Is Dow 17,000 Dangerously High? This Comprehensive Review May Surprise You!

Introduction

The Dow Jones Industrial Average recently closed above 17,000, a historical record and milestone. Consequently, the question at the forefront of every investor’s mind has understandably been raised. Has the market now become dangerously high and therefore destined for a crash? The truthful answer to this important question is that nobody can know for sure what the stock market might do over the short run. On the other hand, just because the stock market as measured by the Dow, or individual stocks for that matter are at all-time highs, it does not necessarily follow that they are dangerously overvalued at the same time.

Investors are best served when they understand that there is a significant difference between price and value. In this regard, there are several possibilities that could be true when a stock (or an index) is trading at an all-time high. For example, if the company’s earnings have grown faster than its price, the company can actually be undervalued or fairly valued at the same time. Conversely, if earnings growth has not kept up with price, then it is quite possible that the company is truly overvalued. However, the point is that a high price alone does not necessarily indicate high valuation.

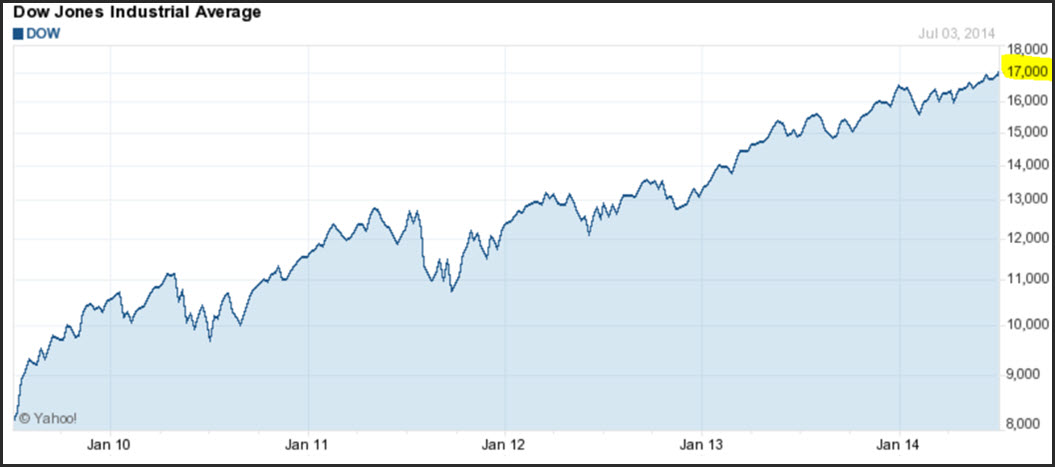

I consider this one of the most important principles of investing that all too often goes ignored. In my humble opinion, measuring price without simultaneously measuring its relationship relative to earnings (fundamental value) is a job half done. Unfortunately, most investors have only price charts to examine, as depicted by the following Dow Jones Industrial Average graph from Yahoo Finance. Based on this graph alone, it is clear that the Dow Jones Industrial Average based on price alone is clearly at an all-time high. However, it is not clear from this price graph that the Dow is simultaneously overvalued.

Moreover, it’s important to also recognize that this index is comprised of 30 constituents spread out over 9 broad sectors. Of the 30 Dow stocks there is one in the Materials sector, 2 in the Energy sector, 5 in the Industrial sector, 4 in the Consumer Discretionary sector, 3 in the Consumer Staples sector, 4 in the Healthcare sector, 4 in the Financial sector, 5 in the Information Technology sector and finally 2 in the Telecom sector. But most importantly, each of these individual companies is trading at their own distinct and specific valuation.

The Relative Valuation of the 30 Dow Jones Industrial Average Constituents

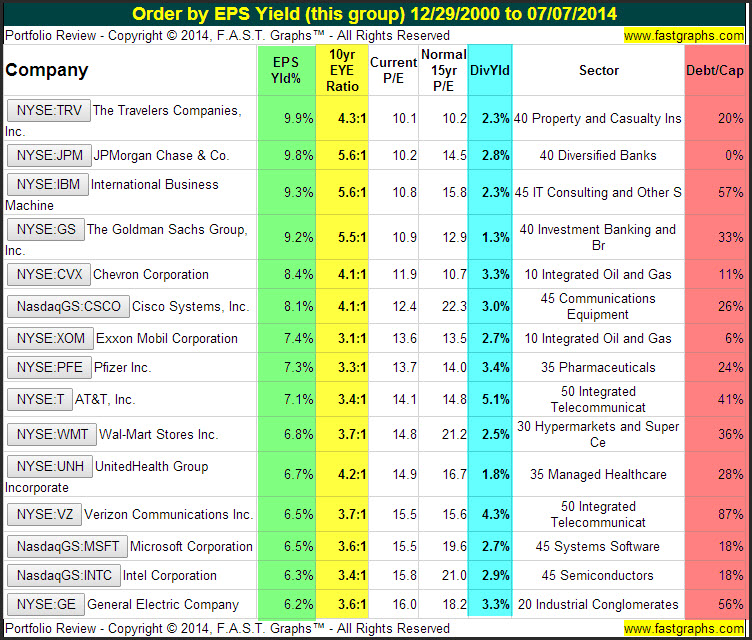

The S&P 500 and the Dow Jones Industrial Average are the two most commonly considered proxies for evaluating the overall level of the stock market. What I like best about the Dow is that it only contains 30 stocks. Consequently, it is very easy to evaluate each constituent in order to gain a more comprehensive view of the specific valuation of each. Utilizing the earnings and price correlatedF.A.S.T. Graphs™ research tool I examined the actual individual valuation of each of the 30 Dow Jones’ stocks. My objective was to gain a truer perspective of whether Dow 17,000, an all-time high, really suggests that the market is overvalued.

What I found was quite interesting. Based on the relationship of earnings to price, I found 15 of the Dow components, or half of the index, to be fairly priced based on earnings yield, and the other half to be fully valued and a few moderately overvalued. However, the true value of my research effort was through the individual fundamental analysis of each of the specific companies making up the Dow Jones Industrial Average.

Therefore, in order to provide the reader a clearer and more detailed perspective, I offer the following fundamental analysis of each component in graphic form. Since each of the 30 Dow components are widely-recognized, I have added only a short business description on each courtesy of Standard & Poor’s Capital IQ. For those not initiated in how to interpret the fundamentals analyzer software tool, I offer the following link to provide a simplified explanation of how to interpret a FAST Graph.

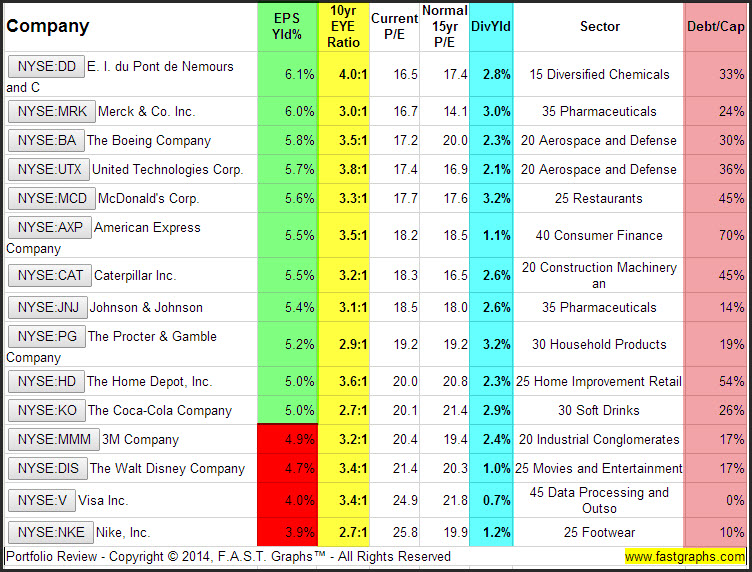

Portfolio Review: 15 Fairly Valued Dow Constituents

The following portfolio review lists 15 Dow constituents that I consider fairly valued based on earnings yield. In my opinion, the true value of analyzing valuation based on P/E ratios is through the understanding of the earnings yield that the P/E ratio represents. Simply stated, the inverse of the P/E ratio (price-to-earnings ratio) or the E/P (earnings to price ratio), calculates the investor’s yield derived from the total earnings of the company.

A simpler way to look at this is to think of the earnings yield as the return on your investment that the company’s operating success provides if you owned the entire business. Obviously, passive investors in a publicly traded company cannot expect to receive all of the company’s earnings as a return. On the other hand, since each Dow component represents high-profile large-cap dividend paying stocks, each company’s earnings represent the source of dividends. Therefore, and if for example, you are a retired investor desirous of a dividend yield of 2% or better, the company’s total earnings yield should be high enough to support that dividend.

Personally, and as a very general rule of thumb, I like to see an earnings yield that is at least twice the company’s dividend yield, and even better, triple the company’s dividend yield. Consequently, I consider an earnings yield in the range of at least 6% to 7% as my minimum threshold for a blue-chip large-cap dividend paying stock. Mathematically, this implies a P/E ratio of 15 or lower. In other words, if I pay $15 (a P/E ratio of 15) for each dollar’s worth of a company’s earnings, my earnings yield is 6.67% (15 /$1=6.67 % earnings yield). This is but one of many reasons why I consider a P/E ratio of 15 to represent a reasonable or fair value for most large-cap dividend paying companies.

The following portfolio review lists 15 of the 30 Dow stocks that offer an earnings yield of 6% or better (green highlighted column). For those companies on the list that offer earnings yields slightly less than that, as a stickler for fair value I would patiently wait for a modest pullback before I invested. On the other hand, a 6% earnings yield for a quality company might be close enough for government work as the saying goes.

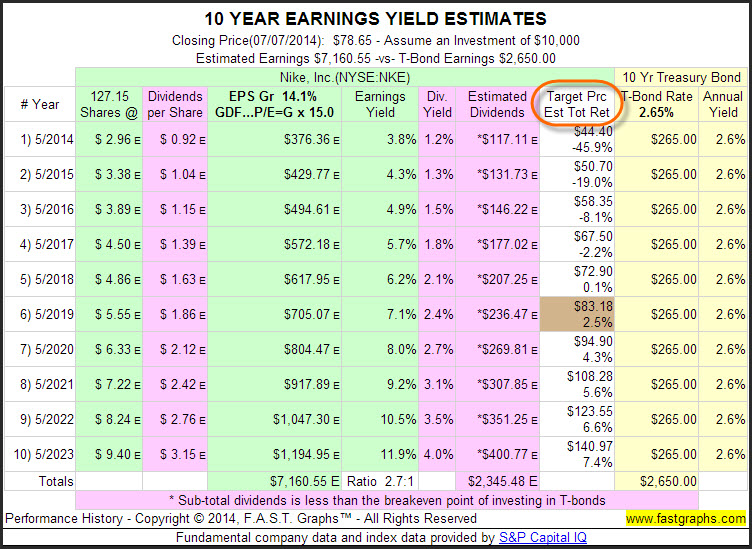

That second column on the portfolio review is the 10-year EYE ratio (earnings yield estimates versus the 10-year T-bond). This is simply another valuation benchmark that compares expected (based on current earnings estimates) cumulative total future earnings in comparison to the cumulative total future interest payments currently available from a 10-year T-bond. Since the latter is virtually guaranteed, and of course the former comprised of significant risk, I like to at least believe there is an opportunity for greater rewards associated with taking that risk. Consequently, the higher the EYE ratio, the better I like it. Although all the other columns on the portfolio review are important valuation checks, they should be self-explanatory.

In summary, the portfolio reviews presented below provide simple valuation metrics for each company in the group. However, since as I like to say “the angels are in the details” I will present each portfolio review company with two historical fundamental focused graphs, followed by two graphs based on consensus forecasts from analysts. My goal is to provide the reader with a more comprehensive view and understanding of Dow 17,000, and what it might mean for the index going forward.

Company by Company Fundamental Analysis: 15 Fairly Valued Dow Constituents

For brevity’s sake, I will let the following historical earnings and price correlated graphs followed by forecasting graphs speak for themselves. However, a few comments on interpreting what the graphs are representing are in order.

