Hong Kong gets occupied

October 10, 2014

Just over three years ago, a group of disaffected young people took over a small public park near Wall Street, and the “Occupy” movement began. Their numbers and their cause reached a zenith a few weeks later, but the effort atrophied without making lasting impact.

The Occupiers found new life last month in Hong Kong, when protestors took over a much larger swath of territory in the Central District to press their case for change. A world apart, the two situations nonetheless have similar roots in economic concerns. It remains to be seen whether the Hong Kong edition will retreat as meekly.

At the core of the grievances laid out by the Occupy Central movement was the electoral system established under the Basic Law, the framework underlying the relationship between Hong Kong and mainland China. Currently, the Basic Law allows open elections for a majority of members of the Legislative Council, but the chief executive is selected in Beijing without any popular input. Pro-democracy protestors usually rally around this issue during Hong Kong’s annual July 1 protests, then matters subside and civility quickly returns.

This year, though, Beijing proposed a reform to election of the chief executive, allowing the populace to choose from among a slate of candidates hand-picked by the Chinese Central Committee. Not surprisingly, this outline was immediately rejected by pro-democracy interests, setting off a new wave of protests. But it is important to note that the demonstrations are not solely political. They are also the manifestation of pent-up economic frustration.

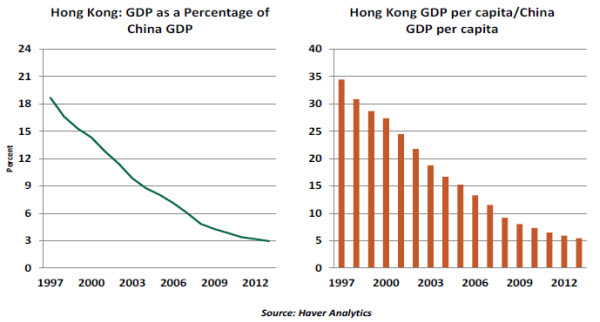

At the time of Hong Kong’s handover to China, officials on both sides took every effort to assure markets that the transition would not disrupt one of the most vibrant, open economies in Asia and that Hong Kong’s freedoms would not be infringed upon. Back then, Hong Kong’s gross domestic product (GDP) amounted to one-fifth that of China, while income per capita was 34 times higher in Hong Kong. So a lot was at stake.

As of last year, Hong Kong’s total output equaled only 3% of China’s GDP, and the income per capita ratio had fallen to 5.4%. While some of this can be attributed to China’s meteoric rise over the past two decades, another portion has come at Hong Kong’s expense. Inflows of mainland Chinese competing for Hong Kong’s unskilled job market have put significant downward pressure on low-end wages. Open investment channels have allowed wealthy Chinese to pour into a controlled real estate market, inflating prices and making housing more difficult to obtain for natives. Hong Kong now has the highest income inequality coefficient in the developed world, and this factor cannot be overlooked when considering the protestors' demands to have a voice in political life.

As of last year, Hong Kong’s total output equaled only 3% of China’s GDP, and the income per capita ratio had fallen to 5.4%. While some of this can be attributed to China’s meteoric rise over the past two decades, another portion has come at Hong Kong’s expense. Inflows of mainland Chinese competing for Hong Kong’s unskilled job market have put significant downward pressure on low-end wages. Open investment channels have allowed wealthy Chinese to pour into a controlled real estate market, inflating prices and making housing more difficult to obtain for natives. Hong Kong now has the highest income inequality coefficient in the developed world, and this factor cannot be overlooked when considering the protestors' demands to have a voice in political life.

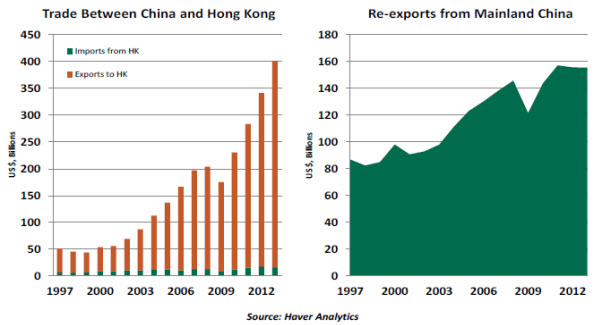

Further, Hong Kong’s role as a pivotal conduit for China’s investments abroad has diminished as China’s domestic financial markets have improved and its banks have grown to rank among the world’s largest. Hong Kong is now a major port for Chinese exports, though the inflow of goods has not followed suit. Rather, Hong Kong increasingly serves as a re-export hub for mainland goods, which does not create the job opportunities and economic dividends expected by Hong Kong’s university graduates.

