I often hear from many of you that you know very little about investing. However, I find that most of you understand investing quite well. Many of the concepts and theories thrown out by those of us who claim to be professionals can be restated into words and phrases you use regularly. For instance, when you say, “what goes up must come down,” or, when you are going through a particularly tough time, “don’t worry, things will get better,” you are showing your knowledge of regression to the mean.

We have a deep conviction that things will return to normal with time. It is the driving force behind our security selection and portfolio management decisions. Because of that, I thought I would share some information on “regression to the mean” with you. Once again, I have sought a little help with this from my library, and am sharing with you an excerpt written by H. Bradlee Perry, CFA in 1987.

At that time, Mr. Perry was employed by David L. Babson & Co., Inc. Babson was known as an excellent investment counselor and manager specializing in equity investments. The company published The Babson Staff Letter, which at the time was one of mine and many other investors’ favorite source of investment insight. The company still publishes the staff letter and it is freely available through the company’s website, www.babsoncapital.com. Although their business has changed substantially since the earlier days of the company, they are still highly regarded in the investment community. Of local interest, the company announced in May of this year that they are considering moving their headquarters to Charlotte, our neighbor city a few miles up the road.

From The Babson Staff Letter, August 14, 1987, H. Bradlee Perry, CFA, Regressing to the Mean

Golfers and baseball players often talk about being “in the groove”, having their swing following the particular pattern which has been successful for them. Different businesses also have a “groove”, a mode of performance that is typical for them, and individual stocks tend to have a normal valuation “groove”.

However, athletes, businesses and stocks deviate from their typical performance from time to time, doing better or worse for a while. Such periods obviously are very significant to sports fans and investors.

Because of aging and other human frailties, golfers and ball players don’t always get back into the groove. However, due primarily to competitive forces, businesses and stocks usually do. Statisticians call this “regressing to the mean”. Understanding the process and observing it carefully can be very rewarding for investors.

Industry Patterns

Most types of businesses are influenced by specific factors that give them distinctive characteristics, and all the participants in those particular businesses tend to perform in somewhat similar fashion. When one doesn’t, history shows that eventually the “outlier” usually falls back in line with the industry pattern.

Banking is a good example. This is a very homogenous business. All banks deal primarily with money; it is a commodity because one bank’s money is just the same as another’s. Through various means they all gather deposits primarily from individuals and businesses and lend those funds to other individuals and businesses.

Some banks are better managed than others so they operate a little more effectively. But in the long run there are rarely major differences in performance in such a homogenous, competitive industry- especially within the geographic areas where economic conditions are similar.

Over the years when a particular bank has been growing faster than its competitors, it has usually been more aggressive in lending. Eventually that leads to greater loan losses and in turn, a reining in of its rapid growth. Occasionally when a bank goes bonkers on profit expansion, it gets into such deep trouble that it has great difficulty regaining its position. Continental Illinois is a recent example and previously First Pennsylvania experienced the same fate (for somewhat different reasons).

However, in most instances overly aggressive banks do regress to the mean. Notable cases are Citizens & Southern many years ago and Chase Manhattan in the late 1970s.

Conversely, banks which go through a period of slower than normal growth and are tagged as “sleepy” usually wake up and get back in the groove. Wells Fargo, First Interstate and State Street Boston are good illustrations.

The same process has occurred in just about every industry: Texaco declining from superiority in the 1970s while Exxon was moving up the scale; Union Carbide losing its position of preeminence in chemicals while Hercules rose from a subpar position to a very good one; Borden and Nabisco waking up in the food business while General Foods was sinking to mediocrity; Pfizer developing much greater strength as Upjohn slipped into the average category; Federated Department Stores sliding from its very strong position while May Department Stores was advancing from the rear of the pack; etc.

The record is clear that more often than not in a business heavily influenced by a few basic forces, companies rarely perform way above the industry average or way below it indefinitely. There is a constant tendency to regress toward the mean….

