Everything is awesome

Everything is cool when you’re part of a team

Everything is awesome

When we’re living our dream

Everything is better when we stick together

Side by side, you and I

Gonna win forever

Let’s party forever

Emmet Brickowski

“Everything is Awesome!”

The LEGO Movie, 2014

Last year, Legos hit the big screen. In “The LEGO Movie”, as those of you with children are more likely to be aware, a Lego mini-figure named Emmet Brickowski (from the town of Bricksburg) and his allies save the universe from the clutches of the evil Lord Business. Victory in hand, our Lego friends then party, to the tune “Everything is Awesome”. And indeed, here too in our more mundane real world...everything is awesome! While we see articles pointing out that we should be celebrating improving economic conditions, we don’t see outright celebratory jubilations; economic awesomeness hasn’t yet fully percolated into the mainstream mindset. What, you ask, is so awesome?

• The U.S. unemployment rate last week came in better than expected at 5.6%

• Crude oil, natural gas and coal prices have plummeted. Cheap energy! Energy independence! (Take that, you petro-kleptocracies!)

• The U.S. dollar has been strong, appreciating approximately 18% vs. major currencies since June 2014

• Inflation is low, well below the Fed’s 2% target and likely headed even lower given oil’s ubiquity and recent price drop

• Both preceding statements make it easy for the Fed to continue the cheap money fiesta of recent years… or at least provide enough justification for people to believe they will. “Let’s party forever!”

• Both the U.S. trade deficit and U.S. government budget deficit have come down sharply in recent months

• A slew of new tech companies has emerged and everyone is getting rich...we would add that many of these billion dollar corporations don’t make any money

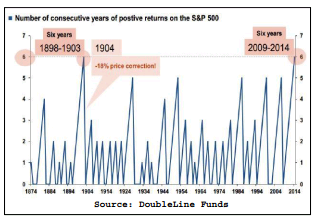

• Six years of substantial stock market appreciation...a rare feat as shown by the chart at right

• If one needs any further evidence that present conditions are improving, just note how the terms “Obamacare” and “the Obama economy” are disappearing and being replaced with “Affordable Care Act” and simply, “the economy”

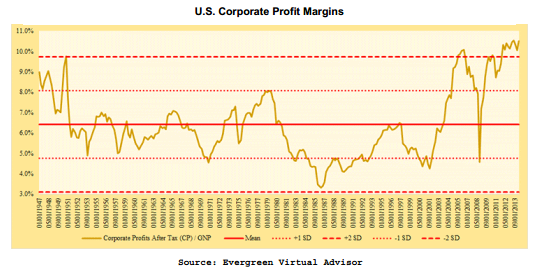

Ok, so things are currently awesome. Unfortunately being awesome isn’t so awesome for equity investors seeking forward returns over the longer term. Huh, say you? Well, say we, great conditions now leave less room for even greater conditions going forward. Yes, while the economy clearly has more room to improve, it is important to remember that the stock market is not the economy. The stock market relates primarily to corporate earnings which have been at record highs for a record duration, as the following chart vividly illustrates.

We wonder how long corporate margins can remain awesome, let alone expand into higher levels of awesomeness. Low unemployment may begin to spur wage growth, which, while great for the economy, won’t be so great for profits. Further, despite low inflation, if and when interest rates finally rise, it may result in a double whammy for stocks: reducing corporate earnings by increasing debt servicing costs, while at the same time reducing the market value of those earnings.

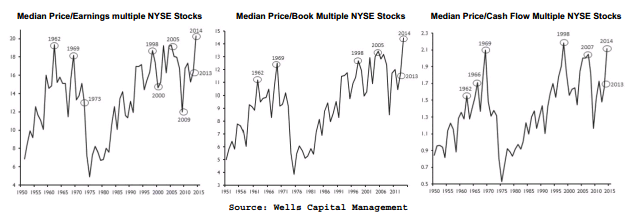

Forward returns also depend greatly on what you pay for awesome. When it comes to U.S. equities, you are paying a lot. “Too much”, we are increasingly thinking. In fact, the median multiples of trailing earnings, cash flows, and book value of the NYSE Composite (a broader collection of companies than those in the S&P 500 Index) are hovering at or above historic postwar highs. The multiples of more commonly cited indexes such as the S&P 500 (which are heavily weighted towards the largest companies) are slightly lower but still near historic highs. This means that, as the below measures show, the “typical” stock is even more expensive than commonly-cited averages indicate.