As China’s growth has far outstripped that of Hong Kong, the incentive for Beijing to be particularly delicate with the region has diminished. Its reticence to compromise with the Occupy Central crowd can also be understood as part of China’s need for social stability. Giving in to the protestors in Hong Kong might make the government appear weak and invite copycats. The Tibet Autonomous Region, Macau and Taiwan are all studying the Hong Kong situation with an eye toward redefining relations with Beijing. China’s comprehensive Internet blackout of events is testimony to how insistent the government is to contain the story.

Legally, China’s control over Hong Kong is limited. The Basic Law places most matters of domestic security squarely in the hands of the Hong Kong government, meaning Beijing can only apply pressure through the chief executive. On the other side, the protestors are negotiating with a Hong Kong government that cannot meet the primary demands of open candidacy for the role of chief executive, which Beijing insists is not within the Hong Kong government’s purview.

A possible compromise would be the resignation of current Chief Executive Leung Chun-ying, who is widely disliked locally, in favor of a candidate seen as willing to listen. Leung has insisted he will not step down, but if the choice is either renewed protests or his ouster, pressure from Beijing may become impossible to resist.

A possible compromise would be the resignation of current Chief Executive Leung Chun-ying, who is widely disliked locally, in favor of a candidate seen as willing to listen. Leung has insisted he will not step down, but if the choice is either renewed protests or his ouster, pressure from Beijing may become impossible to resist.

As the business week started this past Monday, protestors were at a fraction of the numbers seen during the weekend, some barricades had been willingly taken down and there was a sense that normalcy would return to districts that one week ago were congested with demonstrations. But the underlying issues that gave rise to the unrest have not been addressed. Until they are, the renewed calm on the streets of Hong Kong could merely be a prelude to another wave of instability, perhaps even larger than before.

The Truth About Corporate Taxes

The financial press has been buzzing this year with coverage of corporate “inversions.” To some, business combinations between U.S. firms and foreign firms are arranged primarily to avoid a high U.S corporate income tax rate. To stop the practice, these observers say, steep cuts in U.S. corporate taxes are required. But both the nature of these transactions, their motivations and their impact on national finances can be easily misunderstood.

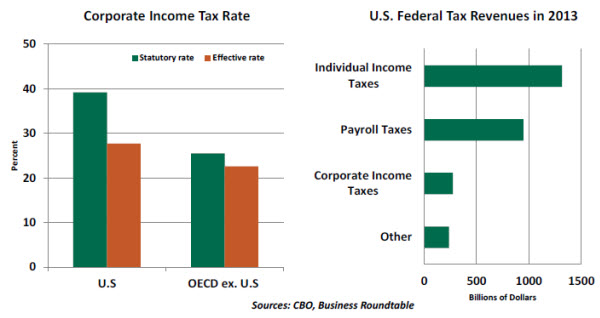

Firstly, some background on the relative standing of U.S. corporate income taxes is useful. The highest statutory U.S. corporate tax rate is 39.2% (35% federal tax plus average of state corporate income tax) compared with 25.5% for OECD countries excluding the United States. These figures are often cited as evidence the United States is harming itself competitively.

However, it is less well-known that the effective corporate income tax rate (what companies actually pay as a percentage of their income) in the United States is significantly lower than the statutory rate.

A PriceWaterhouseCoopers study indicates that the effective U.S. corporate tax rate is 27.7%, versus 22.6% for OECD countries excluding the United States. This study and others show similar results with one important conclusion – the effective U.S. corporate tax rate is noticeably smaller than the statutory rate, and differences in the corporate income tax rate are less than typically assumed.

The large difference between the U.S. statutory rate and the effective rate stems from very generous American tax preferences, which come in the form of deductions, credits and exemptions. The Joint Committee on Taxation estimates that corporate tax preferences amounted to roughly $150 billion in fiscal year 2013. The two largest items are deferral of income tax payments by multinational firms and accelerated depreciation of equipment.