Historical Graphs

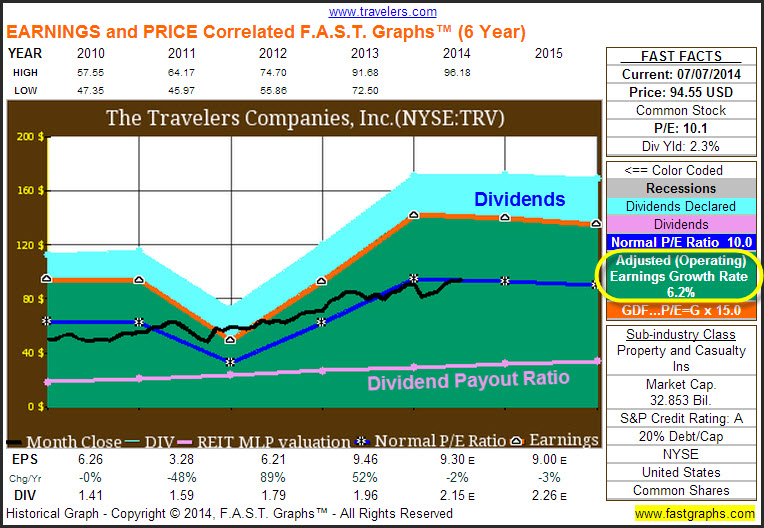

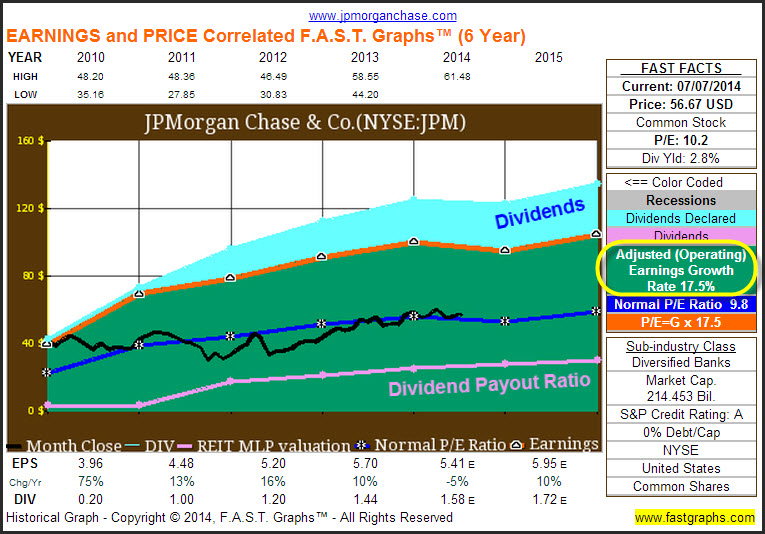

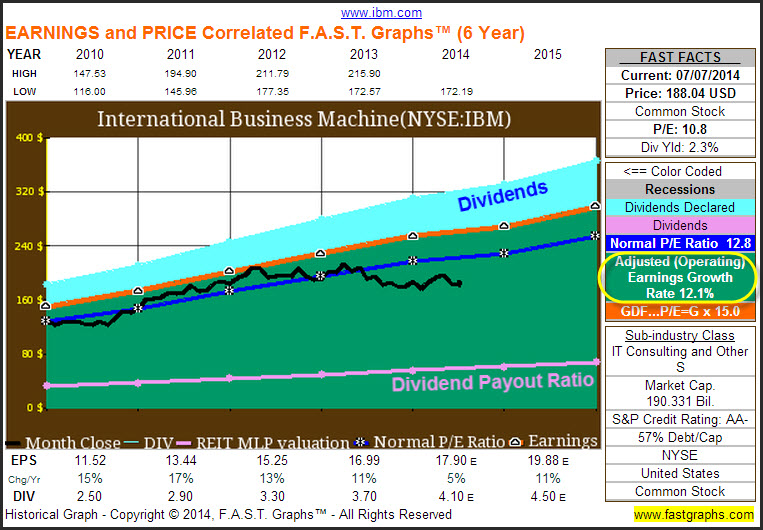

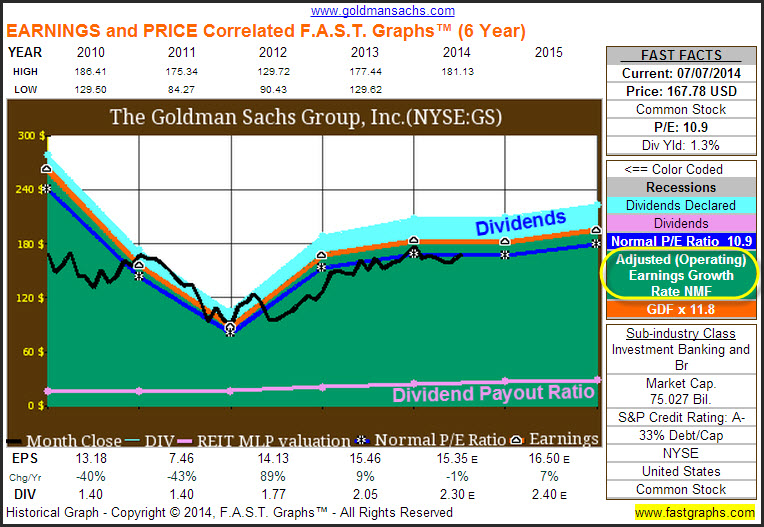

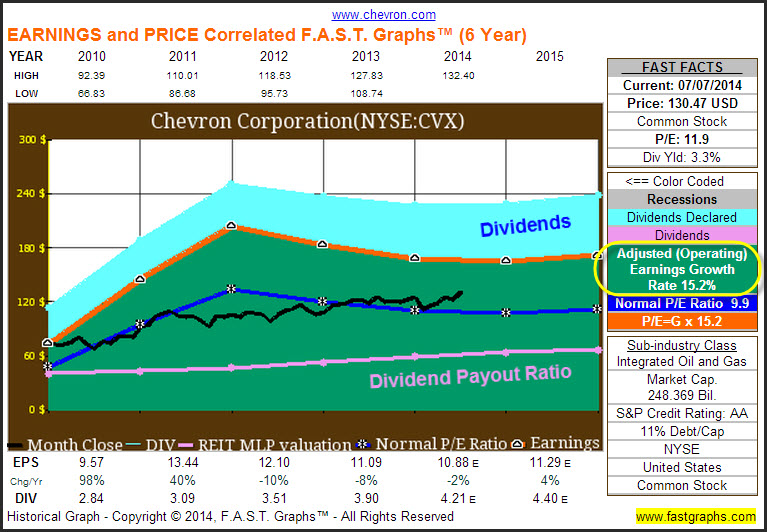

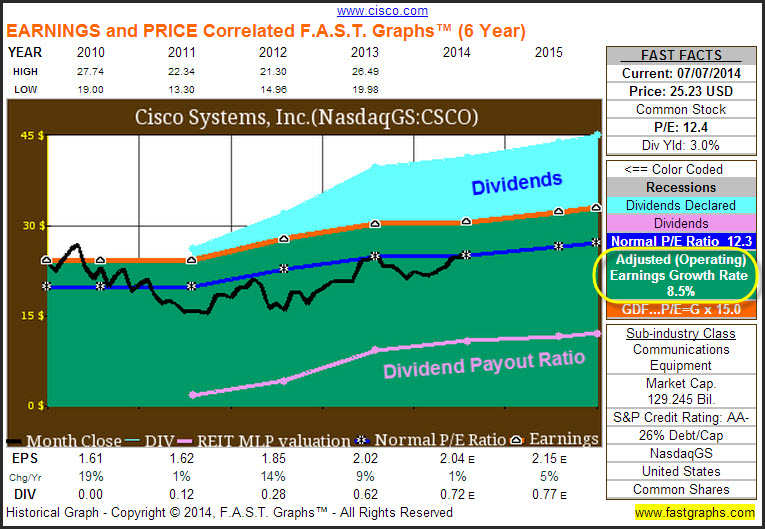

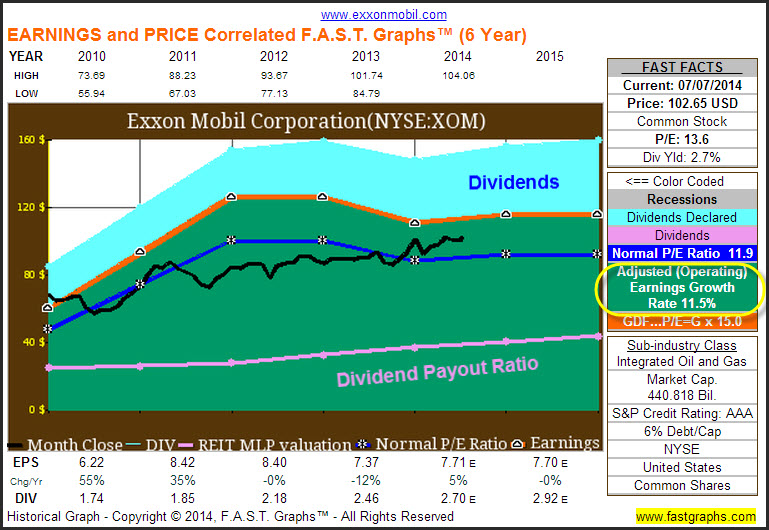

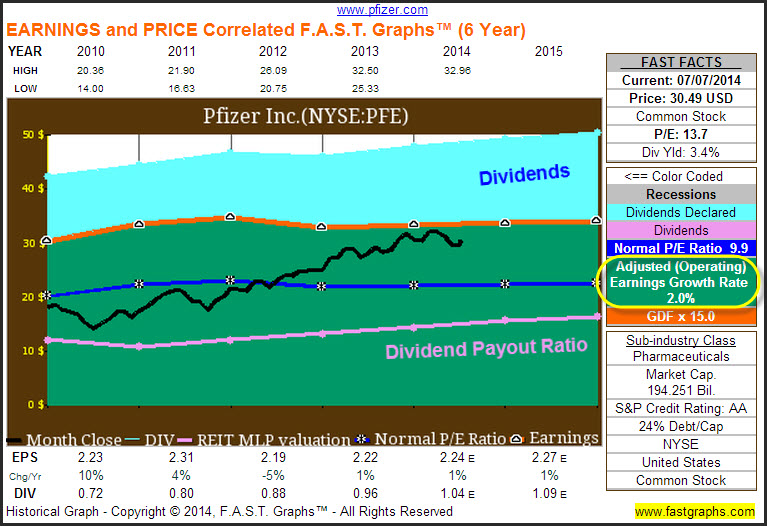

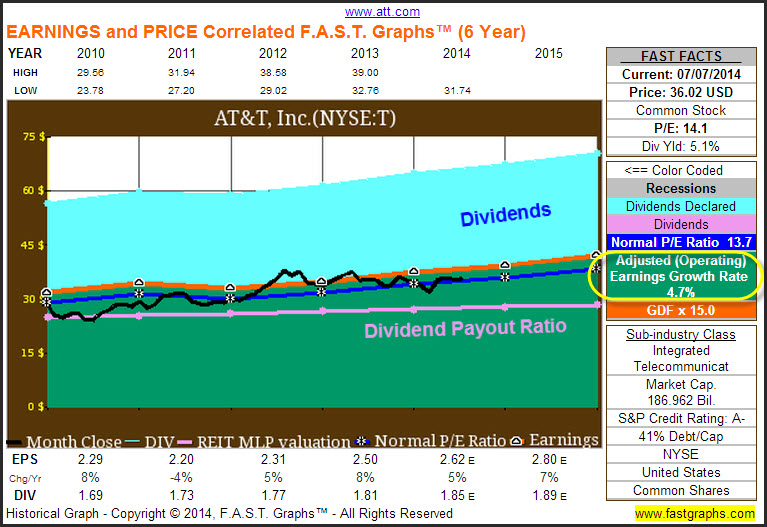

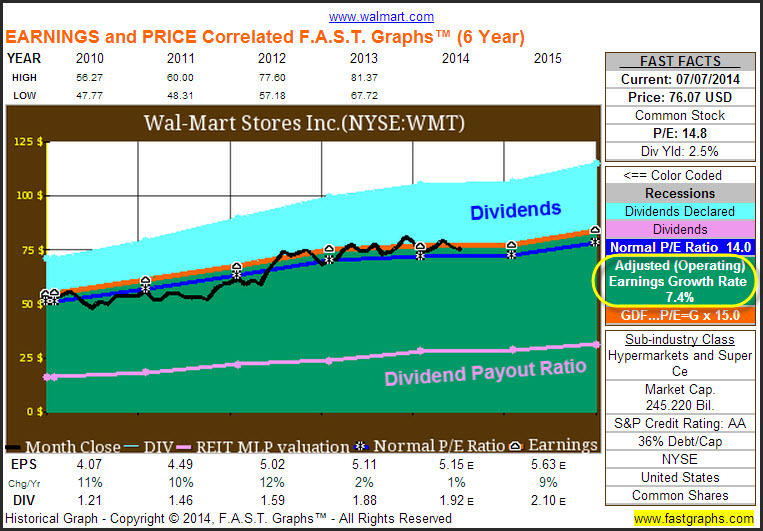

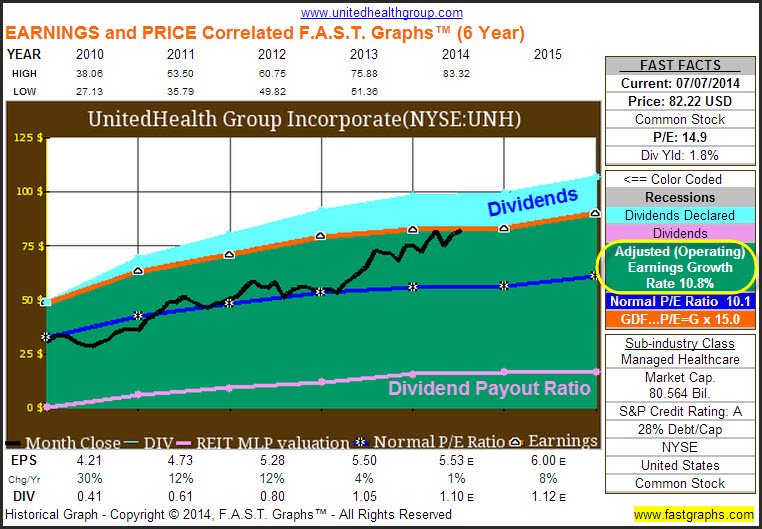

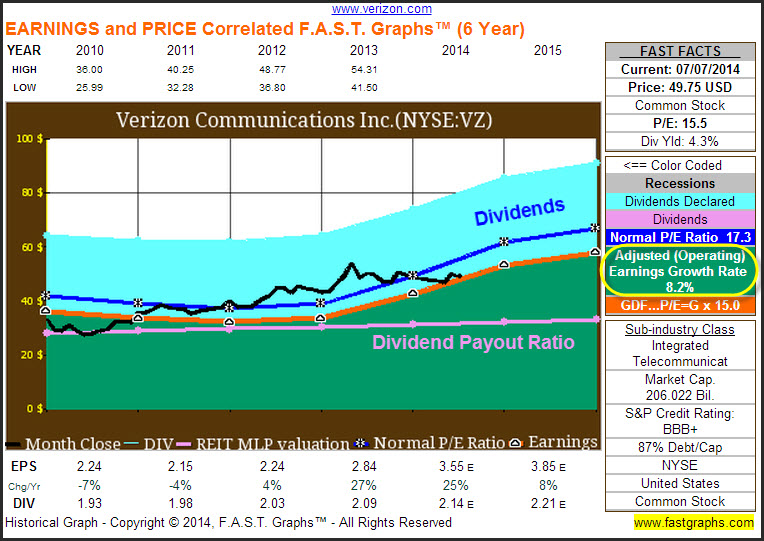

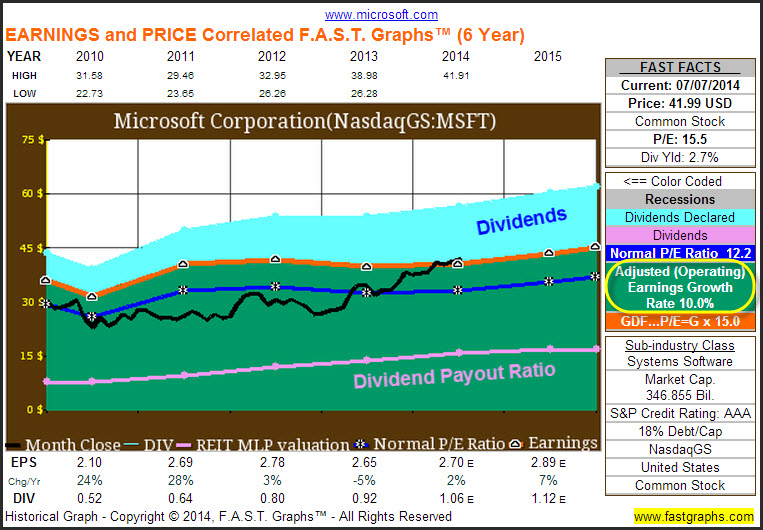

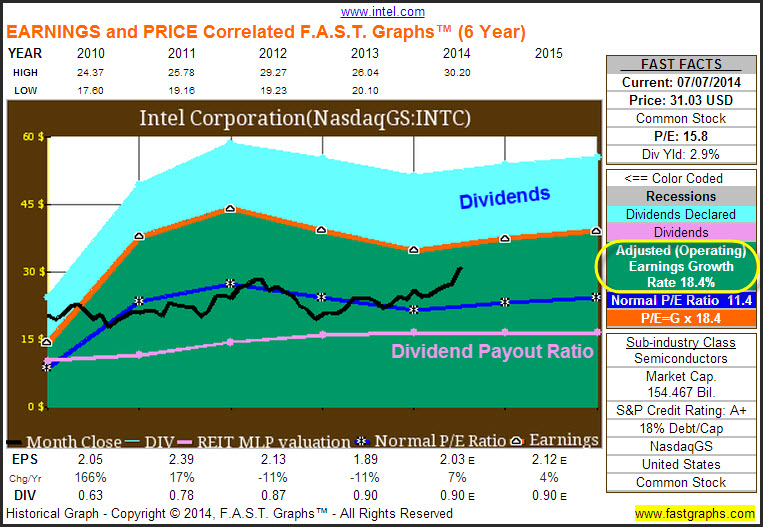

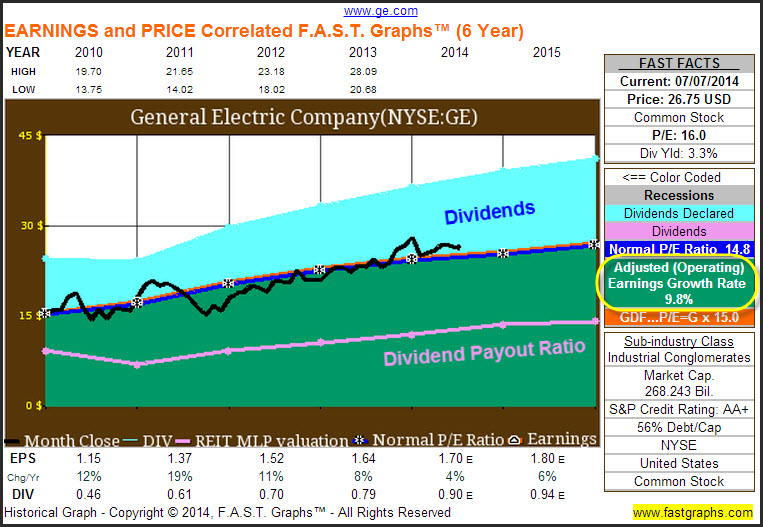

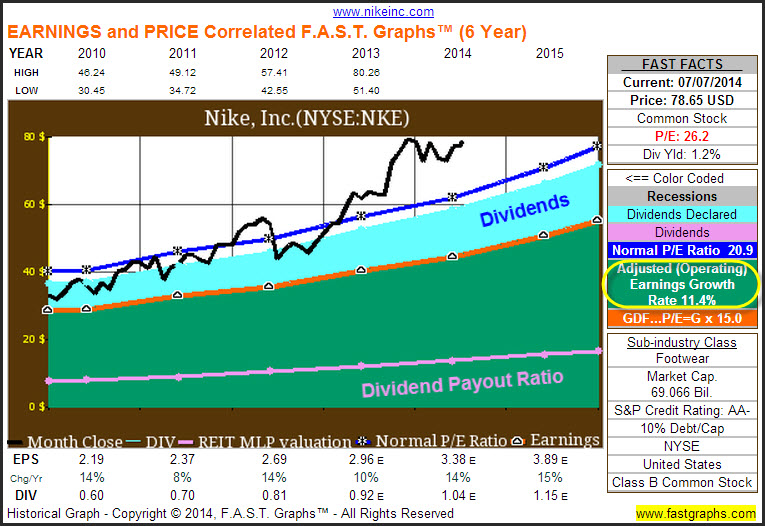

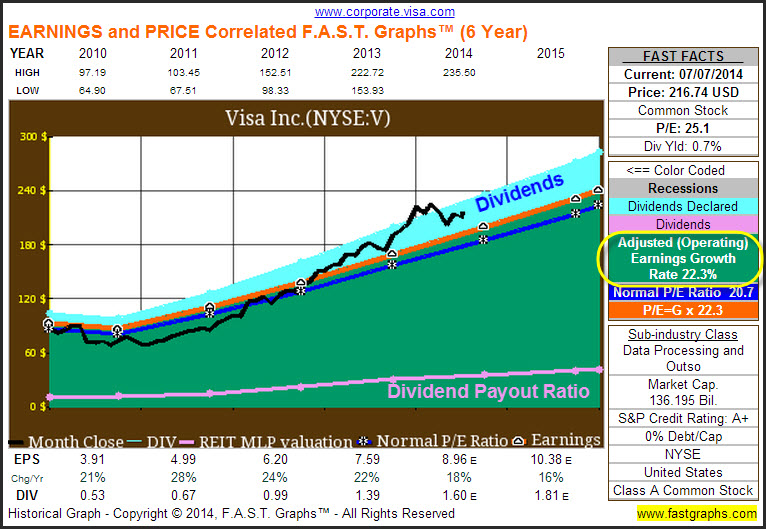

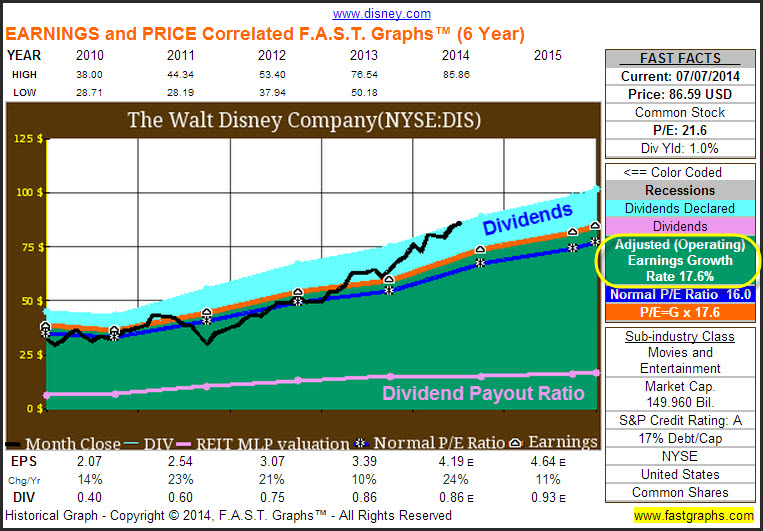

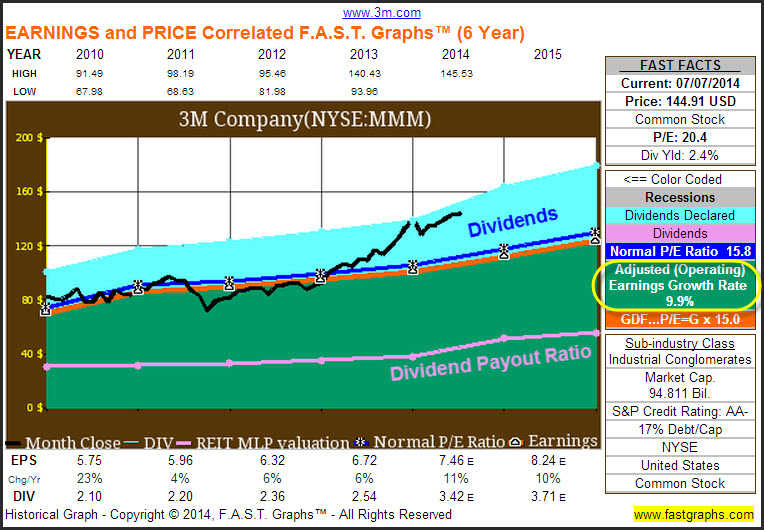

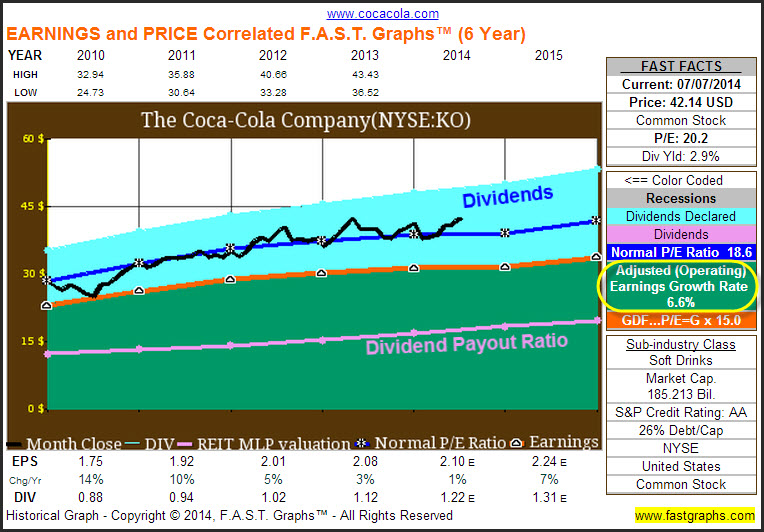

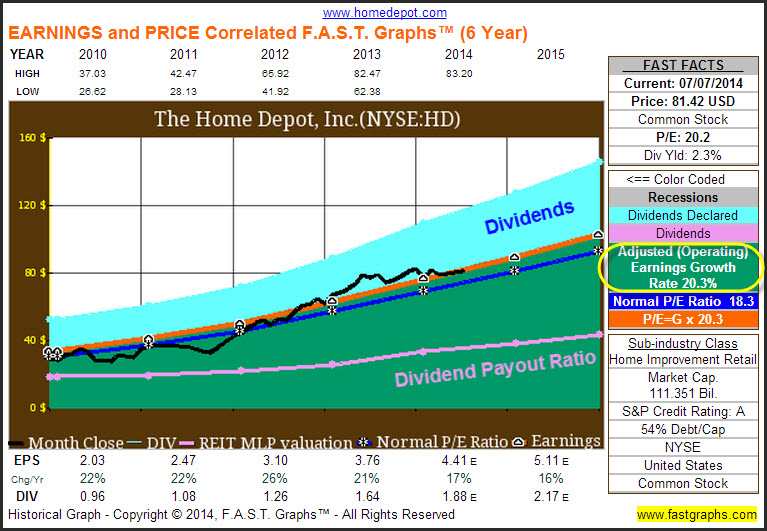

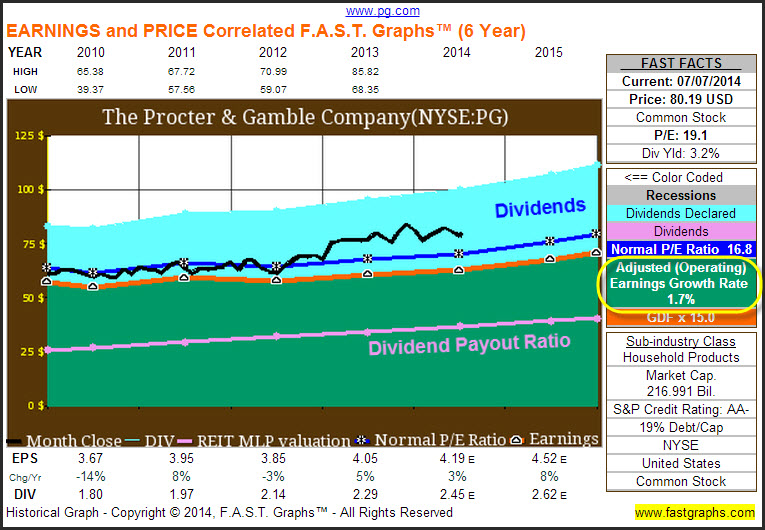

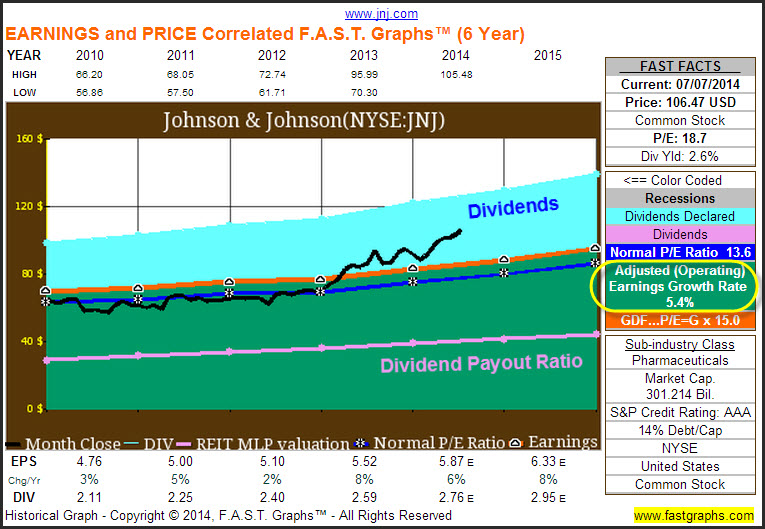

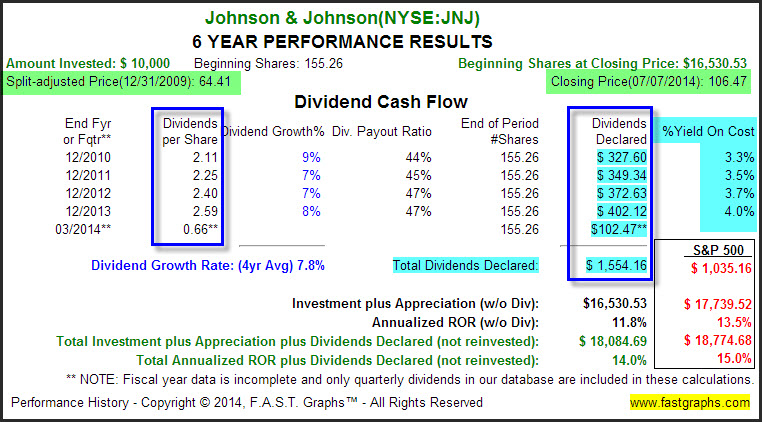

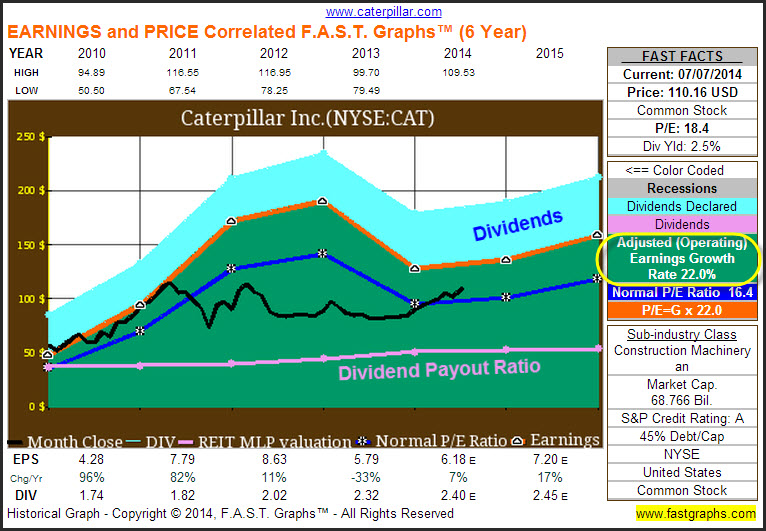

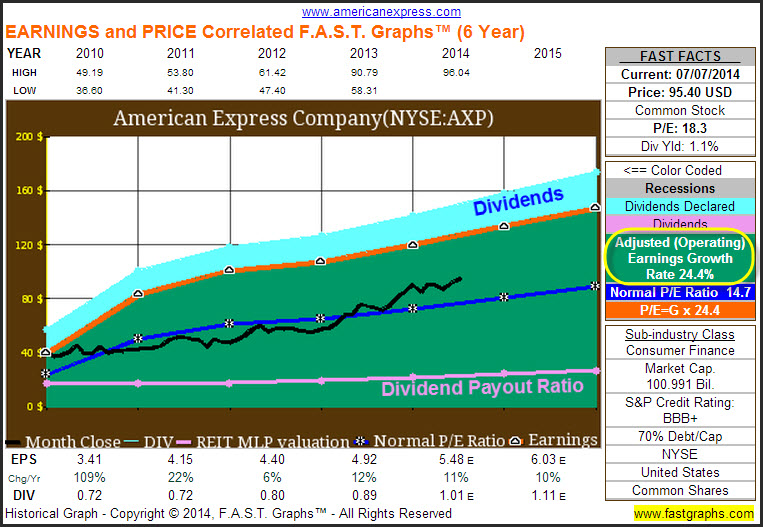

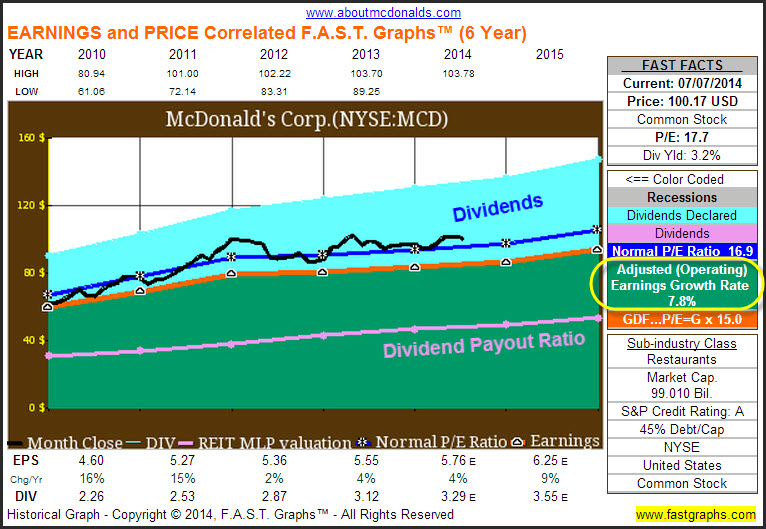

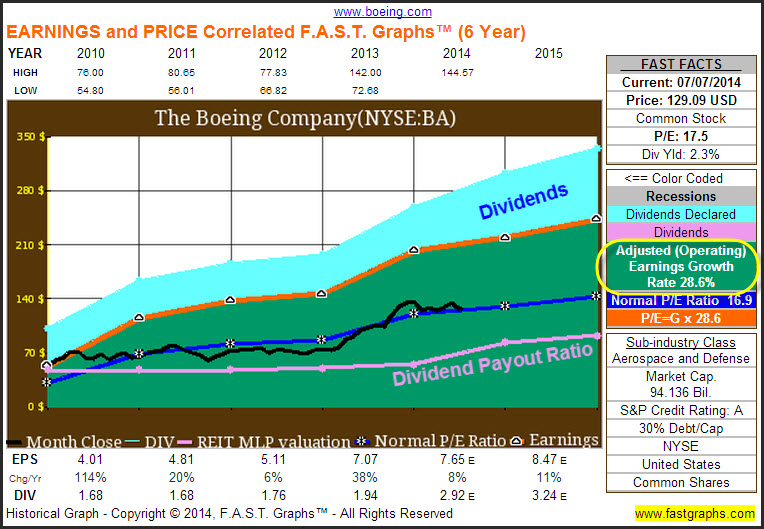

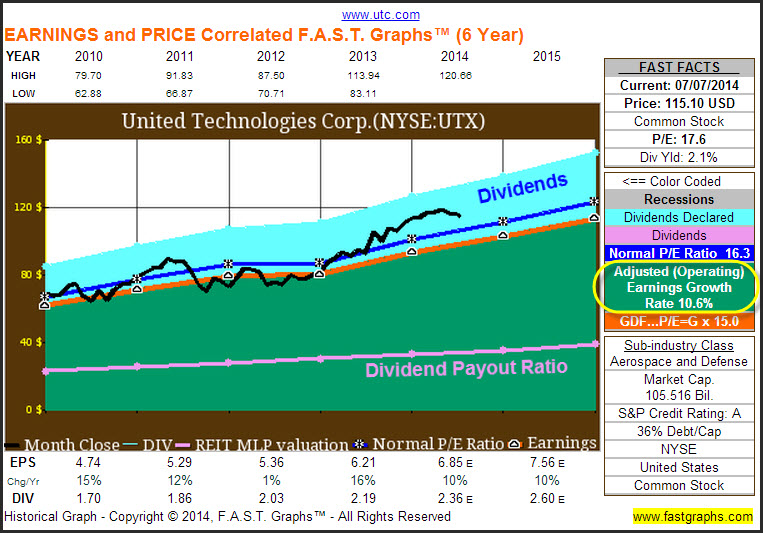

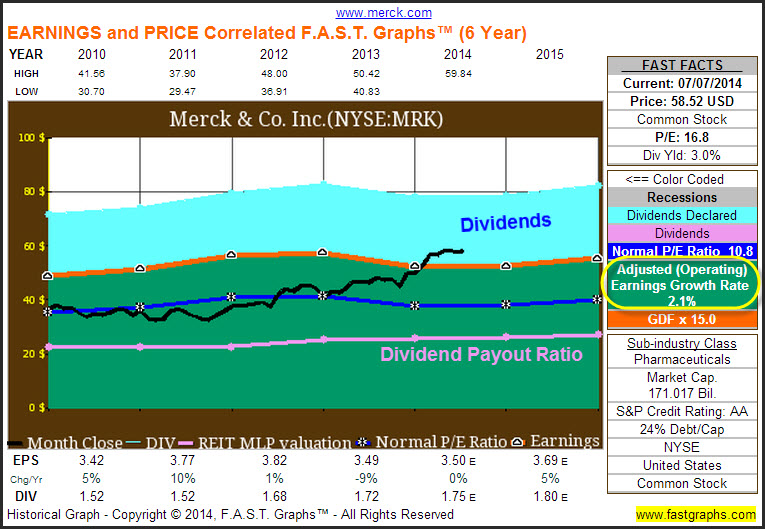

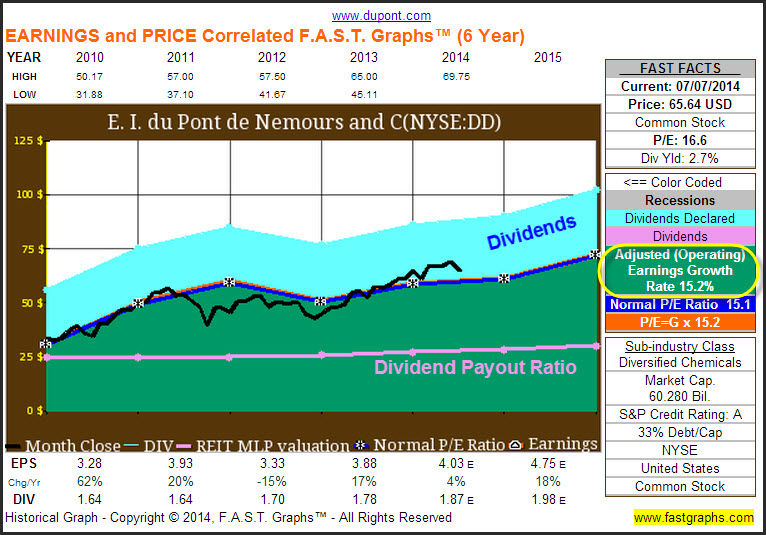

The first graph in each series plots each respective company’s earnings-per-share record since 2010 (the orange valuation reference line and green shaded total earnings area). I chose this specific timeframe because it was post the Great Recession which I feel represents each company’s earnings power under a more normal economic environment.

The orange line and the dark blue line on each graph represent important valuation reference lines. The orange line represents a theoretical fair value P/E ratio that is calculated based on the respective company’s earnings growth rate. The dark blue line represents a reference line that depicts the valuation that the market has typically applied to each respective company over this timeframe (Normal P/E Ratio). It’s important that the reader understands that these are valuation reference lines that are presented to aid with the analysis of fair value.

Dividends are expressed in two forms. The pink line on the graph plots dividends per share for each year and serves the dual purpose of graphically illustrating the company’s dividend payout ratio (the green shaded earnings area below the pink line). The second form is the light blue shaded area above the orange line which indicates dividends after they have been paid out to shareholders from earnings. Note that since this blue shaded area is attached to the earnings line, a drop in earnings in any year could provide the illusion that dividends are cut when in truth they are not. This can easily be determined by examining the pink line.

