Greece’s renewed drama is more noise than signal

January 9, 2015

Reprising a familiar scene, vocal crowds have marched through the streets of Athens over the last few months, demanding relief from the dictates of international financiers. Protestors have recently become even more emboldened by the prospect of electing a prime minister sympathetic to their cause.

Predictably, scolds from Northern Europe have taken a hard line on easing the terms of Greece’s austerity program, leading to renewed concerns of a Greek exit from the eurozone. This has been among the factors contributing to high levels of uncertainty and market volatility in the early days of 2015.

Yet while the rhetoric on both sides is sharp, we think that cooler heads will once again prevail. (Even if one of those heads is a new, left-leaning Greek prime minister.) And the potential that Greece’s situation will lead to broader difficulty in the eurozone seems limited.

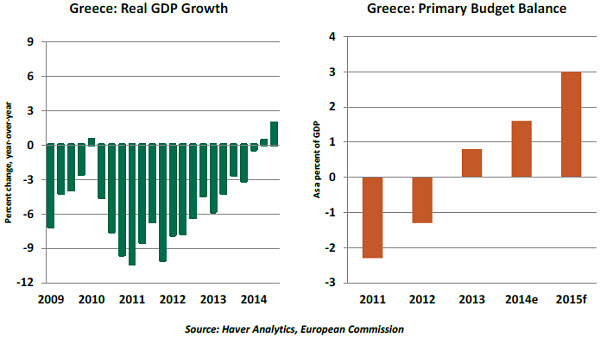

Greece has made important progress since its most-recent agreement with international authorities on a bailout plan in March 2012. Economic growth has been restored, and the national budget is showing a surplus before interest payments.

But austerity is never popular, and there is never a shortage of politicians willing to capitalize on popular discontent. Such is the case in Greece, where a divided parliament failed to elect a new president in December, triggering a snap general election on January 25.

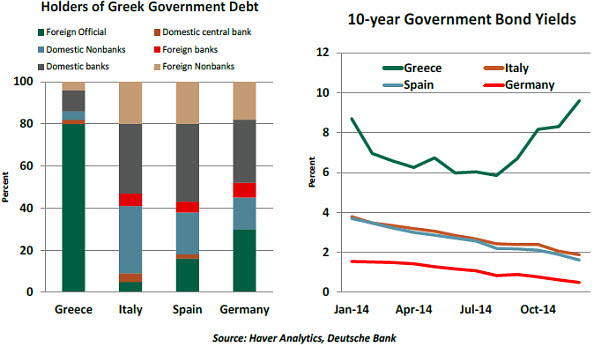

The vote is seen as a contest between current Prime Minister Antonis Samaras of the center-right New Democracy party and Alexis Tsipras of the left-wing Syriza. The prospect of a Syriza victory has rattled markets, as Tsipras called for a write-off of Greek sovereign debt. Greece completed a restructuring of government bonds held by the public in 2012; as a consequence, institutions in the European Union and the European Central Bank (ECB) hold almost 90% of the remaining bonds.

The rhetoric from Tsipras caused yields on Greek sovereign bonds to rise considerably, especially relative to other eurozone members. If they remain at these levels, the task of paying interest on the debt and paying off the debt will become much more difficult.  The risk of the Greeks electing a debt-repudiating government complicates the ECB’s task of launching a full-scale quantitative easing program. The next ECB policy meeting is on January 22, three days before the election. Some members of the governing council might hesitate to purchase additional Greek debt under such a program for fear of not being fully repaid.

The risk of the Greeks electing a debt-repudiating government complicates the ECB’s task of launching a full-scale quantitative easing program. The next ECB policy meeting is on January 22, three days before the election. Some members of the governing council might hesitate to purchase additional Greek debt under such a program for fear of not being fully repaid.

However, we think that Greece and its European sponsors will avoid a worst-case outcome. Consider:

- Like any good politician, Tsipras uses hyperbole as an electioneering strategy. In recent weeks, he retreated from his earlier declarations that a Syriza government would unilaterally stop debt service payments. Tsipras now emphasizes a renegotiation of the international bailout deal and is pledging not to unilaterally repudiate its terms.

- Syriza continues to call for Greece to remain in the eurozone. The party must certainly realize the steep consequences of exit. On the other side, recent press reports that German politicians are countenancing “Grexit” are a maneuvering tactic intended to send a strong signal to both Syriza and to Greek voters. In reality, the ever-pragmatic German Chancellor Angela Merkel would work for a negotiated solution to the Greek debt problem.