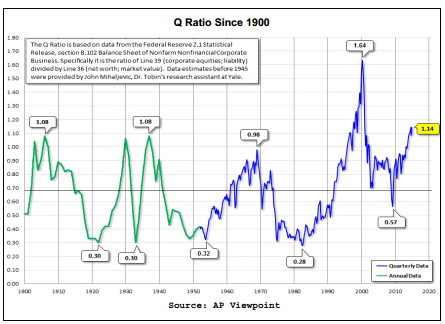

Warning signs are consistent across other measures as well. “Tobin’s Q”, created by Nobel Laureate Dr. James Tobin, measures stock market value to replacement value. Basically this is the ratio of what it would cost you to buy a business versus what it would cost you to build it. As you can see, stocks have rarely sustained a valuation above one, though they (relatively briefly) shot far past this level during the dotcom boom.

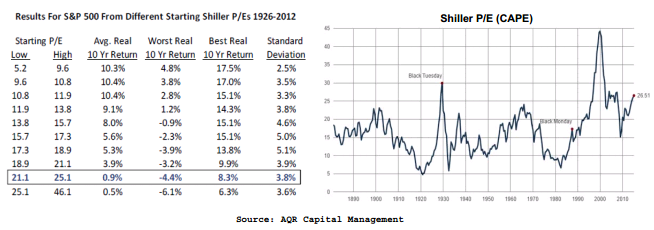

Another way to look at valuation is to use Nobel Laureate Robert Shiller’s Cyclically Adjusted P/E Ratio (CAPE), which is based upon inflation-adjusted earnings from the previous 10 years. This measure has an excellent record of predicting prospective long-term stock market returns. Today’s CAPE is above 26...which, if not quite off the below chart, does fall into the bottom rung of the table, the bottom rung. The table shows that when starting from these levels the real average historical return from stocks over the subsequent 10 years was a half a percent annually.

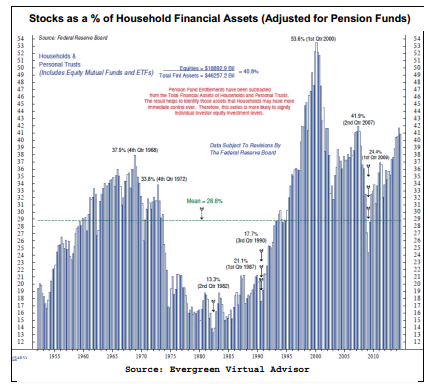

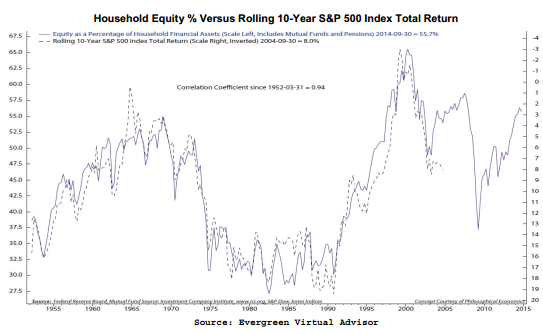

While everyone knows the name of the game in investing is to “buy low, sell high” investors continue to “buy high” thinking that they too will reap the returns they witnessed from the sidelines and forgetting that those very returns have changed the game.1 Stocks as a percentage of financial assets are again reaching high levels...despite (or perhaps, rather, because of) the fact that at this point we are in one of the longest equity bull markets of the last century. For over 60 years this measure of stocks as a percentage of household assets has also shown remarkable negative correlation with forward ten-year returns. The below chart suggests investors should expect low single digit returns for the coming decade2.

