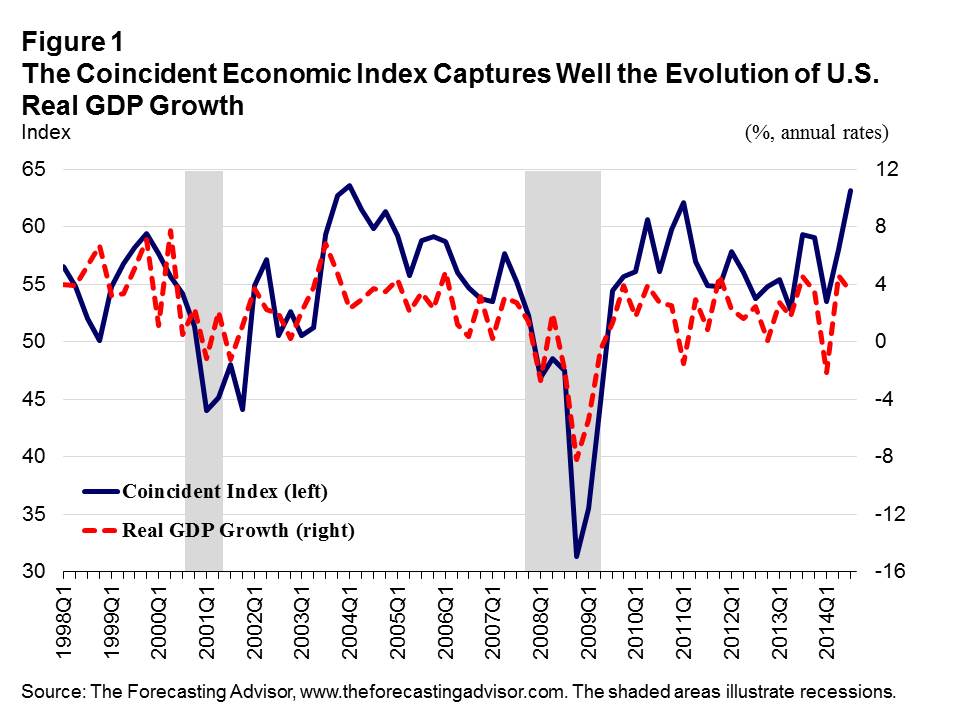

At the start of each month, the U.S. Institute for Supply Management (ISM) released data on the state of the manufacturing and non-manufacturing industries of the U.S. economy. The data are closely followed by economists, stock market brokers, and the media as they provide the earliest reading on the current state of the economy. The ISM provides data on the current performance of a number of indicators related to the manufacturing and non-manufacturing industries, such as production, employment, new orders, and backlog of orders, deliveries, inventories, new exports, imports, and prices. Figure 1 plots the evolution since the first quarter of 1998 of a proprietary coincident economic index from The Forecasting Advisor, built from a number of indicators from both the survey on manufacturing and non-manufacturing industries, and U.S. real GDP growth.

The aggregation of indicators from both surveys into a coincident economic index provides a close relationship with historical movements in real GDP growth. In other words, the Figure suggests that the coincident index contains useful information on the actual strength of economy. Because the ISM data are never revised, except for the annual updates of the seasonal adjustment factors, the coincident economic index is a useful real time forecasting tool and provides valuable leading information on ongoing changes in the pace of economic growth.

U.S. Real GDP Growth Outlook

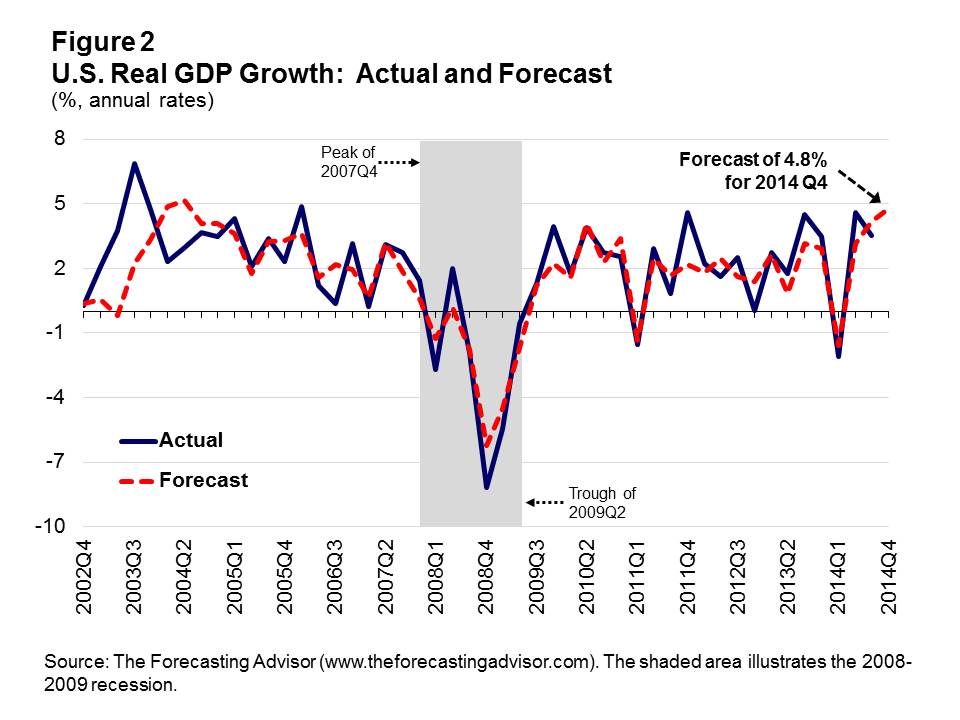

The value of the coincident economic index for the month of October is used here to get a first forecast of the rate of growth in U.S real GDP for the fourth quarter of 2014. The official advance estimate of real GDP growth for the fourth quarter of 2014 will only be released by the U.S. Bureau of Economic Analysis at the end of January 2015.

The forecast for the fourth quarter of 2014 is reported in Figure 2. The U.S. economy is expected to continue to grow at a strong pace, which bodes well for job creation and corporate profits. In the last quarter of 2014, real GDP is projected to rise by 4.8% (annual rate). This follows a gain of 3.6% and 4.6% in the previous two quarters.

© Robert Lamy, The Forecasting Advisor