IN THIS ISSUE:

1. October Unemployment Rate Fell to 5.8%

2. Employment For Young People Highest in Six Years

3. Retirement Saving Not Happening For a Third of Middle-Class

4. Just How Little Have They Saved?

5. The Power of the 401(k) Savings Plan

6. The Retirement Saving Big Picture

Overview

Each year Wells Fargo & Company conducts a survey of middle-class Americans of various ages to see how they are faring with saving for retirement. The results of the 2014 survey were just made public late last month. I will summarize them for you below. Let me warn you in advance – they are not pretty!

But first, let’s take a look at last Friday’s better than expected October unemployment report. The headline unemployment rate fell to 5.8%, the lowest level in almost six years. So far in 2014, new jobs are being added at the fastest pace since 1999. Best of all, the employment rate for young people ages 25-34 rose to the highest level since late 2008.

To all of our brave men and women who have served in our Armed Forces, we thank you and wish you a Happy Veterans Day!

October Unemployment Rate Fell to 5.8%

Non-farm payroll employment rose by 214,000 jobs in October, nudging the unemployment rate down a notch to 5.8%, the lowest level since July 2008, as many companies added workers to gear up for the holiday season. The economy has now added 200,000 workers or more for nine straight months, a feat last accomplished in 1994.

Economists had expected a seasonally adjusted gain of 243,000 nonfarm jobs, so the report fell short of the consensus. However, so far in 2014 the US has gained an average of 229,000 jobs a month, the fastest pace since 1999. Employment gains for September and August were revised up by a combined 31,000.

Yet despite the acceleration in hiring this year, average hourly wages were little changed. Hourly pay rose only 0.1% in October to $24.57, putting the 12-month increase at 2%., the Labor Department said last Friday. The amount of time people worked each week, however, rose a tick to 34.6 hours and matched a post-recession high.

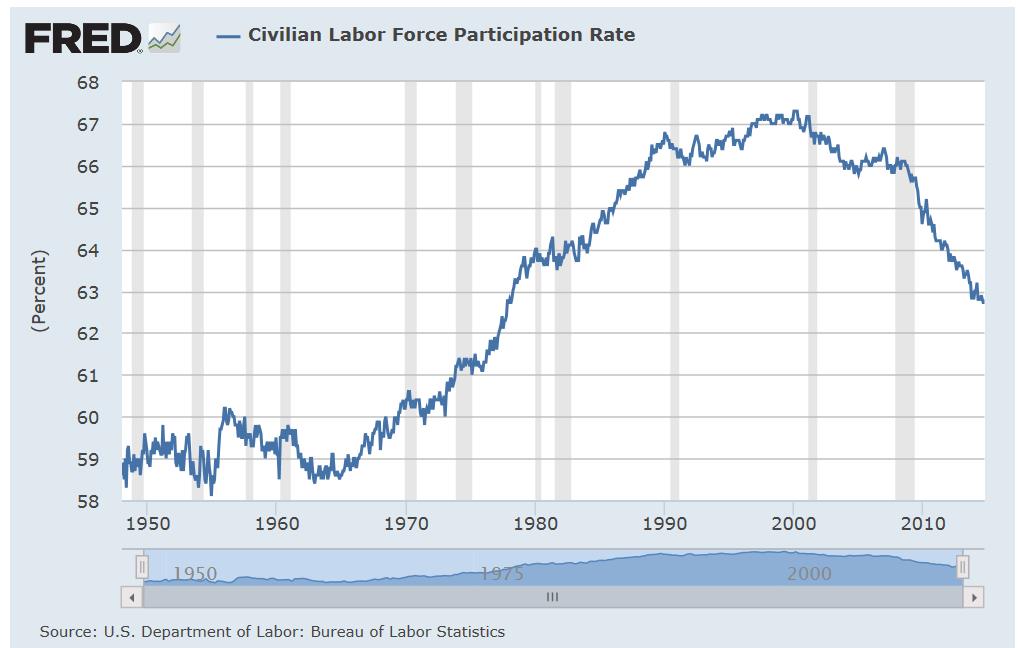

The labor-force participation rate edged up to 62.8% from 62.7% as more people looked for work. Still, as you can see in the chart above, the labor force participation rate peaked in the late 1990s and has been trending down ever since.

