“I think the government solution to a problem is usually as bad as the problem and very often makes the problem worse.” Milton Friedman

A close friend bought a $1 million condo but he did something very unusual, he borrowed the mortgage loan in Yen instead of dollars. This can be confusing so let’s try to simplify and cut to the chase. Loans from both countries were offered at low favorable interest rates but he believed that the U.S. dollar would move higher relative to the Yen so he borrowed in Yen. Since he lives and works here in the U.S., his daily life is based in dollars. Not only does his home appreciate in terms of dollars, his living is made in dollars and the food he buys is in dollars.

Since he took out that loan, the dollar has appreciated 50% against the Yen. This means that it will take just $500,000 to pay back the one million Yen based mortgage. Good news for my friend as he can, if he wishes, walk down the street to his local bank and refinance his mortgage. However, both he and I believe the dollar is going even higher – for now. So he is sitting tight.

Of course, his decision doesn’t come without risk. The dollar could continue to appreciate or it could decline in value against the Yen. Such are the risks we take.

Here is the main point of today’s OMR:

According to the Bank of International Settlements, non-bank borrowers outside the U.S. have borrowed, in dollars, $9 trillion. This is an increase of $4.5 trillion since the financial crisis and it places that $9 trillion on the wrong side of the dollar bet.

The broad trade-weighted dollar strengthened 12.3% since last June. Tack an extra 12.3% on top of $9 trillion and you can see how the borrower is beginning to get squeezed. I, along with a number of other forecasters, expect the dollar to continue higher. If I’m right, this is going to get a lot worse.

The dollar debt is an example of how the Fed’s tightening will impact the world economy. This is a pressure cooker and the pot is starting to boil.

Included in this week’s On My Radar:

- The $9 Trillion Dollar Question

- Margin Debt is High and Rolling Over

- El-Erian says low liquidity biggest market risk –CNBC

- Trade Signals – New All Time High, Trend Evidence Remains Positive

The 9 Trillion Dollar Question

I mention my friend as an example to further look at a much bigger risk that surfaced this week. Forget about a $1 million dollar condo mortgage, this is a $9 trillion crisis.

If you live in Europe and your assets and income are based in Euros, then the dollar’s gain against your Euro means it will take more Euros to pay off your debt.

When you throw around numbers in trillions, it all can become a bit foggy; yet, $9 trillion is a potential powder keg of trouble. It is no wonder that the Group of 20 finance ministers last week urged the Federal Reserve to “minimize negative spillovers” from potential interest rate increases.

Why does this matter? Should the Fed decide to raise interest rates as expected this year, there are significant and potentially explosive unintended consequences. The $9 trillion dollar problem will become much bigger.

Let’s reverse the clock back a few years and shift continents. U.S. interest rates were lower than the rates in much of Europe so non-U.S. borrowers living in London, Paris, Germany or Greece, decided to take out loans from U.S. Banks at low interest rates but priced in dollars not Euros. A lot of people liked that idea.

Today, U.S. interest rates are lower than they were then but they are now higher relative to the rates in most of Europe. Additionally, the U.S. is at or near the end of QE and posturing to begin to raise rates while Europe is at the beginning of QE with short-term rates now negative in a number of countries. The U.S. economy is relatively strong while austerity continues in Europe, unemployment is very high and deflation has taken hold.

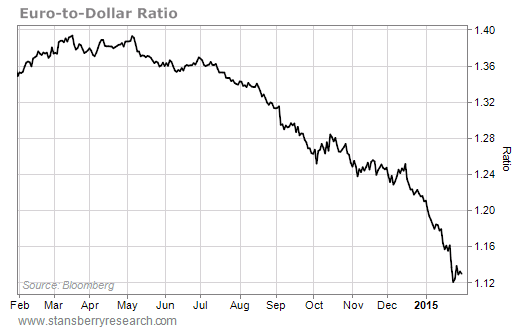

Ok – back to that $9 trillion problem. Think about what would have happened to my friend if the dollar declined against the Yen. He’d need to come up with more dollars to pay back his Yen loan. If the Yen had gone up 50% vs. down 50% against the dollar he’d need $1.5 million to pay off the one million Yen loan. The Euro has declined from $140 to $112 and things may be just starting to heat up. Those folks who borrowed in dollars and have to pay back in Euros will need to come up with more Euros to pay back in dollars because their Euros are worth less.

