1. Why Gilead Is The Most Exciting Growth Opportunity In 2014

1. Why Gilead Is The Most Exciting Growth Opportunity In 2014

Introduction

Earnings drive stock price in the long run and Gilead Sciences Inc (GILD) is entering a remarkable period of what could only be called astounding future earnings growth. This has not gone unnoticed by the market, as the stock price has been on a steady ascent for the past several months.

Furthermore, there have been numerous articles published in the media discussing its future prospects and investment appeal. Therefore, I will not rehash what has already been written about this potentially remarkable investment opportunity, but I will offer the following several links to articles I found most interesting:

Gilead: More Good News For This Biotech Juggernaut

Understanding The Excitement That Surrounds Gilead

A Re-Analysis Of Gilead After Q2 Results And The Early Idelalisib Approval

Gilead Sciences Q2 2014: All Is Good, More To Come At Medical Conferences Later This Year

With this article I will offer a comprehensive fundamental review that I believe supports my view that in spite of its recent price run-up, Gilead remains a reasonably valued and exciting opportunity for those investors seeking maximum capital appreciation. However, I will qualify this position by stating that my view is long-term. In other words, there is always the possibility that current price may retreat over the short-run. But, in the long run earnings determine market price and I believe the future earnings potential of Gilead is clear and well-defined.

Short Company Description

The following short business description on Gilead Sciences Inc provided courtesy of S&P Capital IQ:

“Gilead Sciences, Inc., a research-based biopharmaceutical company, is engaged in the discovery, development, and commercialization of medicines in areas of unmet medical need. The company has operations in North and South America, Europe and Asia-Pacific.

The company’s primary areas of focus include human immunodeficiency virus (HIV), liver diseases such as chronic hepatitis B virus (HBV) infection and chronic hepatitis C virus (HCV) infection, oncology/inflammation and serious cardiovascular and respiratory conditions.

In the liver diseases area, the company received approval from the U.S. Food and Drug Administration (FDA) of new drug application (NDA) for Sovaldi (sofosbuvir 400 mg). Sovaldi is a once-daily oral nucleotide analog polymerase inhibitor for the treatment of HCV infection as a component of a combination antiviral treatment regimen.

The company also received approval of Tybost (cobicistat) and Vitekta (elvitegravir 85 mg and 150 mg), each a component of Stribild, from the European Commission. In the oncology/inflammation area, the company filed for FDA and European Medicines Agency (EMA) marketing approval of idelalisib (formerly GS-1101), an investigational, targeted, oral inhibitor of PI3K delta, for the treatment of patients with refractory indolent non-Hodgkin’s lymphoma (iNHL) and relapsed chronic lymphocytic leukemia (CLL). The company also continued to advanced research and development pipeline, with approximately 200 active clinical studies in 2013, of which approximately 60 were in Phase 3 clinical trials.”

Earnings Operating History

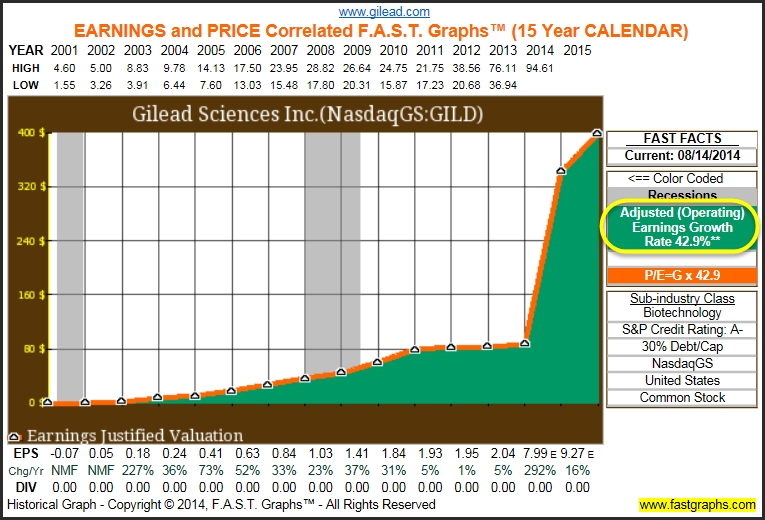

Up through 2013 Gilead was a consistently fast-growing biotechnology company averaging 42.9% per annum earnings growth. However, as the following graph reveals, earnings growth had significantly slowed down since 2011. This simultaneously led to a very low valuation. On the other hand, the company’s stock price went on a rapid ascent in 2013, perhaps in anticipation of what was soon to come.

