Shortly after each month end (after the most recent reported earnings numbers are posted), I like to run through a few of my favorite valuation charts to gauge level, asses risk and to get a sense for what the probable forward return may be. Fortunately, there is a great deal of historical data that can help us.

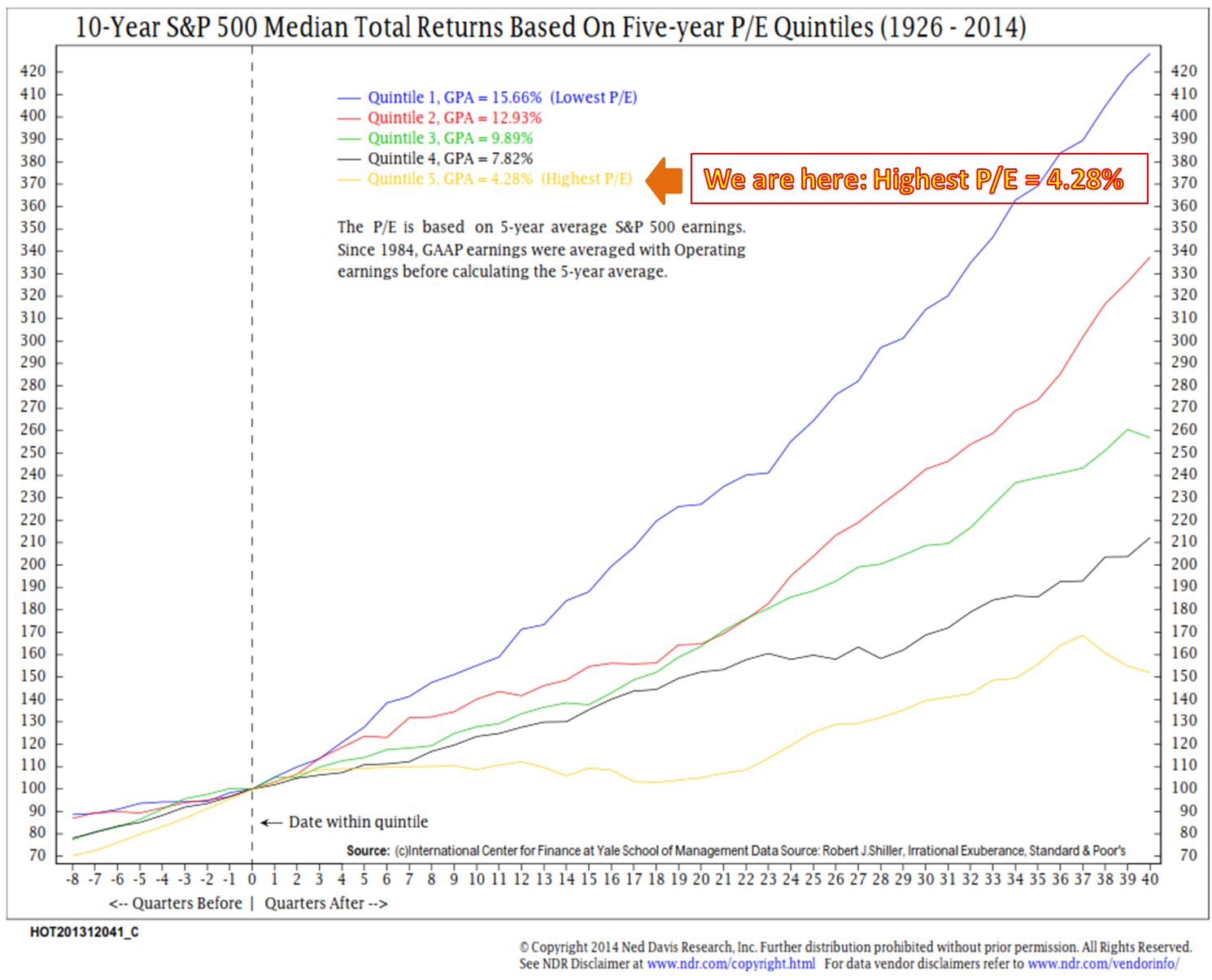

This week you’ll find several familiar valuation charts and one in particular that I believe can give us a meaningful sense of the stock market’s return over the next ten years. This chart looks at Price Earnings (“P/E”) from 1926-2014 and organizes P/E into five quintiles from the lowest P/E quintile (inexpensively priced market) to highest P/E quintile (expensively priced market).

