IN THIS ISSUE:

1. Don’t Let Obama Take Over The Internet… Revisited

2. The Most Successful Public Company in the World

3. Why Much-Hated “Sin” Stocks Tend to Outperform

4. “Socially-Responsible” Investing Comes With a Cost

5. Conclusion: I Want My Clients & Readers to be Informed

6. WEBINAR: Niemann Capital Management, February 26

Overview

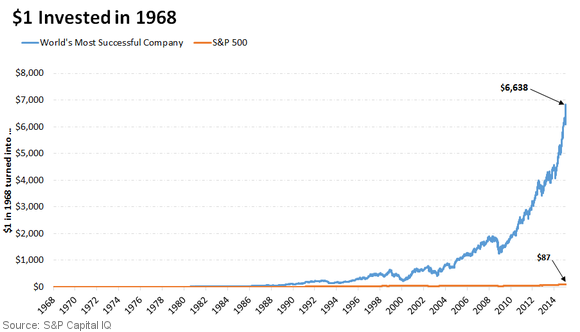

Today we focus on the most successful and profitable company in the entire world. It just happens to be an American company, but many of us have never heard of it. If you had invested $1 in this company in 1968, your investment would have soared to $6,638 at the end of last year. I think you’ll be surprised to see which company this is.

Following that discussion, I will address the growing trend of “socially-responsible” investing. That is, not investing in so-called “sin” stocks such as tobacco, alcohol, gambling, firearms, etc. A new report from Credit Suisse points out that there is a cost associated with socially-responsible investing – in the form of lower performance returns.

I bring this to your attention, not in an attempt to discourage it, but to point out that there is a cost involved in “politically-correct” investing. In my 35+ years in the financial business, I have never seen an analysis that compares socially-responsible investing to investing in so-called sin stocks. I think you’ll find it very interesting.

But before we jump into those topics, I want to briefly revisit the likelihood that the Federal Communications Commission, under orders from President Obama, will vote a week from Thursday to take control of our precious Internet. It now looks inevitable that the federal government will enact what may prove to be one of the largest power grabs in history!

Don’t Let Obama Take Over The Internet… Revisited

Last Thursday, I sent my weekly Blog to everyone who reads this E-Letter. My warning: The Federal Communications Commission, on orders from President Obama, will vote on Thursday February 26 to take control of the Internet. There is little doubt now that this will happen.

The FCC will use the ruse of “net neutrality” to justify sweeping the entire Internet industry into anantiquated regulatory regime that was designed decades ago to deal with a monopoly phone industry that no longer exists. It will give the FCC virtually unlimited power to tax, regulate rates and second-guess every Internet-related business decision made.

This is purely and simply a travesty! Yet there is apparently no way to stop it. In a Rasmussen poll last week, only 26% of Americans agree that the FCC should regulate the Internet, while 61% believe it should not. But as anyone reading me should know by now, this president cares nothing about what Americans want or don’t want.

Sadly, Congress is way behind the curve and is doing next to nothing to stop this huge power grab. Ironically, Congress is currently working on a new bill that would ensure that the government cannot tax the Internet, ever. What this effort fails to realize is that once the FCC takes control of the Internet, the government (Obama) can do whatever it wants until at least early 2017 when we have a new president. Imagine the damage that can be done until then!

With that said, let’s move on to our main topics today.

The Most Successful/Profitable Company in the World

Take a look at the chart below. It shows the performance of the most successful company in the world. One dollar invested in this company in 1968 was worth $6,638 (including dividends) as of last Friday’s close. That’s an annual return of 20.6% per year for nearly half a century.

No other company comes close to matching its long-term results, according to Wharton finance professor Jeremy Siegel who appears regularly on CNBC, CNN, NPR and other programs.

So what company is this? Let’s think about it.

It had to have been revolutionary. It had to have been innovative. It must be in an industry that changed the world – probably the biggest trend of the 20th century. It must have done something no other company could do. Yet you may have never even heard about it.

Computers? No. Satellites? No. Biotech?

Nope. It’s ALTRIA (NYSE: MO), the cigarette company – the parent of Phillip Morris, US Smokeless Tobacco, John Middleton (cigars), NuMark, etc. It is headquartered in Henrico County, Virginia.

Credit Suisse published a report last week on the performance of every major American industry from 1900 to 2010. One thing that jumped out of that report is the fact that it pays to invest in so-called “sin” stocks.I’ll have more to say about that later on today.

