Introduction

On Monday a Wall Street Journal article reported that the hedge fund Elliott Management Corp has taken a more than $1 billion stake in EMC Corp (EMC) and revealed that it intends to petition the company to break itself apart. Elliott believes that this would unlock shareholder value. Implicit in that thesis would be the idea that EMC Corp is not receiving full value from the market. This article is offered as an in-depth analysis of the fundamental value of EMC Corp in relation to how the market is evaluating its business.

Short Company Description

The following short business description on EMC Corp provided courtesy of Capital IQ:

“EMC Corporation develops, delivers, and supports information infrastructure and virtual infrastructure technologies, solutions, and services. It operates in three segments: Information Storage, Information Intelligence Group, and RSA Information Security.

The company offers enterprise storage systems and software deployed in storage area networks (SAN), networked attached storage (NAS), unified storage combining NAS and SAN, object storage, and/or direct attached storage environments, as well as provides backup and recovery, disaster recovery, and archiving solutions.

It also offers information security solutions that are engineered to combine agile controls for identity assurance, fraud detection, and data protection, as well as security analytics and GRC capabilities; and expert consulting and advisory services.

In addition, the company provides information intelligence software, cloud solutions, and services, including EMC Documentum xCP for building business and case management solutions; EMC Captiva for intelligent enterprise capture; EMC Document Sciences for customer communications management; EMC SourceOne Kazeon for e-discovery; the EMC Documentum platform for creating, managing, and deploying business applications and solutions; and the EMC OnDemand private cloud deployment model for enterprise-class applications.

Further, it offers VMware virtual and cloud infrastructure solutions that enable organizations to aggregate multiple servers, storage infrastructure, and networks together into shared pools of capacity that could be allocated to applications as needed. Additionally, the company provides installation, professional, software and hardware maintenance, and training services.

EMC Corporation markets its products through various distribution channels, as well as directly in North America, Latin America, Europe, the Middle East, South Africa, and the Asia Pacific region. The company was founded in 1979 and is headquartered in Hopkinton, Massachusetts.”

