IN THIS ISSUE:

1. Median Household Income Down Since 1999

2. Composition of US Households is Changing Rapidly

3. “No Earner” Households to Increase Significantly

4. Census Bureau: Marriage Rate at 93-Year Low

5. “Marriage Is Pro-Growth” by Larry Kudlow

Median Household Income Down Since 1999

One of the most puzzling questions in economics today is why did median household income peak in 1999 and has yet to recover? Most analysts cite the fact that we had two serious recessions in the space of a decade, including the financial crisis of 2008-2009.

While the Great Recession ended in June 2009, real median household income (adjusted for inflation) remains well below the peak of around $57,000 in 1999 and has been below $52,000 in each of the last three years. The question is, why?

The standard answers, especially among progressives, are: 1) the sluggish economic recovery; 2) growing income inequality; 3) the failure to raise the minimum wage; 4) globalization and outsourcing; 5) corporate greed; and other variations of economic pessimism.

However, there are some other very obvious, but mostly overlooked, factors that can help explain why median household income has declined over the last 15 years that have nothing to do with economic stagnation. The fact is that there have been significant demographic changes in the composition of US households.

Economists Mark Perry and Alex Pollock, who also are contributors at the American Enterprise Institute, offered a very interesting analysis on median household income last week, and I will summarize their latest work for you today.

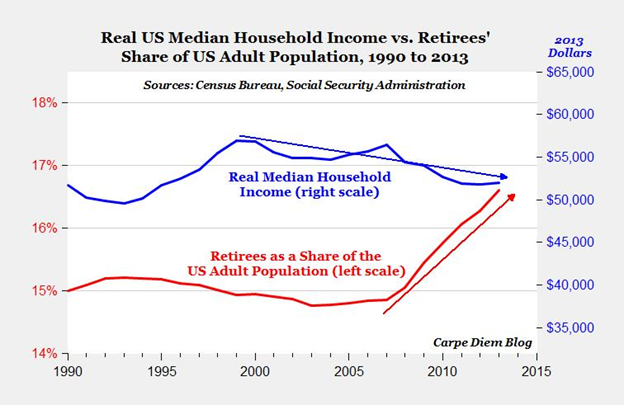

As you can see in the chart below, real median household income has declined since 1999 and has been fairly flat over the last three years. As we all know, the US population is aging and retirees as a share of the US adult population have risen from less than 15% (left scale) in 2007 to over 16.5% today. That number will continue to increase as more Baby Boomers retire.

Since retirees, generally speaking, have less income than their working brethren, that fact alone could drive median household income lower. But that’s only one part of the problem.

Pollock frames the issue of falling household income as follows:

“One of the most commonly cited numbers in discussions of inequality is the trend in median household income… Using median household income poses a fundamental problem, however. It conflates two measurements — changes in the composition of households and changes in income — and thus can easily mislead us.

Has the composition of households in America been changing? Obviously, it has. The percent of married couple households has fallen from more than 60 percent in 1980 to less than 50 percent in 2010. One-person households have risen from 23 percent to 27 percent of households in this period. Shifting from two-earner households to one-earner households lowers the median household income, even if everybody’s income is the same as before [or rising].” [Emphasis mine.]

Composition of US Households is Changing Rapidly

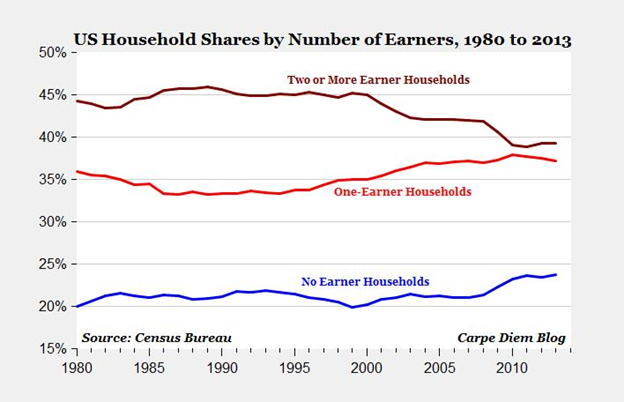

Mark Perry adds that a major dynamic change in household composition is the significant increase in the share of US households with no earners, from fewer than 20% of all US households in 1980 to 23.7% of households in 2013, as shown below.

