IN THIS ISSUE:

1. US Gross Domestic Product Rose Healthy 4.6% in the 2Q

2. “Tax Inversion” Increasingly Popular for US Corporations

3. How the 35% Corporate Tax Rate Stifles the Economy

4. Obamacare Architect: 75 Years is Long Enough to Live

Overview

The US corporate tax rate is the highest among developed nations at 35% at the federal level. Tack on state and local taxes, which can add 5-7%, and US corporations are looking at a 40%-42% income tax burden. But the US takes it even another step further, unlike any other country in the developed world.

Uncle Sam demands that American companies with offshore operations pay US taxes on all income earned abroad – if those profits are repatriated to the US – even though taxes have already been paid to the countries where the income was actually generated. Think of it as double taxation on profits.

No wonder then that more and more US corporations with offshore operations are keeping those profits outside the US in order to avoid this double taxation. It is estimated that up to $2 trillion of those foreign profits are parked outside the US. That is a ton of money which, if brought home, could result in lots of new projects that could create many new jobs.

With an obligation to their shareholders to maximize profits, large US corporations are increasingly taking additional steps to minimize taxes owed to the Treasury in a process that has been coined “tax inversion”as I will explain below. This involves US firms moving their corporate headquarters overseas to countries where the tax burden is lower.

Today, we’ll explore how the extraordinarily high US corporate tax rate hurts the economy and why more and more large American corporations are moving their headquarters offshore. And we’ll look at why the Obama administration is trying to stop it – when all it would take to fix it is the US lowering its tax burden to a more reasonable level. But no, Obama wants to raise corporate taxes even more. This should make for an interesting E-letter.

But before we get into that discussion, let’s take a quick look at last Friday’s third and final report on 2Q Gross Domestic Product.

US Gross Domestic Product Rose Healthy 4.6% in the 2Q

In its third and final estimate of 2Q GDP, the Bureau of Economic Analysis (BEA) reported last Friday that the economy expanded by 4.6% (annual rate) in the April to June quarter, up from 4.2% estimated late last month.

The gain of 4.6% is the strongest since the economic recovery began. But don’t break out the champagne just yet. Much of this growth is simply catching up from the 1Q when severe winter weather led the economy to contract at an annualized pace of 2.1%. The cold weather, it seems, led spending to be deferred a quarter, rather than canceled.

For the first half of this year, the economy expanded at an average rate of only 1.25%. That’s not only slower than the rate through most of the recovery but is also so disappointing that if it persists, it will lead to unemployment rising again. Fortunately, most forecasters expect growth of 2.5%-3.0% for the second half of the year.

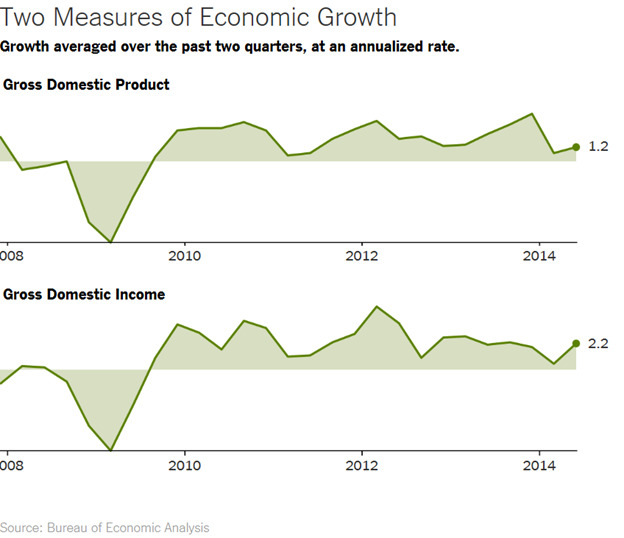

All government reports have their strengths and weaknesses, as does the GDP report. Some economists prefer to look at a separate report within the GDP report called “Gross Domestic Income,” which is calculated by adding up everyone’s income, rather than everyone’s spending.

