“What beat me was not having brains enough to stick to my own game – that is to play the market

only when I was satisfied that precedents favored my play”

Jesse Livermore – Reminiscences of a Stock Operator

There has been a lot of debate on the Reinhart-Rogoff hypothesis. When debt becomes excessive, growth slows. Most of the academic work tends to support their conclusion.

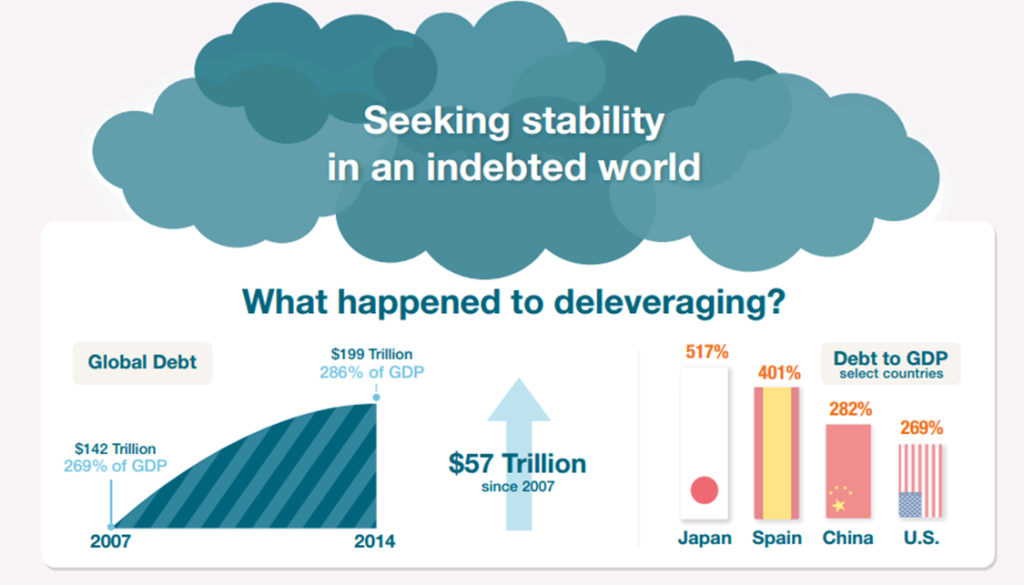

Today we take a sobering look at debt across the globe. It has increased by more than $57 trillion since the 2007 crisis and remains a significant headwind. Some countries are better positioned than others (stronger capital markets, currency advantages, underlying wealth, etc.). Deflation is gaining traction.

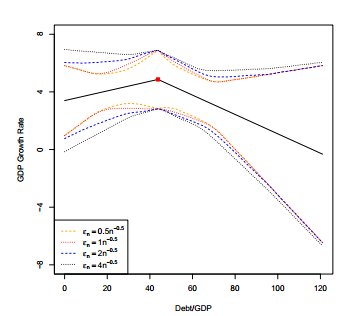

Reinhart and Rogoff suggested that problems accelerated when debt reached 100% of GDP. I’ve seen studies suggesting the number is more like 40% to 50% and others suggesting it is much higher. The following chart, from one such study, looks at U.S. debt-to-GDP and suggests growth begins to decline when Debt/GDP reaches approximately 45%. Today, total U.S. debt/GDP is 269%.

While it would be nice to find a magic debt-to-GDP threshold number that signals a crisis, such findings have proven allusive. However, what I believe we can do is look at debt from a risk measurement perspective. For example, just as Median PE quintiles can tell us a lot about probable 10-year forward returns (high PEs equal low returns and low PEs equal high returns), I believe excessive debt can equally signal periods of high risk.

Like PE, we don’t know if the market will do this year or next but we do know today is that the stock market is expensively priced and 10-year forward returns will likely come in far below what most investors hope them to be. I look at the debt-to-GDP debate much the same way. Debts “a drag man” and we should factor this into our portfolio construction thinking.

If your client wants to jump on a speculative rocket (i.e. throw the chips “all in” stock such as “IVV” the S&P 500 Index), suggest a diversified cab ride instead. The time to hop on that rocket will present itself again; whether it be a recession, cyclical bear and/or crisis.

As Livermore suggests in the lead quote above, stick to the game plan and position more aggressively when you are satisfied that precedents favor your play.

The evidence today suggests otherwise – prices are high and too much debt is slowing growth. See Earnings Estimates Sink – Valuations Remain High.

This week let’s take a look at debt around the globe. I share a great piece from McKinsey & Company that shows just how much more debt, county by country, has been piled on since the 2007 debt induced financial crisis. Evidence is apparent in the commodity market and I also share a few ideas how you may risk manage those allocations.

Grab a coffee, this one prints longer than normal (many charts) and enjoy the holiday weekend.