Tack an extra 12.3% on top of $9 trillion and you can see how the borrower is beginning to get squeezed. I along with a number of other forecasters expect the dollar to continue higher and the Euro lower. If I’m right, this is going to get a lot worse. In the race to debase, the dollar is positioned best.

The dollar debt is an example of how the Fed’s tightening will impact the world economy. This is a pressure cooker and the pot is starting to boil.

“The G20 finance ministers have urged the Federal Reserve to “minimize negative spillovers” from potential interest-rate increases. With the collapse of the Swiss/Euro Peg, they have been stunned into the realization of cross-currency borrowing. For decades, bankers have been marketing loans in different currencies as a means to reduce interest rate costs. However, once the bankers sell these deals, they just walk away.

The collapse in the Swiss/Euro Peg has exposed the amount of mortgages and loans in Swiss being found in Britain to Greece. This is a drop in the bucket. The amount of debt issued in dollars has grown by 50% since 2007 and has now reached some $9 trillion. This the total amount owed in dollars by non-bank borrowers outside the USA. If the Fed raises interest rates as anticipated this year for the first time since 2006, higher borrowing costs for companies and governments, along with a stronger greenback, will create the greatest economic collapse in modern times.”

-Martin Armstrong – G20 Leaders Plead with Fed Not to Raise Rates

As the Fed raises interest rates, with negative short-term rates in Europe, the money will flow into U.S. dollars further accelerating its advance. The Fed is quickly finding itself “between a rock and a hard place” as my father used to always say.

Recently, this piece from Charles Schwab’s crossed my desk – Investing implications of a strong U.S. dollar:

“The U.S. dollar should continue to advance, fueled by a strong economy, the shrinking U.S. trade gap, and the expectation of rate hikes by the Federal Reserve. Schwab’s experts believe the bullish trend could last for at least another year.”

More from Armstrong:

“We expect the dollar outright will advance further as the Fed is forced to tighten while the European Central Bank continues to monetize with negative interest rates buying in failed sovereign debt. Of course, Japan extends its record stimulus as well leaving the USA the only game in town. The pegs of China will have to go as the dollar rises China will have to let go of the balloon or be dragged even higher into the sky without a footing. The pegs in the Middle East and Denmark will also have to go as more and more capital concentrates into the USA.”

Yes, further dollar advance will help my friend. The Yen’s decline is rapidly paying down his mortgage. Good for him yet not such good news for the $9 trillion that sits on the wrong side of the dollar trade. Oh, the problems that come with leverage.

As I mentioned last week, debt has grown by $57 trillion since the 2008 financial crisis. What risks? The point is the world is way out over its skis. With the cyclical bull market aged, valuations high, margin debt high and debt extreme, the simple message is that risk is material. If you can “Vanguard it”, hold your nose and stay the course, then expect low returns over the next ten years and a very bumpy ride. I don’t think most clients can stay on that ride, especially if the next recession brings a 40% correction shortly before they need their money.

Alternatively, put in place a stop-loss risk management process. Studies of past overvalued bull markets suggest that a trailing stop loss exit point at 10% below the one-year high has been a good way of capturing the majority of gains without taking the full brunt of a cyclical bear. When such stop loss level is hit, increase bond exposure to iShares 20+ Year Treasury Bond (TLT) or SPDR Barclays 1-3 Month T-Bill ETF (BIL) until a new uptrend materializes. Alternatively, consider iShares MSCI USA Minimum Volatility ETF (USMV). When the European debt crisis shook U.S. stocks in 2012, the S&P 500 lost 11 percent and USMV lost about half that amount. Expect smaller upside but better downside.

As you may know, I favor Ned Davis Research’s Big Mo and a 13/34-Week EMA as they may guide my hedging and allocation sizing via a disciplined process. See Trade Signals below. For now, the weight of evidence says the trend remains favorable.

