Consumer Confidence Hit a 7-Year High in October... But

IN THIS ISSUE:

1. First Estimate of 3Q GDP Came In Better Than Expected

2. Additional Thoughts on Last Week’s Fed Policy Statement

3. Consumer Confidence & Sentiment Indexes Hit 7-Year Highs

4. Two-Thirds Believe the Country is Headed in Wrong Direction

5. World Trade Center “Freedom Tower” Opens to Tenants

Overview

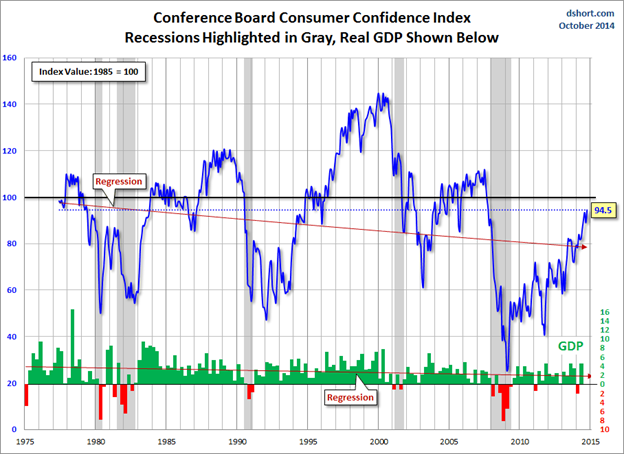

The two most widely-followed indicators of consumer confidence jumped to the highest levels in seven years last week. The Conference Board reported Tuesday that its Consumer Confidence Index climbed to 94.5 in October, the strongest reading since October 2007 before the economy entered the Great Recession.

Then on Friday, the University of Michigan’s Consumer Sentiment Index rose from 84.6 in September to86.9 in October, the highest level since July 2007. It was the third consecutive monthly increase in this Index. Respondents to both surveys cited expectations of better economic growth and job gains in the coming months, along with falling gasoline prices, as reasons for their optimism.

Yet at the same time, the latest polls on the Direction of the Country show that a whopping 66.0% of Americans believe the country is headed in the wrong direction with only 27.8% who believe the nation is moving in the right direction.

There is a huge disconnect between these measures of consumer confidence versus how Americans feel about the direction the country is headed. Today I’ll take a shot at trying to explain how and why this dichotomy exists.

Before we get to that discussion, let’s take a closer look at last Thursday’s advance report on 3Q Gross Domestic Product which came in at a better than expected 3.5% following the 4.6% showing in the 2Q.

We’ll also take another look at the Fed’s decision last Wednesday to end quantitative easing (QE). A further analysis of the official statement released after the policy meeting yields more clues as to when the Fed might start raising interest rates at long last.

Following our discussion of last week’s positive GDP report and the Fed’s decision to end QE, we will examine the consumer confidence measures that hit 7-year highs in October. Let’s get started.

First Estimate of 3Q GDP Came In Better Than Expected

The Commerce Department reported last Thursday that 3Q GDP rose 3.5% (annual rate). That easily beat the pre-report consensus of 3.0%. This was the first of three estimates on 3Q GDP. It will be revised two more times near the end of November and December.

According to the advance report, the increase in GDP in the 3Q primarily reflected positive contributions from consumer spending, exports, nonresidential fixed investment, federal government spending and state and local government spending.

The latest report was a very encouraging sign for the US economy. It was the fourth time in the last five quarters that GDP has increased by 3.5% or more. Take a look:

| 2Q 2013 | +1.8% | 1Q 2014 | -2.1% |

| 3Q 2013 | +4.5% | 2Q 2014 | +4.6% |

| 4Q 2013 | +3.5% | 3Q 2014 | +3.5% |

The US economy is clearly gaining momentum even as most developed economies around the world are struggling. The one negative period shown above was the first quarter of this year and was largely attributed to the severe winter weather. It will be interesting to see how economists adjust their estimates for 4Q GDP in light of last week’s report.

Additional Thoughts on Last Week’s Fed Policy Statement

As I wrote in my blog last Thursday, the Fed’s decision to end its controversial “quantitative easing”program surprised virtually no one. The enormous QE bond buying which began in late 2008 resulted in the Fed’s balance sheet exploding to an unprecedented $4.5 trillion. No central bank in the history of the world has printed this much money!

