Oil isn’t the only commodity enduring a significant correction

December 5, 2014

Television networks have started airing their libraries of holiday movies. There are timeless classics like "It’s A Wonderful Life" and "Miracle on 34th Street," and more recent, campier entries like “Home Alone” and "Scrooged." It’s interesting to see how cinematic visions of the season have evolved.

Among the films running this month is "Trading Places," the Eddie Murphy/Dan Aykroyd production of 30 years ago. At the center of the film is a commodities trading firm run by the Duke Brothers (Don Ameche and Ralph Bellamy), who are trying to make a big score in the futures market. In the end, their plot unravels, leaving unexpected winners and losers.

Commodities really are in the limelight as the 2014 holiday season enters full swing. Markets for some elements are in full retreat, creating a string of unexpected winners and losers. Central banks trying to manage inflation in this scene will be forced to account for these earthy developments.

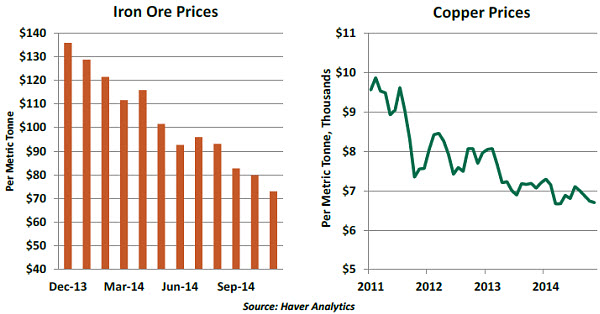

Those who have been shorting futures contracts for certain commodities have been pleased in recent years as industrial metals endured significant corrections.

Recent trends certainly reflect reduced demand from China, which surpassed the United States as the world’s largest manufacturer in 2010. Overall industrial output in China is growing at half the rate it was four years ago. Chinese steel production, which represents more than half of the world’s output, seems poised to decline for the first time in 14 years. China mines a significant fraction of the minerals it needs, but the sheer scale of its operations requires significant imports as well.

Chinese leaders have been trying to bring better balance to their economy, with heavy industry a focus of reform. Aside from achieving better diversification across sectors, the current regime has focused on reducing the environmental consequences of mines and factories. As a result, the country has been on something of a diet when it comes to raw materials.

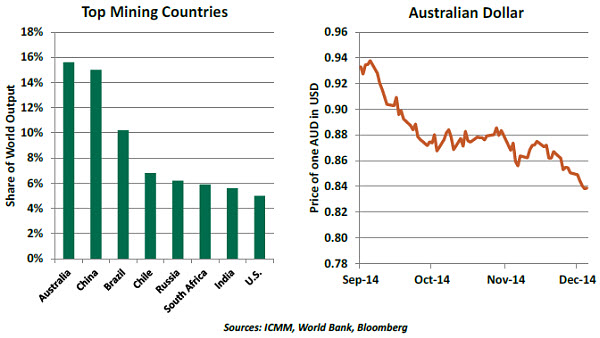

This is bad news for suppliers. Among advanced economies, Australia is bearing the biggest cost. Australia exports 43% of the world’s iron ore and 11% of its copper ore. Investment in the mining sector has contributed significantly to growth in recent years. With that sector now in retreat, the Australian economy grew by just 0.3% in the third quarter of the year.

This is bad news for suppliers. Among advanced economies, Australia is bearing the biggest cost. Australia exports 43% of the world’s iron ore and 11% of its copper ore. Investment in the mining sector has contributed significantly to growth in recent years. With that sector now in retreat, the Australian economy grew by just 0.3% in the third quarter of the year.

Australia has not endured a recession since 1991, and analysts are not calling for one any time soon. Australia has a significant service sector; at 70% of gross domestic product (GDP), it is as large as that of the United States. Nonetheless, the Australian dollar has fallen by more than 10% in the past three months.

Emerging economies that rely on commodities may not fare as well. These countries embrace mining as a means to attract foreign investment and generate exports. The industry provides employment to citizens with more-modest levels of education and generates revenue for governments.

When prices reverse, it can create tremendous problems if development has not been properly managed. The failure to keep reserves against changes of fortune can leave significant holes in public budgets and risks unemployment and unrest. Should recent trends continue, small producers in Africa and South America will be most acutely affected.

