Re-regulation has diminished market liquidity

July 25, 2014

Four years ago this month, the Dodd-Frank Wall Street Reform and Consumer Protection Act (DFA) was signed into law. It took up more than 3,000 pages in the Federal Register and identified 280 areas for additional rulemaking. It is arguably the most consequential piece of American financial legislation since the 1913 Federal Reserve Act.

Since I worked at the Federal Reserve when the DFA was passed, I became a convenient target for those who were concerned about the costs and corollaries of all those new rules. I tried to remind critics that the Fed did not make up the statutes, Congress did. But since the Fed was at the center of enforcing many of the new regulations, I remained the subject of scorn.

There are certainly positive things that have occurred because of post-crisis regulation, but it has also created unintended consequences. One of the casualties seems to be the level of liquidity in the bond markets, which is well down from its peaks. As a result, market swings may become more extreme, potentially raising a threat to financial stability.

It didn’t take long for the “lessons learned” papers to begin flowing after the financial crisis struck. Among the common villains in those catalogues were leverage, opacity of markets and misaligned incentives. The authors of the DFA set out to correct all of these.

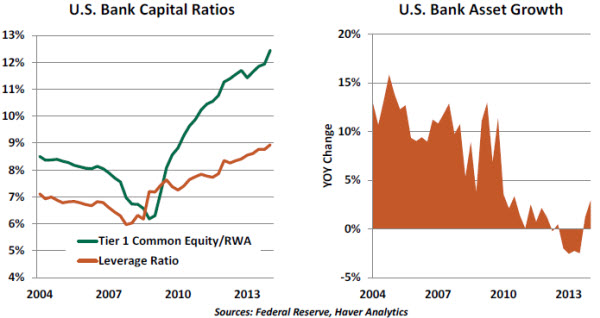

Capital was a particular focus. Insufficient reserves leave little buffer between private and public losses and can incent excessive risk-taking. The institutionalization of annual stress testing, along with new minimum capital requirements, has prompted a substantial increase in the collective equity base of the American banking industry.

One route to this improvement has been a substantial slowing in the growth rate of bank assets. Many think that credit grew too quickly in the years leading up to the crisis, so some moderation is welcome. But there is a tradeoff between capital levels and the level of financial intermediation in an economy.

The DFA and other financial re-regulation have affected not only the size of bank balance sheets but also their composition. Mortgage lending in the United States continues to lag other sectors as underwriting requirements are tightened. There are many fewer loan “warehouses,” where originators would store credits for subsequent securitization. Institutions have shifted their investment portfolios more toward Treasury securities to be prepared for new liquidity rules.  Yet no balance sheet category has felt the pinch of re-regulation more than trading books. Broker/dealers have seen their wings clipped by a series of post-crisis reforms. Positions are subject to special stress tests and require much higher levels of capital coverage. Liability for faulty underwriting has been expanded. Trader compensation can be “clawed back” if problems arise after bonuses are paid.

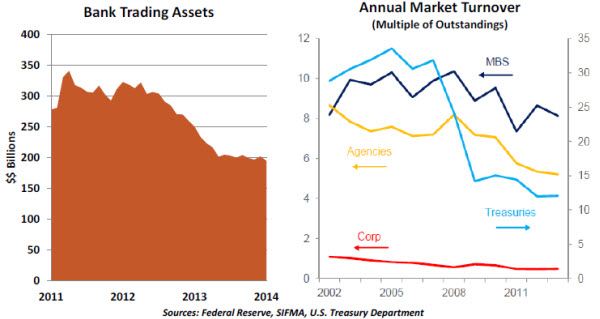

Yet no balance sheet category has felt the pinch of re-regulation more than trading books. Broker/dealers have seen their wings clipped by a series of post-crisis reforms. Positions are subject to special stress tests and require much higher levels of capital coverage. Liability for faulty underwriting has been expanded. Trader compensation can be “clawed back” if problems arise after bonuses are paid.

