Swiss Franc's Surge = Chaos In Global Currency Markets

IN THIS ISSUE:

1. US Economy Stumbled Based on 4Q Reports

2. Swiss Franc’s Surge Led to Turmoil in Global Forex Markets

3. Switzerland Abandons Its Currency "Peg" to the Euro

4. How a Stronger Swiss Franc Will Hurt Its Economy

5. The ECB to Announce QE Bond Buying This Week

Overview

Last Thursday, the Swiss National Bank stunned the financial world by decoupling the Swiss franc from the euro. This surprise move sent the franc up almost 40% against the euro in one day, although it didn’t close that high (up 19%). Nevertheless, many currency traders, banks and brokerages were left with devastating losses. I’ll give you the details below.

But first, let’s take a look at the recent US economic data which has been disappointing overall. Following the stronger than expected GDP growth of 5% (annual rate) in the 3Q, the US economy seemed to stumble a bit in the 4Q. We’ll cover the latest reports before shifting our attention to Europe and Switzerland in particular.

US Economy Stumbled Based on 4Q Reports

A year in which the US economy was supposed to turn the corner and lead the world ended in a bumpy fashion. Retail sales, manufacturing and inflation readings sputtered in late 2014, according to reports released this month. Meanwhile, weekly jobless claims jumped back above 300,000 and a new study called a rebirth of US manufacturing a “myth.”

Economists generally remain hopeful that the new year will turn out well, despite the slowness suggested by the latest reports. Most forecasters still believe that sharply lower energy prices will boost consumer spending this year and breathe life into an economy that grew at about a 2.4% annualized clip in 2014. GDP is expected to climb above 3% for 2015.

However, the early indications are that consumers pocketed the savings they got from plunging prices at the pump. Retail sales for December saw a stunning 0.9% decline, missing even the most modest estimates for the holiday shopping season.

That disappointment was enough for Goldman Sachs to slice its 2015 projection for GDP from 3.1% to2.8% last week, noting that consumer spending “appears at least somewhat less favorable than we were expecting” but noted that fundamentals are still strong due to steady job creation, lower gas prices and rising consumer confidence.

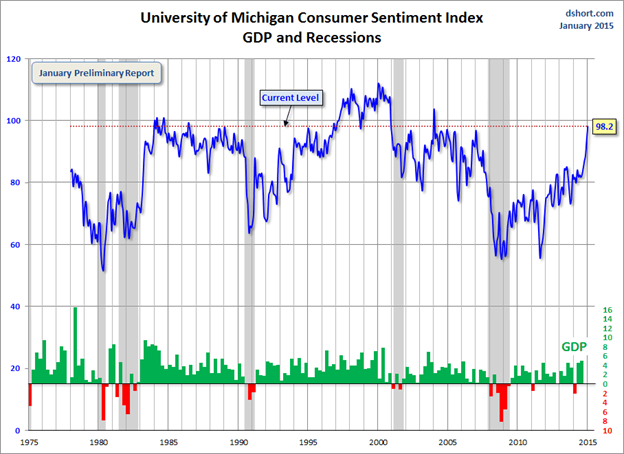

Indeed, the widely followed University of Michigan Consumer Sentiment Index hit an 11-year high in January, which led some forecasters to conclude that the surprise drop in retail sales in December was likely a fluke. We’ll see.

In the bigger picture, rising consumer sentiment is all well and good – and who wouldn’t be happy with gas prices below $2 a gallon? Yet the full economic impact remains to be seen. Saving money at the pump is one thing, but if it doesn’t translate into a more active consumer spending elsewhere, then the net effect is lessened.

As for the manufacturing sector, a new report from the Information Technology and Innovation Foundation, a Washington-based think tank, asserts that the sector’s growth has been merely tepid since the Great Recession ended in 2009. “American manufacturing has still not recovered to 2007 output or employment levels,” the study says. An article on this topic appears in the links at the end of today’s E-Letter.

On another front, interest rates continue to fall more than just about anyone expected. The 10-year Treasury yield has plunged over the last couple of months, falling below 1.8% today, down from 2.25% last month. Meanwhile, the yield on 30-year Treasury bonds has plunged below 2.5%, down from above 3% just a couple of months ago. Most forecasters expected rates to rise in 2015 but are now adjusting their projections lower, while many are rethinking whether or not the Fed will raise short-term rates this year.