On a larger scale, both Brazil and Russia have significant mining sectors. Both face challenging economic times; real GDP has fallen over the last 12 months in both countries. Both rely on foreign investment, which has diminished importantly.

The drop in commodities prices will have an impact on the overall price level in the developed world. This will make it more challenging for central banks to achieve targeted levels of inflation. It also raises the difficult question of how to view adjustments in commodities prices when assessing price stability. Given their historic volatility, such shifts are often viewed as transitory, and “core” measures of inflation are constructed to minimize their impacts.

Yet recent trends in certain commodities prices have been ongoing and may persist for a while longer. Reflecting the diminished outlook for global inflation, precious metals have joined their industrial cousins in decline. The price of gold has fallen by more than 10% since July, and the price of silver is off almost 25% during that interval.

Yet recent trends in certain commodities prices have been ongoing and may persist for a while longer. Reflecting the diminished outlook for global inflation, precious metals have joined their industrial cousins in decline. The price of gold has fallen by more than 10% since July, and the price of silver is off almost 25% during that interval.

Such substantial corrections have roiled the commodities futures markets caricatured in “Trading Places.” Alas, the sea of smocks once seen in the pits has thinned over the years with the onset of electronic trading. A faithful remake of the movie would have computers plotting against one another; I am not sure that would play well at the box office.

Mario Draghi Sets the Stage for More QE

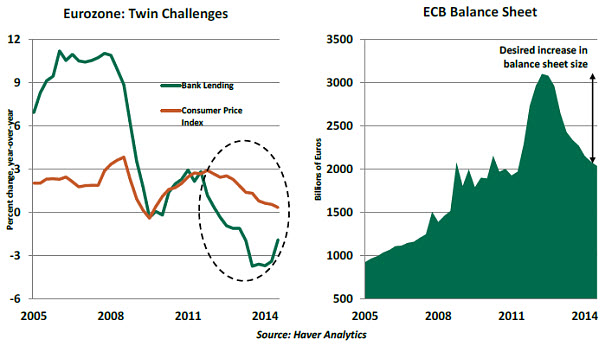

Mario Draghi, president of the European Central Bank (ECB), sent a strong signal that additional monetary accommodation may be necessary in early 2015 in light of weak economic data and low inflation. The underlying implication is that broad-based quantitative easing (QE) would be effective in lifting inflation toward the central bank’s inflation target of 2.0%. However, this outcome is not assured.

The ECB’s updated forecast places eurozone inflation in 2014 at 0.5%, followed by 0.7% and 1.3% in 2015 and 2016, respectively. Eurozone real GDP is currently estimated to grow by 0.8%, 1.0%, and 1.5% during 2014-16, respectively. Updated forecasts of both inflation and GDP in the eurozone are materially lower than the ECB’s September prediction and this raises expectations of QE in 2015.

There are several roadblocks to overcome for these expectations to become reality and for QE to be effective.

First, the initial round of the ECB’s longer-term refinance operations (which offered low-cost funding to banks) expires in 2015 and will reduce the ECB’s balance sheet. To replace the runoff, the new targeted longer-term refinance operations (TLTRO) must be sizeable. The first offering of TLTRO was not well-received; the second one is scheduled for December 11.

In light of this, reaching the ECB’s goal of increasing its balance sheet by €1 trillion will require large-scale purchases of assets. Recent additions of covered bonds and asset-backed securities total just over €21 billion to date, a very modest sum. Clearly, new asset classes will be needed to generate additional volume.

Mr. Draghi mentioned that his governing council considered a range of alternatives for future QE. Previous statements have noted consideration of corporate and sovereign bonds, and Draghi hinted strongly that one or both of them might be approved for purchase early next year. Without them, the ECB will struggle to meet its balance sheet target.

There is ample dissent within the Governing Council of the ECB, particularly from Germany, about purchases of sovereign bonds. However, Draghi noted that he is determined to honor the price stability mandate even at the expense of losing support of some members of the Governing Council.

Assuming that these procedural hurdles can be overcome and QE expands in Europe, attention will turn to its effectiveness.

