I spend a great deal of time writing about valuations, probable future returns (near record lows today), portfolio construction and risk management. Reflecting on four days of non-stop sessions, media interviews and meetings at the Inside ETFs Annual Conference this past week, I thought I’d share several key takeaways with you.

Rock star advisor Ric Edelman believes older advisors will decide that making the changes to adapt to a world slowly shifting to online money management isn’t worth the considerable effort.

Steve here: Advantage to those advisors who weave advanced technology into their practices – not only to enhance efficiency and firm wide productivity but to effectively provide better client education and reporting tools to fully showcase your value proposition. I have some great ideas around this – just drop me a note.

Heidi Richardson, BlackRock’s Global Investment Strategist, sees “a bumpier road ahead for stocks,” Vanguard’s Joe Davis highlighted three headwinds facing investors: ultra-low rates, low spreads and high valuations; concluding that Vanguard has the most guarded outlook since 2006. Jeff Gundlach did not disappoint – believing the yield on the 30-year Treasury bond is headed to 2%. More on this within the body of this OMR.

ETFs are certainly growing at warp speed. Vanguard has just surpassed State Street Global as the #2 ETF firm by assets ($432.65 billion vs. $431.80 billion). BlackRock remains the world’s biggest ETF company with $756.42 billion. Combined, the three firms account for nearly 80% of the nearly $2 trillion invested in ETFs. Vanguard’s office complex is just four minutes down the road from our offices. Good news for the local economy.

Expect the fee compression in the space to continue. Vanguard’s funds are structured so that fund fees come down as their assets increase. Who would have imagined a 5 bps fee for exposure to the S&P 500 index? And BlackRock iShares has over 300 diverse ETFs you can use to create more balanced and broadly diversified endowment like portfolios. That’s good news for all investors, good news for ETF strategist firms like CMG and very good news for you and your firm.

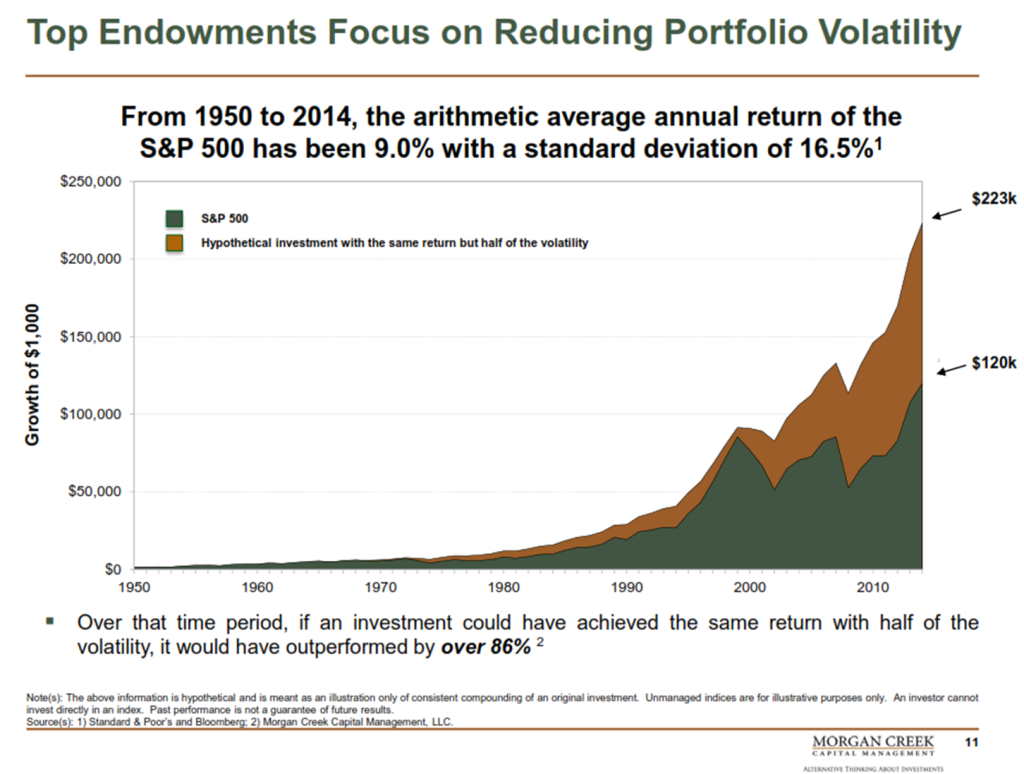

Mark Yusco presented the following on the importance of portfolio diversification. Academic literature shows that 85% to 90% of a portfolio’s returns come from: Asset Allocation (“the largest driver of return”), Manager Selection and Portfolio Construction (“the most overlooked opportunity”) according to Mark. Share the following chart with a client who is upset that his broadly diversified portfolio didn’t outperform a particularly concentrated risk like the S&P 500.

