IN THIS ISSUE:

1. Fed Reduces Economic Forecasts Through 2017

2. Could the Economic Outlook Be Even Worse?

3. US Household Net Worth Hits a Record High

4. Is the Economy Finally Turning the Corner?

5. 2Q GDP Report Due on Friday Expected to be Upbeat

Overview

The Fed’s policy committee announced last Wednesday that it will end its massive QE bond buying program at the end of next month, thus paving the way for the first Fed funds rate increase sometime next year. This was not a surprise. The Fed’s gargantuan balance sheet will peak near $4.5 trillion in Treasury and mortgage-backed bonds at the end of October.

What was surprising in the Fed’s data release last Wednesday was the downward revisions to its economic forecasts for 2014, 2015 and 2016. Furthermore, in its first-ever forecast for 2017, the Fed expects GDP growth of only 2.3% to 2.5% that year. In the wake of the Fed’s forecast downgrades last week, private economists are revising their estimates lower as well.

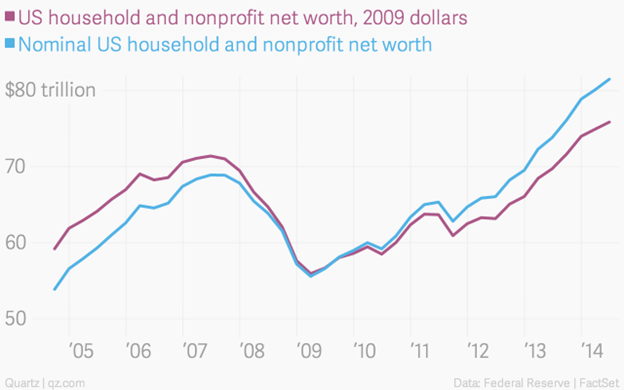

On the bright side, Americans’ combined wealth posted a new high in the 2Q, a development that mightshift the economy into a higher gear. The net worth of US households and nonprofit organizations rose about $1.4 trillion between April and June to a record $81.5 trillion, according to a new report released by the Fed last Thursday.

This Friday, we get the latest estimate of 2Q GDP. In late August, the government estimated that the economy grew by a stronger than expected 4.2% (annual rate) in the 2Q. The pre-report consensus for Friday’s report suggests another jump to 4.6% in the final estimate. Most forecasters attribute the strong 2Q reading to the severe winter weather in the 1Q that pushed many activities into the April-June quarter. In other words, the 2Q was a “catch-up” period, and most economists expect slower growth for the second half of this year.

Finally, I offer three recommendations to kick-start the economy at the end of today’s E-letter. I trust that most clients and readers would heartily agree with me. Unfortunately, the current occupant of the White House does not.

Fed Reduces Economic Forecasts Through 2017

The Fed Open Market Committee (FOMC) concluded its latest policy meeting last Wednesday and, as expected, voted to halt its enormous “quantitative easing” program at the end of October, according to its official policy statement.

Yet even though QE will end by October 31, the Fed maintained that it will be a “considerable time”before the first Fed funds rate hike sometime next year. For reasons unknown to me, many in the financial media thought the Fed would hint at a rate hike considerably sooner than the middle of next year. It didn’t.

With all the attention focused on whether the Fed would signal an earlier time for the first rate hike, some analysts failed to notice the Fed’s downgrades to its economic forecasts that accompanied the official policy statement. The Fed reduced its economic projections for 2014, 2015 and 2016 – and offered its first forecast for 2017, which was also disappointing.

The FOMC revised its economic projections to the downside from its most recent projections issued after the June policy meeting. The Fed now forecasts US Gross Domestic Product to grow as follows (annual rates), as compared to what they said in June:

| 2014 | 2015 | 2016 | 2017 |

| 2.1-2.3% June | 3.0-3.3% June | 2.5-3.0% June | n/a |

| 2.0-2.2% Sept | 2.6-3.0% Sept | 2.6-2.9% Sept | 2.3-2.5% Sept |

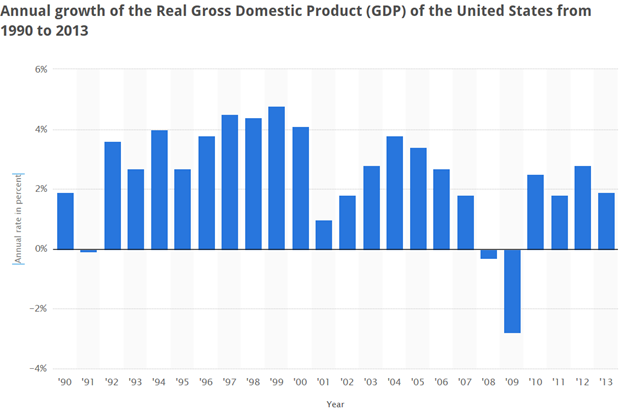

This is the second time this year that the FOMC downgraded its economic forecasts. If their forecasts are anywhere near accurate, our anemic economic growth will continue for several more years. For 2014, the Fed now expects GDP growth of only 2.0% to 2.2%, down from 2.1%-2.3% in June. And this is despite the nice pop in GDP to 4.2% in the 2Q.