A few other things to consider: Years of global central bank easing that has seen more than $5 trillion in liquidity injected into capital markets resulted in surging asset prices, particularly stocks. Yet even that hasn't cured disinflationary pressures, most recently manifested in the biggest drop the consumer price index has seen in six years (-0.4% in December), as plunging energy costs more than offset a 3.4% annualized gain in food prices.

Elsewhere, that 252,000 job creation number from last Friday’s nonfarm payrolls report came with a decline in actual hourly earnings and a 36-year low in the labor force participation rate. While the official unemployment rate unexpectedly shrank to 5.6% from 5.8% in November, the decline was largely due to the shrinking labor force.

Those are the highlights of the latest economic data. Now let’s turn our sights to Europe and specifically the latest shocker from Switzerland, that bastion of fine watches, cuckoo clocks and sound money – at least until last week.

Swiss Franc’s Surge Led to Turmoil in Global Forex Markets

In a complete surprise decision last Thursday, the Swiss National Bank (equivalent of our Federal Reserve) shocked the global financial markets by announcing that it is abandoning its policy of limiting how much the franc can rise against the euro, and therefore the US dollar.

Immediately after the announcement, the Swiss franc exploded higher by almost 40% against the euro on Thursday, which resulted in massive losses at many forex dealers and brokerages that had been “short” the franc due to the currency “cap” or “peg” that was abandoned. Numerous bankruptcies of such firms are expected to be announced in the days just ahead.

Most Americans heard little or nothing about this surprise decision by the Swiss National Bank or the currency market chaos that followed. Yet American investors should know about this because it meansworsening deflation in Europe, a further decline in the euro and an increased chance that deflation will visit our own shores.

Deflation is a very troubling economic development and one that is very hard to reverse. Think Japan over the last two decades – they are still in a deflationary spiral. We do not want to go there. Neither did Switzerland, but that is where the country is almost certainly headed.

I’ll do my best to explain what it all means below. I will also discuss why it is widely expected that the European Central Bank will announce a huge new “Quantitative Easing” program this Thursday in an effort to stimulate the sagging economies in the region. Never mind that QE arguably didn’t work here and it’s not likely to work there either.

Switzerland Abandons Its Currency “Peg” to the Euro

Switzerland has traditionally been considered a “safe haven” country to park your money. Its banking system has long been considered one of the strongest and safest on the planet. And the Swiss franc has long been one of the most trusted currencies. But as of last Thursday, all of that has come into question.

Let me go back and explain how the latest developments occurred. When most of us think of Switzerland, we think of fine watches, cuckoo clocks, financial privacy and sound money policies. With the Swiss, you don’t get surprises… Until you do.

Last Thursday, the Swiss National Bank (SNB) shocked the financial world with a double whammy –simultaneously abandoning its policy of pegging the Swiss franc to the euro and cutting the interest rate it pays on bank reserves to minus, yes minus, -0.75%. You now have to pay the SNB 0.75% to park money there!

Major market turmoil ensued last Thursday with the surprise announcements, including the global equity markets which do not like surprises.

And we should all feel a shiver of fear, including Americans that don’t have any direct financial stake in the value of the franc. That’s because Switzerland’s monetary travails illustrate how hard it is to fight thedeflationary vortex now dragging down much of the world economy.

Let’s go back and review how Switzerland got into this position of having to make a very difficult decision that wills no-doubt hurt its economy.

When Greece entered its debt crisis at the end of 2009, and other European nations found themselves under severe stress, money seeking a safe haven began pouring into Switzerland. This in turn sent theSwiss franc soaring, with devastating effects on the competitiveness of the Swiss manufacturing and export sectors. This threatened to push Switzerland – which already had very low inflation and very low interest rates – into a Japanese-style deflation.

So Swiss monetary officials went all-out in an effort to weaken their currency. You might think that making your currency worth less is easy – can’t you just print more money? But in the post-2008 world, it’s not easy at all. Just printing money and stuffing it into the banks does nothing if it just sits there.