This chart may surprise you, as it did me.

What the data says is that a 9% return delivered with half the risk (as measured by a standard deviation of 8.25%) outperformed the 9% return the S&P 500 delivered at twice the risk (as measured by a standard deviation of 16.5%) by over 86%. It is about understanding the math of loss.

Frankly, I believe this to be an advisor’s number one value proposition and maybe why I find this business to be so exciting. I know, I’m told I need to get a life. Efficient and diverse tools along with enhanced technology are all available today. Nothing like it was when I started in the business in 1984. Heck, I couldn’t get my dad to use email in 2000. Today – way too cool!

In this week’s On My Radar I share a few more notes from the Inside ETFs Conference and end with a cogent piece on Greece. Go Ahead, Angela, make my day:

- Rob Arnott on Forward Returns – Two Quick Charts on Probable Forward Returns

- Top Takeaways from Jeff Gundlach’s Keynote Presentation

- Blackrock’s iThinking – A Fantastic Idea/Resource

- Investors Have Woken Up to Greece’s Nuclear Risk – Ambrose Evans-Pritchard

- Trade Signals – Pessimism Remains, Trend Still Positive – 01-28-2015

Rob Arnott on Forward Returns – Two Quick Charts on Probable Forward Returns

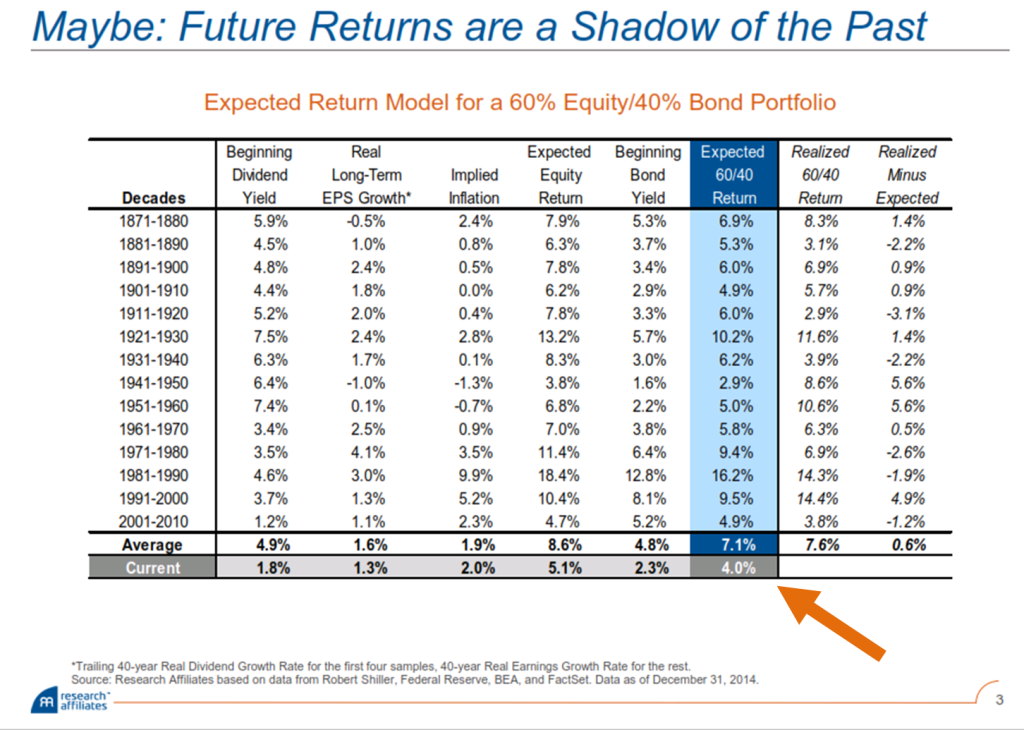

The data below, courtesy of Research Affiliates, looks back to every decade starting in 1871. In simple form, it looks at four factors to determine what the forward return will be for stocks, bonds and the popular 60/40 allocation mix.

For stocks: add together Beginning Dividend Yield, Real Long-Term EPS Growth and Implied Inflation to get to an expected equity return. You can see that the Expected Equity Return (as of December 31, 2014) is 5.1%.

