Not everyone is happy about the dollar’s recent strength

February 6, 2015

My son is tagging along with me on a trip to Europe next month. He’s going to be taking organic chemistry this summer and has military commitments for the summer following that one. So he deserves a bit of a break. My only concern is what he might end up doing with his free time while I am working; the pubs may be a temptation.

Whatever he decides to do, he’ll certainly enjoy the renewed strength of our dollar. The purchasing power of Americans traveling abroad has grown mightily since last summer, providing welcome relief to those of us who had come to expect paying the equivalent of $10 for a small cup of coffee.

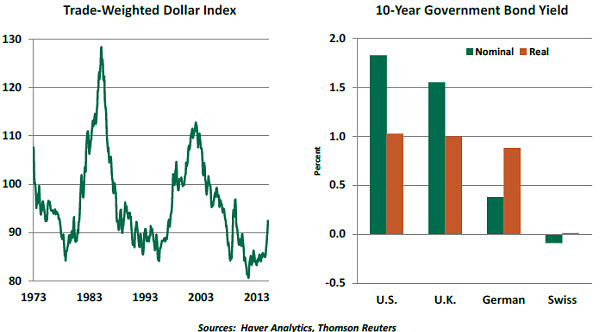

But not everyone is happy at the dollar’s revival. It has hindered American exporters and lowered the value of offshore profits for American multinationals. Inbound capital flows have caused the yield on long-term U.S. Treasury bonds to fall sharply to a level that the Federal Reserve might find undesirable.

A key question as we move through the first quarter of the year is how strong will U.S. policymakers allow the dollar to get before changing their tone and their strategy. The Secretary of the Treasury has been quiet on this front but may not remain so for too much longer.

It isn’t surprising that the U.S. dollar has gained. American growth has been the strongest in the developed world, and the Federal Reserve stands as the only major monetary authority that still seems to be on track to reduce policy accommodation. The trend could have some distance to travel; the recent dollar appreciation is modest compared to past episodes.

Global asset allocation decisions may be accentuating the trend. The demand for safe assets has risen as investors take account of rising levels of market volatility and renewed uncertainty from places like Greece, Russia, the Middle East and China (to name a handful). An expanding number of jurisdictions have pushed government bond rates into negative territory, prompting migration to those markets that still have positive yields and a stable outlook.

When the U.S. dollar rally began last July, it carried on with the tacit approval of American policymakers. Faltering global growth is seen as a significant risk to the U.S. outlook, a point highlighted in the statement following the Federal Reserve’s most-recent meeting.

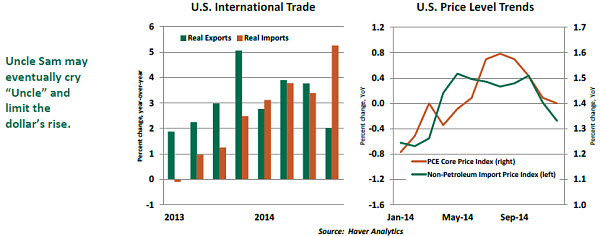

Because exports account for only 13% of U.S. gross domestic product (GDP), any negative impact from changing terms of trade was seen to be manageable, temporary and offset by gains that would accrue if other world markets found firmer footing. But as the rally continues, it will produce several discomforts for the United States.

- Export growth cooled substantially in the final three months of last year, and major exporters are complaining. Earnings reports for the fourth quarter reflected softer foreign sales and foreign earnings that were worth less in U.S. terms.

- Falling import prices are adding to the challenge of restoring targeted levels of inflation. The eight-month-old oil price realignment is certainly part of this, but other purchases from foreign sources are placing downward pressure on the price level.

- Yields on U.S. government bonds have fallen sharply. This has the effect of easing financial conditions at a time when the Federal Reserve has been talking about making them somewhat less-accommodative. With the front end of the yield curve still positioned for short-term rate hikes later this year, the term premium for extending maturity has gotten very thin.