Earnings Operating History

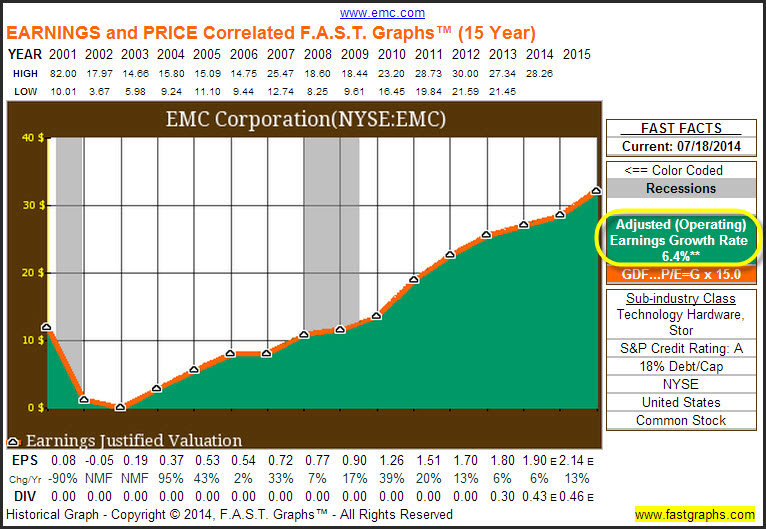

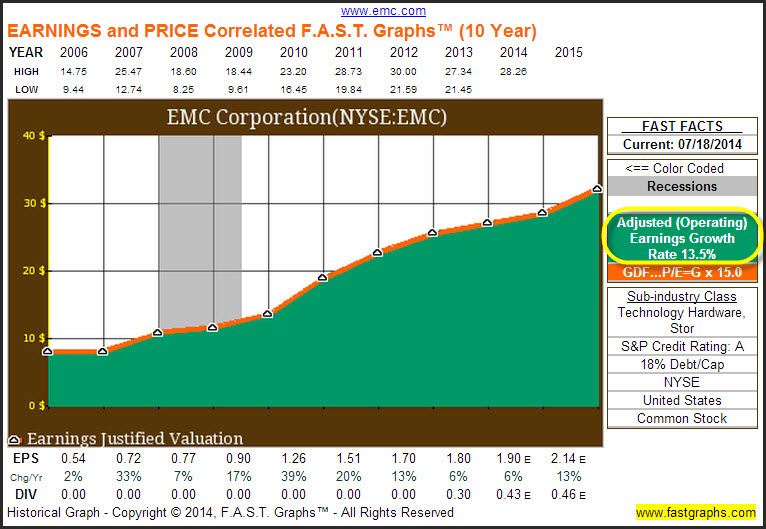

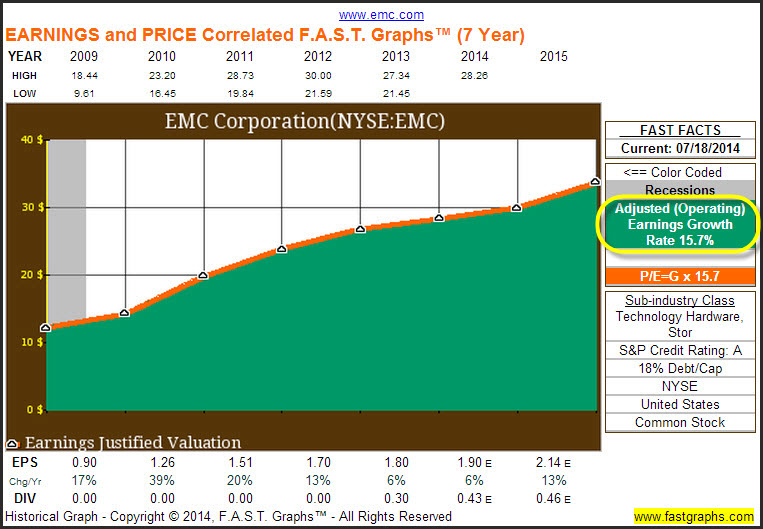

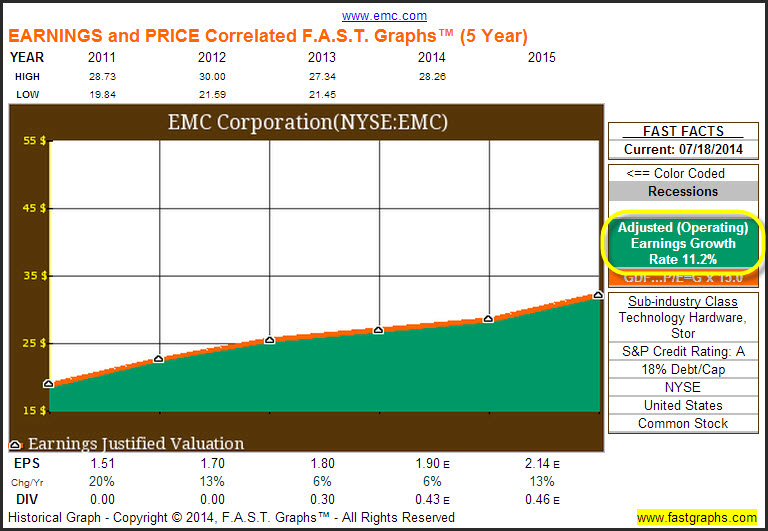

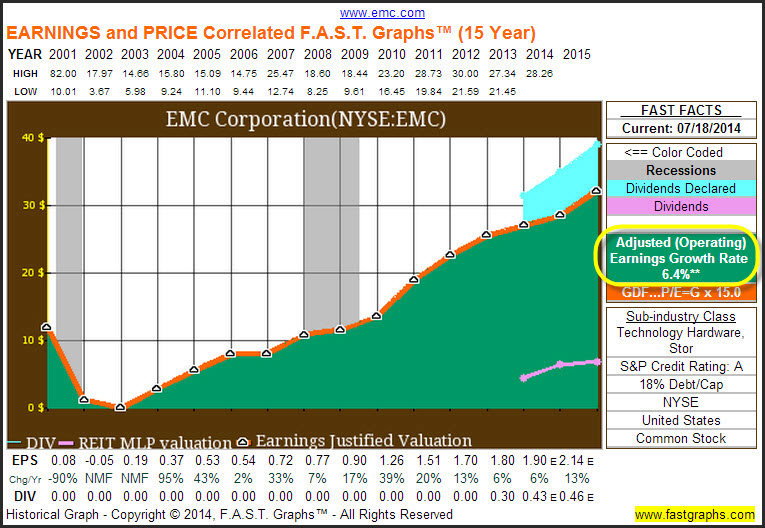

The following earnings only FAST Graphs™ on EMC Corp illustrate the dynamic nature of a company’s earnings per share growth over different time periods. Earnings growth is a dynamic calculation that varies when graphed from one time frame to the next. Consequently, it’s important to review several timeframes when evaluating a company’s historical earnings growth rate. The following 15 calendar year, 10 calendar year, 7 calendar year and 5 calendar year graphs illustrate that EMC’s earnings growth has been accelerating (see earnings growth rates circled in yellow).

Earnings (Operating) History 15-Year

Earnings Operating History 10-Year

Earnings Operating History 7-Year

Earnings Operating History 5-Year

Operating Earnings and Dividend History

The important take-away from the following earnings and dividend graph is that prior to 2013 EMC Corp was purely a growth stock. However, as revealed by the dividends paid out (blue shaded area) and plotting of dividends as a percentage of earnings (the pink line) we see that as of December 2013 the company has recently morphed into a dividend paying stock. It will be interesting to watch how future dividends are paid.