For bonds: take the yield on the 10-year Treasury to come to the Beginning Bond Yield (as of December 31, 2014) or 2.3%.

60% of 5.1% plus 40% of 2.3% gives you an Expected return of just 4.0%.

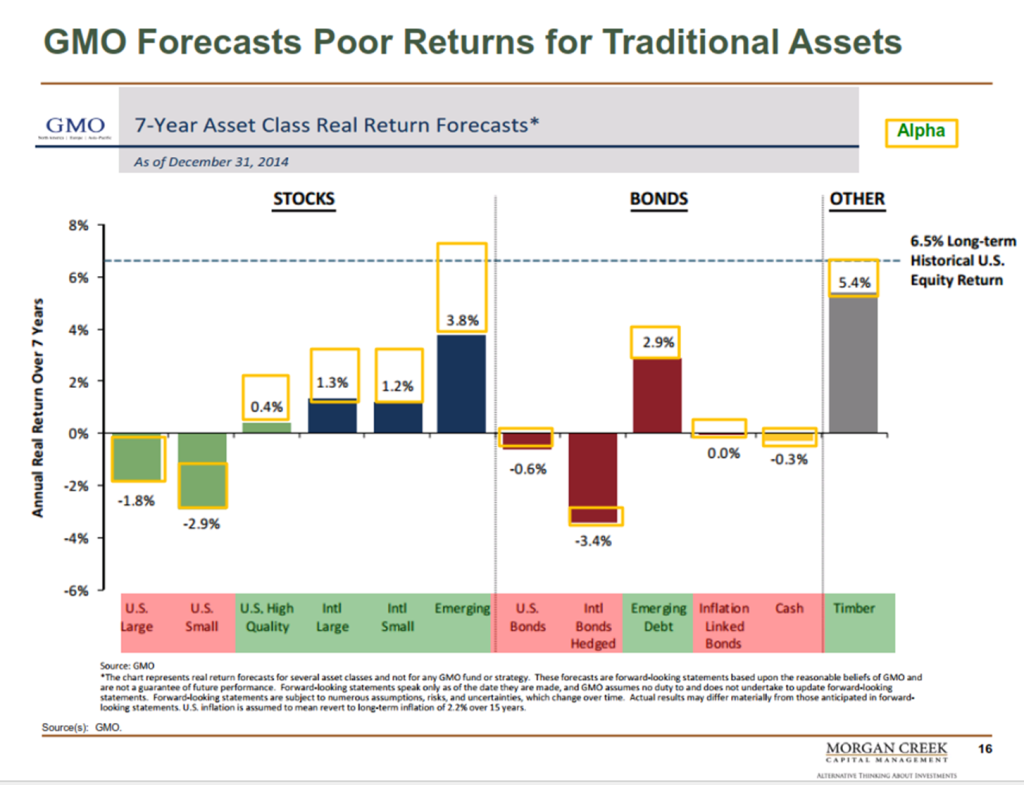

Other expected return models are slightly less optimistic. Yusco presented this next chart from GMO (it may look familiar as I’ve posted it a number of times. Following is GMO’s most recent 7 year Asset Class Real Return Forecast (to get it up to nominal, add to each category roughly 2% implied inflation).

Zero to nominal returns for seven years and today’s current 10-year Treasury yield of just 1.67% (“wow” is all I can say seeing that yield) equals a need to build more broadly diversified portfolios that include disciplined tactical strategies (experienced managers) that seek to allocate to assets that are showing the strongest price leadership.