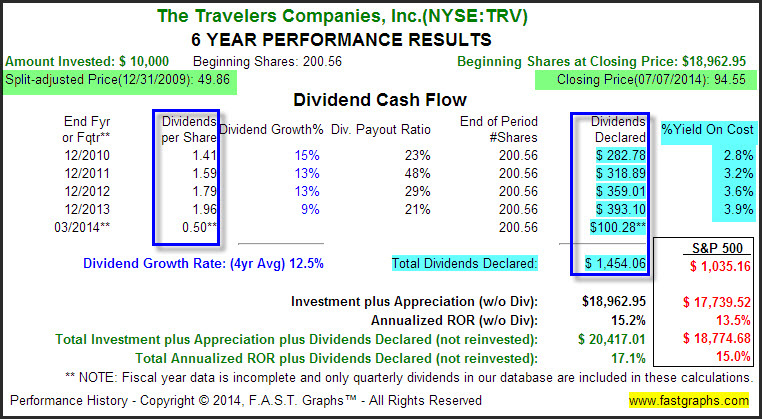

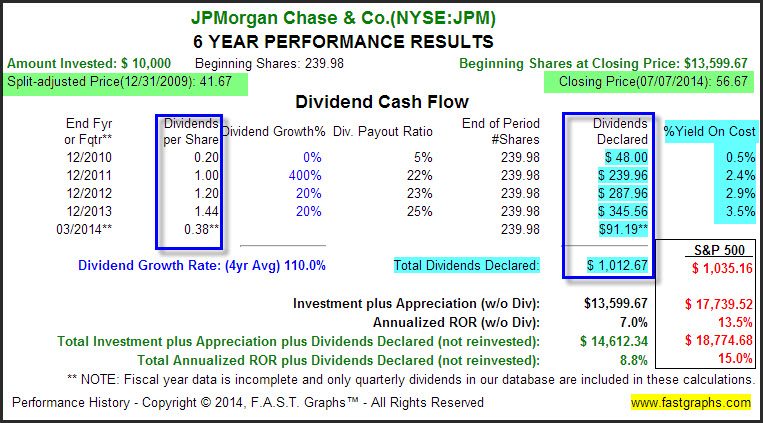

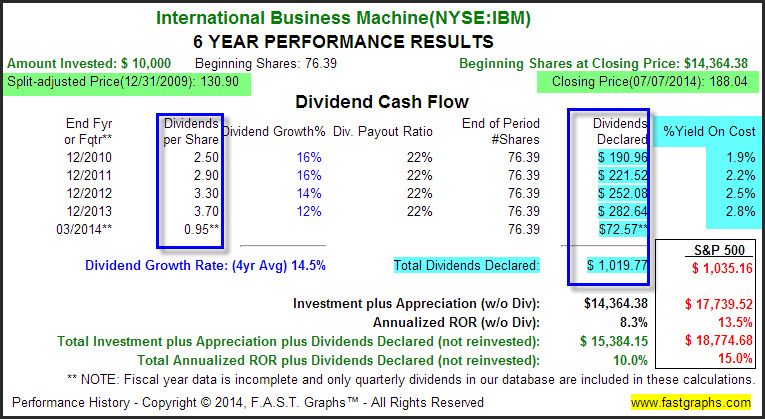

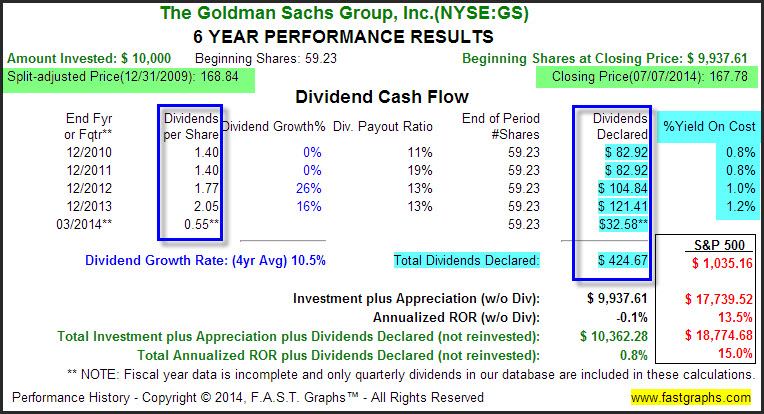

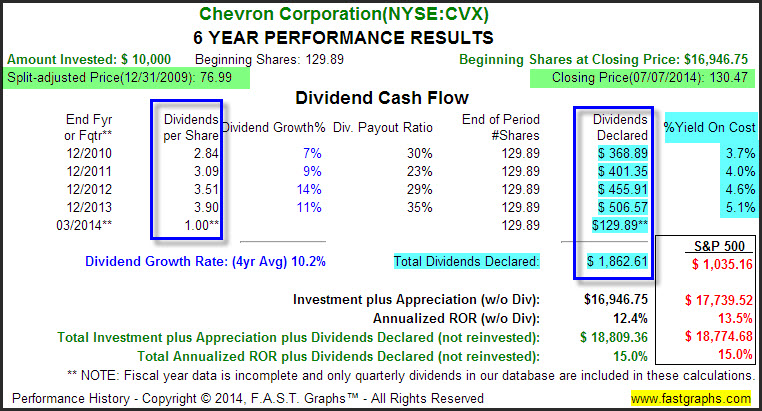

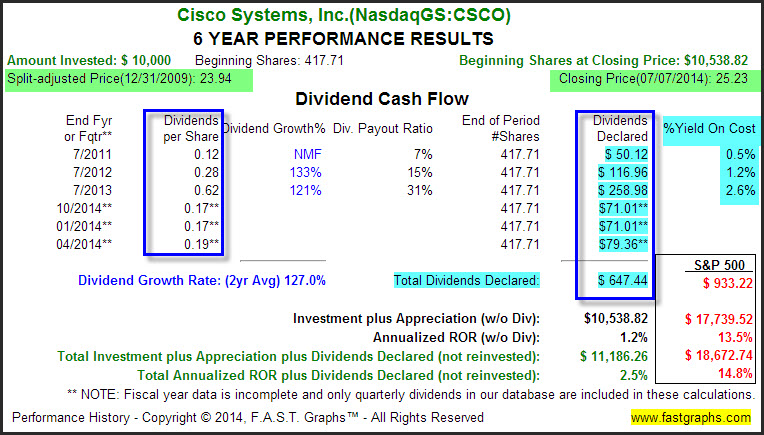

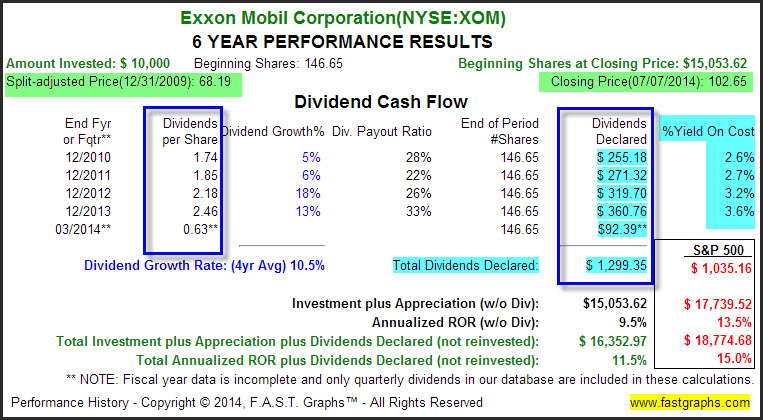

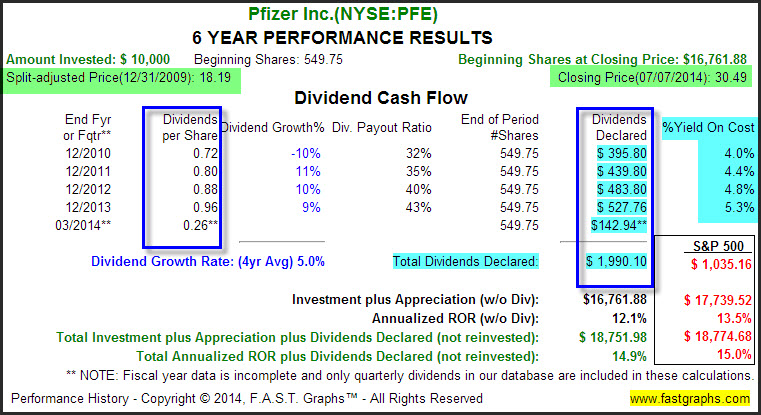

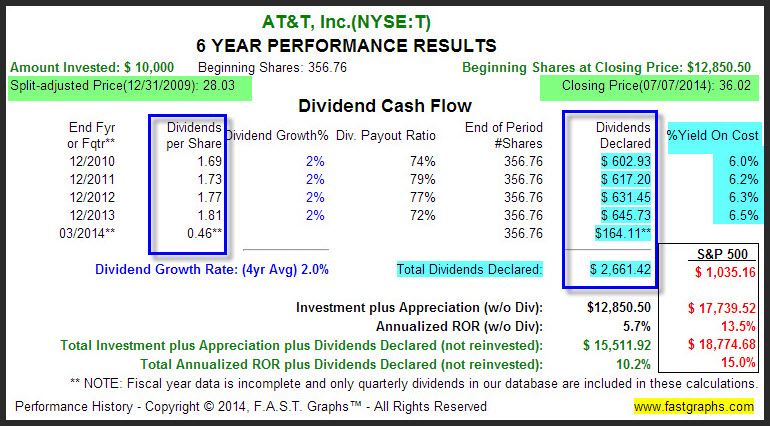

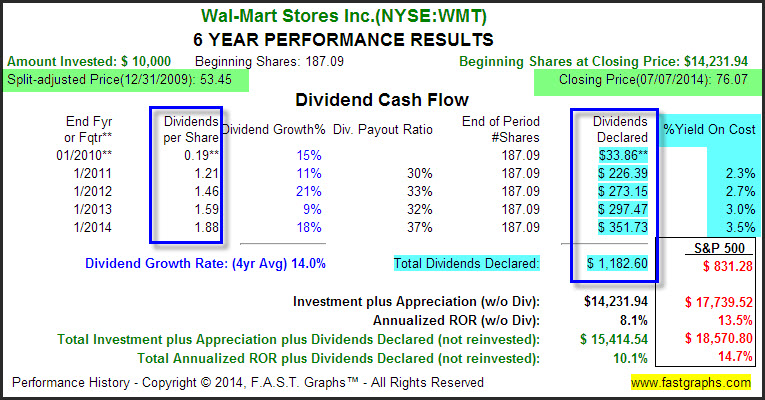

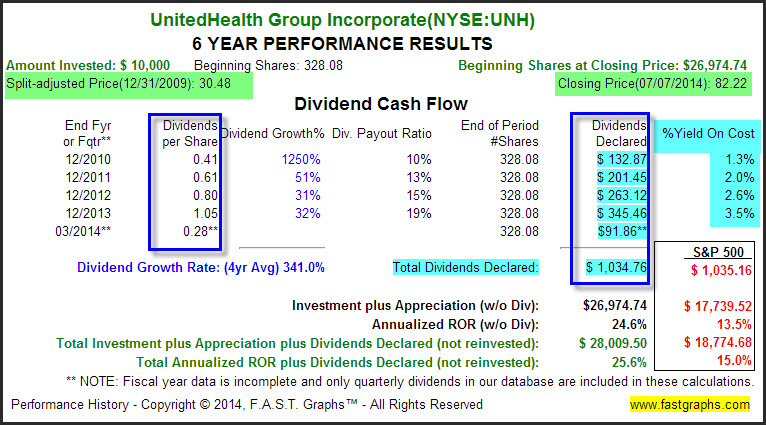

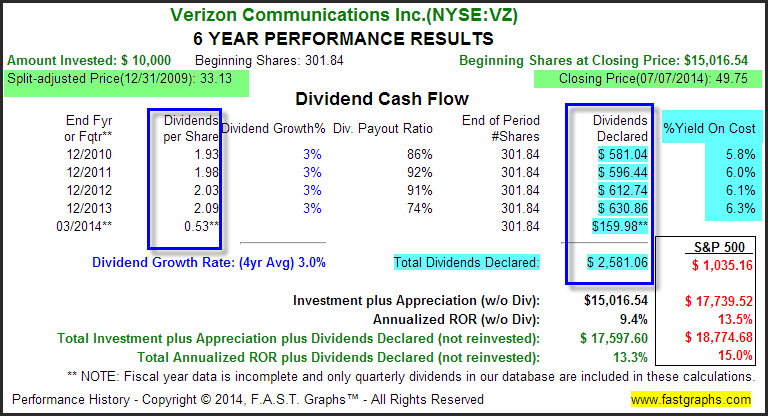

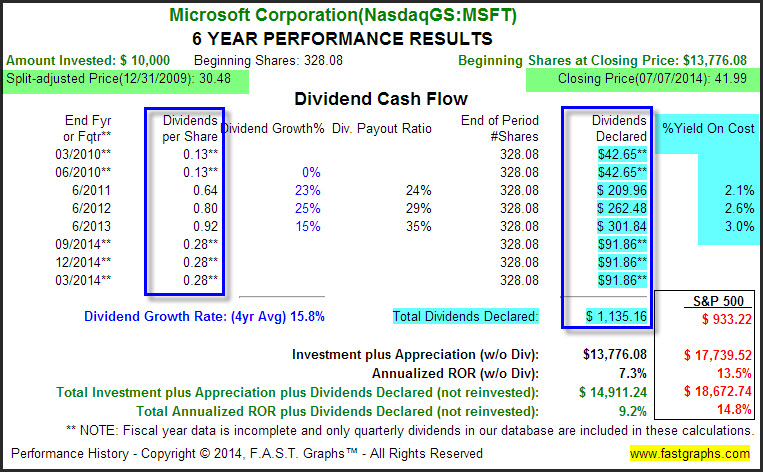

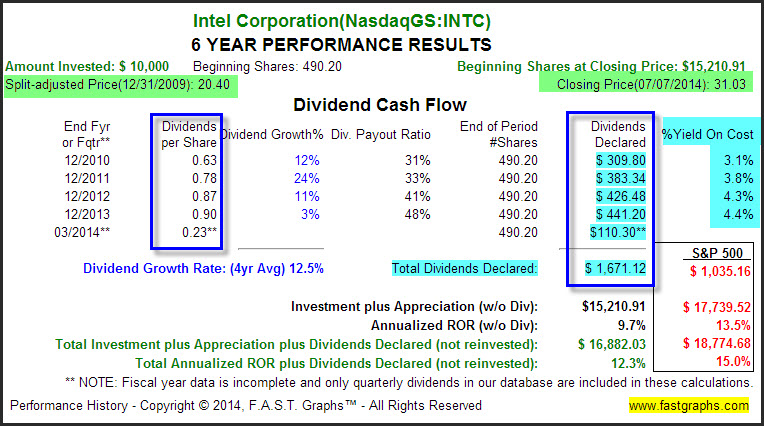

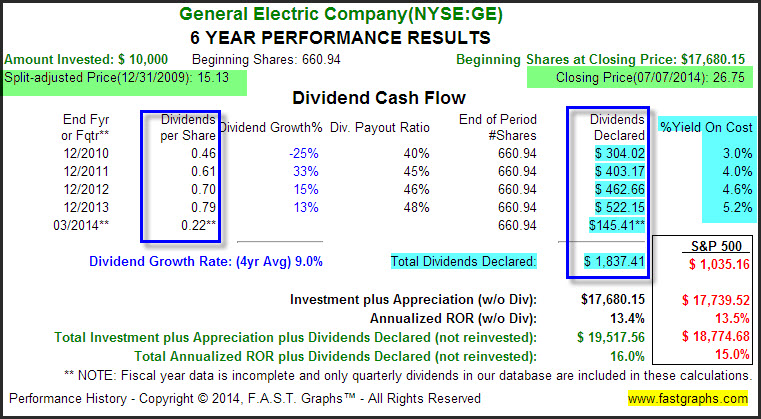

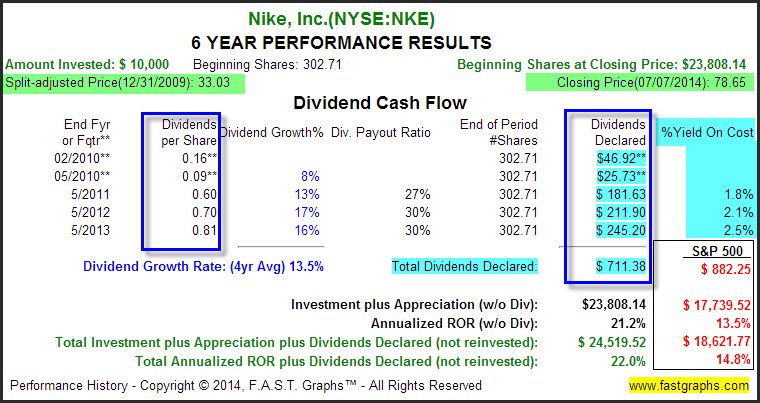

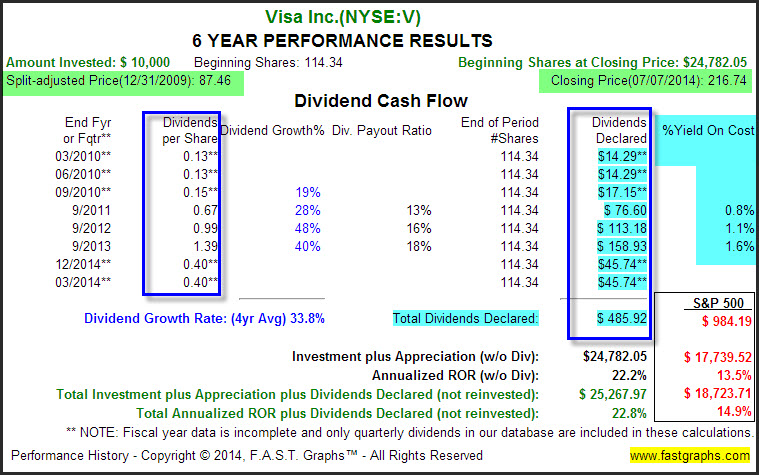

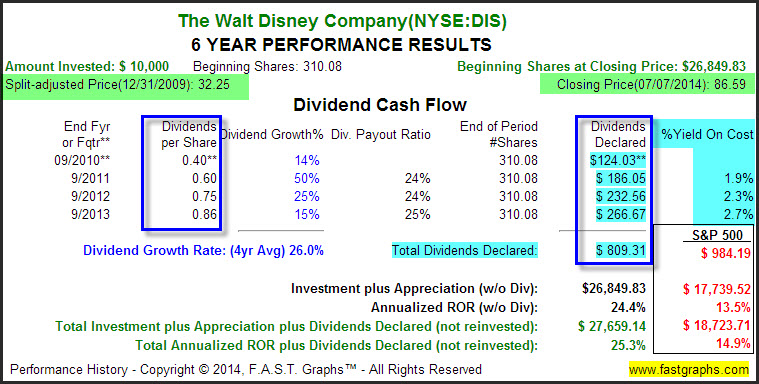

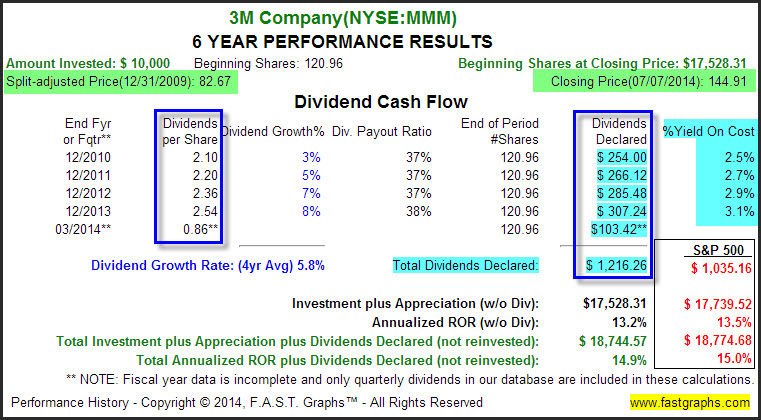

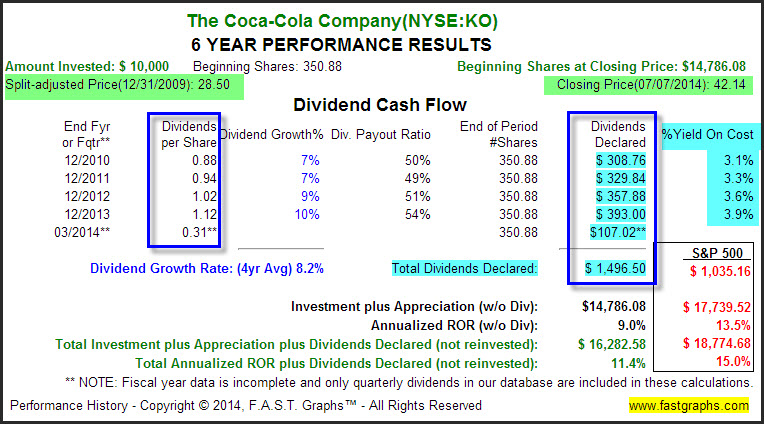