Sub-prime and CDOs were a problem in 2005, 2006 and 2007. $9 trillion in debt is a big one too. It is a potential trigger that may set up the next great buying opportunity. For now, as Art Cashin likes to say, “Best to stick with the drill – stay wary, alert, and very, very nimble.”

Here are a few links on the topic:

- http://business.financialpost.com/2015/02/13/the-9-trillion-question-can-the-world-weather-a-fed-rate-rise/

- http://www.bloomberg.com/news/articles/2015-02-13/-9-trillion-question-is-how-tighter-fed-will-impact-world

Another growing concern is the size of margin debt. Historically, it is when the balance peaks and rolls over that too much margin debt becomes an issue. Next, let’s take a closer look.

Margin Debt is High and Rolling Over

I thought about margin debt when I read a quote this week from David Stockman. David is a former businessman and U.S. politician who served as a Republican U.S. Representative from the state of Michigan (1977–1981) and as the Director of the Office of Management and Budget (1981–1985) under President Ronald Reagan.

“The Fed is caught in a time warp and fails to comprehend that the game of bicycling interest rates to heat and cool the macro-economy is over and done. The credit channel of monetary transmission has fallen victim to “peak debt”. The main street economy no longer gets a temporary pick-me-up from cheap interest rates because balance sheets have been tapped out.

The only actual increases in household debt since the financial crisis has been for student loans, which are guaranteed by Uncle Sam’s balance sheet, and auto loans which are collateralized by over-valued vehicles. Stated differently, home equity was tapped out last time; wage and salary incomes have been fully leveraged for years and households have nothing else left to hock.

So households now only spend what they earn, meaning that the Fed’s interest rate manipulations — which had potency 40 years ago — have no impact at all today. Keynesian monetary policy through the crude tool of money market rate pegging was always a one-time parlor trick.”

With homes no longer serving as ATM machines, many have turned to borrowing from their investment accounts. Whether borrowed to buy more stock or borrowed to cover additional spending, margin debt has reached extreme.

