1. November Unemployment Report Was a Surprise

2. November Jobs Report Was Not All Good News

3. America Still a Long Way From Full Employment

4. Conclusions on the November Jobs Report

5. Could Relief For Businesses be on the Way Next Year?

6. President Obama Considering Sanctions Against Israel?

November Unemployment Report Was a Surprise

Last Friday’s unemployment report for November was a stunner, at least on the surface. US businesses ramped-up hiring across the board in November, putting 2014 on pace to be the best year for job growth since 1999.

Non-farm employers added a seasonally-adjusted 321,000 jobs in November, the most in one month since January 2012, according to the Bureau of Labor Statistics (BLS). That number was substantially higher than the pre-report consensus of just 230,000.

Only 7,000 of the 321,000 new jobs came from government. Nearly all parts of the private sector contributed, including 28,000 new jobs in manufacturing. With total upward job revisions of 44,000 for September and October, the economy has added 2.65 million jobs in the last 12 months.

Also encouraging is that wages rose at a faster clip in November, with average hourly earnings rising nine cents to $24.66. Wage increases year-over-year were 2.1%, which remains historically low, but the November gains are a glimmer that rising job prospects are beginning to flow to workers via bigger paychecks.

Those paychecks and prospects lured another 119,000 Americans back into the workforce in November, which is the main reason the unemployment rate held at 5.8% despite the healthy jobs gains. The labor participation rate didn’t budge from a sickly 62.8%, but if job creation continues at this pace more people will likely return to work.

One hopeful sign: Those saying they were working part-time but wanted full-time employment fell by 177,000. About 6.9 million Americans are working part-time because they cannot find full-time positions. The broadest measure of unemployment, which includes these workers, dropped to 11.3%, down 0.1% from October. Those out of work for 27 weeks or more fell by 101,000. A rising tide lifts even the long-term unemployed.

The best news would be that this jobs trend signals renewed confidence by employers in the prospects for economic growth. The last two quarters were robust at 4.6% and 3.9%, respectively, in annual GDP and would represent the strongest growth since the mid-2000s, if the pace continues. The declines in oil prices, and thus gasoline, are giving consumers a boost in spending power that will further encourage business investment and hiring.

President Obama said on Friday that the United States has added more jobs over the last four years than Europe, Japan, and all other advanced countries combined (I have no idea if that is true). Other US officials noted that job growth in November was driven by better paying blue-collar and higher-skill sectors, a contrast to the low-wage boom earlier in the recovery.

November Jobs Report Was Not All Good News

As is the case with most government reports, last week’s turbocharged jobs headline came in-part thanks to “seasonal adjustments” and other wizardry at the Bureau of Labor Statistics, which reported that US job growth hit 321,000 in November.

Those numbers – from the “establishment survey” (employer payroll numbers) which counts the number of jobs – sound nice on the surface, and they certainly present reasons for confidence that the job market continues to mend. However, the “household survey,” which is a head-count of those actually working, shows a very different picture.

According to the household survey, that big headline number of 321,000 new jobs translated into only 4,000 more Americans working in November than in October. For example, a person working two or three jobs is only counted once in the household survey – versus two or three times in the establishment survey. Yet that difference in counting can’t account for the big discrepancy between the two surveys in November, and suggests some major revisions to one or both surveys in January.

In November, 119,000 new people entered the labor force, according to the BLS, but another 115,000 filed for first-time unemployment benefits – again, a net of only 4,000 more Americans working. As a result of this relatively small number of net new workers, the unemployment rate remained at 5.8%. And the labor force participation rate remained at 62.8%, which is just off the year’s worst level and around a 36-year low.

And there’s more: Full-time jobs declined by 150,000, while lower-paying part-time positions increased by 77,000 – that’s not good. There were 110,000 fewer married men at work, while married women saw their ranks shrink by 59,000.