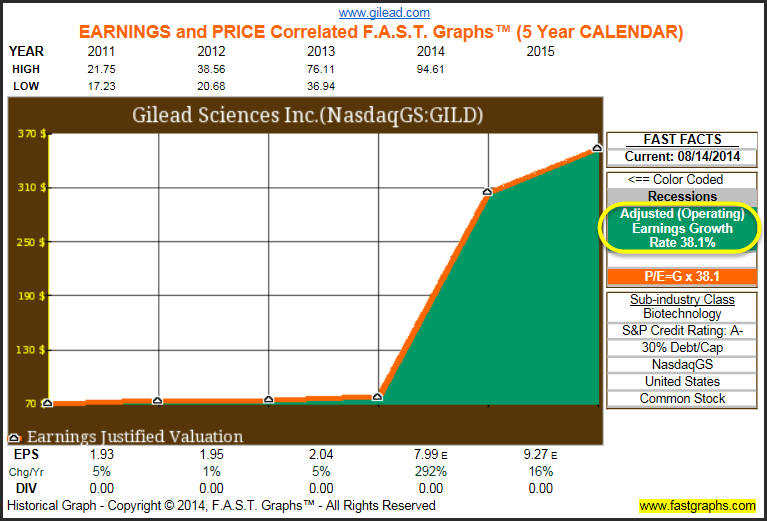

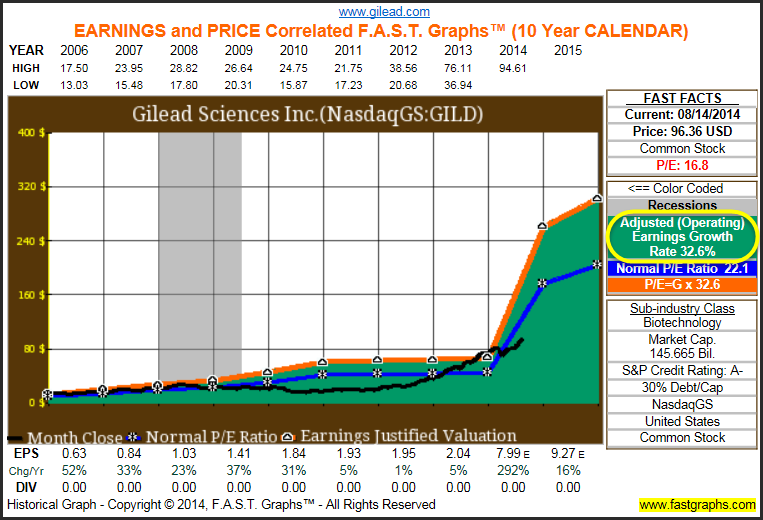

The following earnings only FAST Graphs™ on Gilead Sciences Inc illustrate the dynamic nature of a company’s earnings per share growth over different time periods. Earnings growth is a dynamic calculation that varies when graphed from one timeframe to the next. Consequently, it’s important to review several timeframes when evaluating a company’s historical earnings growth rate. The following 15 calendar year, 10 calendar year, 7 calendar year and 5 calendar year graphs illustrate that although Gilead’s earnings growth has been consistently high over the years, it became explosive for 2014 and beyond (see earnings growth rates circled in yellow). Note: growth rates include all estimates on the graph whether calendar or fiscal year.