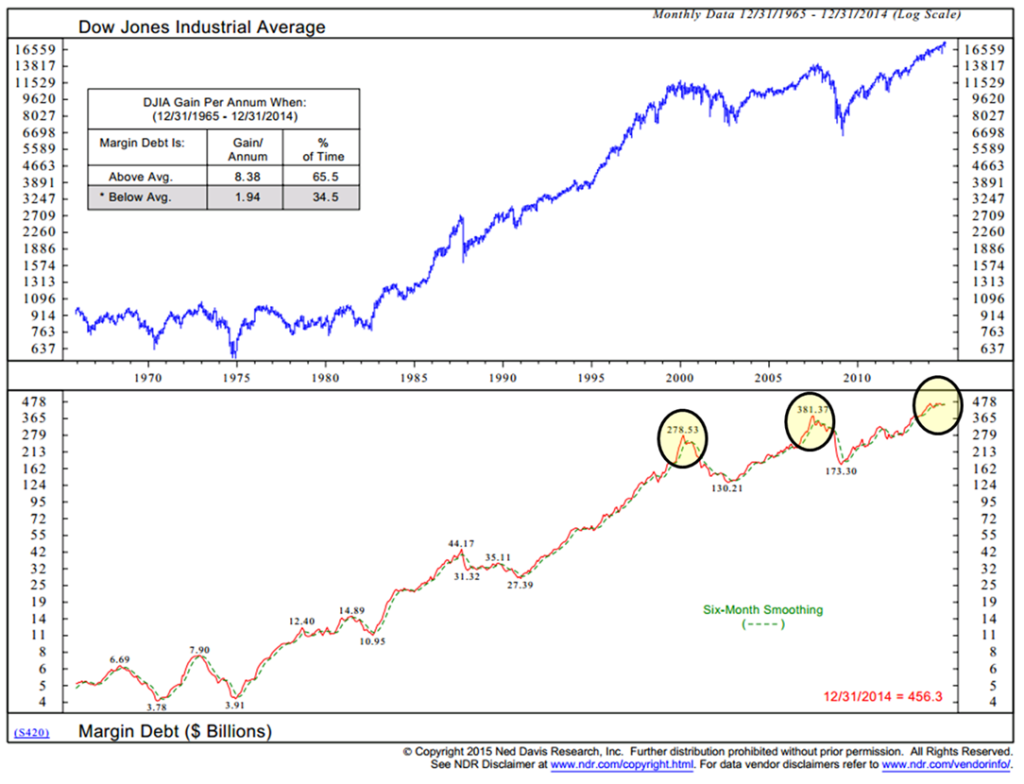

Every once in a while I post a chart on “margin debt”. Like available cash, margin debt can be used to buy stocks. Such demand can fuel stock prices higher. Problems tend to occur when you reach extreme. Evidence suggests we have reached such point.

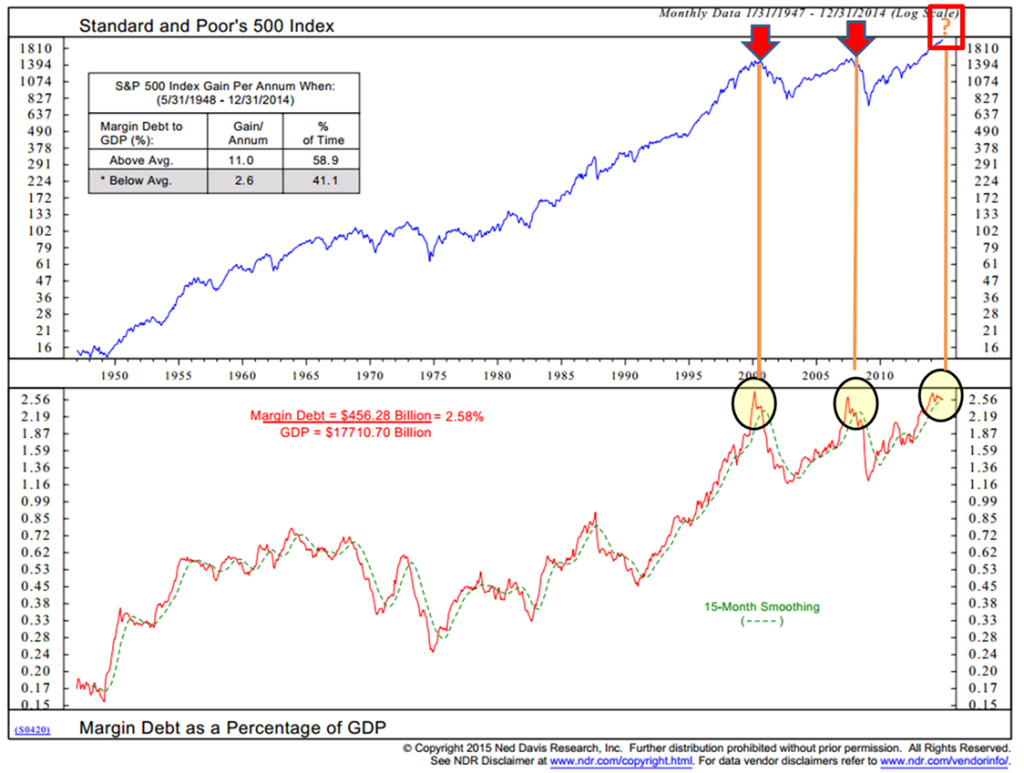

Today, overall margin debt is higher than it was in 2000 and 2007. What I’m watching for is a turn lower from its peak. Chart 1 shows the current level of margin debt. Chart 2 looks at where margin debt is relative to a 15-month trend. Concerning is the recent drop below that trend.

The orange lines (red arrows) mark previous periods in time when margin debt as a percentage of GDP dropped below its 15-month moving average line. Except for a head fake in 2011 and 2012, it has done a pretty good job at calling the prior market peaks.

Further, think about the impact of margin debt in a world where liquidity is a concern. The following from Mohammad El-Erian last week.