As for the nine cent per hour wage increase, supervisors and managers got most of the pay raises and the benefit of extra hours worked in November. For production and non-supervisory workers who make up the vast majority of the work force, average hourly pay rose by only four cents, to $20.74, and the average workweek was unchanged, at 33.8 hours.

Even that overstates the day-to-day reality and prospects for many workers. Fully a quarter of the jobs created in November were in retail and in leisure and hospitality, fields that in general do not offer enough pay or hours to make a decent living.

Finally, let’s not forget that 9.1 million remain unemployed, which is 1.9 million more than there were in November 2007 before the financial crisis and the Great Recession began.

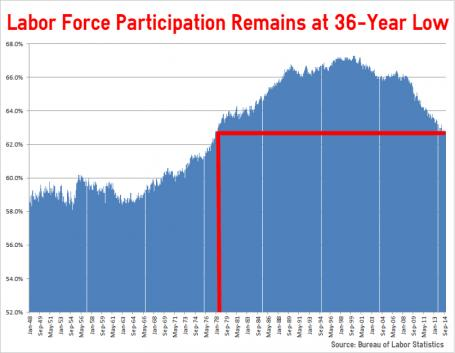

America Still a Long Way From Full Employment

Philadelphia Fed President Charles Plosser proclaimed on Wednesday of last week that “the economy is near full employment.” While that’s what you might expect a hawkish central banker who’s anxious to raise the Fed Funds rate to say, he is simply wrong. With the unemployment rate at 5.8%, the economy is still a good way from full employment.

No matter your economic perspective, there is no arguing that this recovery from the crisis of 2008 has been extremely lame, at best. Historically, full employment in the US rests somewhere below a 5% unemployment rate and coincides with an increase in the labor-force participation rate, along with a healthy, meaningful increase in wages.

As illustrated at left, the labor force participation rate is trending down and remains near a 36-year low. The last time the economy was at full employment was in 2000 when unemployment averaged 4% for the year.

While President Obama touts this economic “recovery,” there are still over 3 million Americans mired in the long-term unemployed camp. And many of those who were hired are in temporary or part-time slots, or full-time positions that pay less than their previous salaries.

These are the people who have either taken part-time work because they can’t find a full-time job, have been jobless for 27 weeks or more, or are considered “marginally attached to the labor force,” meaning they have looked for work in the past 12 months, but not in the most recent four weeks.

This does not include the 770,000 “discouraged workers.” These are the folks who have stopped looking altogether because they believe that no jobs are available for them – a true American tragedy.

Conclusions on the November Jobs Report

Clearly the November employment report was a positive surprise. The 321,000 new jobs added last month was the highest reading since January 2012 and was substantially above the pre-report consensus of 230,000.

The fact that 119,000 more workers re-entered the workforce in November, in excess of those leaving it, was another positive surprise. The rise in average hourly earnings by nine cents to $24.66 was also better than expected.

The question is, will such job growth continue? Or was this a one-month, seasonal anomaly?

Keep in mind that not all of the news in the November jobs report was positive. While the headline new jobs number was 321,000, a deeper dive into the data reveals that there were only 4,000 more Americans working at the end of November. Full-time jobs declined by 150,000, while part-time positions increased by 77,000 – that’s not good.

And finally, despite comments from Philly Fed President Charles Plosser last week, the US economy is not close to full employment. We’ll have to monitor the jobs data over the next few months to see if the November breakout was for real. Let’s hope it is!

Could Relief For Businesses be on the Way Next Year?

With the mid-term elections delivering the Senate to the Republicans, many feel there may be some tax relief on the way next year. For years the economy has had to face a policy bias toward imposing ever-higher costs on private business. You know the litany: the 2007 energy bill, Obamacare, Dodd-Frank, burdens on fossil fuels, higher taxes, and so much more.

The GOP House that was elected in 2010 delayed a tax increase but President Obama’s re-election imposed it in 2013. His Administration’s rule-by-regulation continues, but at least Congress will do no more harm with the GOP in charge.