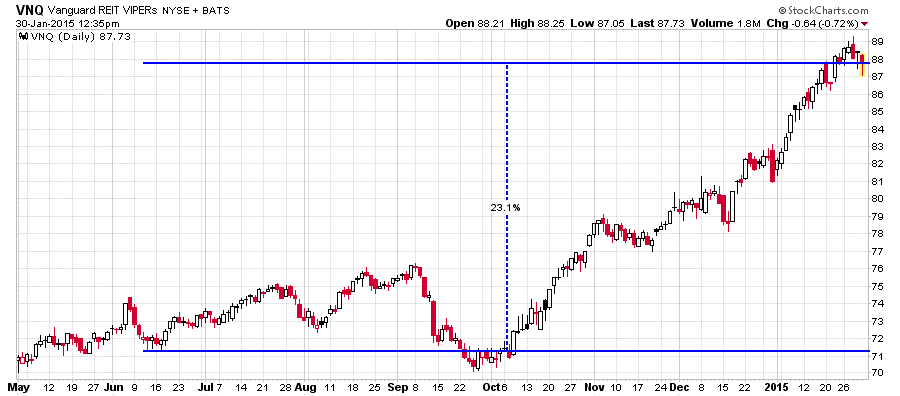

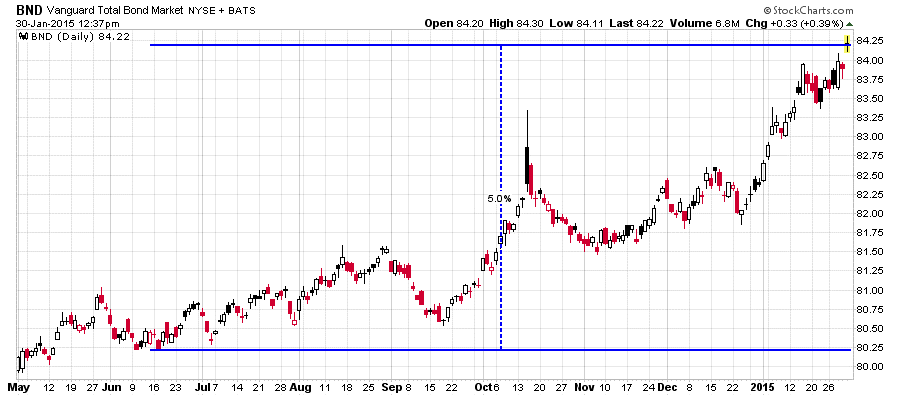

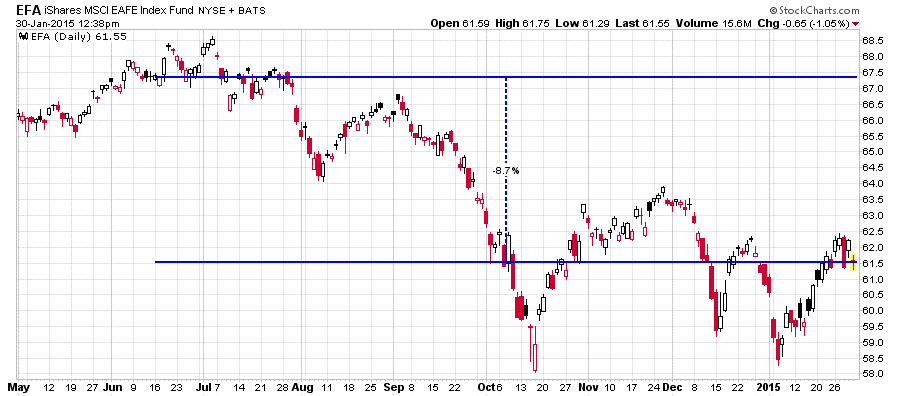

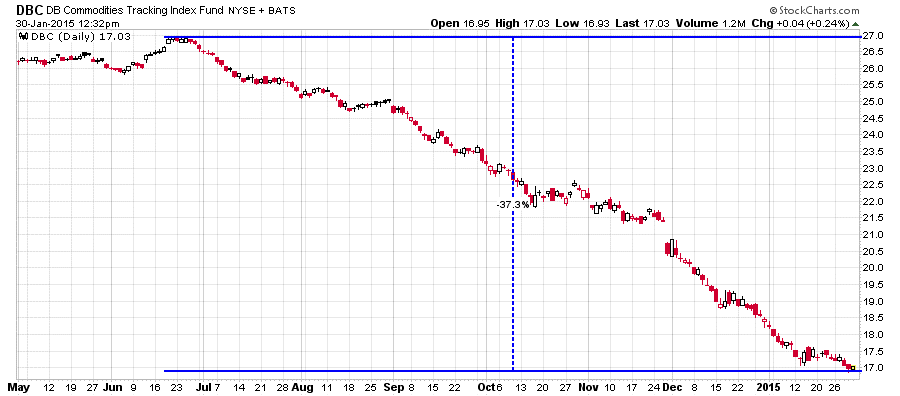

Here is an example of how it works: Take a look at the following six diverse ETFs (returns highlighted since June 16, 2014).

Take a look at the returns of each ETF. If one compares the relative strength of each against each other, it is pretty easy to see where it would have been best to be over the last six months. A systematic relative strength based tactical trading strategy looks to position in leadership (in this case allocate to the top two) and avoid those performing the worst with a rules based disciplined entry and exit process.