Earnings (Operating) History 15-Year

Earnings Operating History 10-Year

Earnings Operating History 7-Year

Earnings Operating History 5-Year

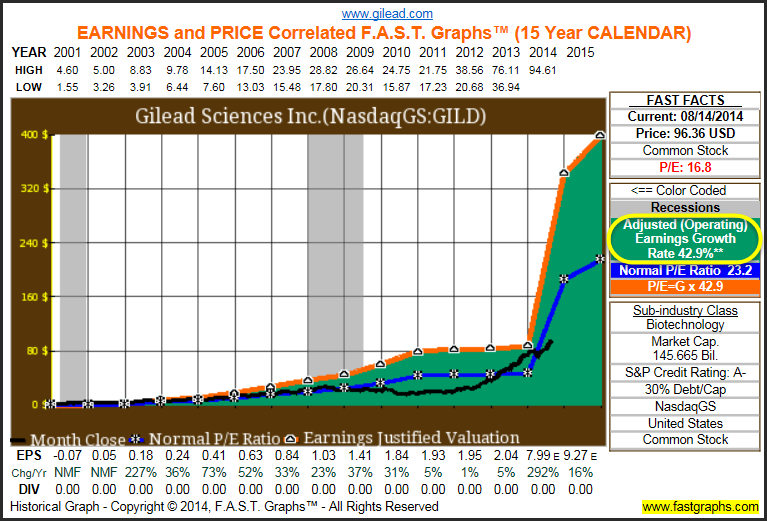

Current 15-Year Earnings and Price Correlated FAST Graph (with Normal P/E Ratio)

Current 10-Year Earnings and Price Correlated FAST Graph (with Normal P/E Ratio)

The key takeaway from the above earnings and price correlated graphs is that Gilead’s quantum leap in earnings growth has not yet been fully credited by the market. Consequently, based on earnings expectations the stock appears to represent a compelling long-term investment.

15-Year Historical P/E Ratio Trend

The dark blue line reflects the fiscal year-end P/E ratio for Gilead Sciences Inc since 2008 (the right scale on the graph). Clearly we see that Gilead’s P/E Ratio had been consistently dropping due to lower-than-average earnings growth, and then began rising again in 2012 and 2013. However, the current explosion in earnings growth has once again brought the P/E Ratio on Gilead back into attractive valuation levels.

Performance

Historical performance is functionally related to earnings growth achievement and starting valuation. Consequently, when performance is properly measured, it is imperative that starting valuation be considered in conjunction with earnings (and dividends, if any) growth.

A high beginning valuation will reduce capital appreciation; a low beginning valuation will enhance capital appreciation. When a company’s beginning valuation is in alignment with earnings, capital appreciation will be highly correlated with the company’s earnings growth rate.

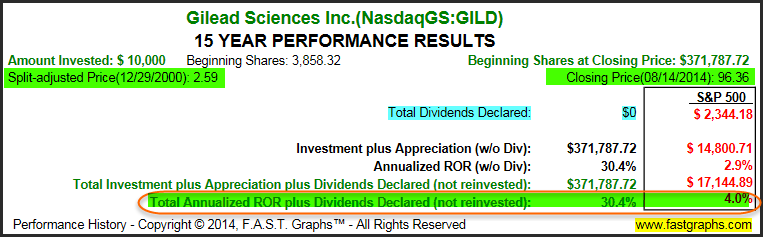

15-Year Performance: From Beginning Undervaluation

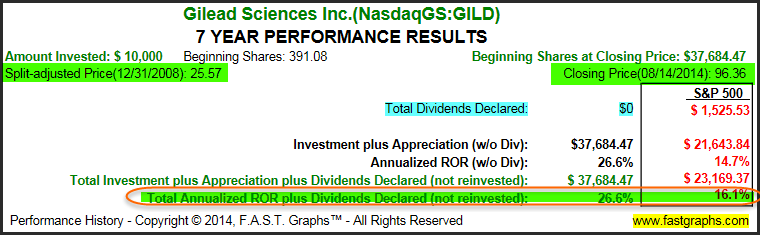

7-Year Performance: From Beginning Undervaluation

Earnings Forecasts

The “Estimated Earnings and Return Calculator” provides several specific future year’s earnings forecasts. Specific near-term earnings forecasts (varies from two to four years) are provided to include the number of analysts reporting to S&P Capital IQ (yellow and green highlights). Additionally, a long-term (three to five year) growth rate is also provided (orange highlights). The specific number of analysts offering the long-term forecast is found in the FAST FACTS box (orange circle).