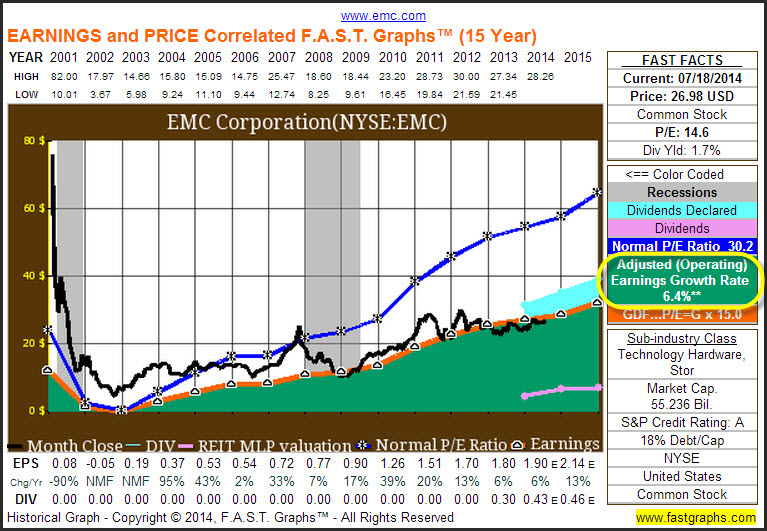

15-Year Earnings and Price Correlated FAST Graph (with Dividends and Normal P/E Ratio)

During the tech bubble that ran from 1995 to 2000 we see that EMC’s stock price was dramatically above its earnings justified valuation. Furthermore, when earnings dropped during the recession of 2001, the stock price correction was swift and severe. However, since that “tech bubble” period EMC Corp has produced a steady stream of above-average earnings growth. Additionally the normal P/E ratio was greatly skewed due to the excessive overvaluation during the tech bubble.

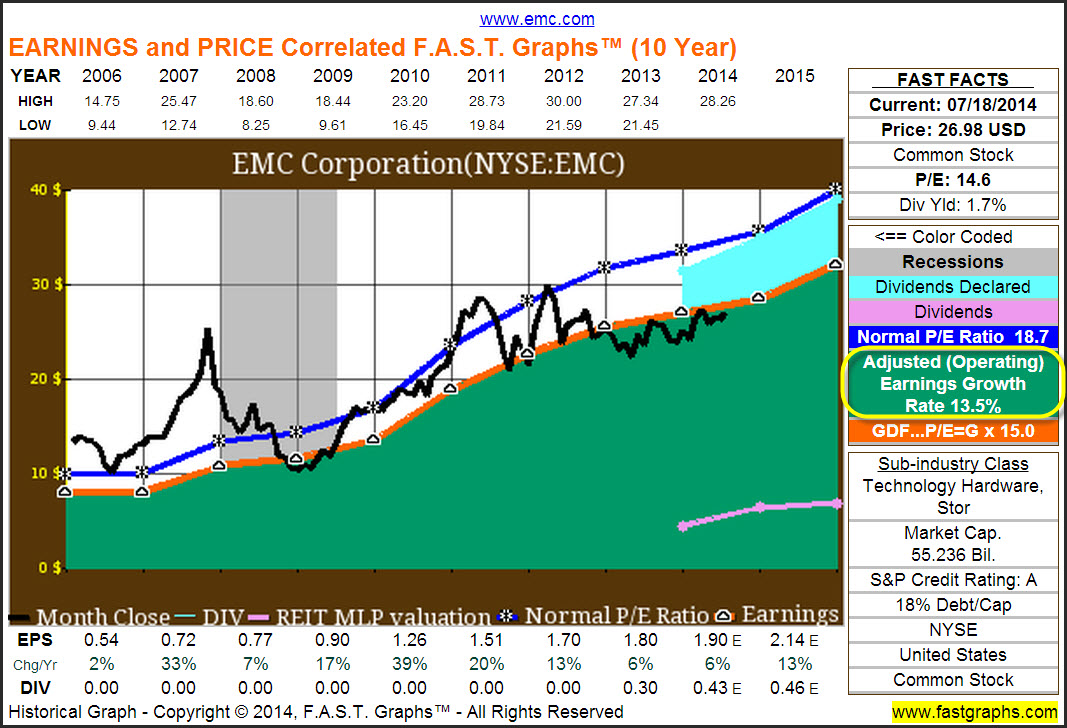

10-Year Earnings and Price Correlated FAST Graph (with Dividends and Normal P/E Ratio)

This timeframe clearly illustrates the importance of earnings and their influence on stock price in the long run. Since 2006 there were several periods where EMC Corp’s stock price deviated from earnings and simultaneously becoming overvalued, before inevitably returning to fair value (the orange line).