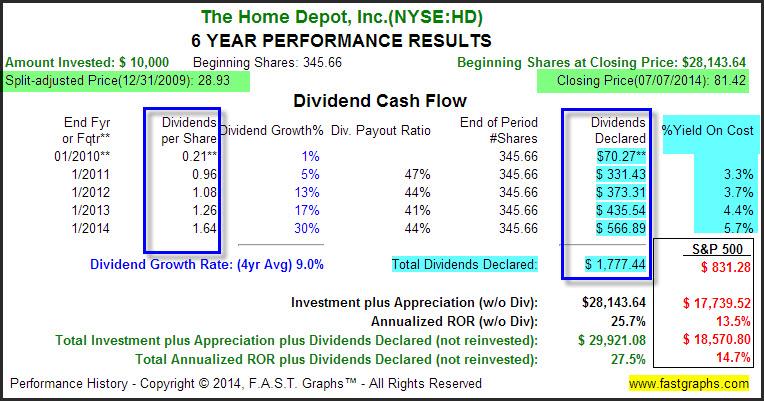

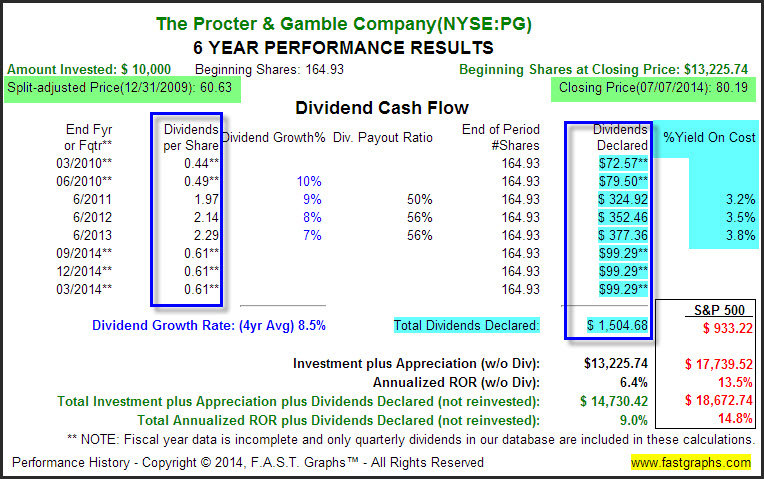

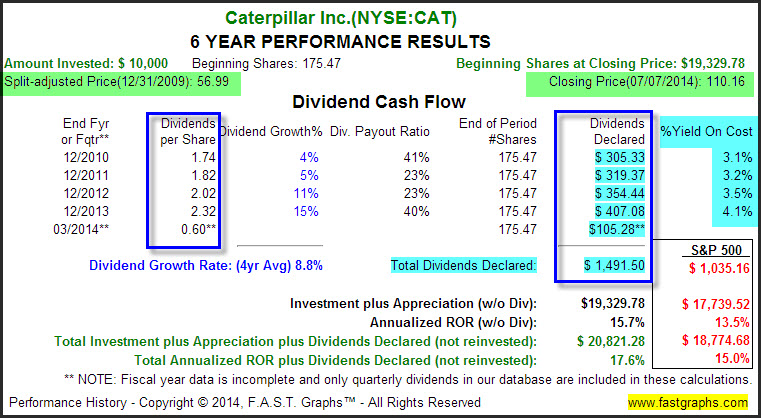

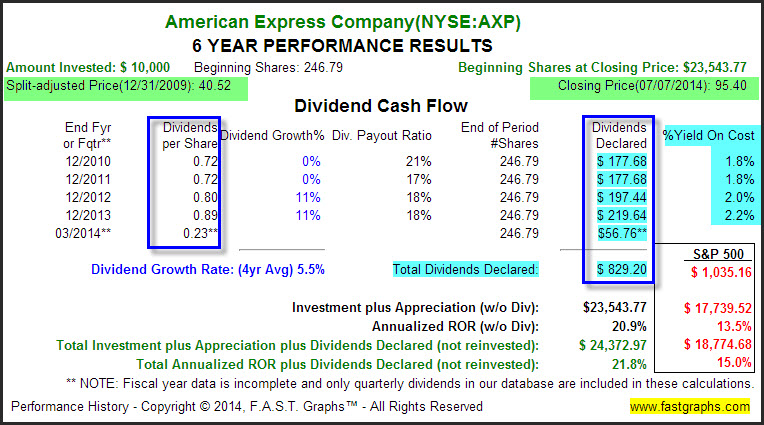

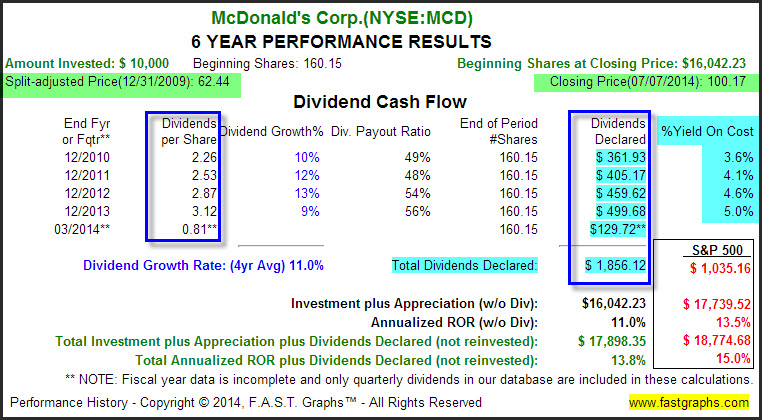

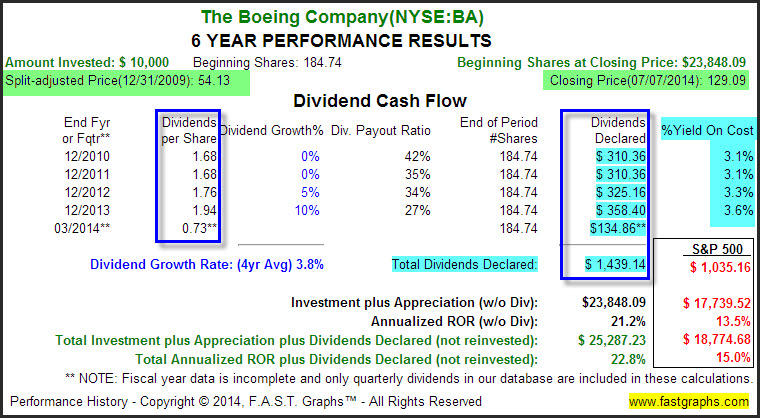

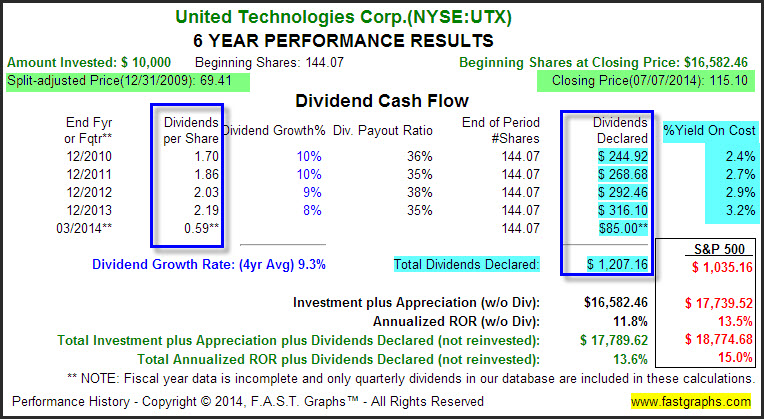

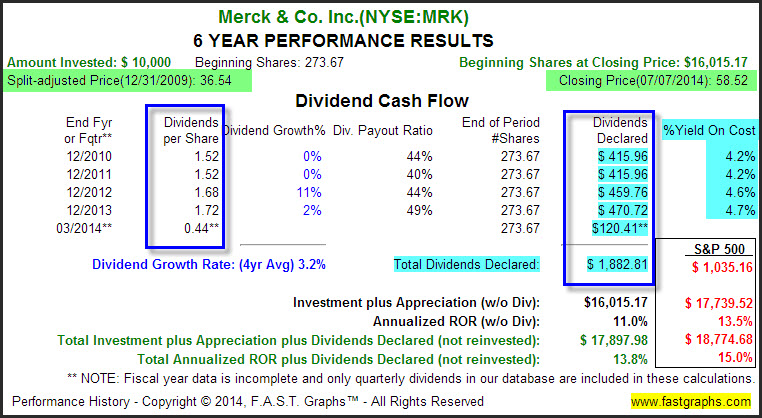

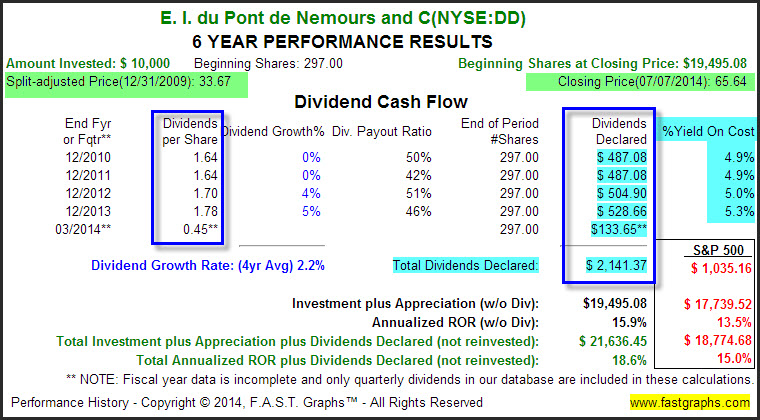

The second historical graph presents each company’s total return performance associated with the earnings and price correlated graphs. However, both components - capital appreciation and dividend income - are presented separately in order to evaluate the contribution from each. The Total Annualized ROR plus Dividends Declared (not reinvested) provides the final total return calculation. For perspective, the returns are also compared to the S&P 500.