The Fed’s largest downward revision in its annual forecasts was for 2015 as it now expects GDP growth of only 2.6% to 3.0%, down from 3.0%-3.3% in its June forecast. So much for the economy shifting into a significantly higher gear next year.

As you can see in the chart above, the last time that the US economy grew at an annual rate above 3% was in 2005. Now the Fed forecasts that growth will be at 3% or lower through at least 2017. Let’s hope the Fed is wrong but sadly, such long-term economic forecasts are often too optimistic.

Could the Economic Outlook Be Even Worse?

The latest cliché to describe our struggling economic recovery is “secular stagnation,” a term reportedly advanced by former Treasury Secretary Lawrence Summers. The term secular stagnation is a suggestion that our economy is caught in a prolonged period of below-trend growth that may continue for at least several more years. But why?

In part, this reflects the Baby Boomers’ retirement, which will reduce the expansion of the labor force. Baby Boomers are those estimated 76 million Americans who were born between 1946 and 1964. Baby Boomer retirements are now estimated at 10,000 per day, and that number is expected to continue for at least a decade (or longer as life expectancy increases).

Older Americans have been retiring from the labor force for as long as records have been kept. However, because of the magnitude of the Baby Boomer generation, more older Americans will be leaving the workforce than younger folks will be joining it over the next decade. As a result, the labor force participation rate will continue to decline, or at best remain stagnant.

As a result, Northwestern University scholar and economist Robert Gordon contends that mainstream economic growth predictions are wildly optimistic. His own calculations are more restrained. By 2024, he projects that annual Gross Domestic Product will be nearly $2 trillion lower (almost 10% less) than currently projected by the Congressional Budget Office (CBO).

The gist of Gordon’s argument is that the nation’s productive capacity – what economists call “the supply side” – will expand only slowly. It won't keep up with the stronger consumer demand projected in other forecasts.

As a result, inflationary pressures will be higher and GDP lower. “The economy is on a collision course between demand-side optimism and supply-side pessimism,” Gordon asserts.

Although Gordon’s analysis addresses economics primarily, the underlying issues are political. Since World War II, advanced democracies – Japan, Western Europe and the US – have depended on strong economic growth. It was a political narcotic: Wages and living standards rose, generating taxes to pay for generous “social safety nets” and rising welfare benefits.

The financial crisis in 2008 shattered that complacency, and the prospect is for years of modest economic growth or, in Europe, possibly nonexistent growth. How will political systems cope? Will “class warfare” intensify as groups battle harder for bigger shares of a stagnant pie? Will racial, ethnic, religious, generational and ideological conflicts worsen?

No one denies the reality of slower growth. The question is, how much slower? From 1950 to 1973, the US economy grew almost 4% annually. From 1974 to 2001, growth averaged slightly more than 3% a year. By contrast, the CBO’s latest growth projection for the next decade is only 2.1% annually, and Gordon’s estimate for the same period is a meager 1.6% per year.

Retiring Baby Boomers are a big drag on growth. Their exodus from the labor force means that millions of younger workers aren’t expanding the labor force. They’re simply replacing retirees. So, labor force growth is a third or less of the post-1950 average, says Gordon.

More controversial is productivity. Among economists, Gordon is a prominent techno-pessimist. He believes the burst of higher productivity from 1996 to 2004 was a one-time event reflecting the “invention of the Internet, web browsing and e-commerce.” Of course, there are many others who disagree.

Exclude these years, Gordon says, and productivity has grown only slowly since the early 1970s, too long a stretch to ignore. He doesn’t expect much change, although some other economists are more optimistic.

Who's right? All the anecdotal evidence seems against Gordon; hardly a day passes, it seems, without a new digital product or a corporate shakeup intended to enhance productivity. But statistics are firmly on his side – since 2010, annual productivity gains have averaged less than 1%.

Nevertheless, the economy can temporarily exceed its potential growth rate by absorbing the unemployed and idle business capacity. But we are approaching an inflection point, and Gordon’s projections are at least plausible.

Of course, they’re subject to many influences. Additional business investment could improve productivity. A tight job market, should that occur, could raise wages and labor force participation. But who knows when that will happen.

The slow recovery from the Great Recession has not solved all our problems. We need to improve our long-term prospects. This is admittedly difficult. Economic growth is too complex a process to be easily manipulated by a few policy changes, even if they are desirable.