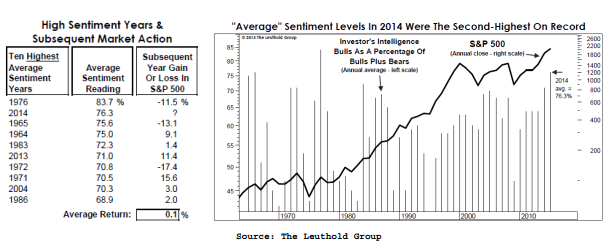

In the nearer term, 2015 may not be so propitious for U.S. equities. Readers know we closely watch investor “sentiment” for contrarian signals. During 2014 one such survey, Investor’s Intelligence, averaged a 76.3% “bullish” reading over the course of the year...the second highest level of optimism over the survey’s history. Equity returns were subpar on average during the year following the nine highest average yearly readings as the table at left highlights.

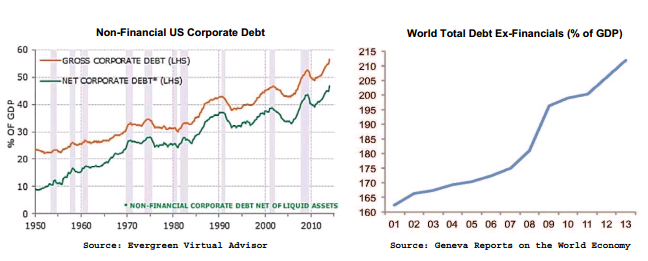

Awesomeness is not only dangerous for valuation reasons; its very stability can set the stage for future instability. As cataclysmic as the global financial crisis may have felt, central banks have been so successful in bringing back stability with low rates that by some measures, risks have actually increased in the system. High debt levels in a financial system are the underlying causes that set the stage for a financial crisis. But high debt levels, even “too much” debt, alone are not sufficient for a crisis. A financial crisis only “flares up” when market participants lose faith that debts will be repaid. Thus, the actual crisis phase of a debt problem, the “flare up”, can be solved by restoring trust, but the underlying driver of a crisis will only be well and truly extinguished when debt is reduced (either by defaults, forgiveness, or erosion via inflation). Therefore it happens that you can temporarily solve a debt crisis by adding more debt to the system, as long as it is debt people trust. This is pretty much exactly what has happened so far with the European debt crisis. The addition of emergency loans to the system has, for now, smothered the flare up...but the stage is still set. One could argue that this has been the case as well with the world economic system. As evidence, we present the charts on the next page showing that both world debt and U.S. corporate debt levels have increased. The stage is set, the seeds are sown, for another financial crisis.

No recent market commentary would be complete without some reflections on perhaps the biggest economic story of 2014-2015: crude oil’s over 50% collapse. While we do believe this development is a net benefit for the country, it is not without its drawbacks: at oil prices anywhere near current levels, the U.S. shale industry will be devastated3. While this is understood by many, we wonder whether it has really been felt. We ask, dear reader: how many energy company bankruptcies have you read about in the papers? None4? How many articles about mass layoffs have you seen? Few? We guarantee these numbers will increase by the end of 2015. And there will be second and third-order effects which have yet to be fully felt. We list some of the potential repercussions below:

• The shale-boom has been financed by debt. To the extent some of these companies default, financial companies will suffer as well.

• Defaults and the specter of defaults affect the credit climate. Already, junk debt credit spreads have widened considerably. The increased difficulty of obtaining financing alone could lead to more energy related defaults since many of these companies are on a treadmill as they need to get more debt...so they can drill more...so they can pay off the old debt. Additionally, energy companies will not be the only ones to suffer from a potentially tougher credit environment.

• Housing prices in energy-rich regions will suffer. If you think Texas housing seems cheap now, just wait. Specifically there could be trouble in Western Canada where housing prices have been in bubble territory for some time. Could this be the shock that pops the bubble?

• Energy service companies will face an environment not only of decreasing demand, but also lower margins as their customers, once scrambling to get drilling, now scramble to cut costs and survive.

• There is a potential for decreased demand for goods from abroad. In theory, every barrel of oil that is bought by one person is sold by another, so more money in one pocket means less in the other with a net effect of zero on total spending power. What this doesn’t take into account is the huge element of general uncertainty that such a monumental change in something as important as oil introduces into the system. The “winners” created by this scenario may be afraid to spend their “winnings”, while the “losers” may cut back on spending by more than the amount of their actual “losses”. The U.S. sells goods to the world; we will not be fully insulated.

