Last week Bill Gross and the former co-CIO of PIMCO, Mohamed El-Erian, were advising clients to lighten up on stocks. You may agree that these are certainly two people with a passion for what they do. To that end, we all benefit.

I personally believe there is more run left in the equity market, yet risk is high and I certainly don’t want to be left sitting on the tracks in front of an oncoming train. Stay nimble and alert. And remember while risk can be measured (high today due to high valuations), it is more difficult to time.

Consider this as a portfolio:

30% Equity exposure:

Since valuations are in Quintile 5 (low forward expected return), weight just 30% of your portfolio to equities. Keep it hedged with a put option strategy. When valuations move lower (which will happen in a bear market), take that weighting back up to 70% and hold unhedged (risk is far less when valuations are low – i.e. Quintile 1 * See discussion and graphs below).

30% Fixed Income exposure:

Rates are so low that the historical benefit to a balanced portfolio is significantly reduced. Allocate to flexible bond strategies and have a relative strength based process in place to know when to shorten and lengthen your bond maturity exposure. Tactical relative strength can help to keep you in line with the fixed income assets showing the strongest price leadership. Tactically trade high yield. Risk of a coming HY default wave is growing.

40% Tactical – Alternative – Other:

Tactical investing strategies can help enhance returns and increase overall stability within investors’ portfolios. They are different from managed futures, global macro and long/short equities. Over the years such strategies have done a good job at providing return and reducing downside risk. No guarantees in anything. Thus the principle of diversification.

One note on diversification. If your client calls up concerned that their well diversified portfolio didn’t do as well as the S&P 500 Index, remind them that there are no bonds held in that index and that there are two types of investment approaches. One is to speculate (target just a few aggressive risks). The other is to broadly diversify many diverse sets of risks.

I would love to have been all-in on Amgen (+47.33%) and Apple (+44.65%) this year (see below) but I would have also thought that small caps would have done much better. They have gained just 1.74% vs 12.56% in the S&P 500. Finally, look at the year-to-date performance of Amazon down 20.63% through December 3, 2014. Glad I didn’t own that.

The reason for diversification in one chart:

I could have included gold, oil, and other commodities. Commodities look to have entered a secular bear market period but that is a topic for another day.

I post several of my long-time favorite market “weight of evidence” indicators each week in Trade Signals. Currently, the evidence supports my view for a strong equity market into mid-2015. No guarantees, of course – I’ll continue to post those indicators each week. Right now they say “the party lives on.”

In the 1973 edition of The Intelligent Investor, Benjamin Graham commented:

“It always seemed, and still seems, ridiculously simple to say that if one can acquire a diversified group of common stocks at a price less than the applicable net current assets alone — after deducting all prior claims, and counting as zero the fixed and other assets— the results should be quite satisfactory.”

According to Graham, investors will benefit greatly if they invest in companies where the stock prices are no more than 67% of their NCAV per share. A study done by the State University of New York to prove the effectiveness of this strategy showed that from the period of 1970 to 1983 (overall, a particular challenging period for stocks) an investor could have earned an average return of 29.4%, by purchasing stocks that fulfilled Graham’s requirement and holding them for one year.

However, Graham did make it clear that not all stocks chosen in this manner will have excessive returns and that investors should also diversify their holdings when using this strategy.

Net-Net Working Capital (NNWC) = Cash and short-term investments + (0.75 * accounts receivable) + (0.5 * inventory) – total liabilities

You won’t find many discounted shares today as QE has inflated most risk assets but as boom follows bust and bust follows boom, the market will fall again. Have some dry powder indeed.