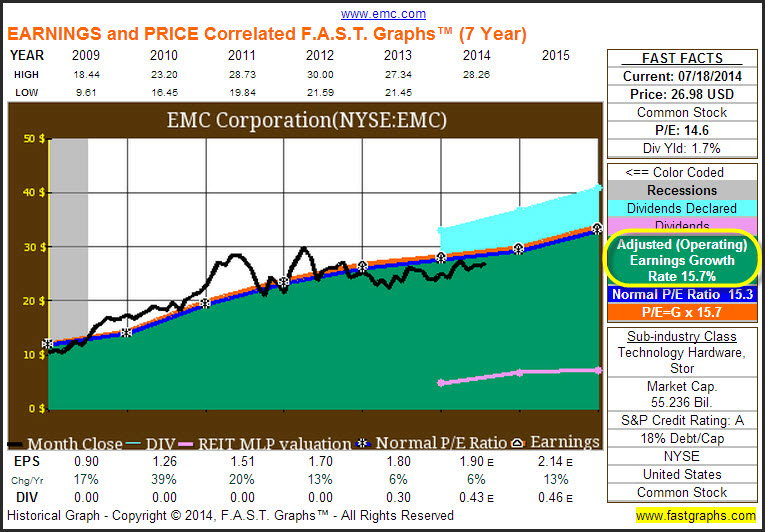

7-Year Earnings and Price Correlated FAST Graph (with Dividends and Normal P/E Ratio)

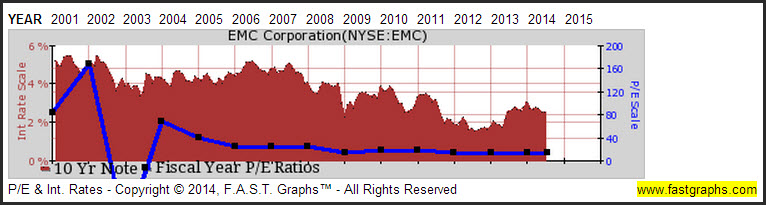

15-Year Historical P/E Ratio Trend

The dark blue line reflects the fiscal year-end P/E ratio for EMC Corp since 2001 (the right scale on the graph). Here we see a steady decline in EMC’s P/E ratio. However, consideration should be given to the excessive high P/E ratios that were afforded most tech stocks during the tech bubble.

Performance

Historical performance is functionally related to earnings growth achievement and starting valuation. Consequently, when performance is properly measured, it is imperative that starting valuation be considered in conjunction with earnings (and dividends, if any) growth.

A high beginning valuation will reduce capital appreciation; a low beginning valuation will enhance capital appreciation. When a company’s beginning valuation is in alignment with earnings, capital appreciation will be highly correlated with the company’s earnings growth rate.