Forecasting Graphs

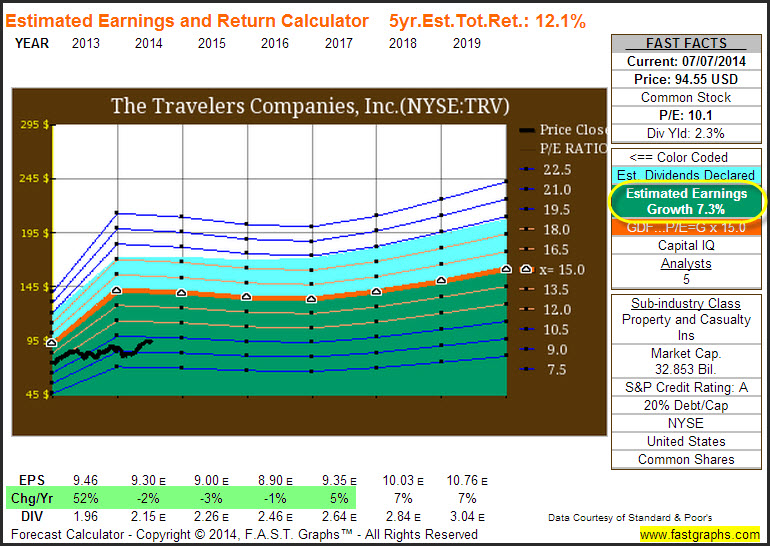

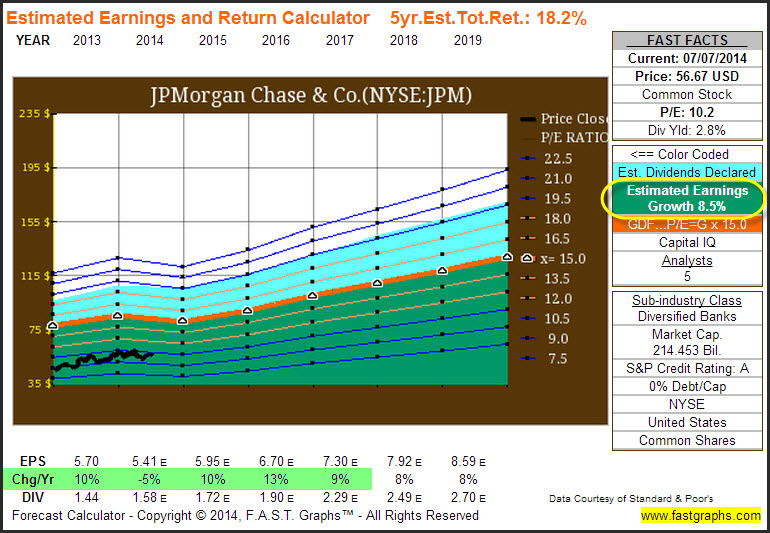

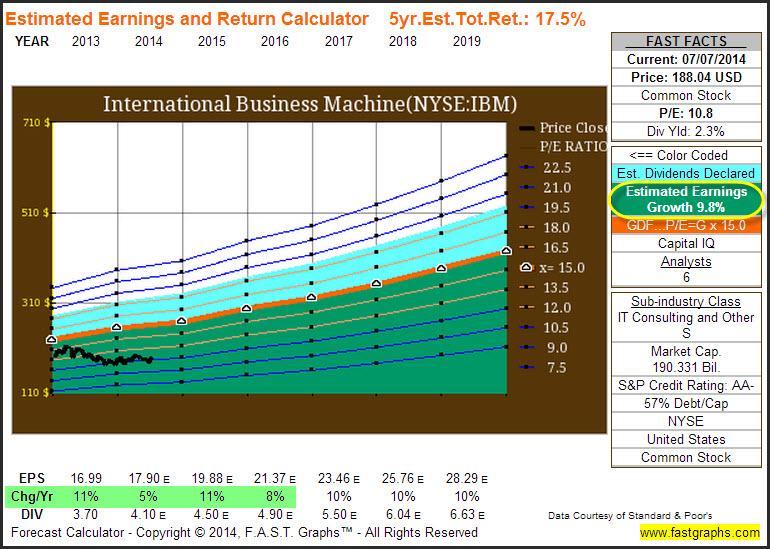

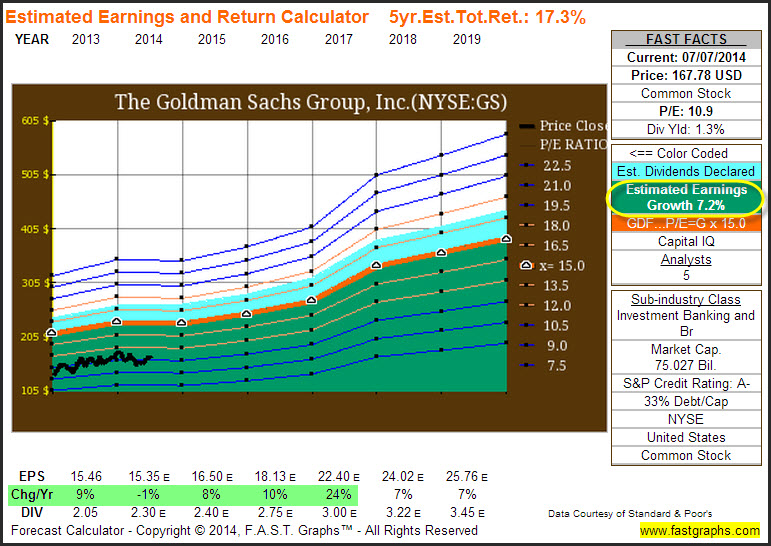

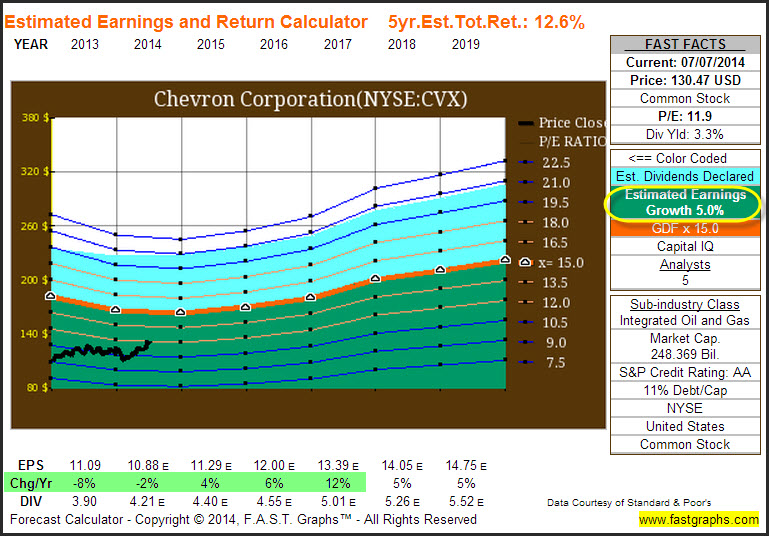

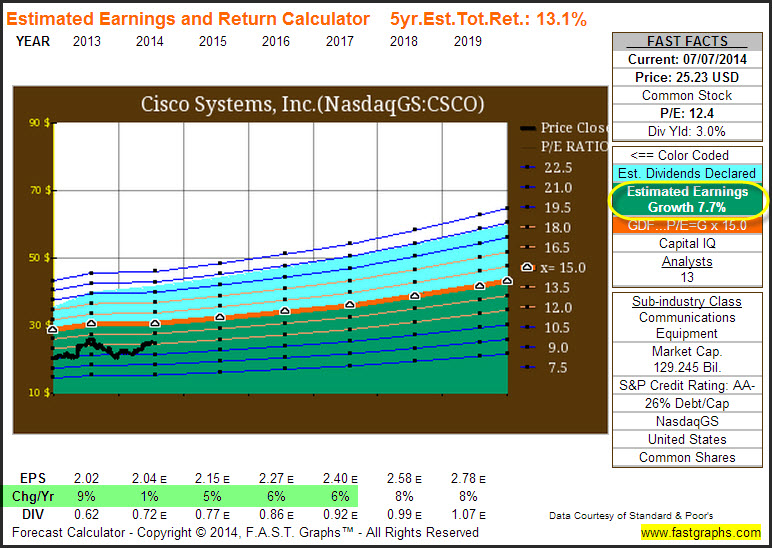

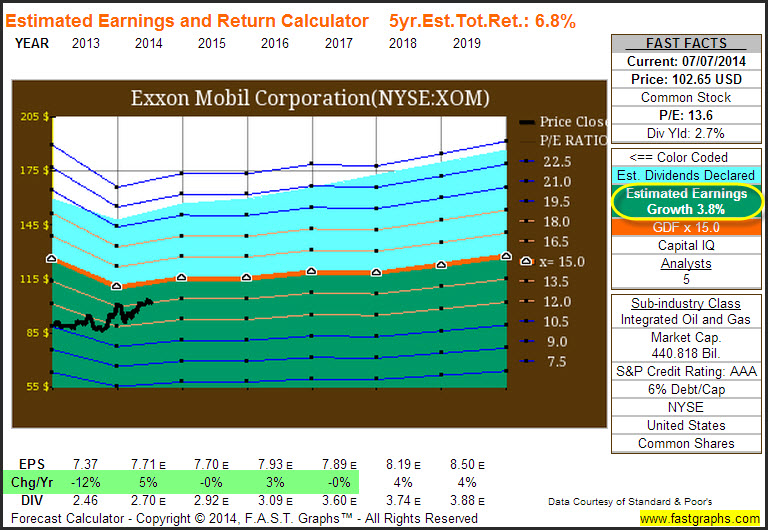

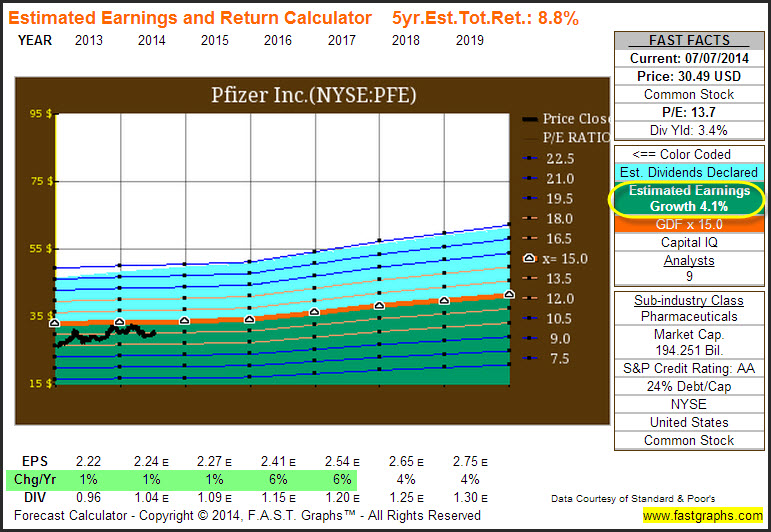

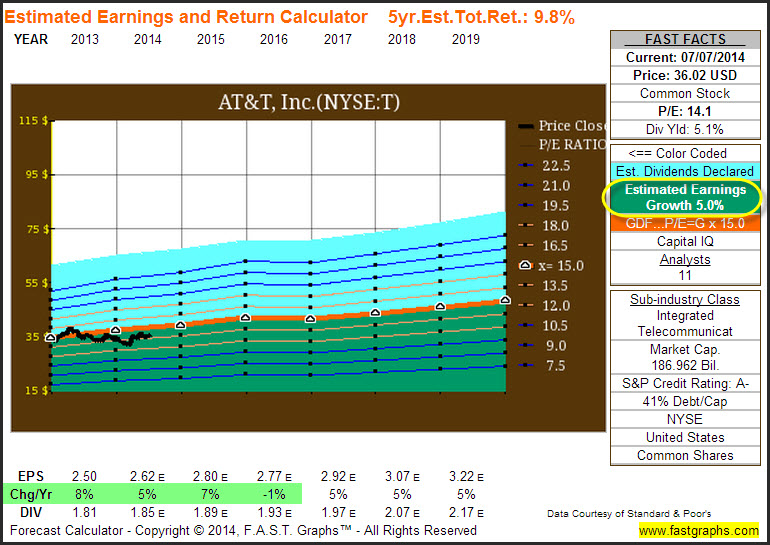

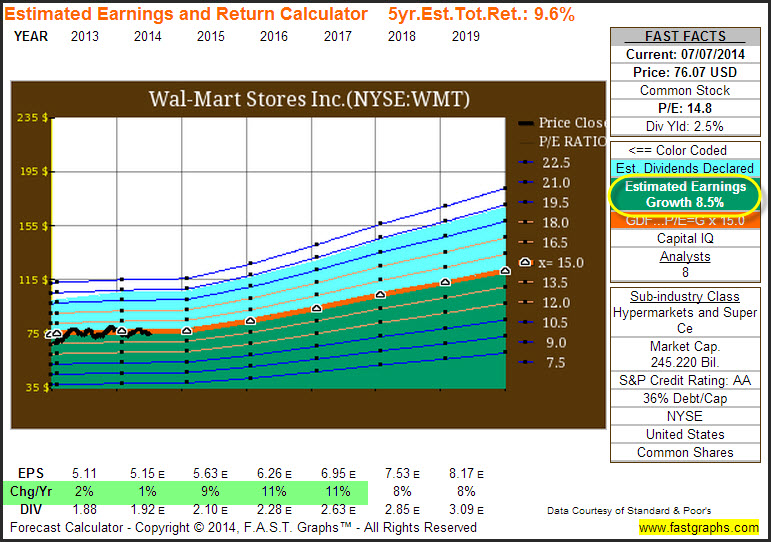

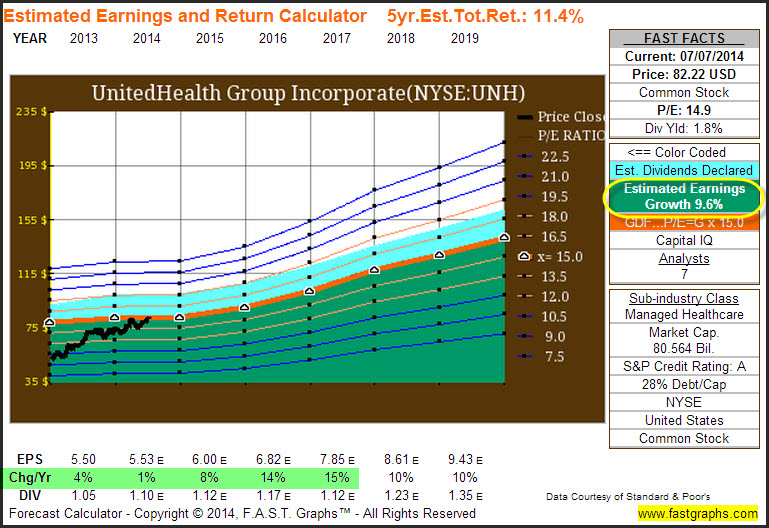

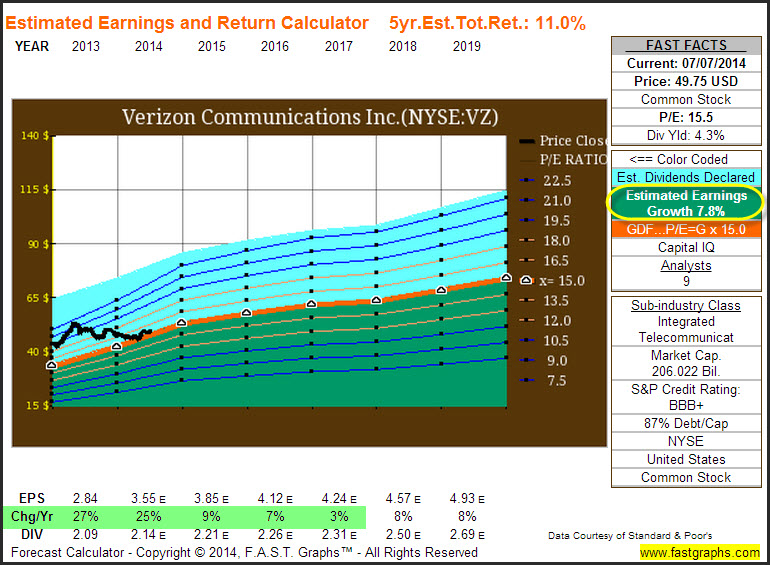

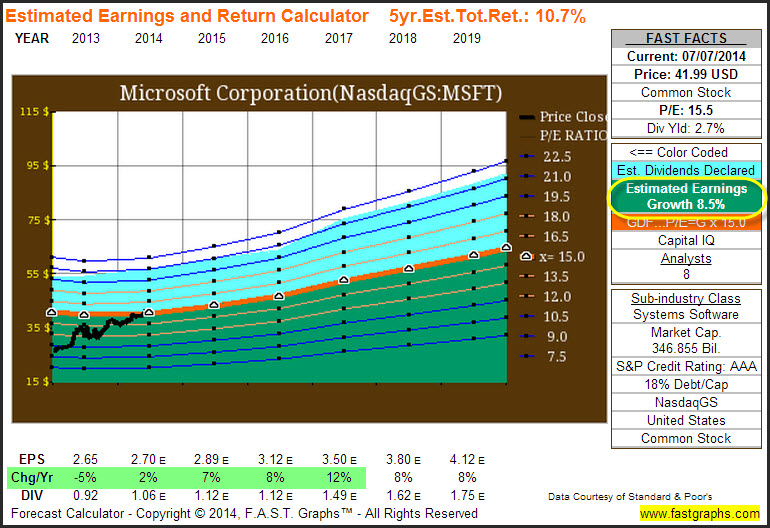

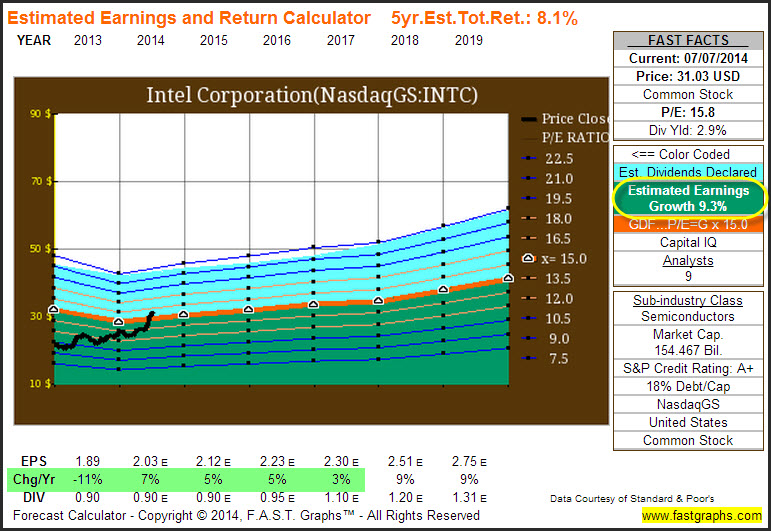

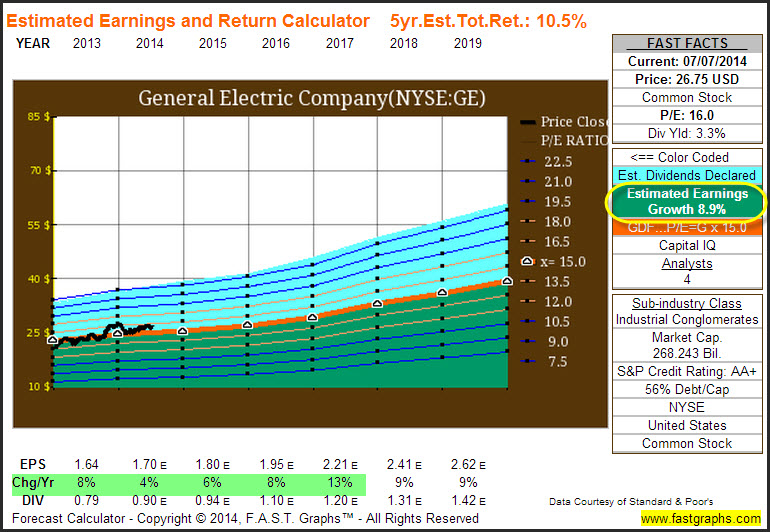

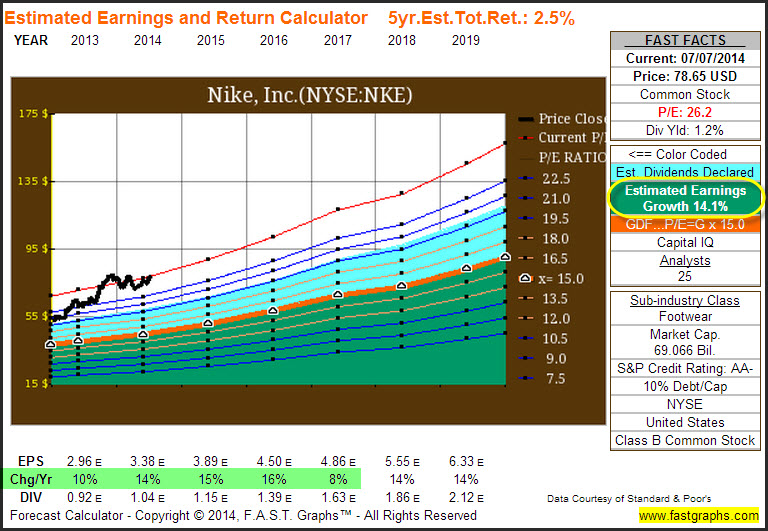

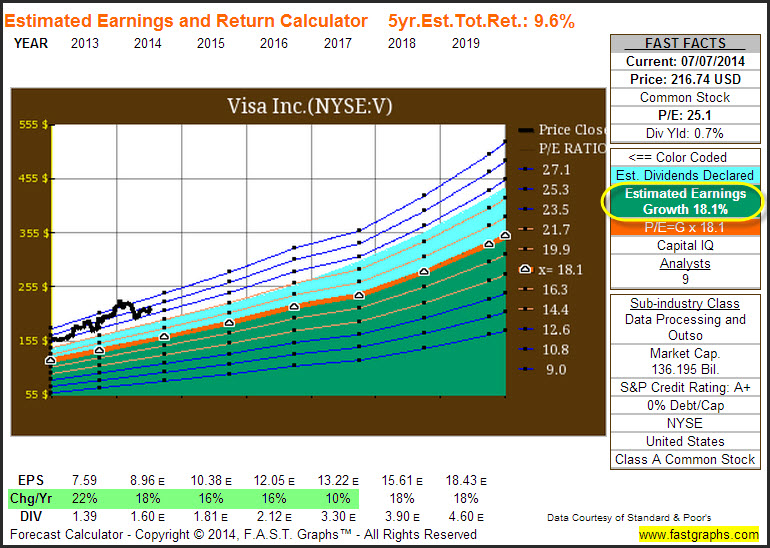

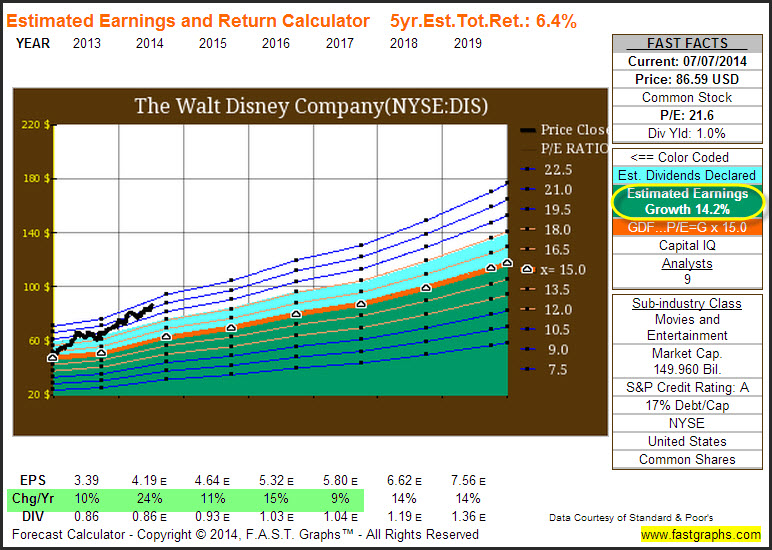

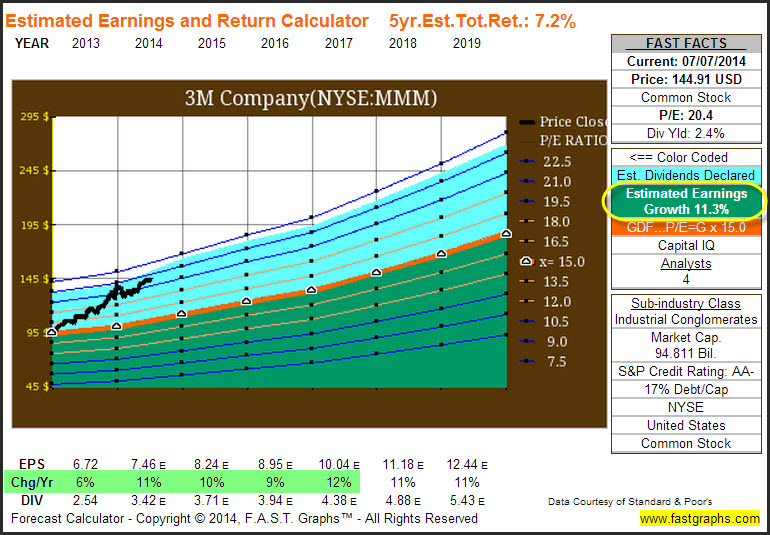

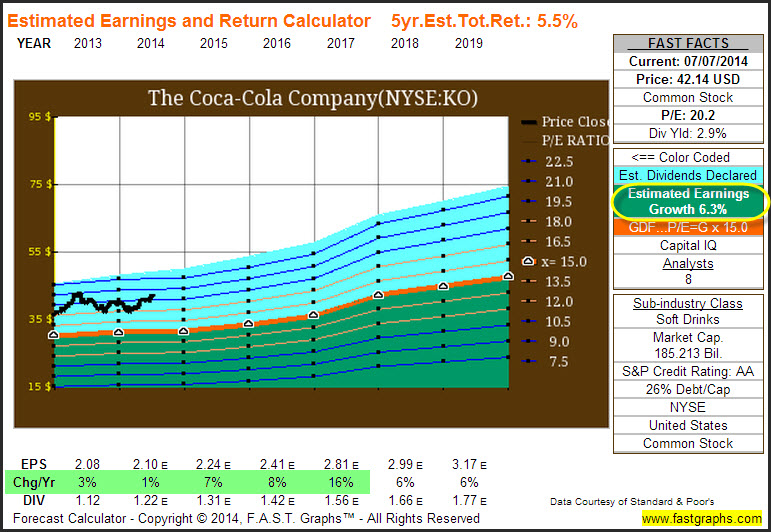

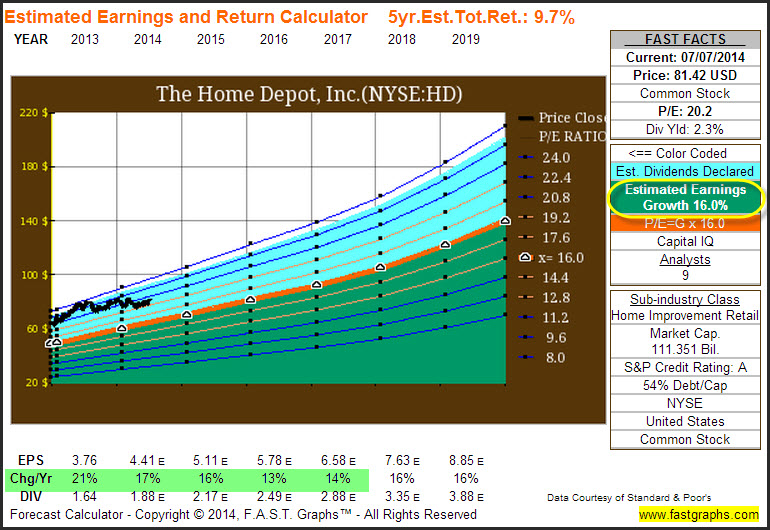