Following the conclusion of its latest FOMC meeting on Wednesday of last week, the Fed issued its usual policy statement outlining what was decided at this latest gathering of officials. The big question was whether or not the Fed would change its so-called “forward guidance” on when it might raise the Fed Funds rate for the first time since 2007.

For most of this year, the Committee included language in the policy statement which stated that short-term rates would remain near zero for a “considerable time” after the QE bond buying program came to an end. Some Fed watchers thought that the central bank might remove that considerable time language at last week’s meeting. It did not.

However, some new language in the latest policy statement suggested that the Committee could well drop the considerable time language at its next meeting in December – after which Fed Chair Janet Yellen will hold a press conference to explain any decisions and answer questions.

Upon further analysis of the Fed policy statement last Wednesday, there are a few interesting changes that are notable. First, the Fed upgraded its assessment of the US economy. The statement noted that consumer spending is improving, and the labor markets are improving.

Second, as for US inflation which is running below the Fed’s target of 2%, the Fed noted that falling energy prices are the main reason inflation has retreated as of late. They expect inflation to increase modestly when energy prices bottom out.

Third, the Fed also added broad, flexible language that ties the timing and pace of any future rate hike to incoming economic data. Since most forecasters expect the economic recovery to remain firm, most Fed watchers took that to mean the first rate hike could come sooner rather than later. We’ll see about that.

The next FOMC meeting will be on December 16-17 followed by a Yellen press conference.

Consumer Confidence & Sentiment Indexes Hit 7-Year Highs

US consumer confidence rebounded strongly in October, hitting a 7-year high as solid job gains and falling gas prices raised expectations for economic growth. This came despite slowing economic growth in Europe and China that has fueled volatility in financial markets.

The Conference Board’s Consumer Confidence Index, which had decreased in September, rebounded strongly in October. The Index now stands at 94.5, up from 89.0 in September, well above the pre-report consensus of 87.2. That’s the highest reading in this Index since the fall of 2007.

The solid increase suggests consumers largely dismissed concerns about slowing global growth and have ignored the sharp swings in financial markets in October. Instead, greater hiring and lower gas prices are boosting their outlook.

On Friday we got the latest University of Michigan Consumer Sentiment Index, which also rose to a 7-year high in October. The Index rose from 86.4 in September to 86.9 last month, which was above the consensus of 86.4.

Both of these consumer indicators are very encouraging since consumer spending accounts for apprx. 70% of GDP. However, the improvement in both indexes conflicts with the Direction of the Country surveys which show a completely different picture.

Two Thirds Believe the Country is Headed in Wrong Direction

According to the latest surveys, a large majority of Americans believe that the country is headed in thewrong direction. The latest RealClearPolitics average of six independent polls on this question finds that66.0% of Americans feel the US is headed in the wrong direction with only 27.8% who believe the nation is moving in the right direction.

These independent polls include the likes of CBS News, ABC News/Washington Post, NBC News/Wall Street Journal, Rasmussen and other big pollsters. And this discontent about the direction of the country is not a new phenomenon.

So the question is, how can consumer confidence be at a 7-year high when two-thirds of Americans believe the country is headed in the wrong direction?

As always, the economic signals are mixed. But the headline numbers over the last year support the public’s optimism. As discussed earlier, the economy grew in the 3Q at an annual rate of 3.5%, and has expanded by that much or more in four of the last five quarters. And it is widely agreed that the decrease in 1Q GDP was due to the severe winter weather this year.

It is true that a big increase in defense spending and a drop in oil imports accounted for a good part of the stronger growth in GDP this year. And true, too, spending on business equipment (+7.2%) and by consumers (+1.8%) grew more slowly in the 3Q than in the previous quarter, but at least such spending did expand.

The Fed has done its part, arguably, by holding short-term interest rates near zero for the last five years and buying trillions of dollars of long-dated Treasury bonds and mortgage-backed securities to keep long rates low. While the Fed did end its QE bond buying program as promised, it committed to keep short rates near zero for a considerable time.