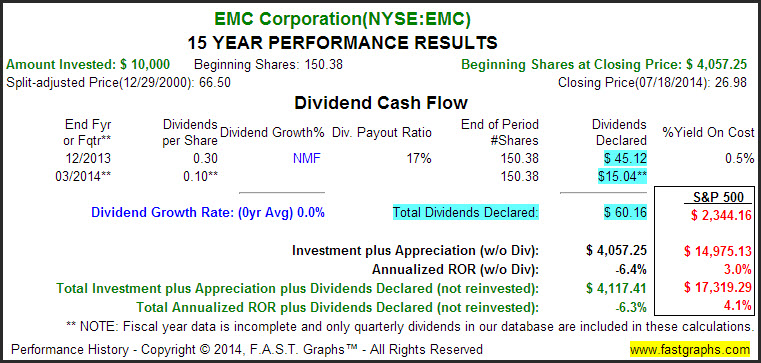

15-Year Performance: From Beginning Overvaluation

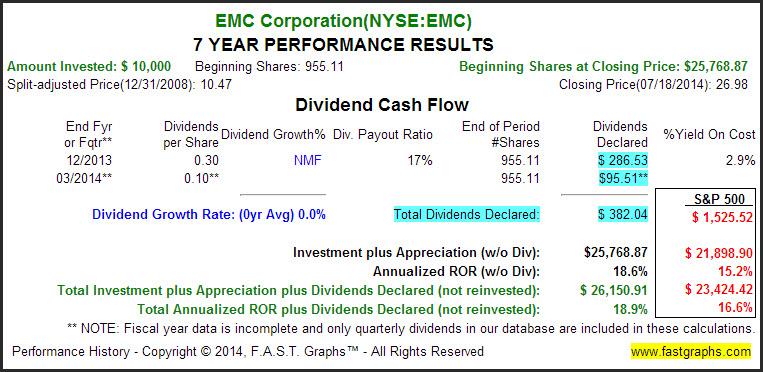

7-Year Performance: From Beginning Fair Valuation

Earnings Forecasts

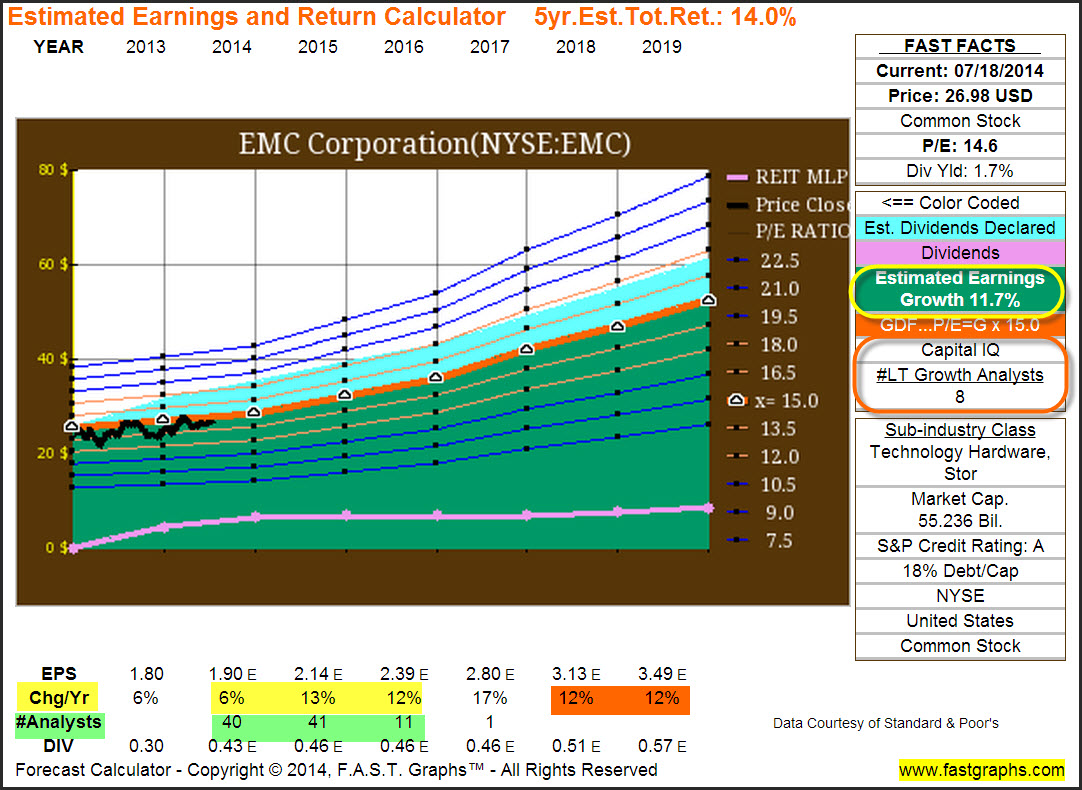

The “Estimated Earnings and Return Calculator” provides several specific future year’s earnings forecasts. Specific near-term earnings forecasts (varies from two to four years) are provided to include the number of analysts reporting to Capital IQ (yellow and green highlights). Additionally a long-term (three to five year) growth rate is also provided (orange highlights). The specific number of analysts offering the long-term forecast is found in the FAST FACTS box (orange circle).

Therefore, we highly recommend placing more credence on the near-term forecasts because they are likely to be more accurate. Moreover, near-term forecasts tend to include a greater number of analysts in the consensus.

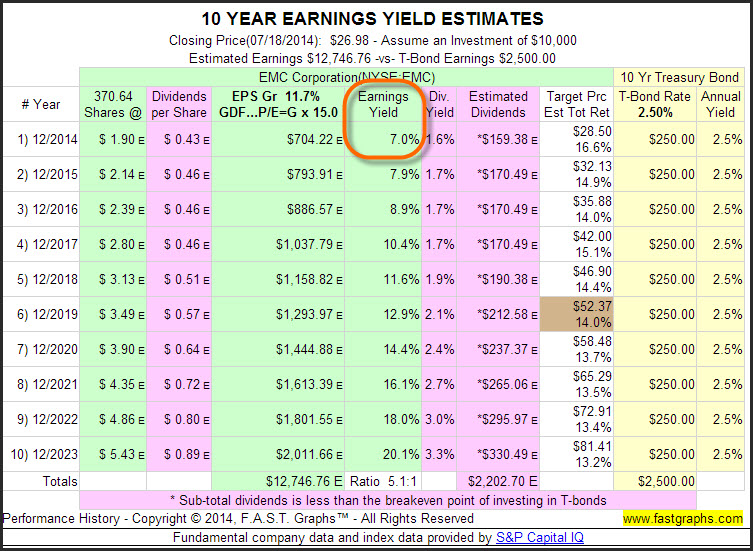

Earnings Yield

Shareholders in publically traded companies, even though they are passive owners, can expect to be rewarded for their investment in proportion to the company’s earnings capacity. Consequently, the earnings yield calculated from current and future (expected) earnings represents an important valuation consideration.

FUNdamentals: A Deeper Look

Utilizing FUN Graphs (fundamental underlying numbers), the following important fundamental metrics and key ratios are offered to provide a deeper look into the company’s financial strength and current valuation.