It should be no surprise that when the starting point is an attractively priced market (lowest P/E quintile), the return over the subsequent ten years is highest at 15.66% per year and when the market is expensively priced (highest P/E quintile), the return over the subsequent ten years is lowest at 4.28% per year.

So where are we now? The market remains in the highest P/E quintile – expect low forward returns.

Let’s keep this week’s post on market valuation short and to the point. I share with you several valuation charts and include a new one (which is a broad look at a number of different valuation measures) I hope you find helpful. In short, stocks remain richly valued.

I conclude today’s post with a few ideas as to what this means and what you can do about it.

Included in this week’s On My Radar:

- S&P 500 Index Median P/E

- What P/E Quintiles Tell Us About Forward Return

- A Broad Look at Various Valuation Factors – Stocks Remain Richly Priced

- Trade Signals – Good News and Bad News (Mostly Good)

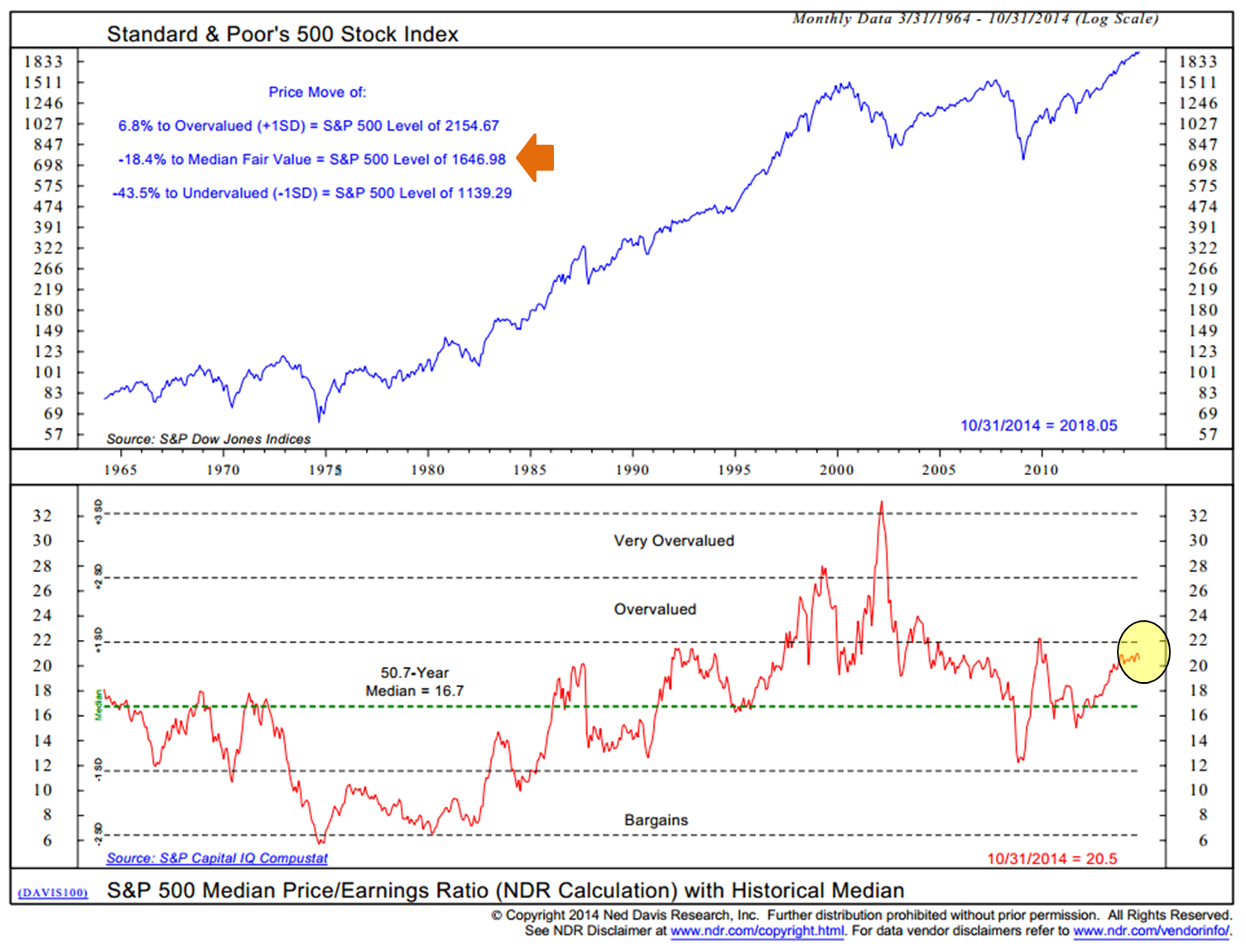

S&P 500 Index Median P/E

When I look at the following chart, I try to get a sense of where Median Fair Value on the S&P 500 Index is – here you can see (orange arrow) that the median fair value is 1646.98. It has crept higher over the last few years just as earnings have advanced higher.

2154.67 marks an overvalued market and 1139.29 an undervalued market. Let’s call these levels the upside and downside of the current opportunity/risk range.

Let’s keep the 20.5 Median P/E reading from 10-31-14 in mind when we look to the next section.

What P/E Quintiles Tell Us About Forward Return

In the following chart, note that the orange arrow shows that the 20.5 reading is in Quintile 5. The forward returns are lowest moving forward when your starting point is a high median P/E.

10-year S&P 500 Index median total returns when your starting point is in Quintile 5 is an average return of 4.28% per year. Note the more attractive returns in Quintile’s 1, 2, 3 and 4 by comparison.

The conclusion is straight forward. It’s best to overweight equities when valuations are favorable – Quintile 1. Even Quintile’s 3 and 4 may be sufficient enough returns but this, of course, depends on your return objectives. Think about overweighting your portfolio exposure more to equities when in Quintile 1 and 2 and underweighting (and hedging) when in Quintile 5. More or less you need to base your exposure on the potential for forward return.