Some suggest that the dollar hasn’t moved all that dramatically, and that these side effects are minor compared with the benefit of taking out insurance against global recession. Yet there is no end in sight to the recent string of central bank easing around the world, which promises to put the dollar under even more upward pressure.

Ultimately, there may be a limit to the Treasury Department’s understanding. Currency markets may trade apprehensively in anticipation of such a statement.

I’ve claimed that I engineered the recent rise of the dollar to help finance my son’s fun while on spring break. But taking that credit would also expose me to considerable blame. One does not want to get on the Treasury Department’s bad side; it runs the Internal Revenue Service, and I would prefer to stay in its good graces as tax season approaches.

Grecian Burn

These are nervous days in Europe, as discussions surrounding Greece’s financial fate progress. We don’t expect a worst-case outcome, but we don’t expect either party to the negotiations to yield quietly. The situation represents significant “event risk” for world markets.

Initial steps taken by Greece’s new prime minister seemed designed to irritate his eurozone creditors. There was an overture to Vladimir Putin and the appointment of a firebrand finance minister. Proposals emerged to restore thousands of government jobs eliminated as part of the country’s austerity program and grant wage increases to a wide swath of government workers.  Provocative on the surface, these moves are the first steps in a complicated dance. The newly elected must play to their supporters first, before pivoting to diplomacy. Given the short longevity of the average Greek government, Prime Minister Alexis Tsipras needs to solidify his standing at home to have the strongest possible standing in negotiations with Greece’s bondholders.

Provocative on the surface, these moves are the first steps in a complicated dance. The newly elected must play to their supporters first, before pivoting to diplomacy. Given the short longevity of the average Greek government, Prime Minister Alexis Tsipras needs to solidify his standing at home to have the strongest possible standing in negotiations with Greece’s bondholders.

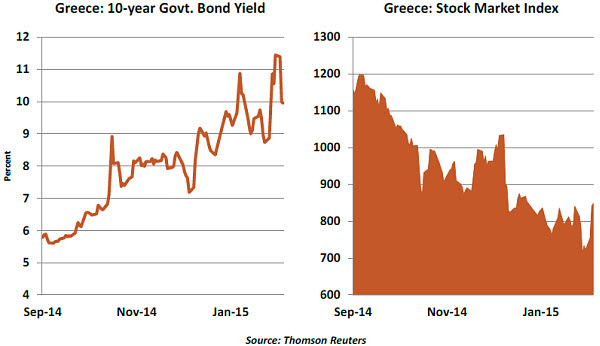

While the public cheered these steps, investors had the opposite reaction. Yields on Greek debt have risen sharply, the Greek equity markets have sold off and deposits are leaving Greek banks at an alarming rate.

As an ameliorative step, Tsipras retreated from his insistence on debt forgiveness. Instead, he asked to extend the maturity of some Greek government bonds (in some cases, into perpetuity) and swap others for instruments whose yield would be tied to the growth rate of Greek GDP.

European institutions hold almost 80% of Greece’s debt. The biggest of these, the European Financial Stability Fund (EFSF), is jointly owned by all the eurozone countries. Terms of the EFSF loan are incredibly generous: a 32-year maturity and an interest rate of 1.5% whose payment has been deferred until 2023. After serial restructuring over the past six years, questions might be asked whether this debt is sustainable; if it is not, institutions like the International Monetary Fund are not allowed to extend themselves further.

Linking bond yields to GDP sounds creative but would leave investors at the mercy of Greek economic performance, over which they have little control. This kind of risk-sharing is unprecedented in the markets for sovereign debt in developed countries.  Tsipras also wants relief from the aggressive budget targets outlined during Greece’s last debt restructuring. This would allow room to use fiscal policy to promote growth. But given Greece’s ongoing need for structural reform, creditors fear that allowing relief would permit Greece to backtrack on measures designed to make the country more competitive in the long run.