Likewise, the share of single-earner households has also increased from 33.2% in the early 1990s to above 37% for the last five years. In contrast, there’s been a decrease in the share of US households with 2 or more earners (typically married couples) from above 46% of all households in 1989 to fewer than 40% of US households in every year since 2010.

Pollock provides a series of hypothetical examples showing how simple household demographic changes can result in rising individual incomes, while at the same time the median household income is falling.

For example, if there is a shift from two-earner households to one-earner single households as a result of divorce, the overall median household income could fall even when income is increasing for all individuals in the new mix of households with a greater share of single households.

The most frequent mistake is to look at median household income over time assuming that household demographics are static. That is precisely the mistake made in most of the discussions about median household income, which leads to a distorted and inaccurate conclusion about why median income is falling.

Perry summarizes that over the last several decades, there’s been an increasing share of no-earner, single-parent and single-earner households and a decreasing share of two-or-more-earner households.That major demographic shift has likely depressed median household income significantly in the last 15 years, even though it’s possible, as Pollock shows, that the income of individual working Americans could be rising.

“No Earner” Households to Increase Significantly

The largest demographic shift is the increasing number of retired Americans as a share of the adult population based on Social Security data. As the red line in the top chart above shows, US retirees represented a pretty stable 15% share of the US population from 1990 to 2008.

Yet starting around 2008 when the first Baby-Boomers reached the early retirement age of 62, the share of retirees started increasing from less than 15% of the adult population in 2007 to more than 16.6% in 2013. That number will continue to grow for the next 20 years.

Perry concludes that most explanations of the recent decline in US median household income are based on some variation of a narrative of economic stagnation, rising inequality and pessimism. But what is almost always overlooked are the very significant demographic changes that have taken place in the composition of US households over time that would significantly impact the income of the median US household.

“Taken together, a) the increase in the share of no-earner, single-earner, and single-parent households, b) the increase in the number and share of retirees, along with c) the decline in the share of two-earner and married households, would logically and necessarily depress the income level of the median US household.

In summary, the composition of US households is not static, fixed and permanent; rather it’s dynamic, evolving and ever-changing. Discussions on changes in median household income over time that ignore the changes in household composition over time will always be incomplete, distorted and misleading.

Perhaps the decline in median household income this century is not a narrative of economic pessimism and stagnation after all, but a more upbeat story of a greater number of Americans living longer lives, and enjoying periods of time in retirement that were never possible until this century.”

I would say it’s a combination of both.

Census Bureau: US Marriage Rate at 93-Year Low

In the previous section, we saw that the number of two or more earner households (typically married couples) has declined significantly over the last 15 years, and continues to do so. A big part of that shrinkage is the fact that our marriage rate has gone down sharply over the years.

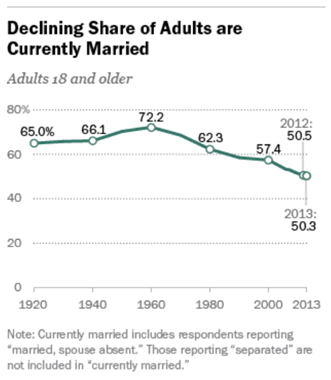

The Census Bureau reported in September that the nation’s marriage rate is the lowest since 1920(when records were first kept), and the first-time inclusion of same-sex married couples did little to reverse the decline.

According to the Pew Research Center analysis, the marriage rate of Americans 18 and older hit a new low of 50.3% in 2013, down from 50.5% in 2012. In 1920, 65% were married, and the marriage rate hit a high of 72.2% in 1960. The economic shock of the Great Recession put marriage on the back burner for many young adults, according to a 2014 study from the Urban Institute.

The overall decline in marriage among adults in part reflects the rising age when people first get married. Although the median age at which Americans first marry was once in the low 20s, it’s now in the late 20s for both men and women. But other factors may also be in play.

The overall decline in marriage among adults in part reflects the rising age when people first get married. Although the median age at which Americans first marry was once in the low 20s, it’s now in the late 20s for both men and women. But other factors may also be in play.

A recent widely-cited analysis by the Martin Prosperity Institute concluded that single people 16 and older make up more than half of the US adult population.

Since 1970, the marriage rate for never-married women declined by nearly 60%, according to the National Center for Family and Marriage Research at Bowling Green State University found.

The descent is even more pronounced for Millennials. In 1960, 68% of all 20-somethings were married. In 2008, just 26% were hitched, according to the Pew Research Center. How many of today’s young people will eventually marry is an open question. For now, the survey finds that the young are much more inclined than their elders to view cohabitation without marriage in a positive light.