But could prolonged economic sluggishness turn the economy into a zero-sum game, where one group’s gain is another’s loss? That’s not a formula for social peace. We’ll have to see.

US Household Net Worth Hits a Record High

Fortunately, not all of the economic news is bad. Americans’ combined household wealth posted a new high in the 2Q, allowing some consumers to ramp-up spending and borrowing – a development that mightshift the economy into a higher gear.

The net worth of US households and nonprofit organizations – the value of homes, stocks and other assets minus debts and other liabilities – rose apprx. $1.4 trillion between April and June to $81.5 trillion, the highest level on record, according to a report by the Federal Reserve released last Thursday.

Overall household borrowing rose at an annualized 3.6% pace in the 2Q, the fastest rate since the 1Q of 2008. Much of that was driven by a sharp increase in consumer credit, including student loans, which grew 8.1%, stronger than the previous quarter’s 6.5% pace. Even mortgage debt grew 0.4%, following two straight quarters of shrinking.

Is the Economy Finally Turning the Corner?

Economists hope that rising asset values and falling unemployment will eventually lead to more consumer spending, which accounts for apprx. 70% of economic output. Yet we should keep in mind that rising wealth can help the economy only so much. Most of the nation’s wealth gains go to the affluent who tend to own stocks and real estate and save their money, as opposed to spending it. This reduces the benefits for the overall economy.

Last quarter was a case in point: The S&P 500 Index rose about 5%, and real estate values also improved modestly. The value of stocks and mutual funds owned by US households rose $1 trillion last quarter, and Fed data show that the value of residential real estate grew by $230 billion in comparison.

Yet another gauge of Americans’ wealth – US household net worth as a share of disposable income – remains below levels seen before the Great Recession, according to the Fed. This may have been another factor that led the Fed to downgrade its economic forecasts for the next three years.

While the US economy enjoyed a nice bounce in the 2Q (more on that below), most forecasters expect that growth has slowed in the second half of this year. As noted above, the Fed expects GDP growth of only2.0%-2.2% for this year overall. Most economists are downgrading their forecasts as well.

With the Fed’s latest downgrade to its economic forecast for 2015 to only 2.6% to 3.0% at best, followed by even weaker estimates for 2016 and 2017, it does not look like our economy has turned the corner.

2Q GDP Report Due on Friday Expected to be Upbeat

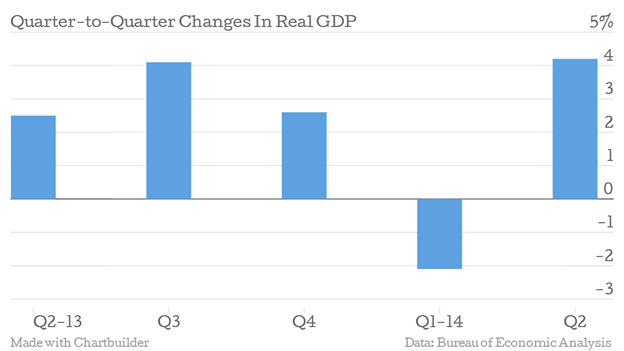

On Friday, we will get the third and final estimate of 2Q GDP growth. In late August, the Commerce Department’s Bureau of Economic Analysis (BEA) reported that 2Q GDP rose by a better than expected 4.2% (annual rate), following a decline of 2.1% in the 1Q.

The pre-report consensus for the next report on Friday is for an increase to 4.6% for the 2Q. The BEA noted that the jump in the 2Q was mainly due to a large increase in nonresidential fixed investment (plants, structures, equipment, software, etc.), which was thought to have been delayed by the severe weather in the 1Q.

Even if the economy grows by 3% in the 3Q and 4Q, which is far from certain, that would mean growth of only 2.1% for the year overall. That is right in-line with the Fed’s latest estimate.

What the economy needs to get back on-track is more consumer spending. In the previous GDP estimate in late August, the BEA said that consumer spending increased only 2.5% (annual rate) in the 2Q, which is well below the 3.3% pace on average since the Great Depression, and even further behind the rate normally seen at this point in past recoveries.

Unfortunately, the US appears stuck in a slow growth trajectory indefinitely. What would it take to get us on the fast track? I’m no economist, but I have a few suggestions:

- Last week marked the sixth anniversary of TransCanada’s application to build the Keystone XL Pipeline. Approve it immediately! At the same time, remove other burdensome federal restrictions on the development, refining and export of abundant US energy supplies. And open up more federal land for exploration.

- Allow US companies to repatriate overseas profits without a tax penalty. We are the only major country that taxes overseas profits that have already been taxed by the countries in which they are earned. This could mean as much as $2 trillion flowing back to the US.

- Finally, how about a simplified US tax code for everyone?

I could go on and on but, unfortunately, our president opposes all of these ideas.

Very best regards,

Gary D. Halbert