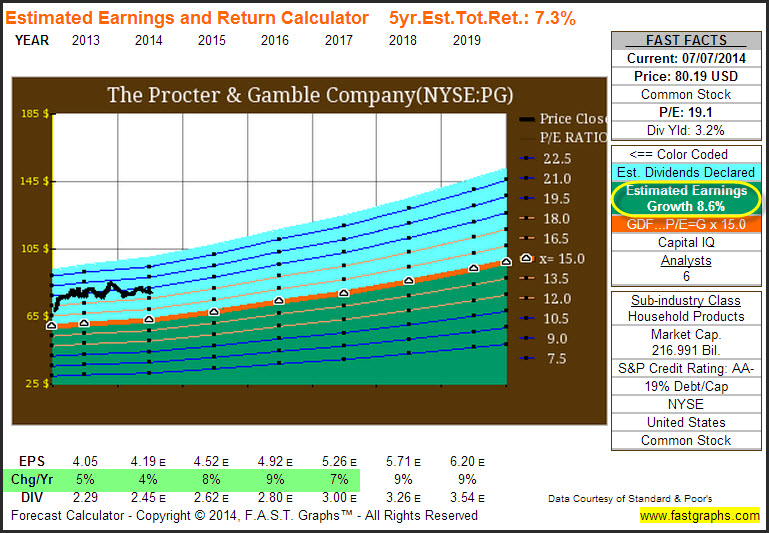

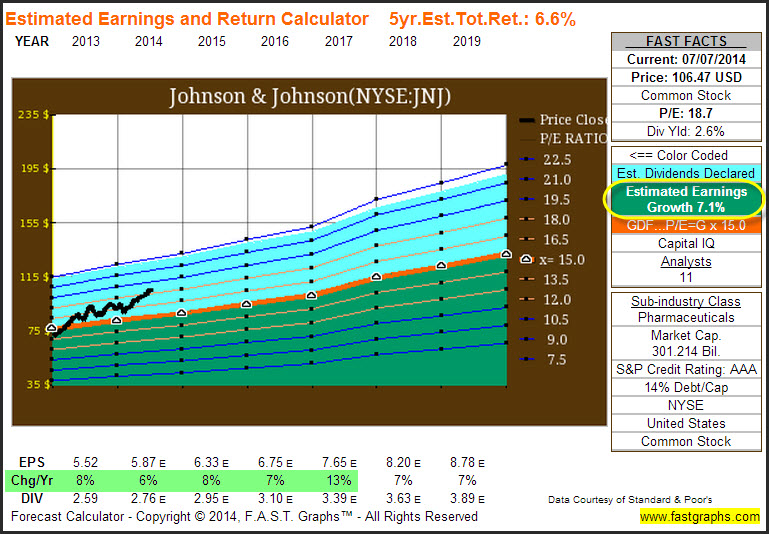

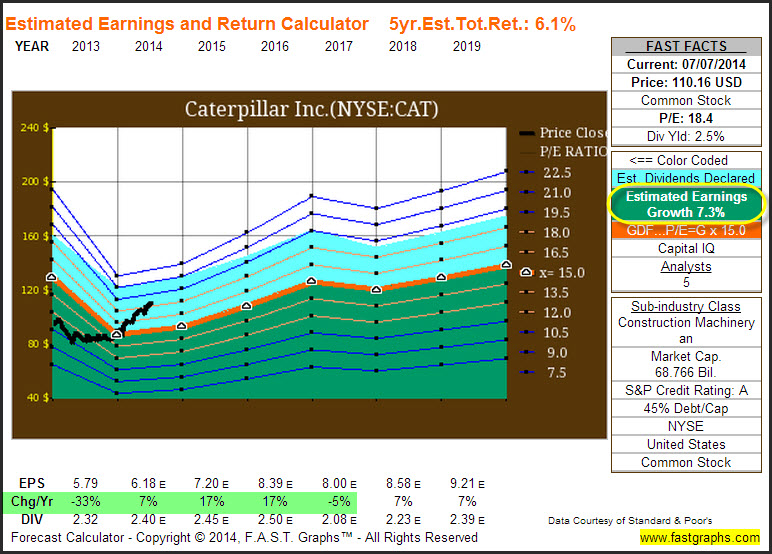

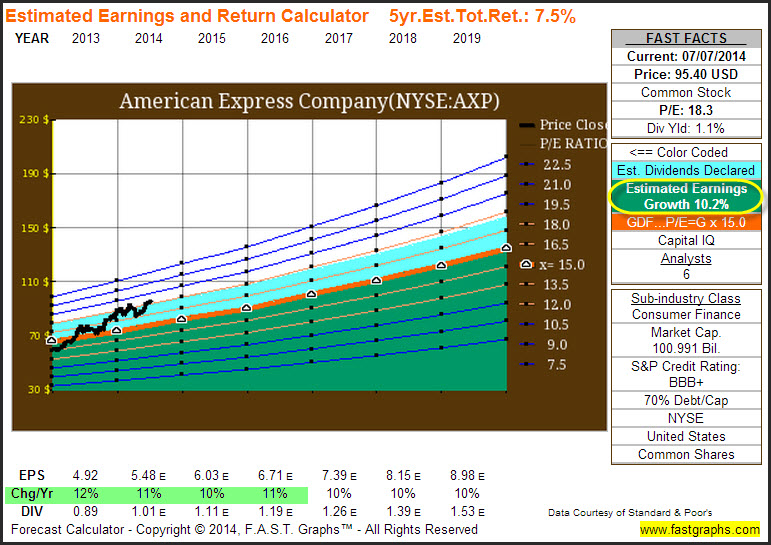

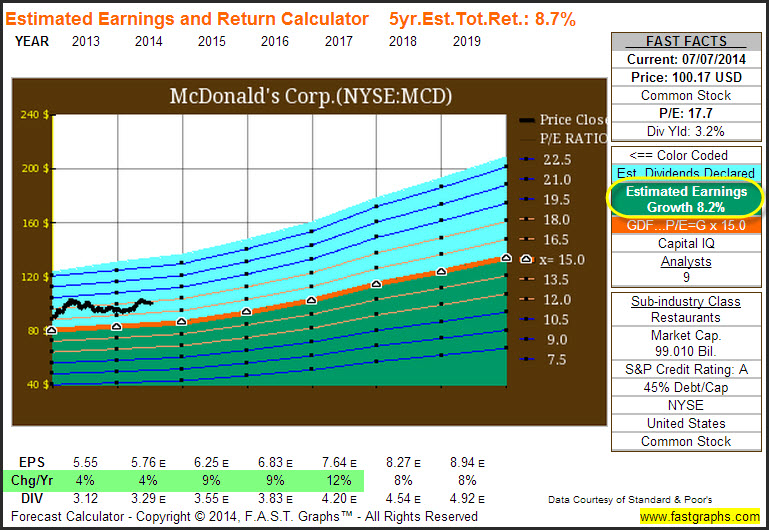

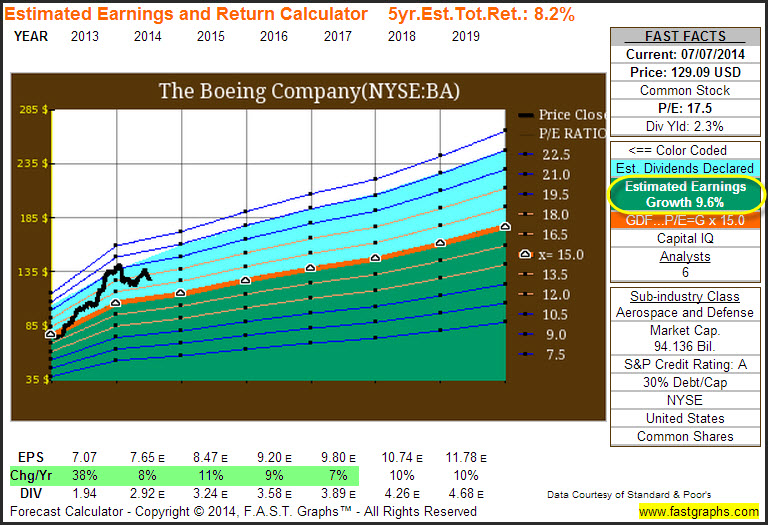

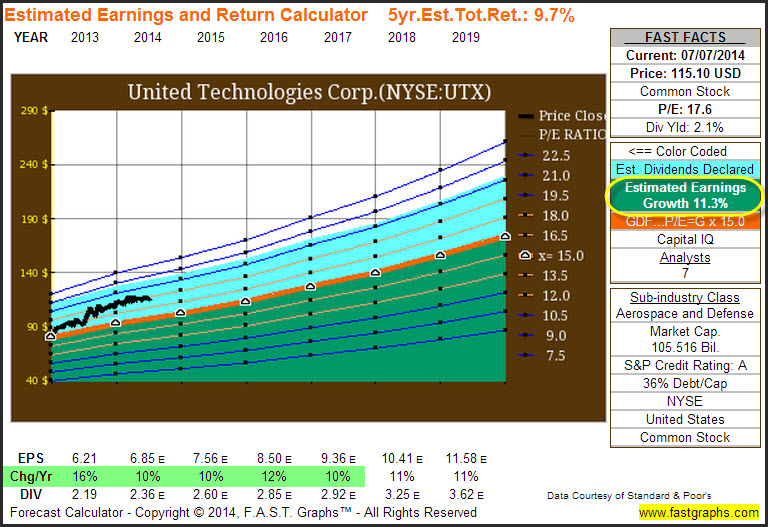

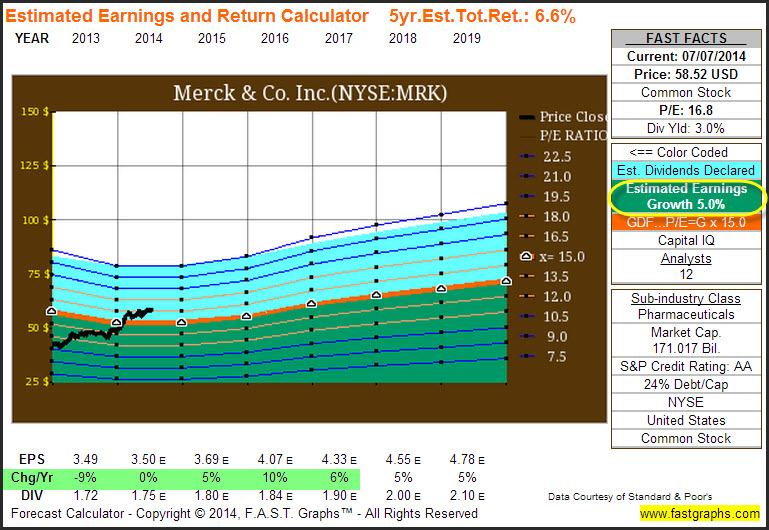

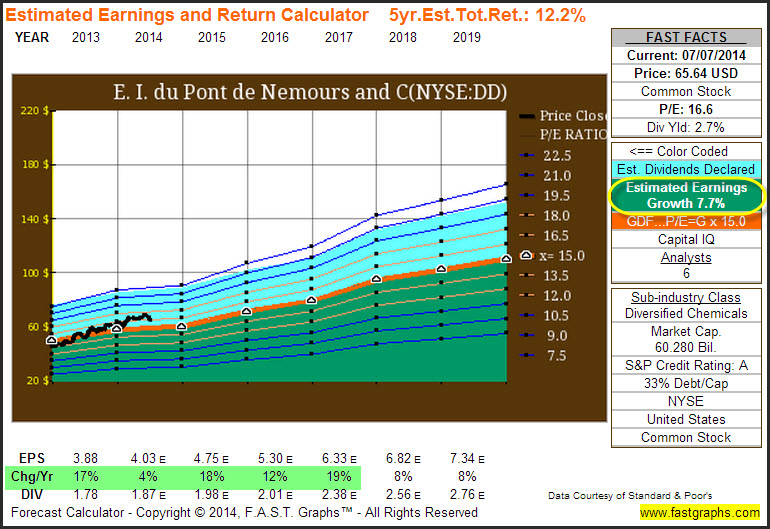

Following the historical graphs are the “Estimated Earnings and Return Calculator” based on consensus analysts’ estimates as reported by Standard & Poor’s Capital IQ. This graph includes several separate estimate items. For most companies a specific estimate is provided for the current year and up to three years forward, with the remaining years on the graph simply extrapolating the long-term growth forecast. It is suggested that the reader focuses on estimates for the current year and one year forward as they are likely to be more accurate and reliable.