Included in this week’s On My Radar:

- Debt and (not much) Deleveraging

- Commodity Bear Market – A Quick Look at the Long-Term Trend

- Lower Gas Price Savings – Who’s Benefiting

- More on Deflation – From CMG’s Kevin Auerbach

- And in Case You’re Wondering Who’s Benefiting From Lower Gas Prices – It’s Restaurants

- Trade Signals – Not Greedy Not Fearful, Trend Evidence Positive

Debt and (not much) Deleveraging – McKinsey & Company

Summary of findings:

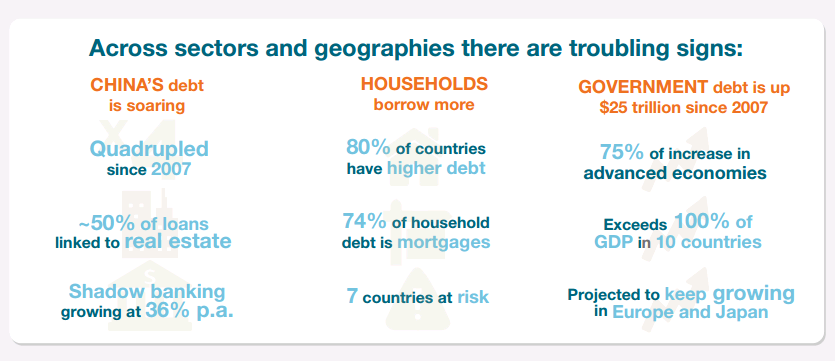

- We find that deleveraging since 2008 remains limited to a handful of sectors in some countries and that, overall, debt relative to GDP is now higher in most nations than it was before the crisis.

- Not only has government debt continued to rise, but so have household and corporate debt in many countries.

- China’s total debt, as a percentage of GDP, now exceeds that of the United States.

- Higher levels of debt pose questions about financial stability and whether some countries face the risk of a crisis.

- One bright spot is that the financial sector has deleveraged and that many of the riskiest forms of shadow banking are in retreat.

- But overall this research paints a picture of a world where debt has reached new levels despite the pain of the financial crisis.

- This reality calls for fresh approaches to reduce the risk of debt crises, repair the damage that debt crises incur, and build stable financial systems that can finance companies and fund economic growth without the devastating boom-bust cycles we have seen in the past.

SB here: “Reduce the risk of debt crises”? To that point I say good luck. Look back to all that set the stage for the last crisis. I remember writing about the probable failure of Fannie and Freddie, the insanity of no-doc mortgages and Greenspan’s “there is not a bubble” in the housing market.

Think back to the seemingly endless amount of available liquidity with Wall Street’s derivative sausage-making machine – CMOs and CDOs with layers of tranches and endless slices and dices of repackaged risk. Here was Paul Krugman in a 2002 New York Times editorial: “To fight this recession the Fed needs…soaring household spending to offset moribund business investment. [So] Alan Greenspan needs to create a housing bubble to replace the Nasdaq bubble.” Source.

The point isn’t to pick on Greenspan or Krugman, the point is that we do go through expansion and contraction and boom and bust for centuries. Not everyone gets a trophy but to have the opportunity to create, compete and advance; that is what makes for a healthy state. Governments have become too large a part of the equation. Somehow, Joseph Schumpeter’s creative destruction sneaks into my mind.

Joseph Schumpeter (1883–1950) coined the seemingly paradoxical term “creative destruction” and generations of economists have adopted it as a shorthand description of the free market’s messy way of delivering progress. In Capitalism, Socialism, and Democracy (1942), the Austrian economist wrote:

The opening up of new markets, foreign or domestic, and the organizational development from the craft shop to such concerns as U.S. Steel illustrate the same process of industrial mutation—if I may use that biological term—that incessantly revolutionizes the economic structure from within, incessantly destroying the old one, incessantly creating a new one. This process of Creative Destruction is the essential fact about capitalism. (p. 83). More here.

Not a bad thing. It is perhaps an important and healthy part of the process to get us to a better place. Put me firmly in that camp.

Ok – sorry for that detour. The next picture below sets the stage and I’ve included a few more select excerpts:

After the 2008 financial crisis and the longest and deepest global recession since World War II, it was widely expected that the world’s economies would deleverage. It has not happened. Instead, debt continues to grow in nearly all countries, in both absolute terms and relative to GDP. This creates fresh risks in some countries and limits growth prospects in many.

- Debt continues to grow. Since 2007, global debt has grown by $57 trillion, raising the ratio of debt to GDP by 17 percentage points. Developing economies account for roughly half of the growth, and in many cases this reflects healthy financial deepening. In advanced economies, government debt has soared and private sector deleveraging has been limited.

- Reducing government debt will require a wider range of solutions. Government debt has grown by $25 trillion since 2007, and will continue to rise in many countries, given current economic fundamentals. For the most highly indebted countries, implausibly large increases in real GDP growth or extremely deep reductions in fiscal deficits would be required to start deleveraging. A broader range of solutions for reducing government debt will need to be considered, including larger asset sales, one-time taxes, and more efficient debt restructuring programs.

- Shadow banking has retreated, but non‑bank credit remains important. One piece of good news: the financial sector has deleveraged and the most damaging elements of shadow banking in the crisis are declining. However, other forms of non‑bank credit, such as corporate bonds and lending by non‑bank intermediaries, remain important. For corporations, non‑bank sources account for nearly all new credit growth since 2008. These intermediaries can help fill the gap as bank lending remains constrained in the new regulatory environment.