Credit easing is one of the channels through which QE operates; purchases of long-term securities lower long-term interest rates. Credit extension in the eurozone is largely done through the banking system, particularly for small- and medium-sized enterprises. Unfortunately, lending to the private sector in the eurozone has declined for 10 quarters in a row. European banks have been conservative with their capital, and firms have been reluctant to borrow amid a soft economic outlook. It will be a challenging task to revive credit in an environment where regulators are strict about strengthening weak bank balance sheets.

Credit easing is one of the channels through which QE operates; purchases of long-term securities lower long-term interest rates. Credit extension in the eurozone is largely done through the banking system, particularly for small- and medium-sized enterprises. Unfortunately, lending to the private sector in the eurozone has declined for 10 quarters in a row. European banks have been conservative with their capital, and firms have been reluctant to borrow amid a soft economic outlook. It will be a challenging task to revive credit in an environment where regulators are strict about strengthening weak bank balance sheets.

QE can be beneficial through another channel. Central bank purchases of securities make available cash that can then be invested in risky assets. This, in turn, increases prices of risky assets and raises wealth. The wealth effect from QE in the United States has helped lift consumer spending. Unfortunately, the percentage of eurozone households with risky assets in their portfolios is smaller than in the United States, which implies that the impact through the wealth effect will most likely be modest.

Despite these potential impediments, the ECB must press forward. European inflation and inflation expectations are both in decline. This implies higher real interest rates and an unintended tightening of monetary policy. It may not be clear that QE will work, but the consequences of doing nothing seem quite clear.

U.S. Employment Gains: Solid But Not Sufficient to Prompt Tightening

The November U.S. employment report was another strong one. But while we continue to make progress in the labor market, the inflation outlook has become the more-important driver of Federal Reserve policy.

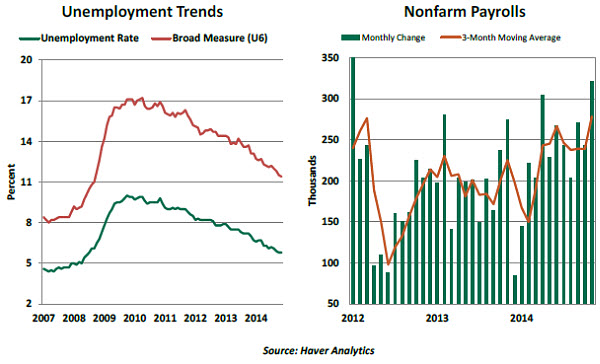

The American unemployment rate was unchanged at 5.8% in November, but this is a notable improvement from a year ago when the jobless rate was 7.0%. The broad measure of unemployment (which includes discouraged workers, part-time employees and marginally attached workers) stands at 11.4%, down from 12.1% in May. Long-term unemployment (30.7% versus 34.6% in May) shows a steady downward trend.

There has also been a noticeable reduction in part-time employment (6.8 million versus 7.5 million in May). These improvements have occurred during a period when the participation rate has held steady. Putting these numbers together, several of the indicators on Janet Yellen’s dashboard are turning green and signify labor market conditions are improving.

The establishment survey results were stronger than the household survey data. Payroll employment increased 321,000 in November, and revisions added 44,000 new jobs. The three-month moving average has held above 200,000 for eight straight months.

The strength of the report is not likely to result in the Fed considering an early date for tightening monetary policy. Although the economy is approaching full employment, inflation remains well below the targeted level of 2.0%. The personal consumption expenditure price index is up only 1.4% over the past year, and “core” inflation is up only 1.6%.

The strength of the report is not likely to result in the Fed considering an early date for tightening monetary policy. Although the economy is approaching full employment, inflation remains well below the targeted level of 2.0%. The personal consumption expenditure price index is up only 1.4% over the past year, and “core” inflation is up only 1.6%.

The recent views of two members of the Federal Open Market Committee are worth noting. Federal Reserve Vice Chairman Stanley Fischer indicated that the inflation part of the Fed’s dual mandate also needs to be met in order to consider tightening monetary policy. New York Fed President William Dudley pointed out that the experience of the Great Depression and Japan in the last two decades “illustrates the risks of raising interest rates too soon, especially when inflation is running below the central bank’s objective.” He added that allowing hiring to proceed at a solid pace for a while when long-term unemployment is elevated will not “jeopardize” the price stability objective.

The bottom line is that as long as inflation is below the Fed’s target and is not showing signs of moving closer to it, the Fed is unlikely to bring forward normalization of interest rates.

© Northern Trust