The single biggest change for trading activity within banks is the Volcker Rule. It is based on the premise that proprietary trading should not go on inside firms with access to the public safety net. Simple on the surface, the Volcker Rule was, nonetheless, very difficult to define. Trading departments typically hold inventory in expectation of client demand. Yet it is difficult to know where market making stops and speculation begins. Drawing the line in the wrong place could impair desirable intermediation.

By the time the Volcker Rule was finalized late last year, American banks had already shed a substantial portion of their trading assets. And as U.S. subsidiaries of foreign firms gradually become subject to the strictures of the DFA, this trend will likely continue.

When you have fewer bidders in a market, trade execution can become more difficult. The willingness of proprietary investors to take positions can serve as a useful circuit-breaker when markets are overly exuberant or depressed. Without them, volatility can be exaggerated at important turning points. Financing might become limited and its price uncertain.  The annual turnover in fixed-income instruments has been trending substantially downward since 2008, with the market for U.S. Treasury securities (the largest debt market in the world) showing an especially significant decline. We saw the consequence of this in May 2013, when Fed Chairman Ben Bernanke suggested that the Fed might begin tapering its bond purchase program. Long-term Treasury yields nearly doubled in four months, and capital shifted away from emerging markets in very sudden fashion. This experience leads some to fear the day that the Fed hints at tightening.

The annual turnover in fixed-income instruments has been trending substantially downward since 2008, with the market for U.S. Treasury securities (the largest debt market in the world) showing an especially significant decline. We saw the consequence of this in May 2013, when Fed Chairman Ben Bernanke suggested that the Fed might begin tapering its bond purchase program. Long-term Treasury yields nearly doubled in four months, and capital shifted away from emerging markets in very sudden fashion. This experience leads some to fear the day that the Fed hints at tightening.

There are certainly substantial private pools of capital that might eventually step in where investment banks used to tread, but they have yet to embrace this role. Hedge funds, for example, operate with much lower levels of leverage and no direct access to the federal safety net. This limits the magnitude of their positioning, relative to what broker/dealers could hold in their heyday.

Regulation runs in cycles, and it is not unusual for mid-course corrections to be offered if outcomes are suboptimal. The “problem” of proprietary trading may have been solved, but only at the potential cost of market function. Let’s hope that legislators who enthusiastically supported DFA are ready to act with equal zeal to ensure the healthy functioning of fixed-income markets

Federal Budget Estimates: Better, But Not Good

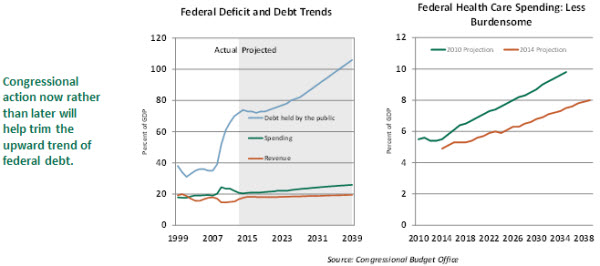

Last week, the Congressional Budget Office (CBO) published the long-term outlook for the U.S. federal budget. If current laws governing taxes and spending go unchanged, the federal budget deficit will hover around 3% of gross domestic product (GDP) from 2015 – 2018. However, in the years after, the deficit is forecast to widen. As a result, federal debt held by the public as a percent of GDP is on track to reach levels last seen after World War II. Federal government revenues would increase relative to GDP in the next 25 years but noticeably more slowly than spending. The CBO estimates that revenues would grow to 19.5% of GDP by 2039, compared with a 17.5% average of the last 40 years. Federal spending, however, is projected to climb to around 26% of GDP by 2039 compared with 21% in 2013 and a 40-year average of 20.5%. This increase reflects:

- Growth in net interest payments from 2% of GDP in the past four decades to 4.5% by 2039;

- A decline in non-interest payments excluding health care and Social Security to 7% of GDP from an average of 11% of GDP in the past 40 years; and

- A large jump in federal spending on Social Security and the federal government’s major health care programs.

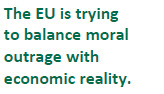

Expenditures on the federal government’s health care programs ¬– Medicare, Medicaid, the Children’s Health Insurance Program and subsidies for health insurance purchased under the Affordable Care Act – are projected to climb from 4.9% of GDP to 8% by 2039. The latest 25-year projections are mostly unchanged from the 2013 exercise.