Therefore, we highly recommend placing more credence on the near-term forecasts because they are likely to be more accurate. Moreover, near-term forecasts tend to include a greater number of analysts in the consensus.

The graph below reports consensus earnings of $7.99 for fiscal 2014 according to 26 analysts reporting to S&P Capital IQ followed by $9.27 for fiscal 2015 according to 27 analysts and $10.00 for fiscal 2016 according to 23 analysts. These near-term forecasts for earnings growth indicate that Gilead is extremely undervalued at current levels.

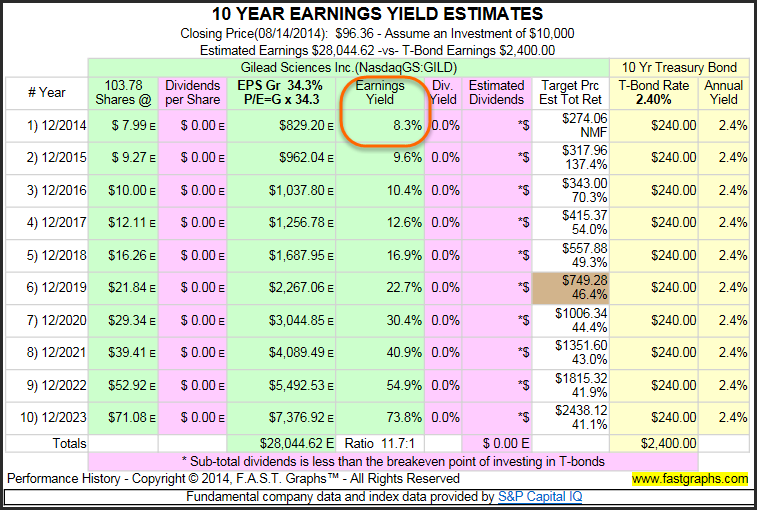

Earnings Yield

Shareholders in publically traded companies, even though they are passive owners, can expect to be rewarded for their investment in proportion to the company’s earnings capacity. Consequently, the earnings yield calculated from current and future (expected) earnings represents an important valuation consideration.

Based on consensus estimates for 2014’s earnings, Gilead offers a current earnings yield of 8.3%. However, since investors are always buying the future, the potential for high earnings yield is extremely robust, assuming earnings growth continues.

FUNdamentals: A Deeper Look

Utilizing FUN Graphs (fundamental underlying numbers), the following important fundamental metrics and key ratios are offered to provide a deeper look into the company’s financial strength and current valuation.

Balance Sheet/Income Statement

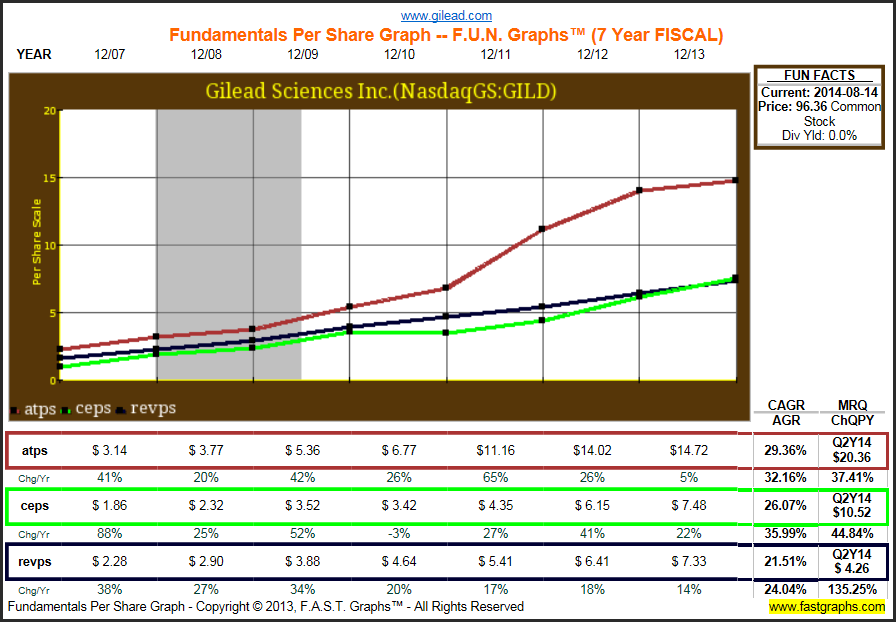

The following balance sheet items are offered to reveal the financial health of the company. They include assets per share (atps), cash and equivalents per share (cashps) and common equity or book value per share (ceps).