Employment For Young People Highest in Six Years

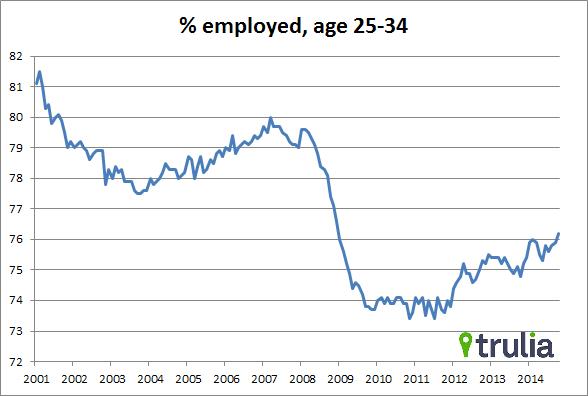

Among 25 to 34-year olds, the percentage who were employed (the “employment-population ratio”) hit76.2% in October – the greatest proportion since the end of 2008 – and up from 74.8% a year earlier, according to the Labor Department.

As the employment environment strengthens for young workers, that should improve their chances of buying homes, as well as their appetite for home ownership.

Young workers face a number of major challenges when it comes to homeownership, with their share of residential purchases recently hitting a 27-year low. Young workers have a particularly tough time putting together enough cash for a down payment, especially as they face a growing load of student debt.

Regulators are working to ease the flow of credit, hoping to widen the pool of borrowers. Didn’t we see this movie before in 2007 and 2008?

Retirement Saving Not Happening For a Third of Middle-Class

Saving for retirement is a formidable challenge for many middle-class Americans. Some say we have a full-blown retirement saving crisis in this country. I would agree. For the past five years, Wells Fargo & Company has conducted a nationwide survey on consumer saving patterns.

On behalf of Wells Fargo, national polling firm Harris Interactive conducted 1,001 telephone interviews from July 20 to August 25, 2014 of middle-class Americans between the ages of 25 and 75, with a median household income of $63,000. Here are the numbers:

Among all those surveyed, 34% are not currently contributing anything to a 401(k), an IRA or other retirement savings vehicle, according to the latest Wells Fargo Middle-Class Retirement Study. Some41% of middle-class Americans between the ages of 50 and 59 are not currently saving for retirement.

Nearly a third of all respondents say they will not have enough money to “survive” on in retirement, and this increases to nearly half of middle-class Americans in their 50s. Over two-thirds of all respondents affirm that saving for retirement is “harder than I anticipated.”

Perhaps the difficulty has caused more than half to say they plan to save “later” for retirement in order to“make up for not saving enough now.” Joe Ready, director of Institutional Retirement and Trust comments:

“Saving for retirement isn’t easy. It requires sacrifice, and it’s not something people can push off and hope to achieve later in life. If people in their 20s, 30s or 40s aren’t saving today, they are losing the benefit of time compounding the value of their money. That growth can’t be made up later, so people have to commit early in life to make savings a regular discipline year after year – it is the only way most people will achieve their financial goals to carry them through retirement.”

For those between the ages of 30 and 49, some 59% say they plan to save later to make up retirement savings, and 27% are not currently contributing savings to a retirement plan.

Some 61% of all middle-class Americans, across all income levels, admit they are not sacrificing “a lot” to save for retirement, whereas 38% say that they are sacrificing to save money for retirement. A staggering72% of all middle-class Americans say they should have started saving earlier for retirement, up from 65% in 2013.

When respondents were asked if they would cut spending “tomorrow” in certain areas in order to save for retirement, over half said they would: 56% say they would give up treating themselves to indulgences like spa treatments, jewelry or impulse purchases; 55% say they’d cut eating out at restaurants as often; and51% say they would give up a major purchase like a car, a computer or a home renovation.

Just How Little Have They Saved?

According to this year’s survey, middle-class Americans have saved a median of only $20,000, which is down from 2013. Middle-class Americans across all age groups in the study expect to need a median savings of $250,000 for retirement, but they are currently saving only a median amount of $125 each month.

Respondents between the ages of 30 and 49 are putting away a median amount of $200 each month for retirement, whereas those between the ages of 50 and 59 are putting away a median of only $78 each month for retirement according to the survey. This is counter intuitive! Older people should be putting more, not less, into their retirement savings.

Only 28% of all age groups included in the survey reported that they have a written financial plan for retirement. People with a written plan for retirement are saving a median of $250 per month, far greater than the median $100 per month that is being saved by those without a financial plan. Mr. Ready added:

“People who have a written plan for retirement are helping themselves create a future on their own terms, with a foundation built on saving, and hopefully, investing. As evidenced by the difference in monthly savings amounts for those with a written plan and those without, it is clear that a plan makes a sizeable difference.”

The Power of the 401(k) Savings Plan

Middle-class Americans value the 401(k) as a way to create a retirement nest egg. Some 70% of respondents said they have a 401(k) or equivalent plan available to them through their employer, and a large majority of them, 93%, are currently contributing to their plans.