The above six investment categories make up our CMG Tactical Rotation Strategy. As mentioned, the goal is to position to the two categories showing the strongest relative strength and avoid those that are the weakest. We believe there is always an asset that is gaining in price though that asset may be bonds or T-bills.

Such strategies offer broader risk diversification value within a portfolio – enabling stronger, more resilient portfolios. Our strategy has been positioned in the S&P 500 and REITs for most of the last six months. Of course, as with all investments, past performance offers zero guarantee. ETFs offer you the ability to create your own or outsource to an ETF Strategist like CMG.

Top Takeaways from Jeff Gundlach’s Keynote Presentation

- Japan – very little success with QE

- U.S. – very little success with QE

- EU – likely they will have very little success with QE

- Yields are down everywhere. The yield curve is flattened across the globe in 2014.

- The Treasury bond not only fell in yield but it did it in an almost steady decline. 2014 was the fourth best year for Treasury bonds. The best year was in 2008.

- He believes the Fed will make an attempt to raise the Fed Funds rate feeling they have to do something to move in that direction but such move will be short-lived. Raising short-term rates will further push the dollar higher and cause the U.S. to further import deflation. (Something I’ve written about – agree)

- The dollars’ long-term down trend line (since 1981) has been powerfully broken. The dollar rallied against almost every global currency in 2014 and it is going to continue. He noted that currency secular cycles last a very long time.

- He thinks the employment/labor market picture in the U.S. looks better. The number of people seeking disability is down to zero (year over year) and food stamp usage has flattened out (though yet to decline)

- The decline in oil prices is flat out positive for economic growth

- He remains bullish on S&P stating the U.S. is clearly the place to be. The strong dollar should continue to help that view. He favors cyclicals.

- Several negatives:

- The S&P has never been positive seven consecutive years in a row – data going back to 1904. It has been positive each of the last six years.

- Margin debt is a worry. When it peaks and rolls lower, it is usually bad news for the equity markets. It appears to be rolling over.

- On inflation: CPI level is lower than it was seven to eight months ago. The story is one of deflation. Deflation is already being imported to the U.S.

- The junk bond market is a wonderful forward leading indicator and today looks “flat out ugly”. (I’ve noted over many years that it leads the economy and the stock market – see Watch Junk Bonds Forbes piece)

- The good news short term is that junk bonds are no longer richly priced saying, “They are now just a little cheap on their way to really cheap” and added, “the good news is that most of the debt is not set to mature/rollover until 2017-2018.” (Steve here – stay tactical with HY). Steve again: the total size of the U.S. high yield bond market is approximately $2 trillion. Approximately $50 billion matures in 2015-2016, $160 billion in 2017-2018, $370 billion in 2019-2020 and nearly $400 billion in 2021-2022.

Blackrock’s iThinking – A Fantastic Idea/Resource

I had a totally enjoyable evening at the BlackRock client dinner last Sunday. I was seated next to an extremely bright and passionate Heidi Richardson, BlackRock’s Global Investment Strategist.

She shared with me, and later shared in her InsideETFs conference presentation, BlackRock’s view on 2015. Summed up it will be “a bumpier road ahead for stocks” but resist the urge to exit. Further, and this is what I want to share with you, BlackRock created a website that expresses what they feel are the best of the research ideas – as can be expressed through ETFs.

It was Heidi’s creation and I think a good one. Being around so many research analysts and hedge fund managers, I’ve always quietly leaned in favor of those who have real money on the line. It is just different when your skin is in the game. Passion is important but so is the skill to execute a trade. She reminded me of some of the great hedge fund managers I know. It was a fun dinner.

iThinking is the best thinking of all of BlackRock’s views: For example, Heidi’s says the number one idea is U.S. Technology expressed through “IYW”. Number two is Japan and she likes it unhedged expressed through “EWJ” but hedged is available via “HEWJ”.

There are more, of course, and those recommendations do not necessarily reflect my views nor CMG’s. I do still like short yen and Japan hedged. When the world’s largest pension plan says it is going to increase its allocation from 12% to 25% in Japanese equities, that’s a big demand shift and others will likely follow. I still think the Yen has much more to fall. Heidi thinks it may fall more but the fall has been pretty large already. Here is the link: www.iShares.com/iThinking.

See the full story and important disclosures in On My Radar: Go Ahead Angela, Make My Day.

Steve Blumenthal is founder and CEO of CMG Capital Management Group and contributor to CMG AdvisorCentral.

© CMG Capital Management Group