Because every dollar that you spend also registers as income for someone else, the two measures should, in theory, yield identical estimates. But in reality, Gross Domestic Income is measured using somewhat higher-quality data, and so it tends to yield more reliable signals. Using this measure, the economy expanded 2.2% in the first half of this year, a little better than the first half GDP rate of 1.25%.

“Tax Inversion” Increasingly Popular for US Corporations

By now, you’ve probably heard the term “tax inversion.” You may have even heard President Obama criticize it as “unpatriotic” on the part of US corporations who do it. Tax inversion is the term used to describe transactions that occur when a US corporation buys or merges with a foreign entity and moves its official headquarters offshore in order to achieve more favorable taxation.

In most circumstances, the foreign company purchased is considerably smaller than the US corporation, and the larger firm’s core operations and personnel stay in the US. The tax savings on offshore profits can be substantial, and as of now tax inversion is perfectly legal. The inversion does not affect the taxes paid on profits generated within the US.

Two of the main reasons companies undertake the inversion are to obtain the lower tax rates in the foreign country and escape the US worldwide corporate income tax. As noted above, when state and local taxes are included, the US corporate tax rate becomes 40%-42%. That is the highest rate of all the major world economies.

The second reason is that most other countries only tax profits that are earned inside their own borders. The US, on the other hand, applies its tax rate to corporate profits no matter where they are earned. If corporations want to invest overseas profits back home (after taxes were already paid to a foreign government), they have to open their checkbook again to pay even more taxes to the US Treasury.

While the current administration would like to stop the tax inversion process completely, it would take new laws from Congress. Since that is not likely to occur, the Treasury Department last week announced new changes in the way it is interpreting current tax law as it pertains to inversions in an effort to make such transactions more difficult and less lucrative for US corporations. In a very aggressive stance, the new rules took effect immediately.

In effect, these aggressive new rules by the Treasury represent just another job-killing Executive Order by the president, since he no doubt approved them. As such, these new rules are almost certain to be challenged in court. Even if they stand, it remains to be seen if the new and complicated Treasury rules will work.

Most Republicans and even some Democrats agree that the reason more US corporations are increasingly considering tax inversion is because the US corporate tax rate is simply too high. In addition, our tax code is far too complex and needs to be broadly reformed.

President Obama and liberals in Congress refuse to admit that US corporations are in business to make profits for their shareholders, and patriotism is not really an issue here, especially when inversion is perfectly legal.

The easiest way the president could stop tax inversions would be to declare a moratorium on the double taxation for overseas profits. These profits, which are estimated at up to $2 trillion, could be quickly repatriated to the US. But that is not an option for this president.

So much for the issues related to tax inversions. Now, let’s tackle the problem of the US corporate tax rate of 35% at the federal level, which is harmful for all of us.

How the 35% Corporate Tax Rate Stifles the Economy

A new international ranking shows that the US tax burden on corporations is close to the highest in the industrialized world. The non-partisan, widely-respected Tax Foundation recently launched a new global benchmark, the “International Tax Competitiveness Index.”

According to the Foundation, the new Index measures “the extent to which a country’s tax system adheres to two important principles of tax policy: competitiveness and neutrality.”

A competitive tax code is one that limits the taxation of businesses and investment. Since capital is mobile and businesses can choose where to invest, tax rates that are too high “drive investment elsewhere, leading to slower economic growth” in the US, as the Tax Foundation puts it.

By neutrality the Foundation means “a tax code that seeks to raise the most revenue with the fewest economic distortions. This means that it doesn't favor consumption over saving, as happens with capital gains and dividends taxes, estate taxes, and high progressive income taxes. This also means no targeted tax breaks for businesses for specific business activities.”

So-called “Crony Capitalism” that rewards the likes of green energy companies with lower tax bills, while imposing higher bills on other firms, is political policy that misallocates capital and reduces economic growth.

The new International Tax Competitiveness Index takes into account more than 40 tax policy variables. And the inaugural ranking puts the US at 32nd out of 34 industrialized countries in the Organization for Economic Cooperation and Development (OECD).

The new International Tax Competitiveness Index takes into account more than 40 tax policy variables. And the inaugural ranking puts the US at 32nd out of 34 industrialized countries in the Organization for Economic Cooperation and Development (OECD).