Then there are those anecdotal statistics that are useful supplements to the more closely followed government reports:

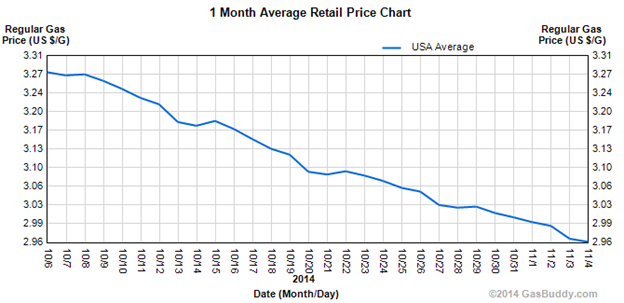

- Gasoline prices are plunging as new supply exceeds shrinking demand, putting cash into consumers’ pockets just as the holiday season starts. The rule-of-thumb is that every 1-cent-per gallon price decline adds $1 billion to consumer purchasing power.

So the 30-cent drop in the past month gives consumers $30 billion more to lavish on toys, apparel, and, of course, iPhones. And economists estimate that every $1 decline in gasoline prices is associated with a 10% increase in sales of cars and trucks, especially of highly profitable SUVs and light trucks.

- Hundreds of thousands of holiday jobs are available. The seven largest retailers have 400,000 openings that are proving so difficult to fill that employers are “bombarding customers’ inboxes and Twitter feeds with help-wanted ads,” according to the Wall Street Journal. Many retailers ring-up between 25% and 50% of their annual sales in the next few months.

- Profits of leading corporations are up, and after some violent gyrations, the S&P 500 Index is up over 10% from the record level reached at the end of last year. This is good for investors and suggests a strong holiday shopping season.

- Finally, Apple’s iPhone 6 and 6Plus accounted for an estimated 10% of all recent US economic growth, adding 0.3% to overall GDP. Innovation is always a good thing.

Taken together, the economic news does explain the uptick in consumer confidence, although that confidence is dampened somewhat by gloomy economic news from Europe, China, Brazil, Russia, and other countries, as well as by stagnant middle-class incomes, and a job market that could be stronger.

But all in all, the good economic news at home outweighs the bad news from numerous foreign countries about which many Americans know very little. Yet despite rising confidence in the economy, most Americans think our country is on the wrong track. The improving economic outlook marches in parallel with a largely bipartisan fear that the institutions of government are just not working.

The administrative branch, led by the president, refuses to protect our borders from an influx of illegal immigrants (many of which are children), or protect the White House from intruders, or talk coherently about the threat of Ebola and how to protect us.

The legislative branch, Congress, is dysfunctional. Democrats are split between moderates appealing to independent voters and the left that is rallying the party’s “core” to remain on a “progressive” path to the 2016 presidential election. Republicans are afraid to speak out on politically-sensitive issues and are divided by the Tea Party that sees compromise as weakness.

Other institutions are also in ill-repute. The once-vaunted Secret Service proved unable to prevent a dangerous intruder from penetrating the inner rooms of the White House, or an armed man with a criminal record from entering an elevator with the president.

The Centers for Disease Control, once the most widely respected government agency, fumbled its response to Ebola, unnerving a public that once looked to the CDC for guidance when faced with a health scare.

The Department of Veterans Affairs is unable to deliver adequate healthcare to the nation’s veterans. The Internal Revenue Service, always unloved but once thought to be impartial as it went about tax collecting, became politicized and targeted conservative groups. The education system continues to graduate students unfit for the modern workforce.

All of this has to be a big part of why two-thirds of Americans believe the country is headed in the wrong direction long-term, even as confidence in the short-term is riding high.

Today is Election Day and the latest polls and early voting data suggest a big turnout by Republicans. We’ll see when the results are in. Most late polls suggest the GOP will gain the majority in the Senate. Again, we’ll see.

World Trade Center “Freedom Tower” Opens to Tenants

Last week, I wrote about our recent trip to New York City to visit the 911 Memorial & Museum. We also saw the World Trade Center Freedom Tower which was not yet open. Now it is. Thirteen years after the Twin Towers were destroyed on September 11, 2001, the new centerpiece skyscraper at the World Trade Center opened for business yesterday morning.

The Freedom Tower is truly iconic in design. Standing at a symbolic 1,776 feet (which includes its landmark spire), it has 104 stories, including a three-floor observatory at the top that will be open to the public in the spring. Also called One World Trade Center, it is the tallest building in the country and the western hemisphere. The cost to build it was $3.9 billion – double the original estimate.

Very best regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert, Mike Posey (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.