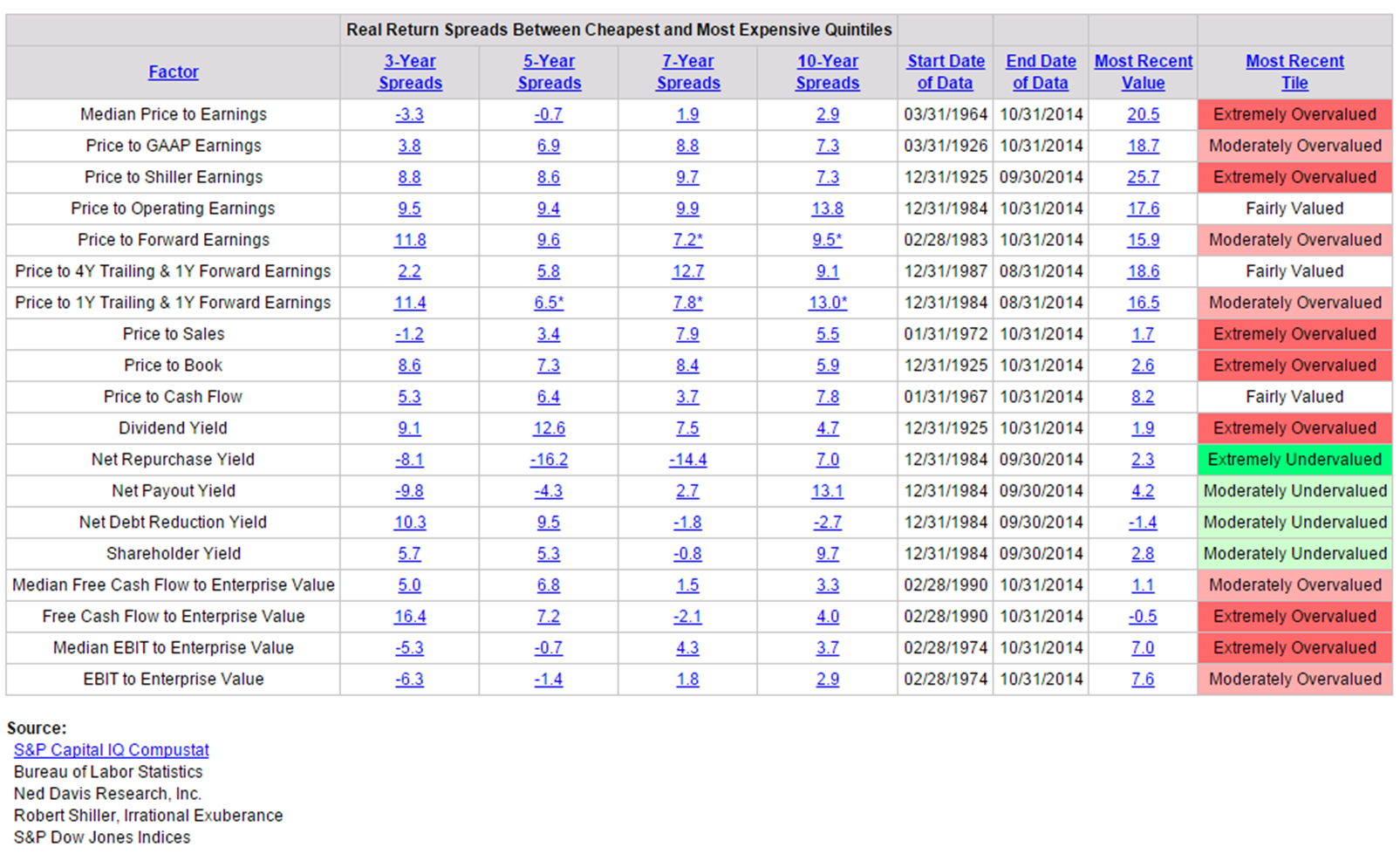

A Broad Look at Various Valuation Factors – Stocks Remain Richly Priced

Next is a simple valuation dashboard. The factors are listed on the left and the far right of the chart sums up the current state. You be the judge of the current state of various valuation factors. Again, I like median P/E.

I mentioned in past posts that P/E based on Forward Earnings is the measure I least favor. Frankly, earnings tend to be highly mean-reverting. Perhaps best summed up in the following quote:

“Profit margins are probably the most mean-reverting series in finance, and if profit margins do not mean-revert, then something has gone badly wrong with capitalism. If high profits do not attract competition, there is something wrong with the system and it is not functioning properly.”

– Jeremy Grantham, Barron’s, Source

As of 10-31-14 that factor’s most recent value was 15.9. That, too, is high by historical standards but to me is an untrustworthy form of measure. Finally, as it relates to P/E. I wrote a piece (HERE) in Forbes titled Stock Market’s High P/E Suggests Lower Returns Ahead. I hope you find this information helpful.

Trade Signals – Good News and Bad News (Mostly Good)

Technical evidence remains positive. Big Momentum (“Mo”) is in a buy signal since October 14, 2011 and trend evidence (as measured by the 13/34-Week EMA – see chart 2) is positive.