With the developed world’s highest corporate tax rate at 40%-42%including state and local levies, plus a rare demand that money earned overseas should be taxed as if it were earned domestically, the US is almost in a class by itself. It ranks just behind Spain and Italy at #32. Only Portugal and France were worse than the US, and these two countries are governed by avowed socialists.

The Tax Foundation benchmark compares developed economies with large and expensive governments, but the US would do even worse if it were measured against the world’s roughly 190 countries. The accounting firm KPMG maintains a corporate tax table that includes more than 130 countries, and only one has a higher overall corporate tax rate than the US.

The new ranking from the Tax Foundation is especially timely coming amid the new Treasury rules to punish companies that move their legal domicile overseas in order to be able to reinvest future profits in the US without paying the punitive American tax rate. If they succeed, the US could fall to dead-last on next year’s ranking. Now there’s a second-term legacy project for the President!

The new Index also suggests taxation is a greater burden on business in the US than in countries that American liberals have long praised as models of enlightened big government. Finland, Germany, Norway and Sweden, with their large social safety nets, all finish in the top 20 on the new Tax Foundation ranking. The United Kingdom manages to fund socialized medicine while finishing 11 spots ahead of the US.

Liberals argue that US corporate tax rates don’t need to come down because they are below the level when Ronald Reagan came into office. But unlike the US, the world hasn’t stood still. Reagan’s tax-cutting example ignited a worldwide revolution that has seen waves of corporate tax rate reductions.

The US last reduced the top marginal corporate income tax rate in 1986. But the Tax Foundation reports that other countries have reduced "the OECD average corporate tax rate from 47.5% in the early 1980s to around 25% today."

This is also a message to self-styled conservative “reformers” who lecture that today’s economic challenges aren’t the same as they were under Reagan, but propose to do nothing about the destructive US corporate tax code. They’re missing what could be the single biggest tax boost to economic growth and worker incomes. Abundant economic research over the years has shown that higher corporate taxes lead to lower wages.

Rather than erecting an iron tax curtain that keeps US companies from turning to tax inversions, the White House and Congress should enact reform that invites more US businesses to stay here and more foreign companies to relocate to America.

Obamacare Architect: 75 Years is Long Enough to Live

In my blog last week, I wrote about a controversial article written by Dr. Ezekiel Emanuel, one of the original architects of Obamacare (and brother of Chicago mayor Rahm Emanuel). Since my blog appeared last Thursday, Dr. Emanuel’s piece has gotten a lot of attention, so I want to revisit this topic today.

While Dr. “Zeke” Emanuel no longer works for the Obama administration, he nonetheless made news recently with his controversial editorial entitled “Why I Hope to Die at 75.” This editorial was first published in The Atlantic online magazine on September 17.

Basically, Dr. Emanuel (age 57) says that once he reaches the age of 75, he will forego all medical treatment and diagnostic tests and let nature run its course. “SEVENTY-FIVE. That’s how long I want to live: 75 years.” You might be thinking, “So what?” Who cares what some liberal kook may be saying?

Emanuel contends that his decision to forego medical treatment at age 75 is a “personal decision.”However, there is no question in my mind that he is raising this issue – that the government should consider the idea of ending healthcare at age 75 – to a level of national discourse in the ongoing evolution of Obamacare.

This is where the national debate on Emanuel’s article has focused: The question is whether Emanuel’s decision is really just his own personal intention; or is it a veiled policy recommendation for Obamacare?

Based on the large response we got from my readers, most think it was the latter, that the former architect of Obamacare made this “personal decision” public for the purpose of having it considered by those who run the Affordable Care Act. I obviously agree and so do a lot of others. I have a few good articles that debunk Dr. Emanuel’s twisted idea in SPECIAL ARTICLES below.

As always, a few of my liberal readers blasted me for suggesting that Emanuel wants his controversial message to become a part of the national discourse on healthcare. Basically, they argue that this was just a personal decision, and I’m a right-wing fear monger. That’s what they usually say when the truth comes out!

Wishing you healthcare to 75 and beyond,

Gary D. Halbert