• Many “industrial” companies are actually large suppliers to the energy industry. We have heard estimates that count fully one third of U.S. capital expenditures as coming from the energy industry. Considering that the world has spent the last three years executing circa $100-a-barrel projects designed to bring more oil to an unquenchable world, we expect to be swimming in hydrocarbons for some time, and for future energy-related capital expenditures to be slashed considerably, in much greater quantities than have been announced so far.

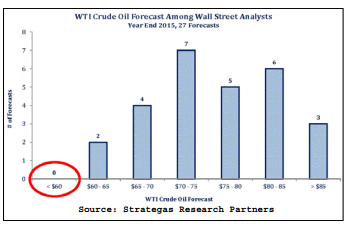

So things are not quite awesome in the oil patch at present. Does this make us excited to invest? We’re interested, but so far are holding off. A quick rebound in the price of oil is the consensus view (albeit a rapidly deteriorating one). Wall Street continues to lack imagination in how “bad” things could get for the energy sector, as evidenced by the chart at left which shows not a single Wall Street analyst forecasts crude to end 2015 below $60. Put another way everyone expects oil to gain at least 20% from current prices. (Update: right before this letter went to press, Goldman Sach slashed its near term oil estimate to below spot, so perhaps a bottom is finally near.)

So, will the shocks from a violent change in the price of the world’s most important commodity be the spark that sets off another conflagration? Probably not...but maybe. The danger of an unsteady, debt-filled environment is that small problems can set larger dominoes in motion. Global debt at oil companies is only $1.6 trillion dollars, which is rather small when compared to global GDP or global debt markets. Then again, total subprime housing debt before the blowup was “only” $1.3 trillion dollars.

So what is an asset manager to do against this backdrop? We must distinguish identification of a precarious situation from a prediction of imminent collapse. Indeed, we consider it a likely scenario that as the U.S. economy becomes more awesome, stock values may continue to inflate. Specifically, when savers fire their underperforming hedge funds and other active managers to invest in indexes, they will effectively be moving more and more money into the largest mega-cap stocks which could send them into overdrive.

We were recently reminded of the difficulty of timing overvalued markets when we went back and read our quarterly letters (available on our website) from the late 1990’s. Those letters presciently warned of the dangers of ebullient markets and inflated valuations… well, maybe not so presciently because our warnings began in earnest in 1997, a full three years, or 12 quarterly letters, before the bubble broke. After reading the same warnings, and watching the markets rip higher for 10 quarters in a row, who could be blamed for firing their underperforming manager and piling into the NASDAQ? Yet, to do so would have been folly...and yet it also would have been folly to be completely out of the markets during that whole period. Thus, instead of running immediately to shelter from a storm that may not break for years, we think it prudent to slowly, ever so slowly, start dialing back risk. We hold more cash than normal. We prefer companies with stronger balance sheets. We look for foreign securities in less inflated markets. We continue to hold our long-suffering gold-related position with the knowledge that gold is often the only asset that doesn’t fall in a crisis...and therefore has the extremely valuable property that it can be sold in a panic to buy other depressed securities. Unfortunately, to not fully invest in the hot market, to not fully participate in the advancing issues of the day, is to almost 10 by definition underperform as the market reaches a top. Yet we feel this is the more appropriate path for long-term preservation and advancement of capital. Rest assured we are investing your capital as we invest our own.

Very Truly Yours,

John G. Prichard, CFA Miles E. Yourman

1The “sell low” part comes later.

2Such potential returns may be disappointing and below long-term average returns from equities, but still may be better than future returns from owning cash or bonds.

3Well, to be more precise, the returns of first generation investors will be devastated. Much shale production will continue...even after bankruptcies as the assets are purchased (or assumed) by second generation owners/investors. Along with technological efficiencies still likely to be gained, the bankruptcies themselves will lower “all in” costs for those who pick up the pieces.

4Some sharp-eyed readers will have noted one recently...interestingly this was because the company in question could not obtain the additional financing they expected.

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

© Knightsbridge Asset Management