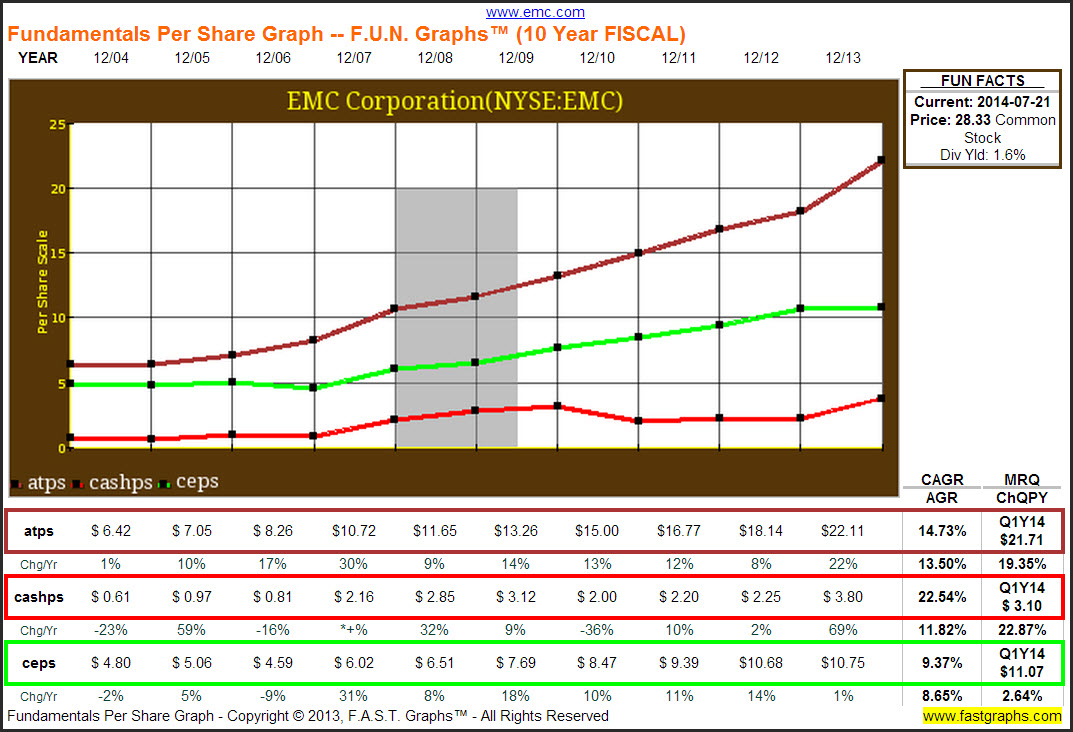

Balance Sheet

The following balance sheet items are offered to reveal the financial health of the company. They include assets per share (atps), cash and equivalents per share (cashps) and common equity or book value per share (ceps).

These key balance sheet items reveal that EMC Corp possesses a strong and healthy balance sheet. This begs the question as to whether or not it makes sense to break the company apart as Elliott Management suggests.

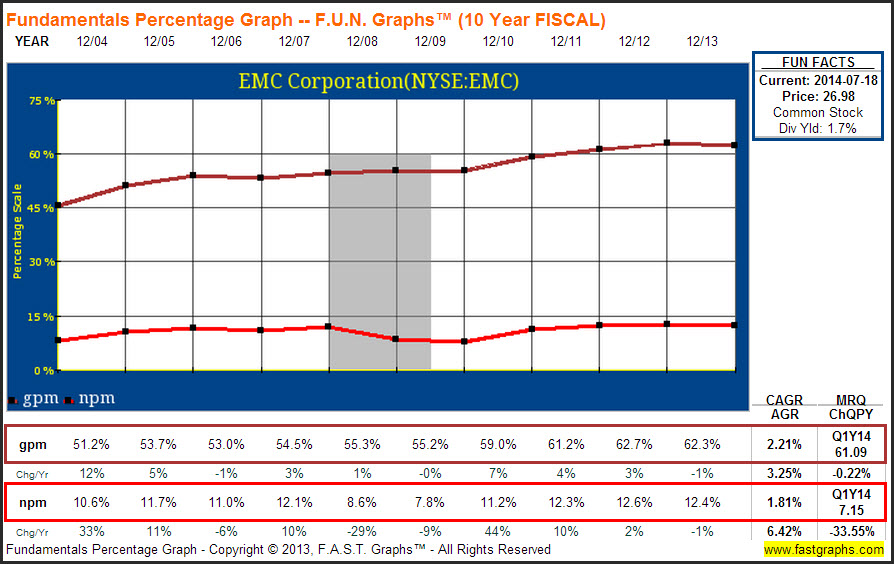

Gross and Net Profit Margins

EMC Corp has maintained consistently strong gross profit margin (gpm) and net profit margin (npm). Moreover, both have shown increases in recent years. Once again, this raises the question of the need to have this company broken apart.