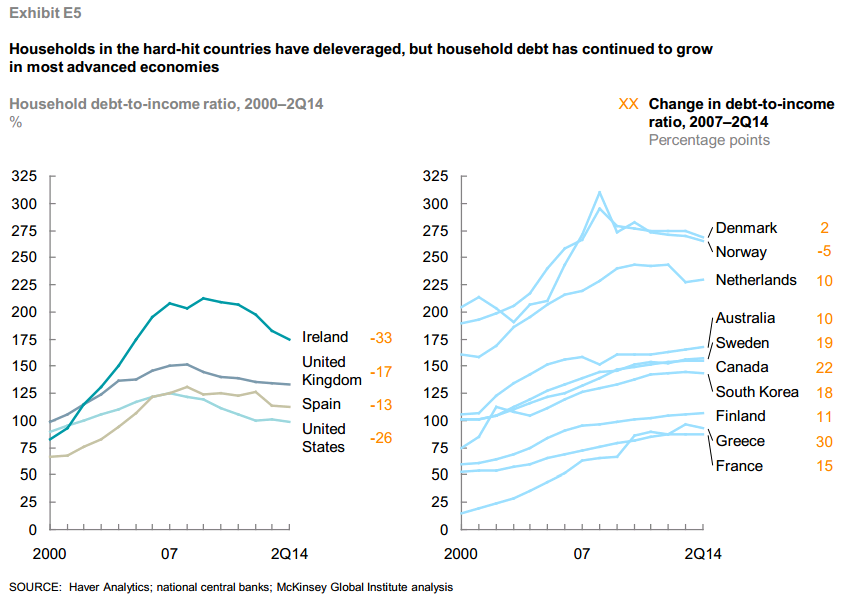

- Households borrow more. In the four “core” crisis countries that were hit hard—the United States, the United Kingdom, Spain and Ireland—households have deleveraged. But in many other countries, household debt-to-income ratios have continued to grow and, in some cases, far exceed the peak levels in the crisis countries.

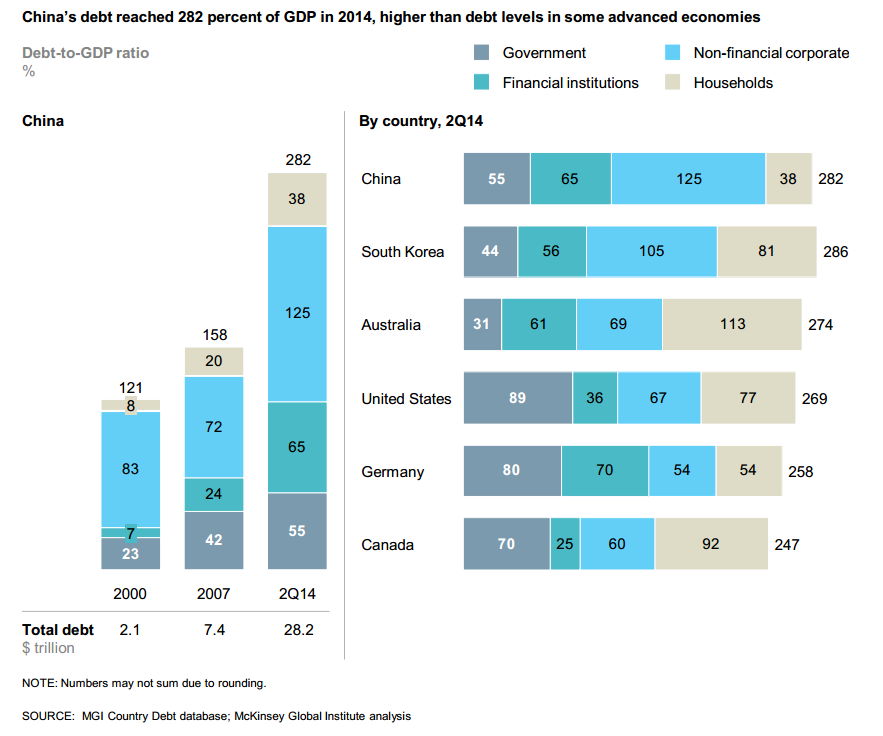

- China’s debt is rising rapidly. Fueled by real estate and shadow banking, China’s total debt has quadrupled, rising from $7 trillion in 2007 to $28 trillion by mid-2014. At 282 percent of GDP, China’s debt as a share of GDP, while manageable, is larger than that of the United States or Germany. Several factors are worrisome: half of the loans are linked directly or indirectly to China’s real estate market, unregulated shadow banking accounts for nearly half of new lending, and the debt of many local governments is likely unsustainable.

It is clear that deleveraging is rare and that solutions are in short supply. Given the scale of debt in the most highly indebted countries, the current solutions for sparking growth or cutting fiscal deficits alone will not be sufficient. (Emphasis mine).

The above is good but here are just a few more snapshots if you want to get geekier like me.

A mild bright spot has been the reduction of household debt in the U.S. – down 26% as measured by total debt relative to income:

Noting a bright spot:

- It is a welcome sign, then, that financial-sector debt relative to GDP has declined in the United States and a few other crisis countries, and has stabilized in other advanced economies. At the same time, banks have raised capital and reduced leverage.

- Moreover, the riskiest elements of shadow banking are in decline. For example, the assets of off-balance sheet special-purpose vehicles formed to securitize mortgages and other loans have fallen by $3 trillion in the United States. Repurchase agreements (repos), collateralized debt obligations, and credit default swaps have declined by 19 percent, 43 percent, and 67 percent, respectively, since 2007.

- However, if we consider the broader context of non‑bank credit, including corporate bonds, simple securitizations, and lending by various non‑bank institutions, we see that non‑bank credit is an important source of financing for the private sector.

- Since 2007, corporate bonds and lending by non‑bank institutions—including insurers, pension funds, leasing programs, and government programs—has accounted for nearly all net new credit for companies, while corporate bank lending has shrunk. The value of corporate bonds outstanding globally has grown by $4.3 trillion since 2007, compared with $1.2 trillion from 2000 to 2007.

- Most of these forms of non‑bank credit has fewer of the shadow banking risks seen before the crisis, in terms of leverage, maturity mismatch, and opacity.