But it is noteworthy that the CBO’s projections of federal health care spending are significantly lower than its projections from 2010 after Congress passed the Affordable Care Act. The CBO projects total federal health care spending will stand at 7.5% of GDP by 2035 – about 2.3 percentage points lower than the 2010 estimate. A reduction in Medicare spending is largely the reason. Actual Medicare spending has shown a mild deceleration in recent years, and this trend is expected to prevail until 2018, followed by a more-worrisome increase thereafter.

Health care spending is the biggest challenge in the battle to contain the growth of federal debt in the United States. The CBO’s latest projections are indicative of a constructive development in health care expenditures. However, there is a great deal of uncertainty to contend with. The impact of new technology, new medical procedures and innovations in the delivery of health care services could change the trajectory of costs.

There is considerable uncertainty around these outcomes. The CBO estimates that if mortality rates, productivity, interest rates and health care spending move modestly in one direction or the other, the publicly held federal debt-GDP ratio in 2039 could be as low as 75% – about where it is today – or as high as 160%.

The baseline scenario estimates that publicly held federal debt would move up to 106% of GDP over 25 years. The United States found itself in a similar situation after World War II. Back then, the ratio declined in a steady manner as the U.S. economy roared in the postwar period. Forces are not in place now for a repeat performance, particularly if Congress fails to act soon. Cuts in spending and an enhanced tax revenue stream will be less burdensome if suitable steps are taken sooner rather than later.

Checking Putin

I wandered onto the treadmill at midday on Thursday of last week. I usually don’t pay attention to the TV monitors arrayed around the gym, since it takes all of my concentration to cheat the aging process and complete my workout. But I looked up and noticed that all the networks were covering the same story: the downing of Malaysia Airlines flight 17.

My first thoughts were of those lost. Our prayers go out to their friends and their families. Having worked many years for a Dutch company, I came to admire their culture of peaceful coexistence. To have innocent citizens killed in a conflict to which they were not party must be especially challenging to sensibilities in the Netherlands.

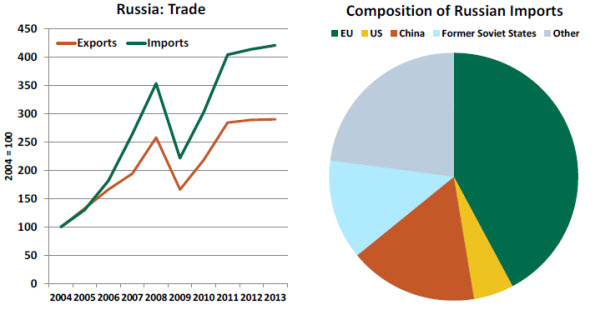

From there, I had to put on my professional hat and try to understand how this escalation of stakes in Ukraine might affect the global economy. Earlier this summer, the American government broadened its sanctions against Russian banks and energy companies. In the wake of the MH17 disaster, the European Union has considered following suit.  While member countries are united in their outrage, reaching consensus on new sanctions is tricky. The eurozone economy is struggling, and a further loss of commerce with Russia will not help recovery efforts. Business sacrifices must be shared evenly: if asked to forfeit financial revenue, London will certainly ask that France and Germany get tough on industrial exchanges. Compromise will take time.

While member countries are united in their outrage, reaching consensus on new sanctions is tricky. The eurozone economy is struggling, and a further loss of commerce with Russia will not help recovery efforts. Business sacrifices must be shared evenly: if asked to forfeit financial revenue, London will certainly ask that France and Germany get tough on industrial exchanges. Compromise will take time.

Hopefully, any sacrifices will be modest and short-lived. Russia’s economy is already in deep recession, and it risks losing some of the significant trade gains it has made over the past 20 years. There are reports of capital moving out of the country in huge amounts. This should provide ample incentive to capitulate.

Since World War II, transnational organizations have formed to foster international commerce and cooperation, in the hope of heading off aggression. The current tension with Russia will prove a true test of whether the balance sheet is more powerful than the bayonet.