Tsipras also wants relief from the aggressive budget targets outlined during Greece’s last debt restructuring. This would allow room to use fiscal policy to promote growth. But given Greece’s ongoing need for structural reform, creditors fear that allowing relief would permit Greece to backtrack on measures designed to make the country more competitive in the long run.

The next major milestone on the calendar is February 28, when Greece’s most-recent round of emergency funding runs out. The country has some reserves to tide it over for a time but risks losing access to emergency liquidity from the European Central Bank (ECB) if a new agreement with creditors has not been reached by then. Concerned about the state of debt negotiations, the ECB will cease accepting Greek sovereign debt as collateral later this month.

All parties to the negotiations have said that they want Greece to stay in the eurozone. But this shared desire has created a game of chicken between the two sides. The inexperience of the new Greek leadership brings an added element of uncertainty to the process.

Other debtor countries in the eurozone are watching the outcome closely. If concessions are offered to Greece, it could serve as a benchmark for others. And if the worst comes to pass, and Greece is excused from membership in the euro, the economic implications for all concerned would be severe.

In the end, we expect cooler heads to prevail. More than likely, some financial sleight of hand will be designed that allows both sides to claim victory. But there could be a lot of finger- pointing before the final handshake.

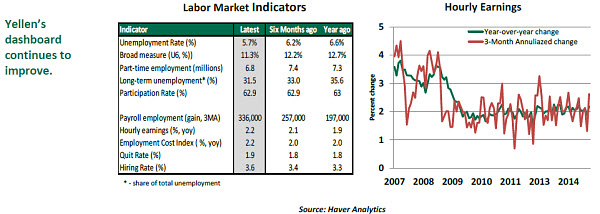

U.S. Hiring Advances, Wages Move Up

Amid a steady stream of challenging news from overseas, the U.S. labor market continues to show very strong progress. The January employment readings included significant job gains and better wage growth.

The establishment survey results were much better than expected. It showed that 257,000 positions were created last month, and annual measurement revisions raised overall employment for 2014 by 196,000. A large portion of the revisions (+147,000) occurred in November and December. The average monthly payroll gain in 2014 was 260,000 versus an increase of 199,000 in 2013.

In the household survey, the unemployment rate moved up one notch to 5.7%. But this should not be viewed as a negative; exceptional job creation of 759,000 was offset by a rise in the labor force participation rate (+0.2 percentage points to 62.9%). This suggests movement into the labor force, something that the Federal Reserve has been hoping to see more of.

New population data partly influenced the big jump in the labor force, which most likely will be partly reversed next month. In order to account for these sorts of events, the three-month moving average of the jobless rate is more useful, and it stands unchanged at 5.7% compared with 6.8% in January 2014.

Employment in the goods-producing category rose 58,000, reflecting increased hiring in construction, mining and factory sectors. Service-producing employment advanced 220,000, after a nearly similar increase in the prior month. The large gains were concentrated in health care, financial activities, eating and drinking places, and professional and technical services.

The closely watched hourly earnings number posted a creditable 2.2% year-over-year increase in January and has risen at a 2.6% annualized pace over the past three months. Along with the 2.2% fourth-quarter rise in the Employment Cost Index, a broader measure that includes both wages and benefits, this provides evidence that wage growth is starting to advance.

The January employment report might lead some to suspect that the Fed might consider raising rates at its June meeting. We are still projecting the first increase in September, because:

- The core personal consumption expenditure price index is only 1.3% higher than it was a year ago, which is far below the Fed’s 2.0% inflation target. Market-based measures of inflation expectations are still well down.

- As discussed earlier, the strength of the dollar may hinder growth and hold inflation down.

- Global uncertainty is high, and the Fed will likely want to be sure that its actions won’t add to financial instability.

Nonetheless, the recent run of U.S. employment figures depicts an economy with a good deal of positive momentum. Hopefully, the spending prompted by that momentum will help pull other global markets ahead.

(c) Northern Trust