- Some specific types of non‑bank credit are growing very rapidly, such as credit funds operated by hedge funds and other alternative asset managers. Assets in credit funds from a sample of eight alternative asset managers have more than doubled since 2009 and now exceed $400 billion.

- Another small, but rapidly growing, source of non‑bank debt is peer-to-peer lending. These online lending platforms have originated only about $30 billion in loans so far, but private equity funds, other asset managers, and even banks have begun investing in peer-to-peer platforms, suggesting that these lenders could build greater scale.

China is potentially a surprise left hook we may not be watching for (SB comment):

Here is the short summary on China.

- China’s debt is rising rapidly, with several potential risks ahead. Since 2007, China’s total debt (including debt of the financial sector) has nearly quadrupled, rising from $7.4 trillion to $28.2 trillion by the second quarter of 2014, or from 158 percent of GDP to 282 percent.

- China’s overall debt ratio today appears manageable, although it is now higher in proportion to GDP than that of the United States, Germany, or Canada.

- Continuing the current pace of growth would put China at Spain’s current level of debt—400 percent of GDP—by 2018.

- We find three particular areas of potential concern: the concentration of debt in real estate, the rapid growth and complexity of shadow banking in China, and the off-balance sheet borrowing by local governments.

Finally, here is my attempt to cut to the chase – (emphasis mine) from the McKinsey research piece:

Government debt has now reached high levels in a range of countries and is projected to continue to grow. Given current primary fiscal balances, interest rates, inflation and consensus real GDP growth projections, we find that government debt-to-GDP ratios will continue to rise over the next five years in Japan (where government debt is already 234 percent of GDP), the United States, and most European countries, with the exceptions of Germany, Ireland, and Greece.

It is unclear how the most highly indebted of these advanced economies can reduce government debt. We calculate that the fiscal adjustment (or improvement in government budget balances) required to start government deleveraging is close to 2 percent of GDP or more in six countries: Spain, Japan, Portugal, France, Italy, and the United Kingdom (Exhibit E4).

Attaining and then sustaining such dramatic changes in fiscal balances would be challenging. Furthermore, efforts to reduce fiscal deficits could be self-defeating— inhibiting the growth that is needed to reduce leverage.

Nor are these economies likely to grow their way out of high government debt…

Here is the link to the full piece.

My general view is that we are witnessing the beginning of a global sovereign debt crisis. Perhaps Greece will be the first meaningful domino to fall. The risk is the follow-on behavior of equally troubled neighbors – pressure is mounting to “cut the debt”.

The debt deleveraging cycle has yet to begin. Deflation has gained traction. Europe looks to be stepping center stage. Like a game of dominoes, we’ll have to carefully watch what happens once set in motion. Greece, Spain, Japan, Portugal, France, Italy, China, U.S.

The currency wars are clearly advancing. Pressure is building.

Simply writing down the debt comes with great consequence: pensions become impaired (as pensions are large holders of Greek, Italian, Spain sovereign debt). Write down the debt and the bank’s collapse. A mighty fine mess we are in. It will likely take a crisis to reset the system.

I have no answer as to how it all plays out (wish I did); yet, if I’m correct and your portfolio is more broadly diversified and risk managed, you will be positioned to take advantage of the buying opportunity such a correction will create. In the meantime, you can continue to seek growth.

I have finalized a research piece on investment correlations and have nearly finished a research report sharing some ideas around portfolio construction. I’ll provide you with a link as soon as they are published.