Investor sentiment has moved quickly from Extreme Pessimism to Extreme Optimism. This is neutral at best with such optimism suggesting caution.

I remain modestly bullish on equities (but favor that exposure hedged) and remain bullish on both high yield bonds (uptrend) and high grade bonds (uptrend as measured by the Zweig Bond Model).

Included in this week’s Trade Signals:

- Cyclical Equity Market Trend: Cyclical Bullish Trend for Stocks Remains Bullish (as measured by NDR’s Big Momentum indicator and separately by the 13/34-Week EMA S&P 500 Index Trend Chart)

- Weekly Investor Sentiment Indicator – NDR Crowd Sentiment Poll: Extreme Optimism

- Daily Trading Sentiment Composite: Extreme Optimism

- The Zweig Bond Model: Cyclical Bull Trend for Bonds (supporting longer-term treasury and Corporate bond exposure)

Click here for the full link, including updated charts, to Wednesday’s Trade Signals post (trend and sentiment charts)

Conclusion

It’s easy to get confused about P/E. Some say the current P/E is 15.9, therefore the market is attractively priced. However, those estimates are based on Wall Street’s forward earnings estimates and those analysts have a bad habit of over-estimating and tend miss by a wide margin. I favor median P/E or some form of a smoothing method (like Shiller) that is based on actual reported earnings. From there we can compare against its historical data set to get a sense on what forward returns might be. To that end, the math today is clear – the market is expensively priced.

What this means for you and me is that risk is higher than normal. Since stocks are richly priced, forward return is likely to be low.

I share several ideas as to what you can do:

- In such an environment, common sense to me says to tighten up risk management and overweight strategies that are far more flexible in nature.

- Learn more about relative strength trading strategies: There is always an asset moving up in price and strategies such as relative strength can help move you towards the assets that are showing the strongest price leadership.

- Trend following, such as setting a stop-loss exit trigger at a security’s 200-day smoothed moving price average, can help you stay with a stock, ETF, bond or commodities primary trend. I like Big Momentum (see Trade Signals) to help me identify the market’s primary trend.

One of the all-time great investors, Paul Tudor Jones, was interviewed in Tony Robbins’ new book called Money: Master the Game. Following are several quotes:

- “There’s never going to be a time where you can say with certainty that this is the mix I should have for the next five or ten years. The world changes so fast. If you go and look right now, the valuations of both stocks and bonds in the US are both ridiculously overvalued. And cash is worthless, so what do you do with your money? Well, there’s a time when to hold ‘em and a time when to fold ‘em. You’re not going to necessarily always be in situation to make a lot of money, where the opportunities are great.

- So the turtle wins the race, right? I think the single most important things that you can do is diversify your portfolio. Diversification is key, playing defense is key and, again, just staying in the game for as long as you can.

- I teach an undergrad class at the University of Virginia and I tell my students, “I’m going to save you from going to business school. Here, you’re getting a $100k class, and I’m going to give it to you in two thoughts, okay? You don’t need to go to business school; you’ve only got to remember two things. The first is, you always want to be with whatever the predominant trend is.

- My metric for everything I look at is the 200-day moving average of closing prices. I’ve seen too many things go to zero, stocks and commodities. The whole trick in investing is: “How do I keep from losing everything?” If you use the 200-day moving average rule, then you get out. You play defense, and you get out.”, Source

When risk is high (an expensive market or security), it makes sense to think and plan accordingly. The market’s trend remains positive (see Trade Signals) and I sit patiently in the cyclical bull market camp; however, risk remains high so include a diverse set of risks within your portfolios, overweight tactical strategies (look at relative strength and trend strategies) and hedge that equity exposure. Some day soon equity valuations will be back in Quintile 1 and we can shift back once again to overweight equities.

See On My Radar: Stocks Remain Richly Valued for Important Disclosure Information.

© CMG Capital Management Group

© CMG Capital Management Group