The following income statement item, revenues per share (revps) is offered to reveal the consistency of revenue growth.

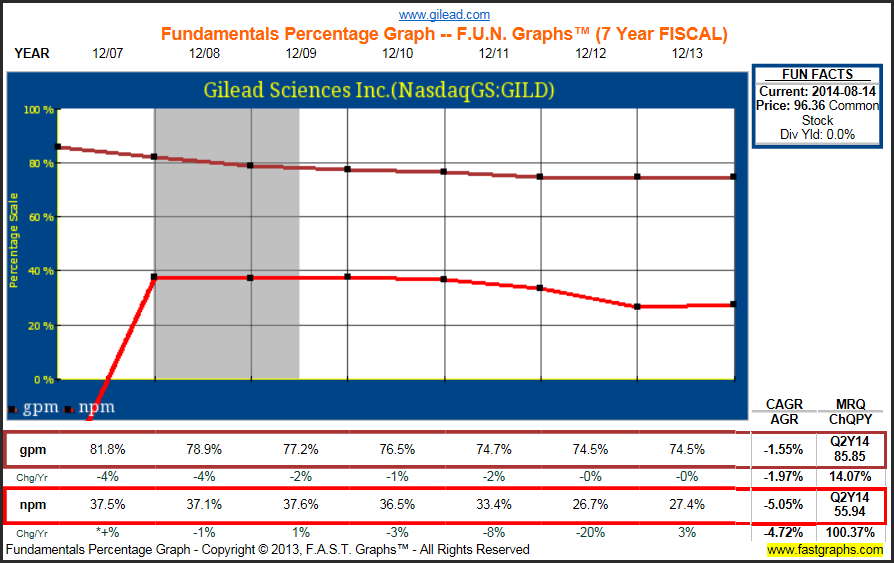

Gross and Net Profit Margins

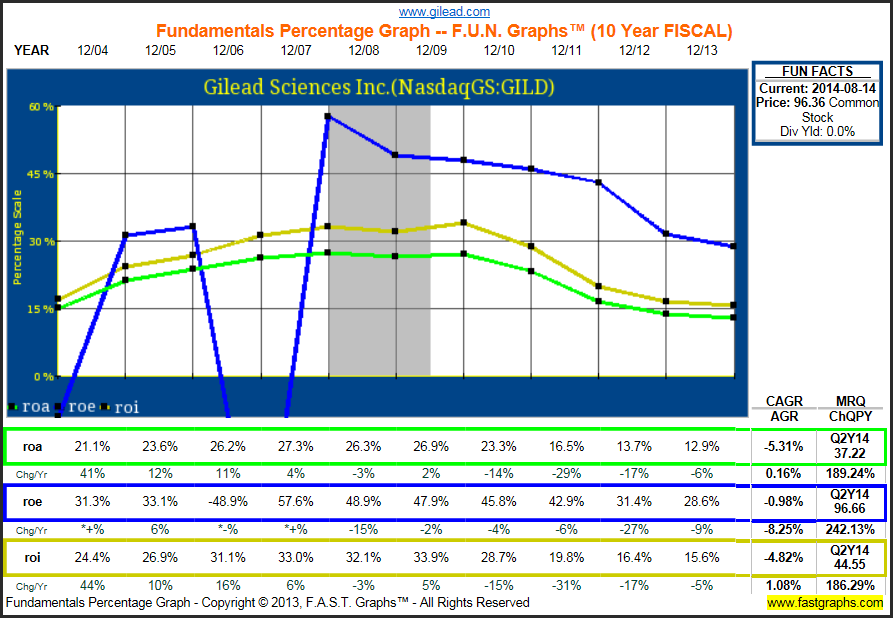

Return on Assets, Equity and Invested Capital

Key Liquidity Ratios

Liquidity is an important consideration when evaluating a business. The primary liquidity ratio that prudent investors look to is the current ratio (cr).