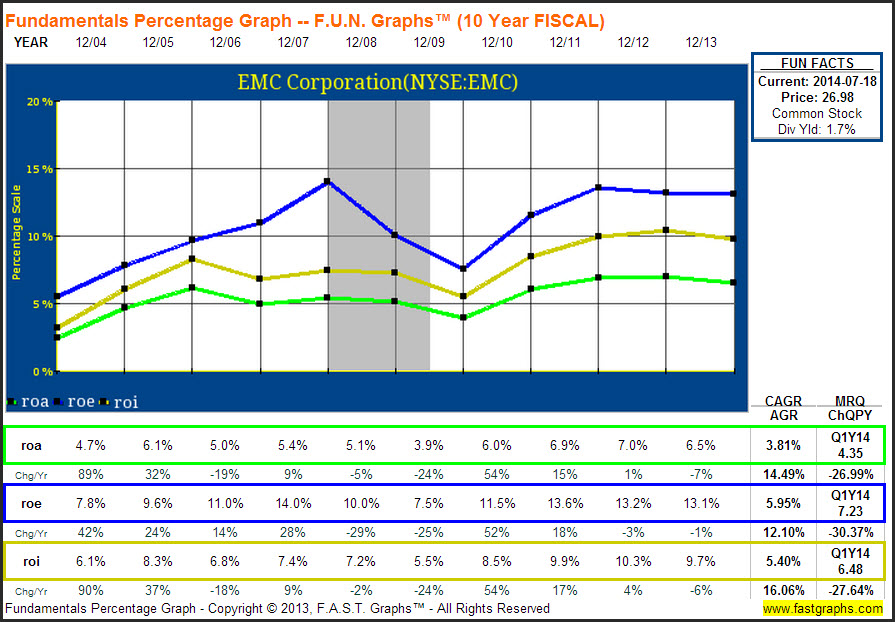

Return on Assets, Equity and Invested Capital

EMC Corp has produced strong returns on assets (roa), returns on equity (roe) and returns on invested capital (roi). Although all three fell during the Great Recession (gray shaded area) they remained at reasonably healthy levels.

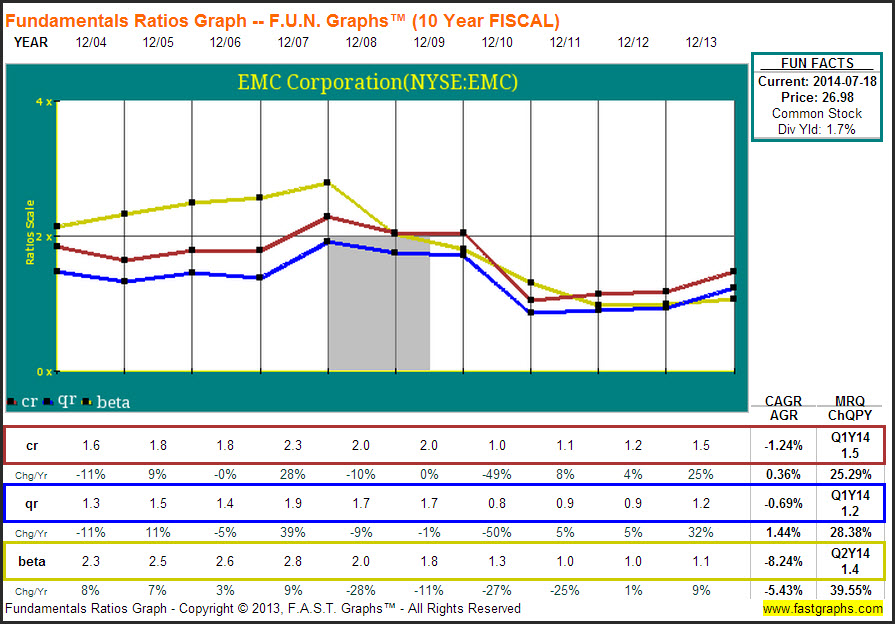

Key Liquidity Ratios

Liquidity is an important consideration when evaluating a business. There are two primary ratios that prudent investors look to.

The quick ratio (qr) also known as the acid-test ratio, measures a company’s ability to meet short-term obligations by utilizing its liquid assets. Generally speaking, a quick ratio of one or better is considered healthy.

Additionally, the current ratio (cr) measures the company’s ability to retire its short-term liabilities (debt and payables) with its short-term assets (cash, inventory and receivables). This important ratio is often referred to as the liquidity ratio and is a good indicator of a company’s ability to remain a going concern.

Since many investors are concerned about price volatility, we have included five-year beta as an additional key ratio. A beta of one or lower is considered ideal relative to risk. On the other hand, a beta above one may also indicate the potential for above-market long-term performance.

Although these key liquidity ratios relating to EMC have deteriorated following the Great Recession, both have shown positive improvements since 2011. Consequently, it is clear that EMC Corp is capable of meeting short-term obligations.