According to Credit Suisse, one dollar invested in 1900 in the average American industry was worth$38,255 by 2010. That’s an annual return of about 10% per year. Some did far better: $1 invested in food companies was worth about $700,000 by 2010. Chemical and electrical equipment companies returned about the same.

Then there’s tobacco, which is in a league of its own. One dollar invested in tobacco stocks in 1900 was worth $6.3 million by 2010. That’s 165 times greater than the average industry. During a century of innovation, progress and scientific advancement, no industry did better than cigarettes.

Most people would look at these numbers and say, “Well, sure. That's what happens when you sell an addictive product.” But what’s extraordinary about this story is that the cigarette industry has been in decline for decades.

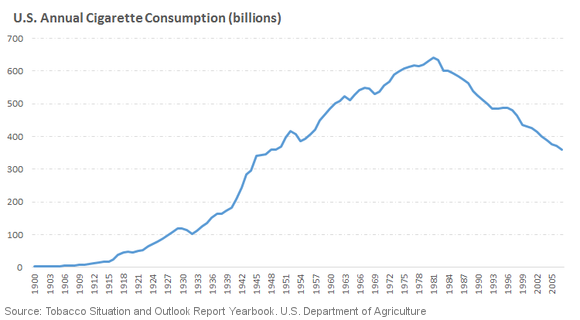

Cigarettes are, of course, addictive. But smoking rates have been falling for half a century. Half as many US adults smoke today than did in the 1950s. And even though there’s been population growth during that period, it hasn’t been enough to offset the decline in smoking rates. Total US cigarette consumption peaked in 1981 at 640 billion cigarettes. By 2007 that dropped 44%, to 360 billion:

By unit sales, tobacco is one of the least successful American industries of the last 30 years. Add to it that tobacco advertising has been largely banned for more than a decade, and legal settlements have cost the industry billions. It’s amazing that tobacco has been able to produce any returns, let alone the highest in American history.

Part of tobacco stocks’ rise is due to foreign operations in countries where smoking is more common and hasn’t declined as much as in the US. But there’s more going on here. Altria spun off its international division, Philip Morris International in 2008. Altria stock is up 289% since then, versus 79% for the S&P 500.

Part of it is the ability to raise prices. Tobacco product inflation has increased almost five times fasterthan overall inflation since 1950. But that, too, doesn’t explain everything. A lot of the price increases have been to offset rising tobacco taxes, which in some states make up more than one-third of the sales price. Altria pays far more in excise taxes than it earns in profits.

Why Much-Hated “Sin” Stocks Tend to Outperform

There is something about tobacco that leads to extraordinary returns despite a subpar business. What is it? It comes down to two factors, both of which are paradoxical and relevant to all investors in all industries. According to Credit Suisse:

1. Fear, disgust, hatred, and outrage toward a business are good for shareholders.

Lots of investors (understandably) want nothing to do with tobacco companies. Some pension funds are barred from owning them. And then there’s the constant threat of litigation, which has hung over the industry for decades. It adds up to millions of otherwise enterprising investors who won't touch tobacco stocks.

Low investor demand keeps tobacco-stock valuations low. Low valuations lead to high dividend yields. And high dividend yields, compounded over decades, add up to massive returns. The more hated an investment is, the higher future returns are likely to be. This is one of the most difficult investing concepts to come to terms with, but probably one of the most powerful.

2. Tobacco companies rarely innovate. That keeps them sustainable.

Innovation is exciting because it promises something new: New products, new markets and a new future.But it’s expensive. And even if you're great at it – like Apple is – you’ll probably stumble one day.

The products Apple made just five years ago are mostly irrelevant today. The company has to reinvent itself every few years, continuously coming up with breakthrough products that blow us away. Yet what are the odds it will keep innovating consistently at the rate it has for another 20, 30, 50 years? Pretty low, don’t you think?

Even the best players strike out from time to time, and ruthlessly competitive markets show them no mercy. It’s rare that a leader sticks around for more than a decade in industries that undergo constant change.

Companies that make the same product today that they did 50 years ago are different. They generally don’t innovate, but they don't have to, and it saves them a lot of money. It’s a boring business, but it can be great for shareholders because it keeps the companies chugging along for decades or longer.

The ridiculously large gains from compound interest occur over long holding periods. The key to building wealth isn’t necessarily high returns in the short-term, but mediocre returns sustained for long periods of time. It is not unusual for boring companies that don’t innovate to be selling the same products today that they did 50 years ago – and may be selling 50 years from now. Food, soap, toothpaste and, yes, cigarettes are good examples.

