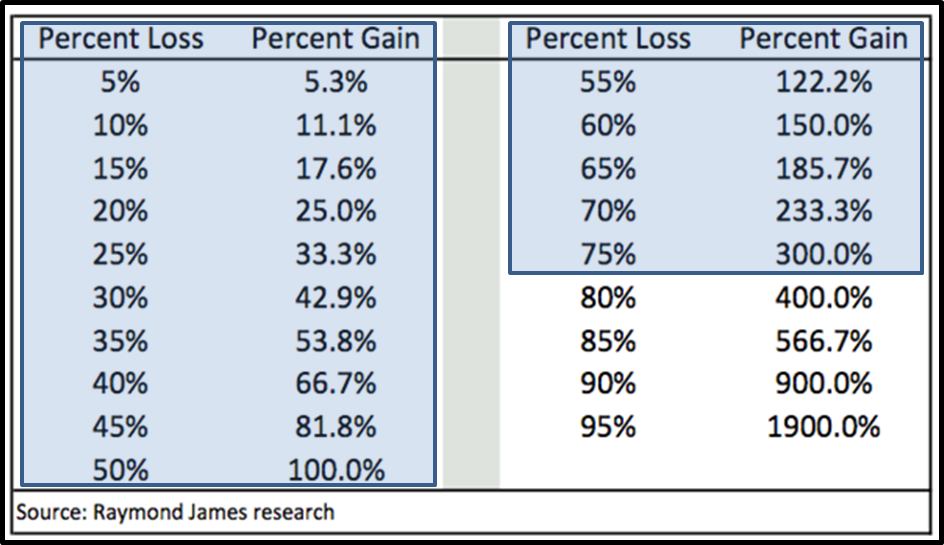

Ultimately, what we want to protect against are periods of significant decline. The percent gain required to overcome loss becomes exponentially more challenging the larger the loss becomes.

Trade Signals - Sentiment Turns Negative, Trend Remains Bullish

Trend evidence remains favorable yet sentiment has climbed back to Extreme Optimism. Such readings are short-term bearish for the market.

This week, along with the usual trend and sentiment charts, I include a special chart that tracks the amount of total equity market exposure of a group of professional traders. Note the current reading in the Extreme Optimism zone (yellow circle) and the historical 1.1% return per annum when excessive optimism is reached (orange arrow). Also note how much greater the returns are when the professionals are excessively bearish – underweight equities.

It is best to be bullish when the majority are bearish and vice versa.

Included in this week’s Trade Signal:

- Cyclical Equity Market Trend: The Primary Trend Remains Bullish for Stocks

- Volume Demand Continues to Better Volume Supply: Bullish for Stocks

- Weekly Investor Sentiment Indicator:

- o NDR Crowd Sentiment Poll: Extreme Optimism (short-term BEARISH for stocks)

- o Daily Trading Sentiment Composite: Extreme Pessimism (short-term BEARISH for stocks)

- The Zweig Bond Model: The Cyclical Trend for Bonds Remains Bullish

Click here for the full piece.

Concluding thoughts

All I can say is “hire these kids”. Penn State’s annual THON raised another $13 million this year. I arrived at midnight last Friday night and after a three hour wait, I was able to get down to the floor and visit with my daughter, Brianna. A time together that I’ll remember forever. Life’s going by way too fast.

I’m writing you today from beautiful Park City, Utah. The snow is falling and the management team is up on the mountain. We meet in an hour for day two of our quarterly management meeting. So much gets accomplished and this year my good friend, Jim Ruff, is with us once again to offer his wisdom. His experience, business logic and common sense has proven to be invaluable to us.

Years ago he told me, “You just don’t know what you don’t know”. “I’ll get you there,” he said. I remind him frequently how important he is and try to express to him the impact he is having not only on our CMG family, but those we’ll be able to help in the years to come. To that he humbly says nonsense. Telling him how grateful I am just doesn’t seem quite big enough. He is a “pay it forward” kind of man and I hope to follow in his footsteps as I dance forward.

Here is a quick toast to slowing down and taking in all that is most important to you in your life. And here is a toast to paying the greatest gifts forward.

Wishing you life’s very best!

With kind regards,

Steve

Stephen B. Blumenthal Founder & CEO CMG Capital Management Group, Inc.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM: Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456. Please read the prospectus carefully before investing. The CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA. NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, or the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

(c) CMG Capital Management Group

© CMG Capital Management Group