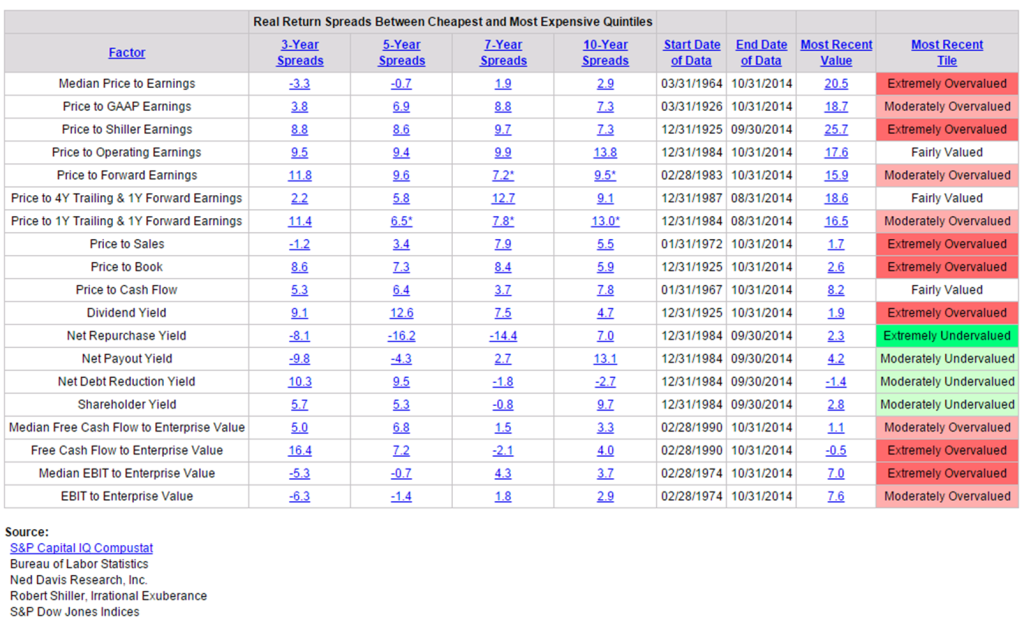

As a quick aside, there are subscription based websites that can help you screen for stocks that meet Graham’s approach to value investing, though, as you can see in the above series of valuation charts, now is a time to be underweight stock market exposure. Just Google ‘Benjamin Graham Net Working Capital.’

Also, if you’d like to learn more about tactical relative strength, I presented, along with Tom Dorsey, on a webinar hosted by Joe Cunningham of Horizon ETFs and MC’d by Tom Lydon of ETF Trends. Here is a link to the Webinar. You may have to sign in and provide your email information.

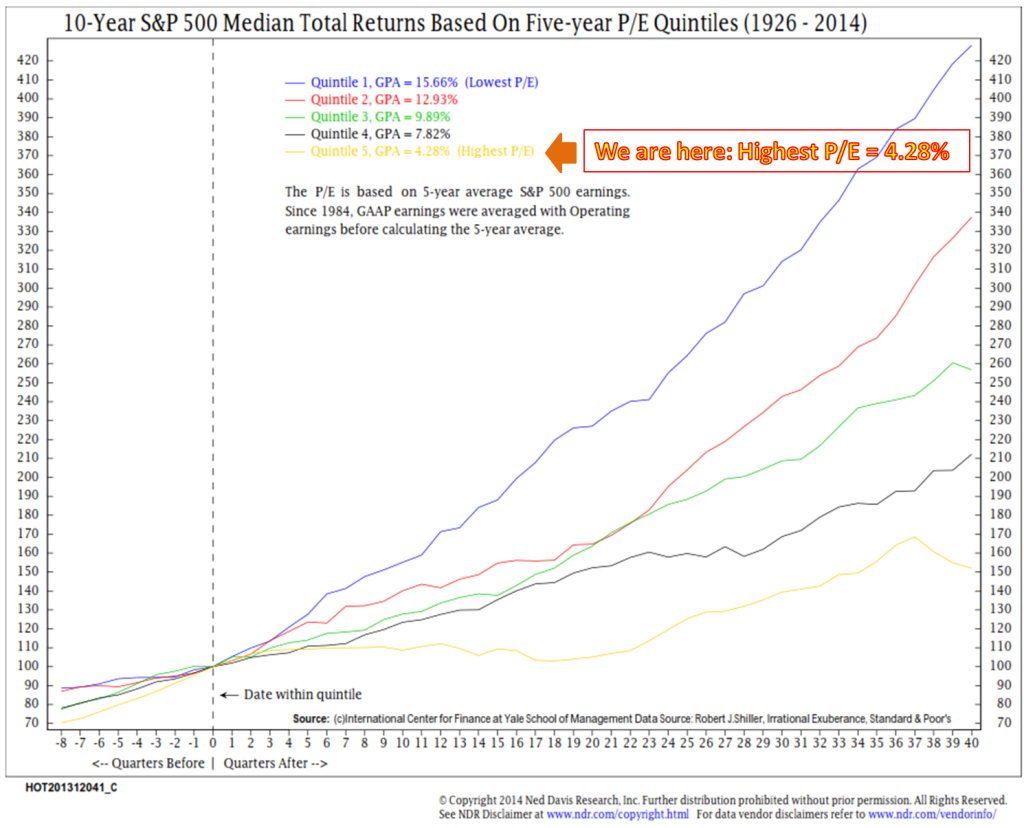

*Quintile 5 – Predicting Forward Return Over the Next Ten Years: Just 4.28%

The following chart looks at historical data and ranks PE into five quintiles. Quintile 1 (blue line) shows an annual gain of 15.66% in the S&P 500 index over the 10 years following periods when PEs where low. Quintile 5 (yellow line) shows an annual gain of just 4.28% following periods when PEs were high.

Think of it this way. The study looked at what happened ten years after PE was at a certain point. NDR grouped PEs into 5 quintiles ranging from low to high. They then took the median total returns of the ten years that followed. It is based on what actually happened. Not surprisingly, when PE valuations were low, the subsequent 10-year returns were the highest.

The market is richly priced by other measures as well; however, I still expect a positive surge in 2015 through Q2.

Source: NDR Data through December 1, 2014

Steve Blumenthal is CEO of CMG Capital Management Group and a regular contributor to CMG AdvisorCentral.

© CMG Capital Management Group

© CMG Capital Management Group