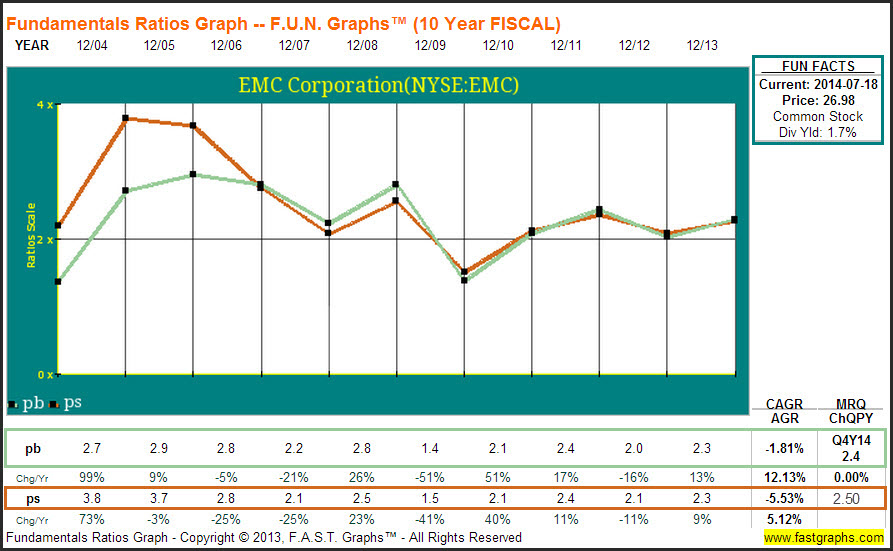

Additional Key Valuation Ratios

Two important valuation ratios that investors consider are price to book value (pb) and price to sales (ps). When considering both of these valuation ratios, the lower the better.

Consequently, it is clear that EMC’s current price to book and price to sales ratios are on the historically low side. This offers an additional indication that the company is currently fairly valued.

Key Management Shareholder-Friendly Metrics

Many investors consider a company’s shareholder-friendliness based on its dividend policy and/or share buyback policy. A consistent record of paying dividends, and better yet, increasing the dividend are considered positive attributes of management.

However, many companies in the growth phase may consider it more profitable to retain their cash to fund growth. Consequently, the lack of a dividend does not necessarily indicate that management is not shareholder-friendly.

Regarding share buybacks, they are considered friendly because they are anti-dilutive. However, share buybacks should only be considered shareholder-friendly when management is buying back shares when stock price is sound or undervalued.

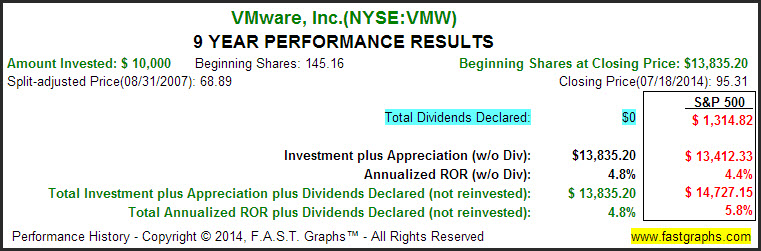

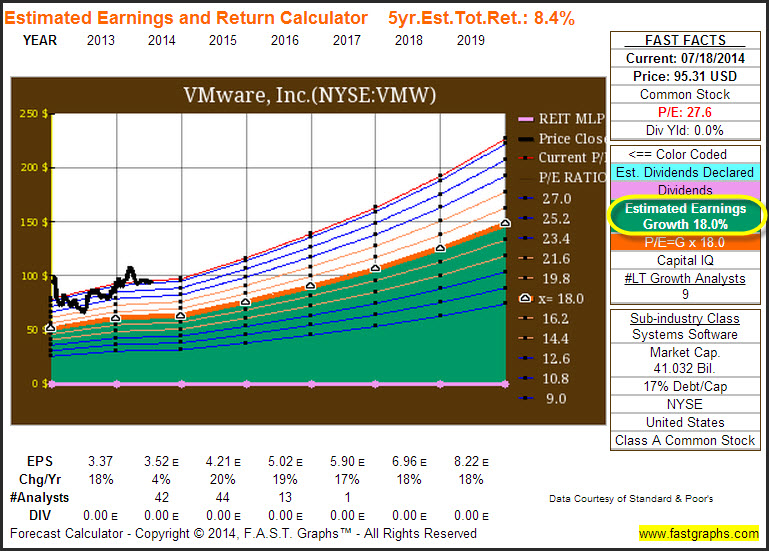

Bonus: VMware Inc (VMW) Earnings and Price Correlated Graphs and Performance

As reported in The Wall Street Journal on Monday, and again in The Wall Street Journal today, EMC Corp maintains an 80% stake in VMware Inc, which is also a publically traded company. Elliott Management believes that EMC’s stock would receive a substantial boost if they were to spin-off these assets. However, we believe that based on the high rate of earnings growth that VMware Inc has achieved, and the high earnings growth that it is forecast to achieve, does not support Elliott Management’s thesis. Furthermore, as reported in The Wall Street Journal above, VMware Inc contributed less than a quarter of EMC’s consolidated revenue last year.

Summary and Conclusions

It seems that Elliott Management is disturbed about EMC’s current market price, contending that the shares are not being fairly valued by the market price. However, based on fundamental value, we contend that EMC Corp is being properly valued by the market currently, and has been for the last 18 months. Therefore, we believe that this company is best left at its current capital structure.

On the other hand, if Elliott Management continues, it could prove temporarily destructive. Therefore, prospective investors should consider and monitor these developments as they unfold.

Disclosure: No position at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.