El-Erian says low liquidity biggest market risk -CNBC

NEW YORK Feb 17 (Reuters) – Mohamed El-Erian, chief economic adviser at Allianz SE, said Tuesday that Ukraine and Greece are major market risks, but that the biggest risk is the “illusion of liquidity.”

“The biggest risk is this illusion of liquidity,” El-Erian told cable television network CNBC. “The major concern is that you get a change in the paradigm, and then people discover that there isn’t enough liquidity to reposition.”

El-Erian said that the lack of liquidity could result in a market selloff, although he said such a scenario was not his “baseline.”

“If people no longer believe that we are in a low-volatility, improving U.S. economy, geopolitical shocks become too big. If all that changes, then you’re looking at at least a 10 percent correction, and at that point, there is going to be a question of what holds.”

Curbs on banks’ ability to take risks and an increase in technology-driven trading have resulted in dramatic upswings in volatility that have put post-crisis financial markets to the test in recent months.

A selloff in stocks and lower-rated bonds last October was worsened by a lack of banks and market-makers able to step in and buy assets that were being dumped.

El-Erian also said that, while the risks surrounding Greece’s finances and continued conflict in Ukraine were significant, a Greek exit from the euro zone would not be cataclysmic for the global economy, though it would create “short-term chaos.” (Reporting by Sam Forgione; Editing by Alden Bentley and Nick Zieminski)

Trade Signals – New All Time High, Trend Evidence Remains Positive

Trend remains positive, the Fed supportive and sentiment neutral. I’m keeping a very close eye on my trend indicators (Big Mo and 13/34-Week EMA) as risk remains high. Following are the usual weekly charts.

Included in this week’s Trade Signal:

- Cyclical Equity Market Trend: Cyclical Bullish Trend for Stocks

- Volume Demand Continues to Better Volume Supply – Bullish for Stocks

- Weekly Investor Sentiment Indicator:

- o NDR Crowd Sentiment Poll: Neutral Optimism (short-term neutral for stocks)

- o Daily Trading Sentiment Composite: Extreme Pessimism (short-term bullish for stocks)

- The Zweig Bond Model: The Cyclical Trend for Bonds Remains Bullish

Click here for the full piece.

Concluding thoughts

It is the massive amount of government involvement in potential solution and, in many cases, around the globe, it is government’s mismanagement of resources and poor stewardship of capital that the very governments are attempting to fix. Personally, I think Friedman is right.

“I think the government solution to a problem is usually as bad as the problem and very often makes the problem worse.”

– Milton Friedman

All the currency gamesmanship creates tension and with debt the common denominator, I personally don’t believe more debt and higher taxes is the answer. My best guess is that a sovereign default wave is fast approaching.

I’m heading to Penn State this weekend to support my oldest daughter as she dances in a 48 hour dance marathon called THON. The energy level is high and for now the feet are feeling good. I’ll be crutching in with my torn ACL and hope that gets me to the front of the line. Nearly 15,000 will pack PSU’s Bryce Jordon Center and the music will be rockin. I danced in THON in 1982.

In 1982, Penn State Heisman Trophy winner John Cappelletti spoke to the dancers about losing his brother, Joey, to leukemia ten years earlier. The event that year raised more than $95,000 and the following year, the sum of $131,000 was raised. Remember those days of big hair and gym shorts? Not a good look.

Last year the students raised more than $13 million for children with cancer. A wonderful thing!

I’ll be thinking about my dad in the stands in the very early morning hours tossing a football with me and my friends as we dance. I’m setting the alarm to show up and surprise my daughter in the wee hours. That’s when it’s likely to be the toughest. No football allowed but I’m hoping a good hug will help.

Have a great weekend. Here’s a toast to good hugs.

Wishing you the very best.

With kind regards,

Steve

Stephen B. Blumenthal

Founder & CEO

CMG Capital Management Group, Inc.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM: Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456. Please read the prospectus carefully before investing. The CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA. NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, or the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

(c) CMG Capital Management Group

© CMG Capital Management Group