“Socially-Responsible” Investing Comes With a Cost

In its latest report on American industries, Credit Suisse provides the following analysis which compares socially-responsible investing to investing in so-called “sin” stocks. While I fully understand why many investors insist on owning only socially-responsible companies, it is important to know that doing so often comes with a cost.

In all the years I have been in the investment business, I have never before seen an analysis such as this – one that compares socially-responsible investing with sin stocks, head-to-head. That’s why I bring it to your attention. For the record, I don’t own any individual stocks, so I personally don’t own any individual “sin” stocks. However, some of the mutual funds and ETFs I am invested in (and some of the money managers I recommend) may hold relatively small positions in such stocks from time to time.

The following is a summary of that portion of the latest Credit Suisse report which discusses the pros and cons of socially-responsible investing. I think you’ll find it interesting as I did.

Credit Suisse acknowledges that investors are increasingly concerned about social, environmental and ethical issues, and asset managers are under growing pressure to demonstrate socially-responsible investment behavior. This has led more and more investors and money managers to avoid so-called sin stocks.

What Credit Suisse points out is that there is a “cost” to be paid by avoiding many of these stocks for ethical reasons. They also argue that it is partly because of this hatred of such stocks that allows them to offer higher returns/dividends to those less troubled by ethical considerations.

Some faith-based investors veto investing in certain companies (ie - cigarettes, alcohol, etc.) on the grounds that such businesses are offensive to their values. Their avoidance of such companies is believed by many to be a form of “leverage” to persuade such companies to behave differently. But Credit Suisse argues that simply not buying such stocks doesn’t amount to leverage, since there are plenty of other buyers to go around.

For most institutions (including large pension funds), there is a risk that by practicing socially-responsible investment to the greatest extent possible, they could forego higher investment returns by allocating to sin stocks. This explains in part why most large investment institutions don’t practice socially-responsible investing.

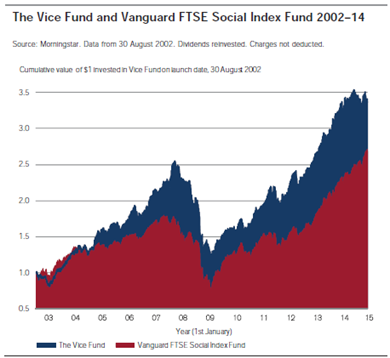

Essentially, Credit Suisse is arguing that it makes sense to include sin stocks in a diversified portfolio in order to boost returns. To illustrate this point, they compare the Vice Fund (VICEX) with the politically-correct Vanguard Social Index Fund (VFTFX). Both funds were started in the early 2000s.

Essentially, Credit Suisse is arguing that it makes sense to include sin stocks in a diversified portfolio in order to boost returns. To illustrate this point, they compare the Vice Fund (VICEX) with the politically-correct Vanguard Social Index Fund (VFTFX). Both funds were started in the early 2000s.

As you can see, the Vice Fund was the winner. It would have grown from $10,000 at inception to$33,655 at the end of 2014, which earned it a top rating from Lipper and Morningstar. On the other hand, the Vanguard Social Index Fund, over the same time, grew from $10,000 to $26,788. During this period, the S&P 500 had performance midway between these two funds.

The Vice Fund invests in businesses that are considered by many to be socially-irresponsible. Recently renamed the Barrier Fund, it has assets of apprx. $290 million invested in industries with significant barriers to entry, including tobacco, alcoholic beverage, gambling, firearms, etc., etc.

The Vanguard Social Index Fund tracks an index screened by social, human rights and environmental criteria. Most of its holdings have superior environmental policies, strong hiring/promotion records for minorities and women, and a safe workplace. There are no companies that are considered to be sin stocks. It has assets under management of apprx. $1.5 billion.

Conclusion: I Want My Clients & Readers to be Informed

The point Credit Suisse wishes to make is simply that including so-called “sin” stocks in a diversified portfolio may increase performance. While the difference in performance in the two funds illustrated above is significant, there are other analysts who claim that there are ways to minimize that gap. I’m waiting to see the proof.

Still, there will always be investors who simply do not want to include so-called sin stocks in their portfolios for a variety of reasons. My only point today is that there may be a cost in terms of reduced performance in doing so. As always, I want my clients and readers to be informed.

Wishing you profits,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.