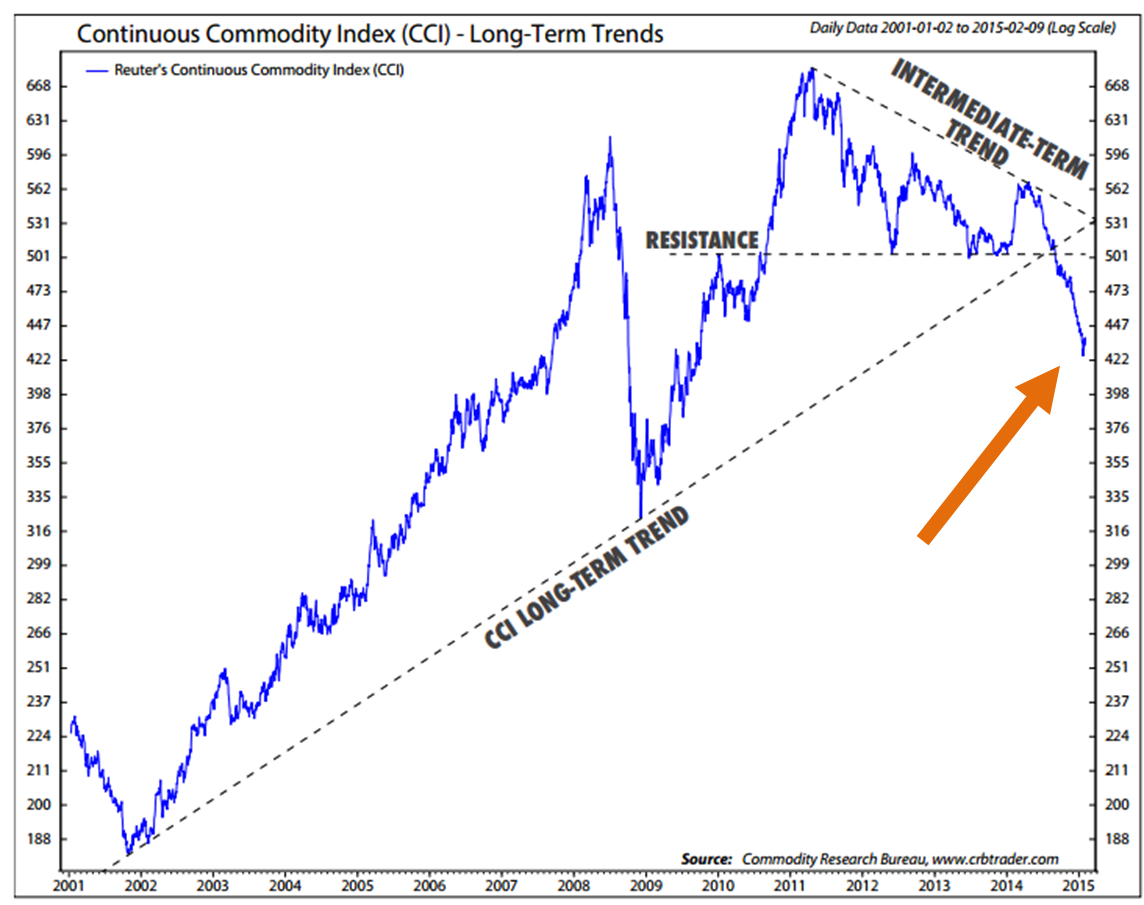

Commodity Bear Market – A Quick Look at Long-Term Trend

The message here is pretty clear. Commodities are in a bear market. Such bear cycles in commodities tend to last a long time. Slowdown and deflation? Certainly an impact. Oversupply near the top of the cycle – another factor.

To me, it seems probable that the CCI will bounce back to the dotted “RESISTANCE” line. I’d use that technical level to reduce exposure.

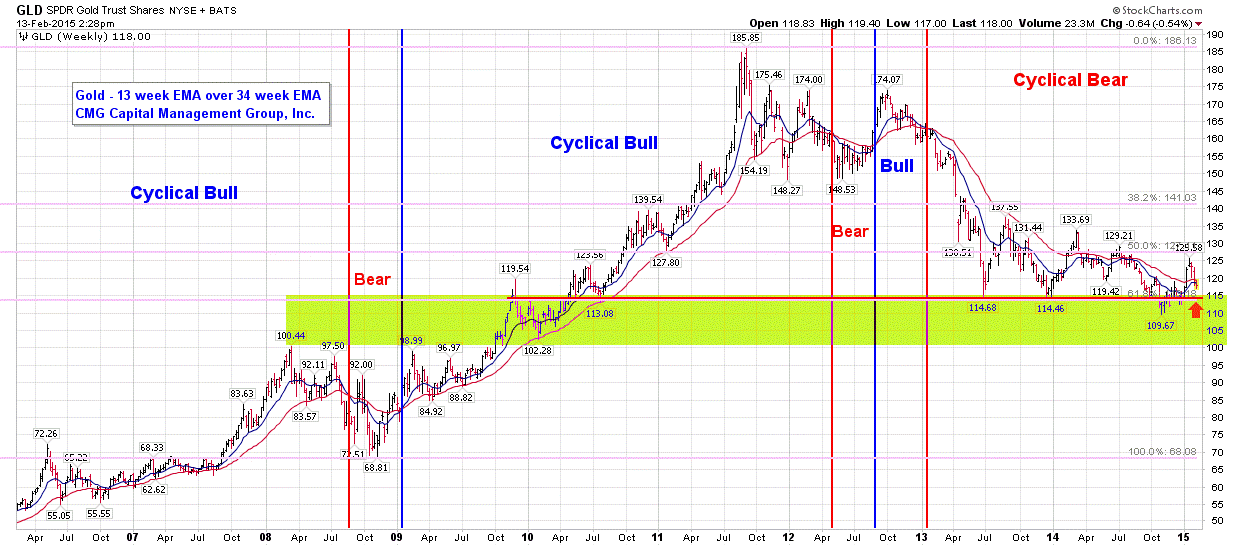

Here is a possible way to look at risk managing your gold allocation. I put a 13-week over 34-week EMA (Exponential Moving Average) on a weekly chart of GLD (a gold ETF). While there are no guarantees in this business and certainly some trades will do better than others, this is a process that can help your risk manage the exposure.

While I’m generally bullish on gold (as it is a hedge against the insanity of governments and global central bankers), it will be a bumpy ride to higher prices and, frankly, my fundamental view could prove to be wrong. This simple trend following approach can get you in and out.

Here is how it works: buy when the blue 13-week trend line is above the red 34-week trend line and reposition to something else when it is in a bear cycle. One idea is to hold a minimum 5% position in a portfolio and when in a cyclical bullish period, take that position up to 10%, 15% or 20% depending on your clients’ needs and risk tolerance.

A similar process can be applied on most any ETF. See more in the Trade Signals piece below.

Just an idea to consider.