Apprx. 67% of those in a plan contribute enough to maximize their company’s 401(k) match, and the median contribution rate for those between the ages of 30 and 59 is 7%.

Apprx. 85% of those with access to a 401(k) or equivalent plan from their employer affirm they “wouldn’t have saved as much for retirement” if they did not have the 401(k). Moreover, 90% say the 401(k) or equivalent plan “makes it easy to save for retirement.”Mr. Ready adds:

“The 401(k) makes a significant difference for people in that it gives them the ability to save in a regular, systematic way. It conditions people to think that saving money is paying themselves first and is just as important as paying day-to-day bills.”

If you have access to a 401(k) plan, by all means maximize your contributions to it.

Retirement Savings by Age Groups

Examining retirement savings by age, the median amount saved by those in their 40s is $40,000; for those in their 50s it’s only $20,000; and those in the age range of 60 to 75 it’s $25,000. Kudos to those younger folks who have saved more than their older counterparts!

The median amount saved by those who have access to a 401(k) plan is much higher than that saved by those without access to a plan, particularly for those who are younger. Middle-class Americans between the ages of 25 and 29 with access to a 401(k) plan have saved a median of $10,000 versus a median of zero savings for those without access.

Respondents between the ages of 30 and 39 with access to a 401(k) have saved a median of $35,000 versus those without access who have saved a median of less than $1,000. Those between the ages of 40 and 49 with access to a 401(k) have saved a median of $50,000 versus the $10,000 saved by those without access.

Having access to a 401(k) also seems to positively impact a sense for what is possible. More than half of workers without access to a 401(k) plan say “it is not possible” to pay bills and save for retirement, compared to a third of those who have access to a plan.

Those who have access to a 401(k) are more likely to say they would cut expenses and forego big purchases in order to save for retirement, at a rate approximately 10 percentage points higher than those without access to a 401(k).

The Retirement Savings Big Picture

Across all age groups, almost half of non-retirees are not confident that they will have saved enough “to live the lifestyle they want” in retirement. This lack of confidence jumps to 71% for non-retirees between the age of 50 and 59.

A quarter of all middle-class Americans say they “get depressed” when thinking about their financial life in retirement. However, the rate of those who feel down about retirement increases to one in three for those in their 40s and 50s.

In a new Wells Fargo survey question this year, 22% of the middle-class say they would rather “die early”than not have enough money to live comfortably in retirement.

Working longer into traditional retirement years appears to be a predicted reality for one-third of middle-class Americans who say they will need to work until they are “at least 80 years old,” because they will not have enough retirement savings. Half of those in their 50s say they will need to work until age 80.

In another new question asked this year, a quarter of middle-class Americans say working into their 80s is something they plan to do even if it’s not a financial necessity. But the reality is that there’s no way to know if your health will allow that or if jobs will be available.

Some 70% of middle-class Americans do not think Social Security will be their primary funding source for retirement, but the perception varies greatly for those based on age. Almost half of non-retirees in their 50s think Social Security will be their primary source of income, as do 56% of non-retirees between the ages of 60 and 75.

Those are the highlights (or lowlights) from the 2014 Wells Fargo Middle-Class Retirement Study. There are some out there that dispute the fact that there is a retirement savings crisis. Ignore them! It’s real.

Conclusions: Start Early, Save More

Over the last 40-50 years, corporate America has transitioned away from so-called “defined-benefit plans” and pensions which guarantee lifetime income, in addition to Social Security. Just three decades ago almost 40% of private sector workers had such a pension, while only 17% had a “defined-contribution plan” like a 401(k).

Those figures have reversed. Today, only 14% have a traditional pension while 42% have a 401(k) or similar plan. This means individuals are becoming increasingly responsible for their own retirement security. Unfortunately, as the data above show, most Americans are doing a very poor job of saving and planning for their retirement.

My own two kids will be graduating from college next spring; both will have a Master’s Degree in their respective fields (engineering and accounting); and thankfully, both already have solid, well-paying jobs waiting for them.

Even though our kids have long been frugal savers, Debi and I will strongly encourage them to save at least 15% of their take-home pay when they start their new jobs next summer. We will also encourage them to fully participate in their employers’ 401(k) plans, contributing enough each year to maximize any “matches” offered by their new employers.

For those in their 40s, 50s or older that haven’t saved much (or anything) for retirement, start saving as much as you possibly can as soon as you possibly can. For those already in retirement, talk to your kids and grandkids about the importance of saving enough for their retirement.

Happy Veterans Day!!

All of us at ProFutures/Halbert Wealth Management offer our sincere thanks and appreciation for all of the men and women who have served our great country. For all of you reading this, we hope you have a wonderful Veterans Day, and we salute you for your service.

Very best regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert, Mike Posey (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.