Additionally, the current ratio (cr) measures the company’s ability to retire its short-term liabilities (debt and payables) with its short-term assets (cash, inventory and receivables). This important ratio is often referred to as the liquidity ratio and is a good indicator of a company’s ability to remain a going concern. Gilead’s current ratio in the most recent quarter (MRQ) was a very healthy 2.5.

Since many investors are concerned about price volatility, we have included five-year beta as an additional key ratio. A beta of one or lower is considered ideal relative to risk. On the other hand, a beta above one may also indicate the potential for above-market long-term performance.

Additional Key Valuation Ratios

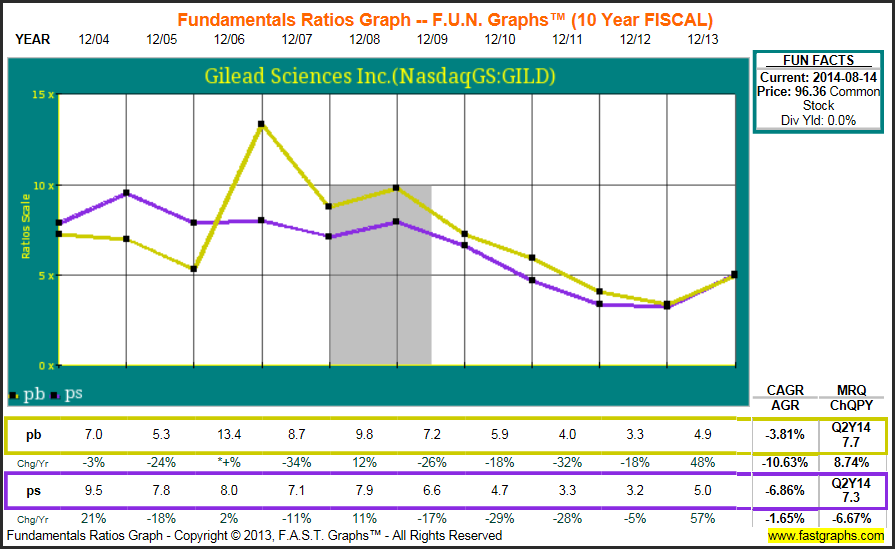

Two important valuation ratios that investors consider are price to book value (pb) and price to sales (ps). When considering both of these valuation ratios, the lower the better.

Key Management Shareholder-Friendly Metrics

Many investors consider a company’s shareholder-friendliness based on its dividend policy and/or share buyback policy. A consistent record of paying dividends, and better yet, increasing the dividend are considered positive attributes of management.

However, many companies in the growth phase may consider it more profitable to retain their cash to fund growth. Consequently, the lack of a dividend does not necessarily indicate that management is not shareholder-friendly.

Regarding share buybacks, they are considered friendly because they are anti-dilutive. However, share buybacks should only be considered shareholder-friendly when management is buying back shares when stock price is sound or undervalued.

Summary and Conclusions

Investors are often deterred from investing in a stock when its price reaches an all-time high as it recently has in Gilead. However, those same investors often fail to recognize that price and valuation are not the same. In the case of Gilead, its current valuation remains quite attractive in spite of its recent price rise because of 2014’s explosive growth of earnings primarily attributed to the recent approval and sales of Sovaldi. However, there are additional pipeline opportunities that suggest future earnings growth to continue, albeit at lower rates than 2014. Consequently, based on valuation, Gilead appears to be a very attractive growth story for at least the next couple of years. In other words, it’s not too late.

Moreover, most of the risks associated with Gilead’s future earnings power have been reduced based on recent reports and rulings. The following articles from The Wall Street Journal, Barron’s and MarketWatch support this view:

Gilead Sciences: Arbitrator Removes ‘Doomsday Scenario’

English Drug Panel Backs Hepatitis Drug at a Discount

Gilead wins critical Sovaldi legal fight, Roche finds consolation

Disclosure: Long GILD at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.