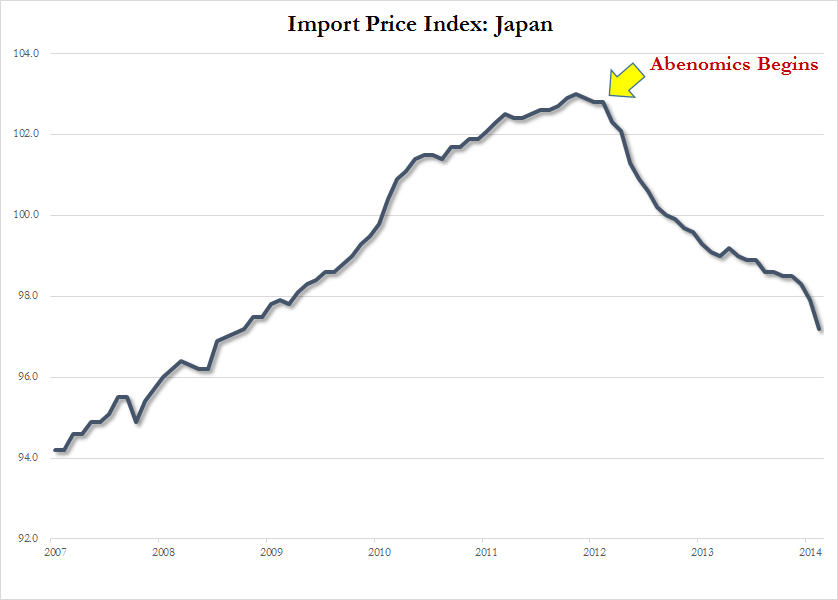

More on Deflation – From CMG’s Kevin Auerbach

Kevin sent me the following charts this morning. In the inflation/deflation battle, deflation is winning (at least for now). Of the two enemies, inflation is favored.

Import prices dropped 8.0% YoY (modestly beating expectations of an 8.9% plunge) and 2.8% MoM. The last time import prices started to fall at this pace was a month after Lehman Brothers failed. Of course, the crash of oil prices is largely responsible as imported fuel costs slumped 16.9% YoY – the most since December 2008 (petroleum -17.7%). However, the price of imported capital goods collapsed the most since March 2009 with the biggest rise in Japanese (foreign central banks) exported deflation since April 2013 (when QE really accelerated).

As the world’s central banks export deflation on to U.S. shores…

Charts: Bloomberg

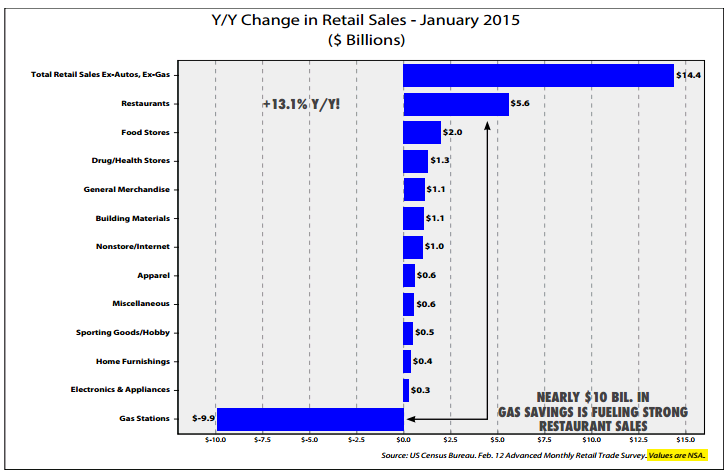

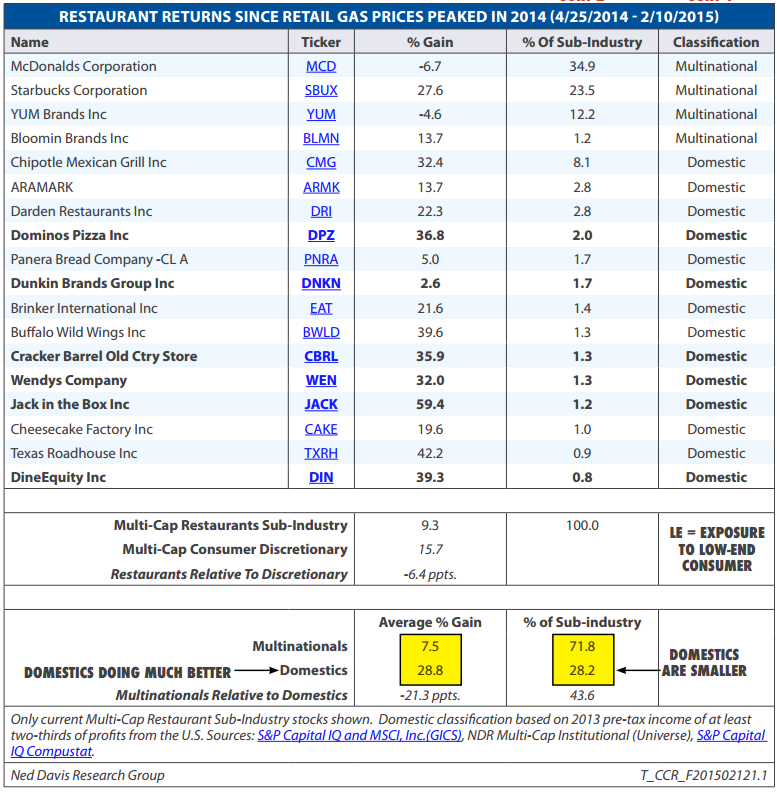

And in Case You’re Wondering Who’s Benefiting From Lower Gas Prices – It’s Restaurants

Put this chart in the “curious” category. CNBC has been asking CEO after CEO if lower gas prices are showing up in sales. The consensus answer is no. In fact, the latest retail sales data shocked to the downside. I continue to believe the overriding problem is too much debt.

With gas savings on everyone’s mind, I found this chart in an NDR research report titled, Are Consumers Eating Their Gas Savings? Anyway, if you were wondering, like me, who might be seeing a pickup in sales it looks to be the restaurant industry (especially domestic restaurants).