These and other tax preferences result in an inefficient allocation of resources, as decisions are partly based on which project has the largest tax benefit as opposed to choosing projects that yield the best economic return. They also result in complexities and compliance costs.

These and other tax preferences result in an inefficient allocation of resources, as decisions are partly based on which project has the largest tax benefit as opposed to choosing projects that yield the best economic return. They also result in complexities and compliance costs.

As well, comparisons of tax conditions must take into account where corporate taxes stand in relationship to other revenue sources. For example, the United States does not have the kind of value-added tax that is common in many other countries. So overall, the current U.S. tax system may not be as anti-competitive as some have suggested.

Nonetheless, there are several interesting outlines out there for modifying the current U.S. corporate tax system. The Wyden-Coats proposal reduces the tax rate to a flat 24%, eliminates many tax preferences and accelerates depreciation for larger businesses. It would also limit the interest expense deduction, which is noteworthy because it would reduce debt financing and discourage over-leveraging. The proposal also includes a one-time repatriation holiday for businesses with minimal taxes.

The current administration’s proposal reduces the corporate tax rate to 28%, inclusive of a minimum tax on overseas profits. U.S. multinational firms can opt to defer taxes on foreign earned income until it is repatriated, which encourages deferrals and shifting of income. There is a controversy about this provision, as multinationals have amassed considerable sums abroad resulting in a loss of tax revenue. Some have suggested that the world move to more of a territorial system of revenue collection in which U.S. firms pay taxes on income generated abroad and vice versa.

There are many ways to go about streamlining the corporate tax system to improve incentives without reducing revenue. The objective should be to prevent base erosion and profit-shifting strategies and maintain the competitiveness of the U.S. economy. But given today’s political and lobbying climate, it is unclear if these reforms will be enacted. Like many other things, we’ll have to wait until after next month’s elections to find out more.

Working at Cross-Purposes?

The relationship between Treasury departments and central banks is a complicated one. Ideally, monetary and fiscal policy should be set independently, but neither can have much success without the other’s cooperation.

In some regions, the two are uncomfortably close. Central banks in developing countries are often called upon to purchase government debt or to engineer market conditions that minimize its costs. This can lead monetary policy to stray from its core mission of containing inflation.

The Federal Reserve fell into this practice during World War II, actively monetizing borrowing done to finance U.S. involvement. But in the decades that followed, the Fed stepped back to its traditional focus on growth and inflation. Today, the U.S. Treasury and the Fed keep a studied distance from one another.

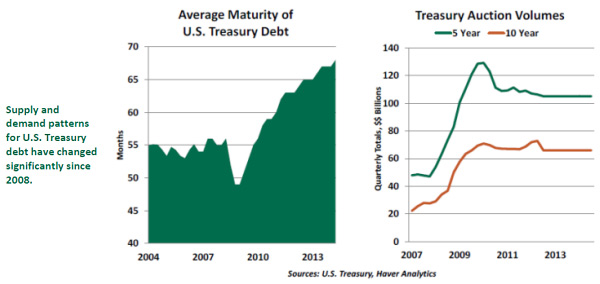

But recent work suggests they may have been tangling with one another recently. Since 2008, the Fed has been increasing its ownership of Treasury securities through quantitative easing (QE). Current holdings of $2.45 trillion represent almost 14% of all Treasury debt held by the public. QE has endeavored to reduce long-term interest rates and thereby stimulate activity.

Over the same period, though, the Treasury has made significant increases in its auctions of longer-term government bonds.

As the supply of long-term securities rises, it offsets the impact of expanded demand from the central bank. A recent study from the Brookings Institution finds that Treasury yields would be almost 50 basis points lower now if the maturity mix of Treasury auctions had remained constant since 2008. Some have said that maturity extension “undermined” the Fed’s efforts.

We don’t doubt the Brookings calculations, but we don’t see anything confrontational going on. The Treasury is looking at the opportunity to lock in very low long-term rates to help finance its long-term obligations (such as Social Security and Medicare). Raising long-term liabilities to fund them seems like good fiscal practice. And limiting the nation’s borrowing costs can be helpful to private sector growth, which helps the Fed achieve its mission.

There certainly are issues over which the Treasury and the Fed have clashed, and there will certainly be others in the future. But trying to find controversy in the recent patterns of government finance seems to be a stretch.

© Northern Trust