The Swiss tried a more direct approach, selling francs and buying euros on the foreign exchange market, in the process acquiring a huge hoard of euros. But even that wasn’t doing the trick.

Then, in 2011, the Swiss National Bank tried a psychological tactic. “The current massive overvaluation of the Swiss franc,” it declared, “poses an acute threat to the Swiss economy and carries the risk of a deflationary development.” And the central bank therefore announced that it would set a minimum value for the euro – 1.2 Swiss francs – and that to enforce this minimum it was “prepared to buy foreign currency [euros] in unlimited quantities.”

What the bank clearly hoped was that by drawing this line in the sand it would limit the number of euros it actually had to buy to enforce the currency peg. For three years it worked, more or less. But on Thursday of last week, the Swiss suddenly gave up and abandoned its currency peg to the euro. The Swiss central bank said it was because of the weakening euro, and the fact that euro purchases would only increase going forward.

How a Stronger Swiss Franc Hurts Its Economy

I don’t want to oversimplify here, but as a country’s currency rate increases, that makes its export prices more expensive to foreign buyers. Over half of Switzerland’s economy (55%) is made up of exports and tourism. If the value of the Swiss franc goes up, that is bad for its exporters and it makes it more expensive for foreigners to visit Switzerland. Not good.

Yet the Swiss National Bank decided to go there anyway last Thursday. Most observers were stunned. When the SNB decoupled from the euro last Thursday, the franc exploded almost 40% against the euro initially (in mere minutes) and settled apprx. 19% higher on the day.

So the question remains, why did the SNB take this action? Why did it do so, despite the negative/deflationary implications, after denying any chance of doing it as recently as a week ago?

The answer may be that the SNB saw the handwriting on the wall – that it would have to purchase far more euros when the European Central Bank embarks on Quantitative Easing in the months just ahead, which will very likely result in a considerably lower euro.

The bottom line is that the Swiss chose arguably the better of two bad options. It could have stuck with its policy of pegging the value of the franc to the falling euro, or it could have made the choice it did to decouple the franc from the euro. This also explains why the SNB cut its interest rate on reserves held at the bank to -0.75% to hopefully curb new money flowing into the franc.

If, as many expect, the euro weakens considerably just ahead – assuming a major QE effort is announced later this week – then the Swiss may have made the right decision, even though a stronger franc will likely be bad for their economy.

The bottom line in this: Decoupling the Swiss franc from the euro means that the franc will almost certainly move higher against the euro and perhaps the US dollar going forward. This will hurt the Swiss economy and means intensifying deflation in Europe and perhaps elsewhere.

The question is, will deflation make its way to the US? That remains to be seen.

The ECB to Announce QE Bond Buying This Week

It is widely expected that the European Central Bank (ECB) will announce its own large QE bond buying program this Thursday. Never mind that most outside of Washington DC agree that our own Fed’s massive $4 trillion bond buying program did little to rescue our economy. Yet Europe seems intent to go down the same dangerous path.

Word is that the ECB will announce this Thursday its intentions to embark on its own massive QE program,initially $500 billion to $1 trillion, and perhaps more later in printed money bond buying over the next year or longer.

European Central Bank President Mario Draghi has been promising for over a year that the ECB will undertake a huge QE bond buying program that will do “whatever it takes” to revive the European economy. Based on what we are told, such an announcement will come on Thursday following the ECB’s first policy meeting of the year in Frankfurt. That remains to be seen, of course.

With area-wide inflation turning negative in December – consumer prices fell by 0.2%across the euro currency region – the alarm bells have been ringing, and Draghi and other top ECB officials have been busy priming the markets for action.

Draghi said the central bank had few other options at its disposal to counter the risk of deflation, a dangerous downward spiral of falling prices. And ECB executive board member Benoit Coeure said in multiple interviews recently that the central bank’s governing council would debate the size of such a QE program this week.

So it now looks like Europe will go down the same road as our own Federal Reserve went, with very questionable results.

Finally, President Obama will deliver his 7th State of the Union address this evening. In it, he will call for higher taxes on high income earners and even large IRAs, more pork-barrel spending and a host of other liberal items he wants. The first link in SPECIAL ARTICLES tells you all you need to know about the speech and the president’s liberal agenda for these last two years.

Very best regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.