I have limited knowledge on this particular category except I do love a good Dunkin Donuts coffee and spend a lot of time at Chipotle Mexican Grill (which is also a stock we own in our global equity strategy). But please know this is not a recommendation to buy or sell any security.

Trade Signals – Not Greedy Not Fearful, Trend Evidence Positive- 02-11-2015

Overall, despite many well-founded global fundamental concerns as well as the aged nature of the current cyclical bull move, the weight of evidence continues to support a bullish market view on U.S. equities. Risk remains elevated to high current valuations and low probable 10-year forward returns.

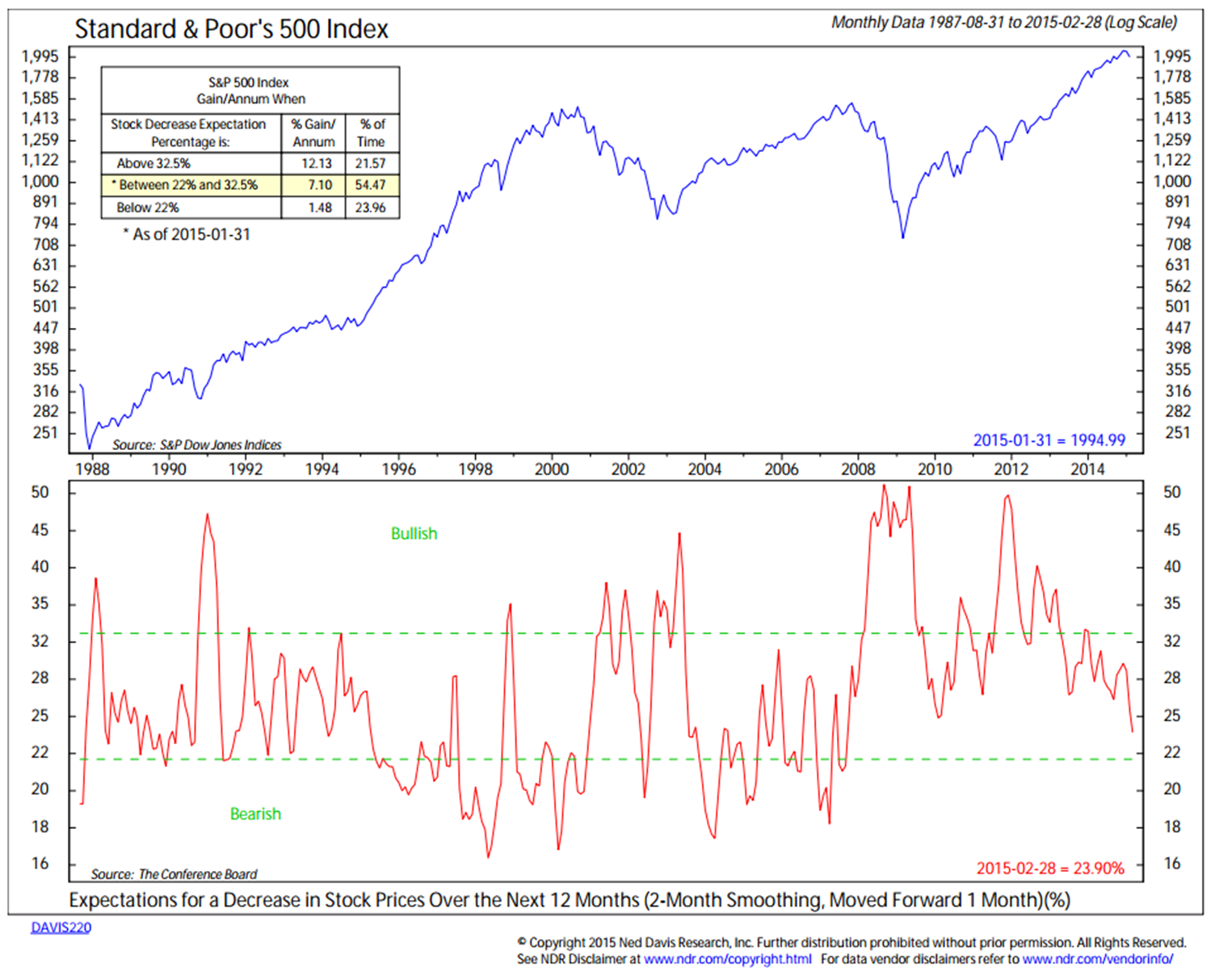

I came across the following chart this week. It speaks directly to investor behavior and how it tends to be wrong (behaviorally buying and selling at the wrong times). Often quoted Warren Buffett says, “Be fearful when others are greedy, and be greedy when others are fearful”. Today, evidence is neither greedy nor fearful.