The key point is that for the first time in years, Washington may even have a “growth bias.” Hopefully Congress will attempt to reform the business tax code, ease or repeal regulations, reduce the burdens of Obamacare, and otherwise remove barriers to job creation. It’s impossible to know how much will pass while Mr. Obama is still president, but some pro-growth measures will hopefully make it through.

The psychological effect of this change shouldn’t be underrated. American businesses have been hunkered down for years, even with a rising stock market and near-zero interest rates, because CEOs haven’t known what damage Washington might do next. Now the main question is what good might happen now that the Republicans are in charge of both houses of Congress.

With Congress mostly checking Mr. Obama, the biggest remaining policy uncertainty is when and how quickly the Federal Reserve will continue its march back to monetary policy normalcy. The Fed ended its massive QE bond-buying program in October, and the economy survived. Now the question is, what will happen when the Fed begins to hike the Fed Funds rate next year?

President Obama Considering Sanctions Against Israel?

Rumors are swirling in Washington that President Obama is seriously considering new sanctions against Israel. Sanctions against Israel, our strongest ally in the Middle East? You’ve got to be kidding, right? Maybe not.

Dozens of House Republicans on Friday demanded that President Barack Obama explain and clarify the latest reports that say his administration is considering new sanctions against Israel.

The Obama administration has repeatedly said it disapproves of Israel’s decision to build new homes in East Jerusalem, and that this construction “undermines the peace process.” But officials on Friday refused to confirm or deny reports that they are considering sanctions against Israel.

A letter sent Friday to Obama by Rep. Mark Meadows (R-NC) and 44 other House Republicans demanded more clarity than what’s been offered so far. Reportedly, the letter included the following:

“Recent reports suggest that your administration has held classified meetings over the past several weeks to discuss the possibility of imposing sanctions against Israel for its decision to construct homes in East Jerusalem. We urge you and your administration to clarify these reports immediately.

Israel is one of our strongest allies, and the mere notion that the administration would unilaterally impose sanctions against Israel is not only unwise, but is extremely worrisome. Such reports send a clear message to our friends and enemies alike that such alliances with the United States government can no longer be unquestionably trusted.”

The letter also said Congress has not given the White House any authority to sanction Israel, and in fact just passed legislation last week – by a unanimous vote – to boost US-Israel security ties.

“While it is our hope that these reports are untrue, the fact that your administration has failed to denounce or clarify them is deeply troubling. We urge you to quickly and sharply address these concerns, as well as take the steps necessary to demonstrate America’s unwavering support for Israel.”

White House Press Secretary Josh Earnest admitted on Friday that he is aware of news reports that the United States is considering sanctions against Israel, but wouldn’t say if they are true. Fox News reporter Ed Henry asked Earnest about the reports and said, “I wondered if you could say true or false.” Ernest responded:

“I’ve been informed of some of these reports. What I can tell you is that I’m not going to talk about any internal deliberations inside the administration and certainly not inside the White House.”

The point is, he did not deny it.

The Israel sanctions discussions are said to have begun after Prime Minister Benjamin Netanyahu visited the White House in October and clashed with President Obama over the construction of a new housing development in East Jerusalem.

The administration warned Israel that the project would raise questions about Israel’s commitment to peace with the Palestinians. Netanyahu reportedly replied that Israel does not accept restrictions on where Jews can live, and that Arabs and Jews in the Israeli capital should be allowed to purchase homes wherever they choose.

The decision to even consider sanctions against Israel is, in my view, a part of Obama’s “Temper-Tantrum” (as I called it last week), since the shellacking he and the Democrats suffered in the mid-term elections on November 4.

I’ve said it before and will say it again: This man will stop at nothing to advance his ultra-liberal agenda, no matter if doing so would be damaging for America. If anyone doubted me, this latest threat of sanctions against Israel should convince you.

While I have no doubt that Obama would love to levy sanctions on Israel, my bet is that he will back off due to heavy objections – and it won’t surprise me if his press secretary denies that it was ever a serious consideration. We’ll see.

Warmest holiday regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.