- Syriza’s lead in the polls has narrowed, and it now runs only 3 to 4 percentage points ahead of the nearest pursuer. The fragmented nature of Greek politics will also limit the winning party’s ability to implement its agenda unilaterally, as negotiations with coalition partners will be required.

A debt write-off will not happen: the precedent would inflame investors, not to mention voters in countries such as Germany. However, Tsipras recently mentioned the goal of reducing annual debt service costs from the current level of around 3% of gross domestic product to below 2%. A Syriza-dominated government would likely push for lower interest rates and extended maturities and perhaps a rollover of debt coming due this year. Other nations subject to similar programs from international authorities will watch the negotiations closely.

A debt write-off will not happen: the precedent would inflame investors, not to mention voters in countries such as Germany. However, Tsipras recently mentioned the goal of reducing annual debt service costs from the current level of around 3% of gross domestic product to below 2%. A Syriza-dominated government would likely push for lower interest rates and extended maturities and perhaps a rollover of debt coming due this year. Other nations subject to similar programs from international authorities will watch the negotiations closely.

The worst-case Greek election scenario is not a Syriza victory but a “hung” parliament with no one party able to command a majority of the 300 seats, triggering a second election – which is what happened in the summer of 2012. This would leave markets in an uncomfortable limbo.

Drama is a Greek invention, so it isn’t unusual to see a little theater in that country. We can only hope that the current play does not end in tragedy.

U.S. Employment Report: More Jobs, Less Pay

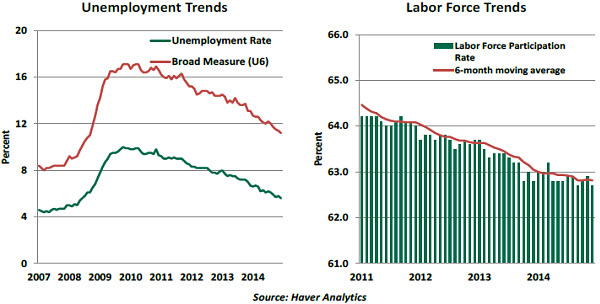

The U.S. unemployment rate declined to 5.6% in December, and payroll employment rose 252,000. These numbers place the 2014 labor market performance in special spot – we have the lowest unemployment rate since 2000 and the largest increase in payroll employment since 1999. But there remain opportunities for improvement that will need to be seized before the Fed commences tightening monetary policy.

The details of the household survey indicate that the drop in the jobless rate was a combination of an increase in employment and a reduction of the workforce. The latter is not a positive development, as a lower participation rate exaggerates the improvement in the unemployment picture. The jobless rate is now within reach of the Fed’s current estimate of the long-term unemployment rate (5.2% – 5.5%).

On the positive side, the broad measure of unemployment (U6), inclusive of those attached marginally to the labor force and those working part-time for economic reasons, fell two notches to 11.2%.

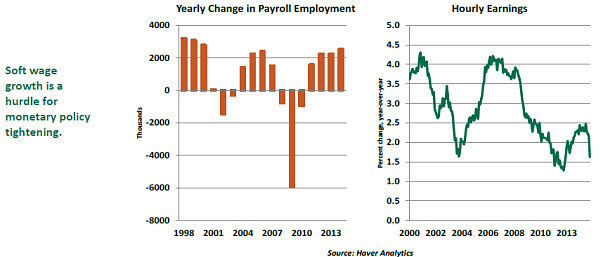

Payrolls data from the establishment survey were noticeably strong. On average, payroll employment rose 289,000 in the last three months of 2014 compared with 190,000 in the first three months of the year.

In the goods sector, construction employment posted a solid gain (+48,000), while factory employment advanced 17,000. Gains in business services (52,000), education and health (48,000), and trade and transport (23,000) led the 173,000 increase in private service-sector jobs. Hiring in the oil and gas extraction industry showed a small increase during December, implying that lower oil prices have yet to affect employment in this sector.

Average hourly earnings posted a surprising 0.2% drop in December. The declines in earnings were widespread, and the year-to-year gain of 1.7% slipped from the 2.0% pace seen in recent months. This development will concern members of the Federal Open Market Committee, who consider wage gains as an important factor that will help move inflation toward the Fed’s 2.0% target.

The recent hiring trend supports expectations of the Fed’s plan to tighten monetary policy, but the wage picture complicates assessment of labor market conditions. Both trends play neatly into the Fed’s pledge to be patient in considering when to apply the monetary policy brake.

© Northern Trust