Special Chart #1 – Expectations for a Decrease in Stock Prices

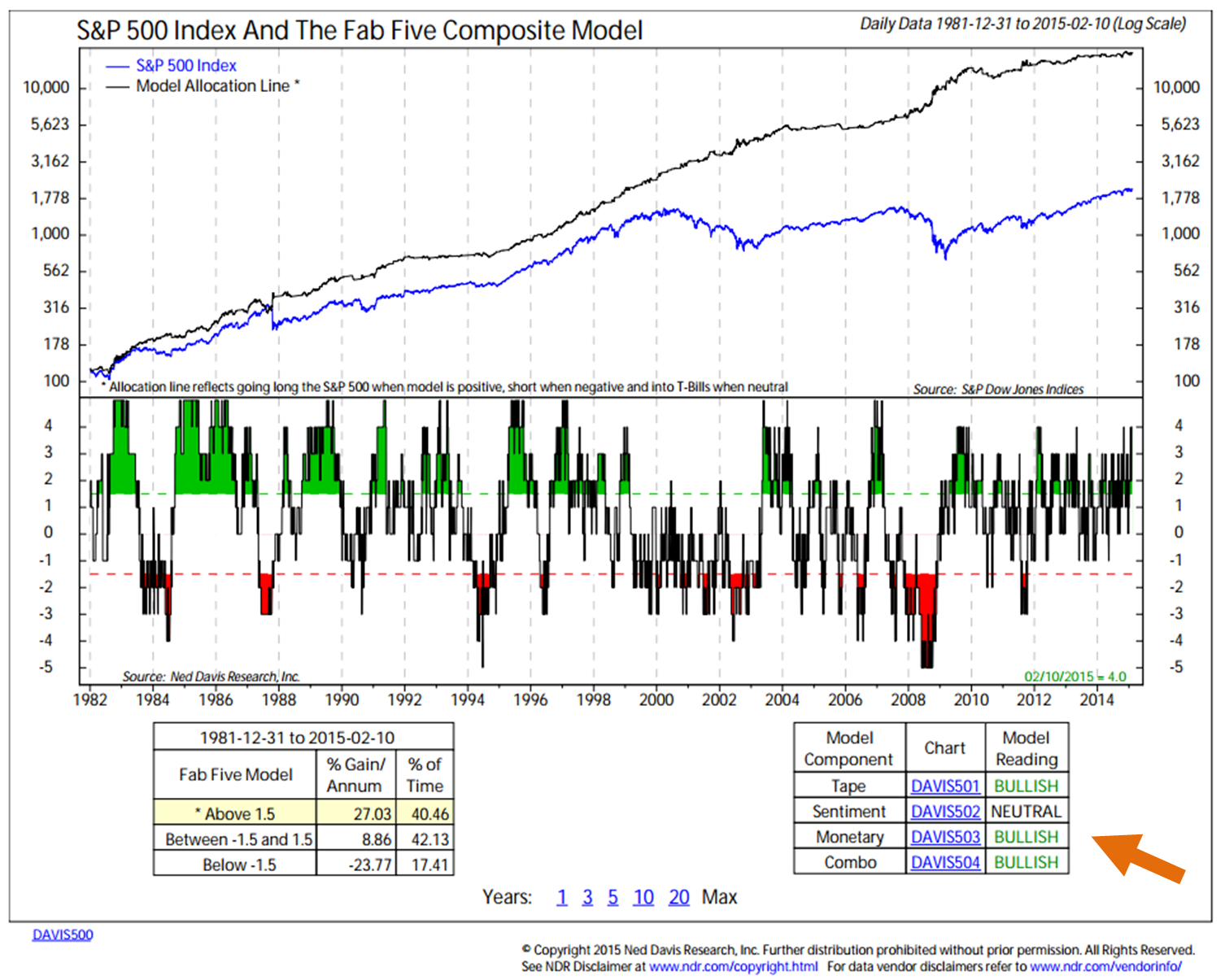

Special Chart #2 – Fab Five Composite Model

I regularly keep an eye on the above chart as it looks at the Tape (trend evidence), Investor Sentiment, Monetary Policy and something called Combo. I find it to be a quick dashboard-like summary review. Note in the bottom right section of the chart that three of the four components are bullish.

- If you would like to get a feel for what makes up the components, please drop me a note.

- You can go to ndr.com to learn more about their research service. I am a long-time customer and very big fan.

Included in this week’s Trade Signals (posted are the usual weekly charts):

- Cyclical Equity Market Trend: Cyclical Bullish Trend for Stocks

- Volume Demand Continues to Better Volume Supply – Bullish for Stocks

- Weekly Investor Sentiment Indicator:

- NDR Crowd Sentiment Poll: Neutral Optimism (short-term neutral for stocks)

- Daily Trading Sentiment Composite: Extreme Pessimism (short-term bullish for stocks)

- The Zweig Bond Model: The Cyclical Trend for Bonds Remains Bullish

Click here for the full piece.

Personal Notes

What beat me was not having brains enough to stick to my own game – that is to play the market only when I was satisfied that precedents favored my play”, Jesse Livermore – Reminiscences of a Stock Operator

Odds point to lower growth. Debt is a problem and current high valuations point to a period of enhanced risk. A better risk plan today will lead to significant opportunity when “the precedents” better favor the play. I plan to stick to my game plan.

Dallas, then Arkansas and New York were to follow in early March but I’ve hit a personal snag. Acting more like 23 than 53 I caught a little too much air skiing last Saturday and I’m sad to report that I’m one of the newest members of the torn ACL club. Surgery is set for March 2. Apparently, I have the option to watch the process…have to think on that!

My father used to have a saying as it related to the bumps we all take with sports in our lives, “The prize is worth the price”. It carried me through a number of bumps over the years. He’d probably whisper to me now something like – “what in the world were you thinking?” I’m in good spirits and will keep moving forward.

Hope you and your family are well and doing something fun this holiday weekend.

Wishing you the very best.

Have a great weekend.

With kind regards,

Steve

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM: Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456. Please read the prospectus carefully before investing. The CMG Global Equity FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA. NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, or the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

(c) CMG Capital Management Group

© CMG Capital Management Group