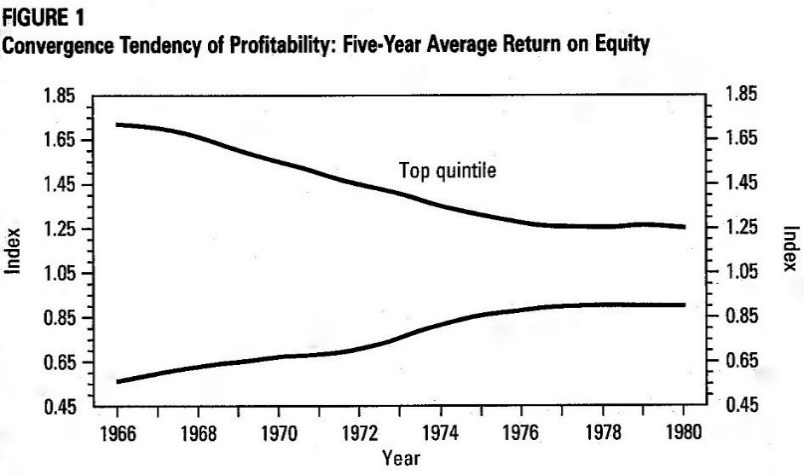

This is illustrated in Figure 1 prepared a few years ago by Merrill Lynch. Covering a broad universe of over 1,5000 corporations, it shows how those in the top quintile of profitability in 1966 gradually experienced a decline in their return on equity from way above average to moderately above average over the next 14 years – and how those at the bottom of the scale in 1966 improved to just slightly below average….

Stock Market Performance

One lesson we need to remember constantly is that stock prices tend to reflect quite fully the most recent performance of companies. When a business has been going extremely well, almost invariably that fact has already been factored into the stock – because everyone has seen the good reports from the company. Similarly, when the recent results of a company have been poor, the stock is usually depressed.

Then when the news on the “good” companies becomes even slightly less favorable – or perhaps merely fails to get more favorable – their shares are likely to underperform the market. On the other hand, even a slight improvement in the news on a “bad” company can park a major upswing in its stock….

Conclusion

Many years ago we knew a person outside this firm who had developed a very simple—and very effective—method of selecting stocks to buy. He kept careful records of the returns on assets earned by different companies. He would only buy a stock when the firm’s profitability was below its historic norm—and he would only sell the stock when profitability had risen above that norm. This gentleman was an extremely successful investor and his commonsense approach (which predates the general understanding of regression to the mean) works just as well today as it ever did.

The reason it does is that most investors take a relatively short-term view and assume that what has happened most recently will continue. They fail to recognize that economic and market forces are always working to press companies (and whole industries) back toward their respective grooves. Furthermore, there is a human element in the equation. As with athletes, it is difficult for management to play over their heads for long. Nor does any management want to continue performing badly. And if they do for very long, the directors (or an outside buyer) usually step in and replace management.

Appraising where a company is in relation to its normal pattern of performance and how its current status has affected its stock prices is a very useful process. Like any other investment technique it doesn’t work all the time because exceptions do occur, but clearly this type of analysis can improve one’s portfolio batting average.

While it is easy for us to understand the concept of regression to the mean, it can be difficult for us individually to use this powerful force when we are investing our own money. We often do not want to sell when everything seems perfect, nor do we consider buying when things look bleak. Even if we do buy low, we often do not have the patience to wait and allow the business to make the changes needed to correct and improve their operations. Yet I know that if we can overcome these instincts, we will, as Mr. Perry states, improve our batting average.

Until next time,

Kendall J. Anderson, CFA

Anderson Griggs & Company, Inc., doing business as Anderson Griggs Investments, is a registered investment adviser. Anderson Griggs only conducts business in states and locations where it is properly registered or meets state requirement for advisors. This commentary is for informational purposes only and is not an offer of investment advice. We will only render advice after we deliver our Form ADV Part 2 to a client in an authorized jurisdiction and receive a properly executed Investment Supervisory Services Agreement. Any reference to performance is historical in nature and no assumption about future performance should be made based on the past performance of any Anderson Griggs’ Investment Objectives, individual account, individual security or index. Upon request, Anderson Griggs Investments will provide to you a list of all trade recommendations made by us for the immediately preceding 12 months. The authors of publications are expressing general opinions and commentary. They are not attempting to provide legal, accounting, or specific advice to any individual concerning their personal situation. Anderson Griggs Investments’ office is located at 113 E. Main St., Suite 310, Rock Hill, SC 29730. The local phone number is 803-324-5044 and nationally can be reached via its toll-free number 800-254-0874.