Also, Pew found that 36% of young adults ages 18 to 31 (Millennials) were living in their parents’ home in 2012 (latest data available). A record 21.6 million Millennials lived in their parents’ home in 2012, up from 18.5 million in 2007. Young people living with their parents are not likely to get married.

As long as we’re on the subject of marriage, here’s good article written by Larry Kudlow of CNBC on November 15.

QUOTE:

Marriage Is Pro-Growth

by Larry Kudlow

The greatest economic challenge of our time is how to restore economic growth. Over the past dozen years, average real growth has slowed to 1.8 percent annually, under both Republican and Democratic presidents and congresses. It's a bipartisan problem.

And it's a new one. For the past 50 years or so, the American economy grew at just less than 3.5 percent per year. But we're now experiencing one of the longest slow-growth periods in the past 100 years. Excluding the Great Depression, I bet it is the longest slow-growth period in a century.

There are any number of fiscal and monetary prescriptions for restoring economic growth. As a Reagan supply sider, I would recommend lower marginal tax rates, lighter regulations, limited government and a sound dollar.

But I want to add this to the list: marriage. I have come to believe that marriage is a key element of a stronger economy.

At a dinner sponsored by the Calvin Coolidge Memorial Foundation a couple of weeks ago I gave a talk on the economic importance of marriage. Columnist Cal Thomas was nice enough to write about my talk. And many others have written about this topic. But before I jump into the statistics -- which are overwhelmingly in favor of marriage as a means of improving incomes, wealth and economic growth -- let me try a thought experiment.

I worry that we are creating a permanent underclass of poverty. Broken homes and children that have only one parent are at the root of this poverty trap. And when I think of young people from broken families, barely existing economically, this is what I find myself telling them:

Please go to school. Do what it takes to finish high school, be it a trade school or a tech-related school, and then maybe a community college. You will learn things -- how to fix things. And you'll open the door to a pretty good living.

Then get a job. And stay with the job for several years, perhaps climbing the ladder along the way.

And then get married. But don't jump into bed immediately. As my wife puts it, "Do some research." Then stay married for several years. Learn the sacrifices and responsibilities and compromises -- and the happiness.

And only then, have a kid.

There's nothing original about this thinking. I call it Kudlow 101. The trouble is, in our society, we are doing this backward. People don't finish school. Don't take a job. Don't get married. But do have kids. Wrong order. Wrong formula.

Now some statistics.

Naomi Schaefer Riley writes that "children of married parents are more likely to graduate high school, less likely to go to jail and more likely to delay sexual activity. And of course, children of unmarried parents are more than five times as likely to live in poverty."

Economic writer Robert Samuelson notes that single-parent families have exploded, that more than 40 percent of births now go to the unwed, and that the flight from marriage "may have subtracted from happiness." Citing a study from Isabel Sawhill, he notes that some unwed mothers "will have multiple partners and subject their children 'to a degree of relationship chaos and instability that is hard to grasp.'"

Heritage Foundation economist Stephen Moore writes "that marriage with a devoted husband and wife in the home is a far better social program than food stamps, Medicaid, public housing or even all of the combined." Moore points to a Heritage study showing how welfare households are much more likely to have no one working at all, with social assistance becoming a substitute for work.

A recent report from the American Enterprise Institute and the Institute for Family Studies, authored by W. Bradford Wilcox and Robert Lerman, reveals that married men have higher average incomes, seem to be more productive at work and work more and earn more. Wilcox and Lerman write that 51 percent of the 1980-2000 decline in male employment is due to the drop in marriage rates, and is highest among unmarried men. They find that "differing employment rates among married and unmarried men aren't simply due to education levels or race, either." [Emphasis mine.]

They conclude: "Promoting the importance of marriage, looking for ways to reduce marriage penalties in current means-tested welfare programs and engaging leaders at every level to find ways to strengthen marriage in their communities, are other critical steps to take to restore a culture of marriage."

I'll only add this, as I did at the Coolidge Foundation dinner: While restoring economic growth may be the great challenge of our time, this goal will never be realized until we restore marriage.

In short, marriage is pro-growth. We can't do without it.

END QUOTE

On behalf of all of us at Halbert Wealth Management and ProFutures, let me wish you and yours a very memorable and HAPPY THANKSGIVING!

Very best regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.