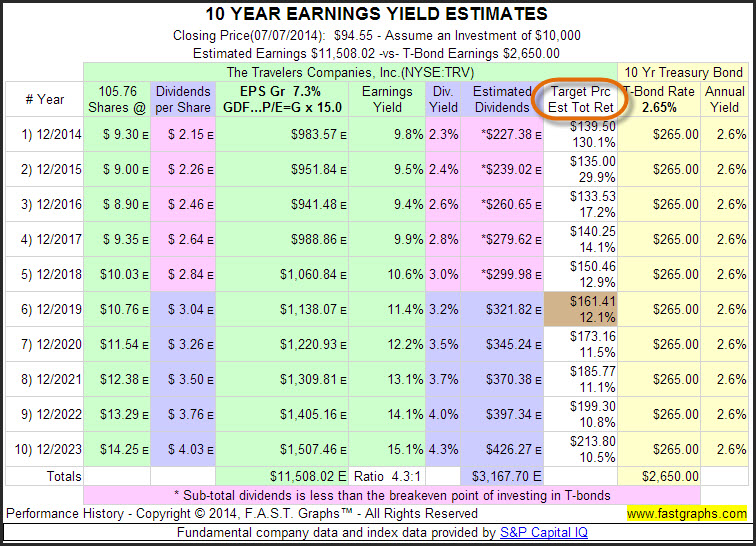

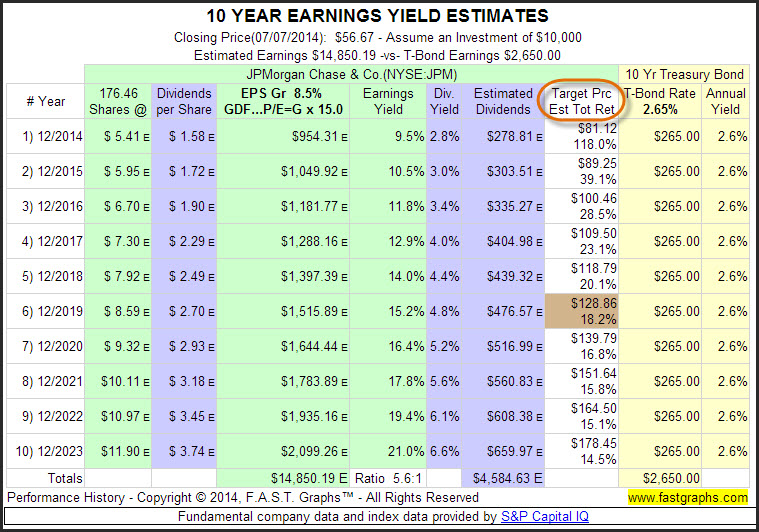

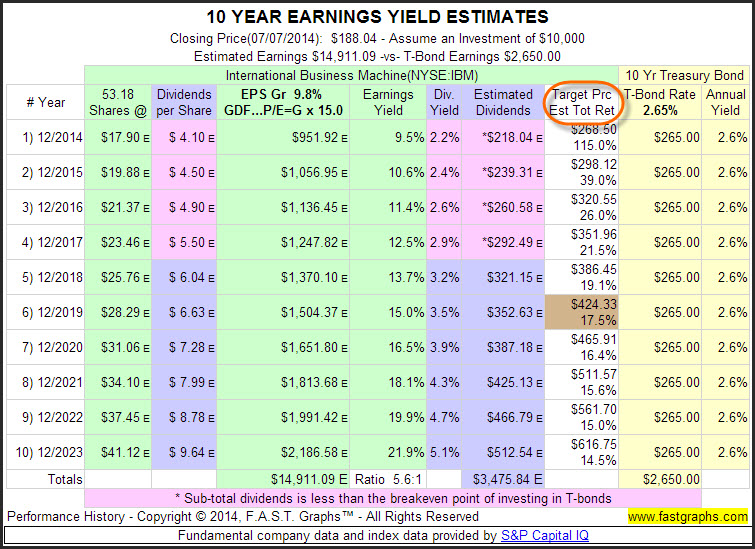

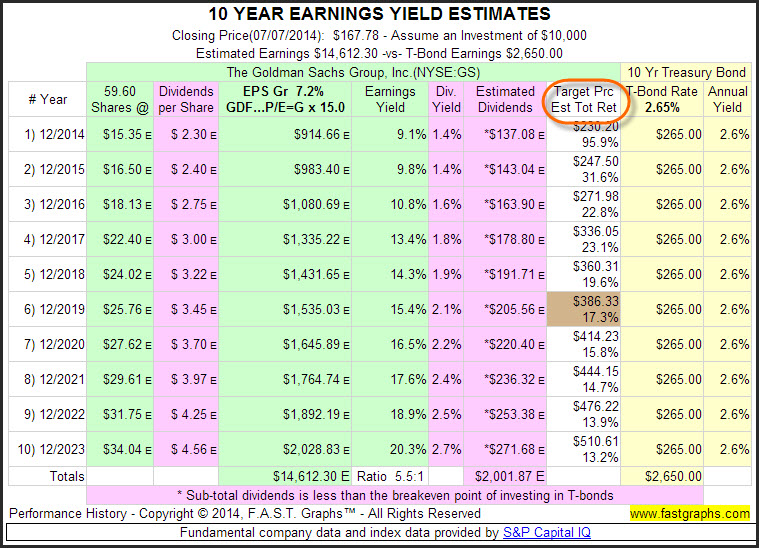

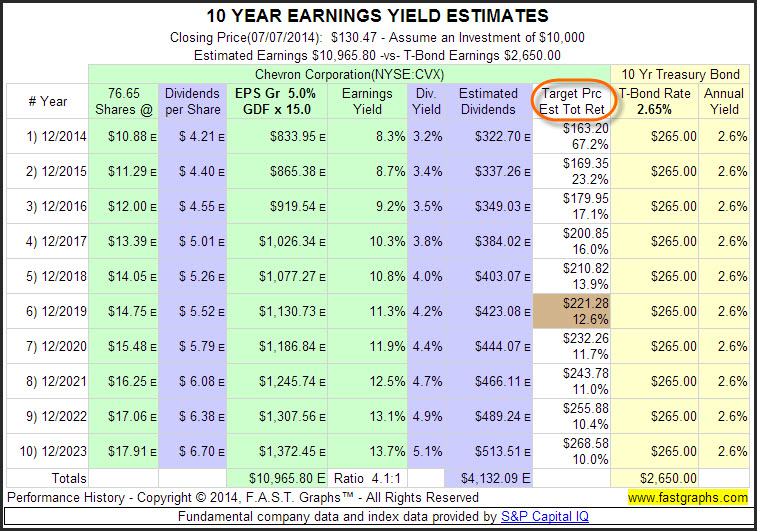

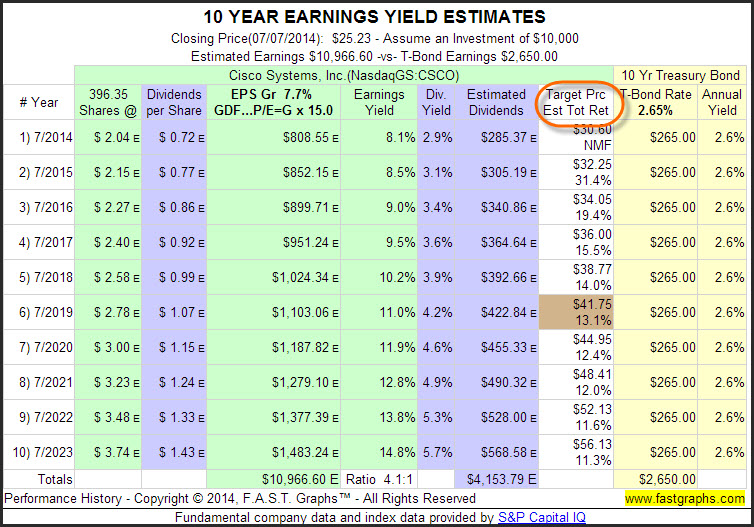

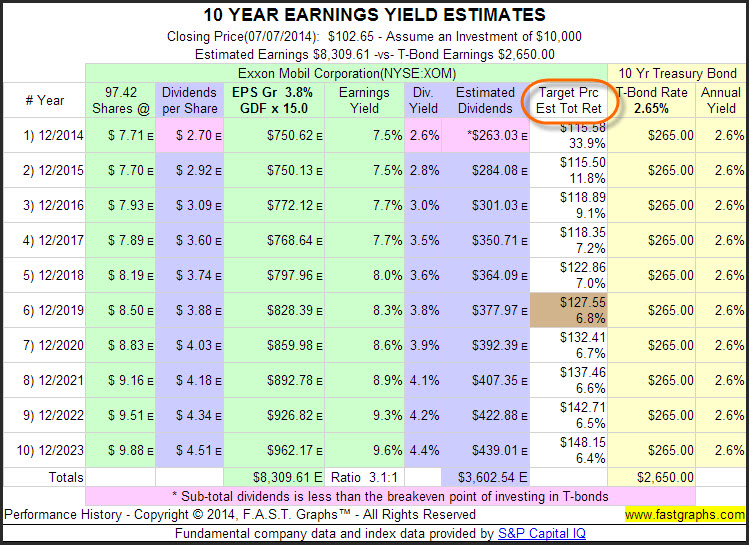

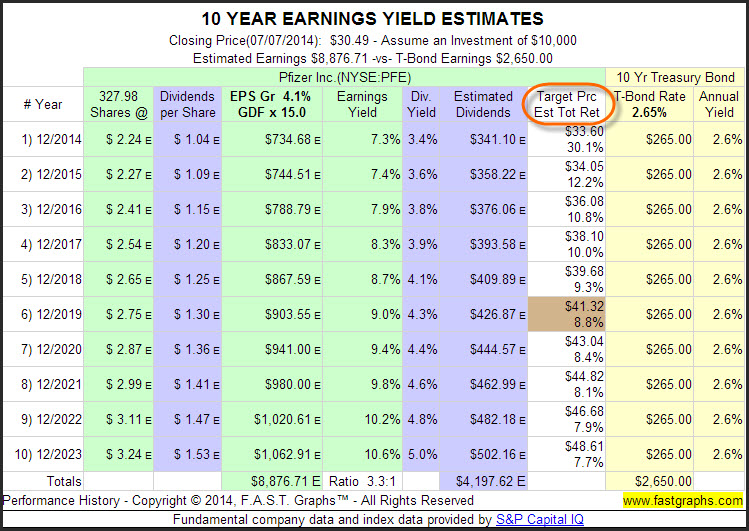

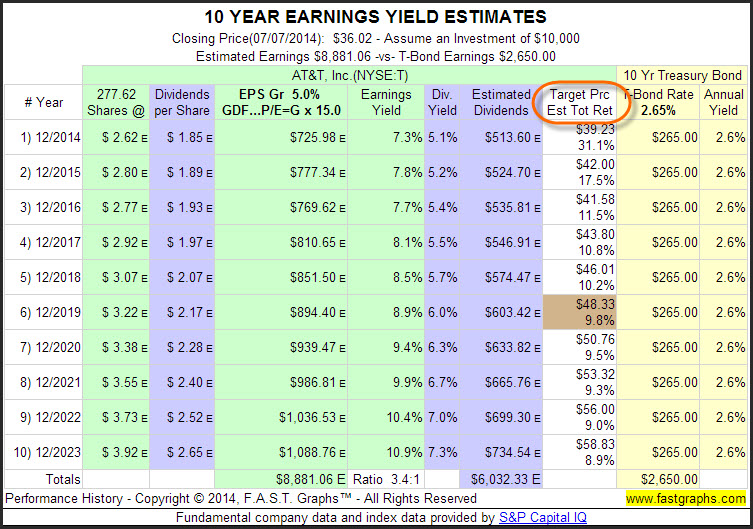

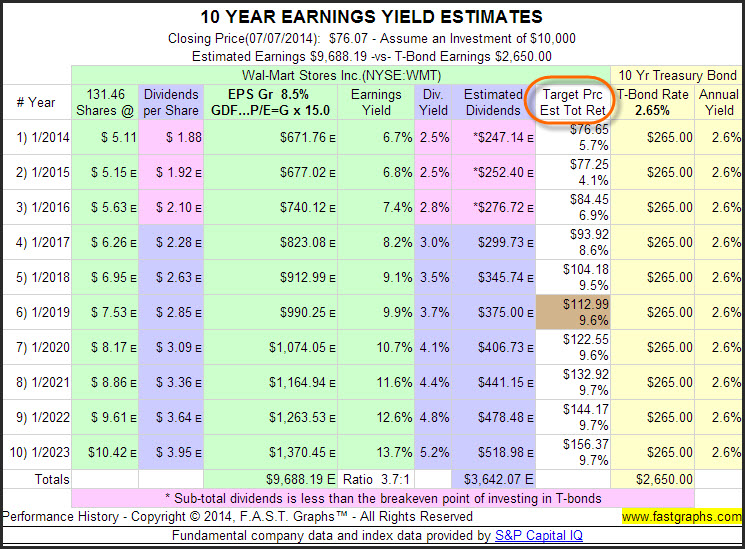

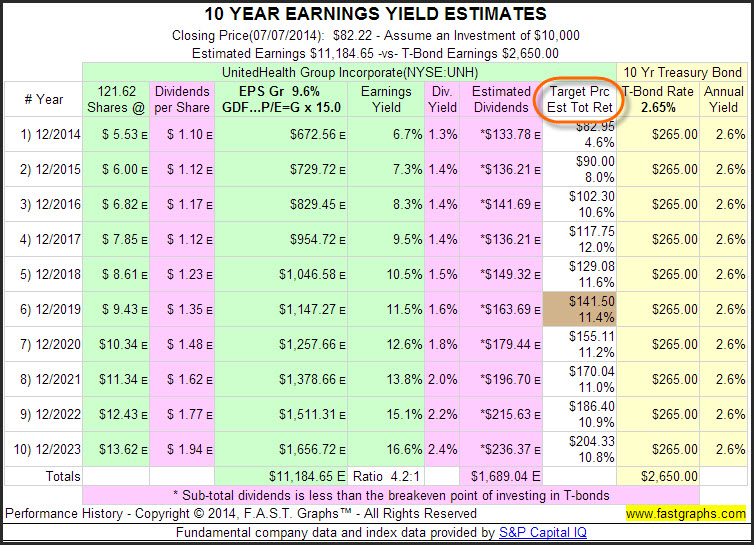

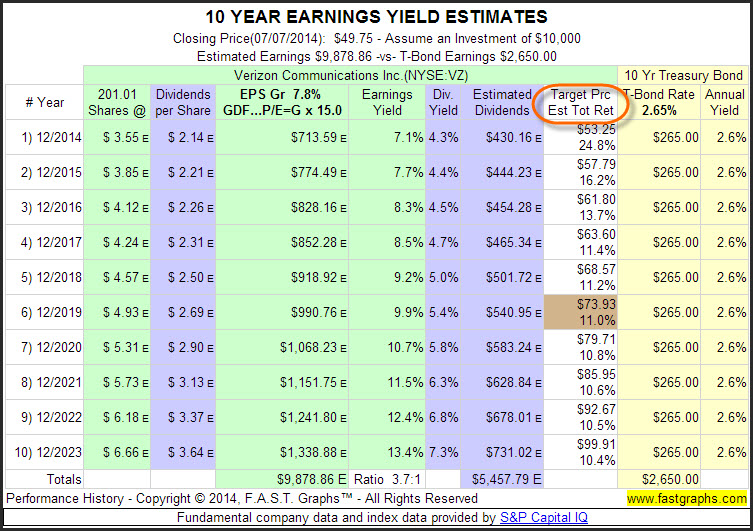

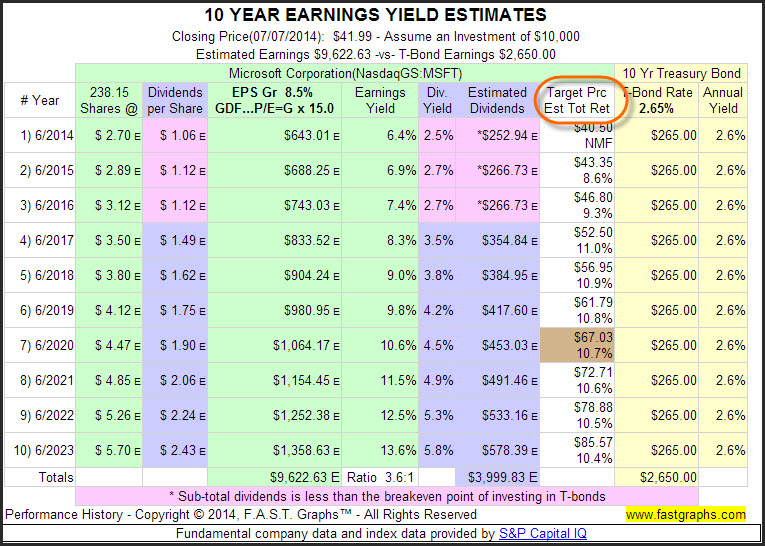

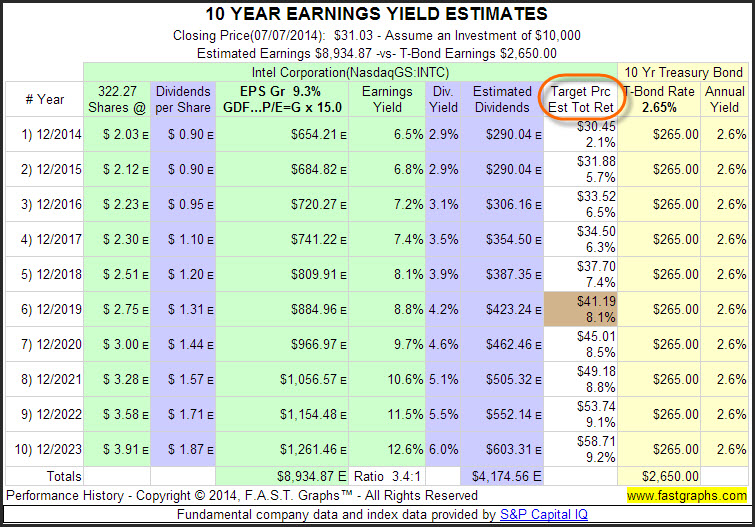

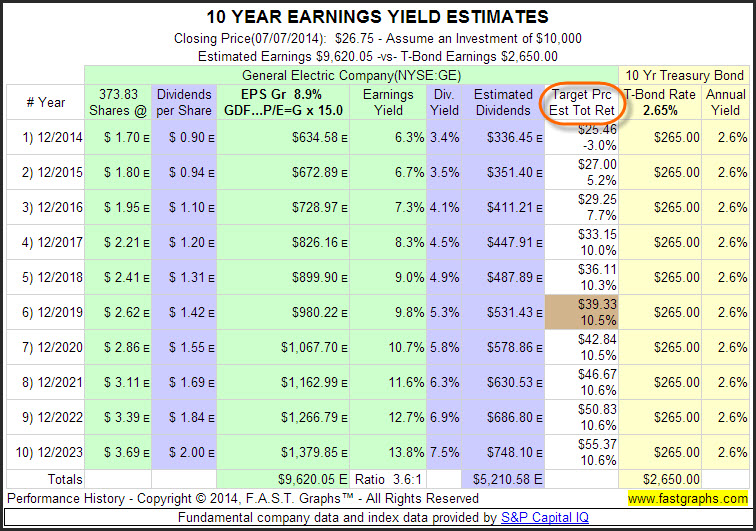

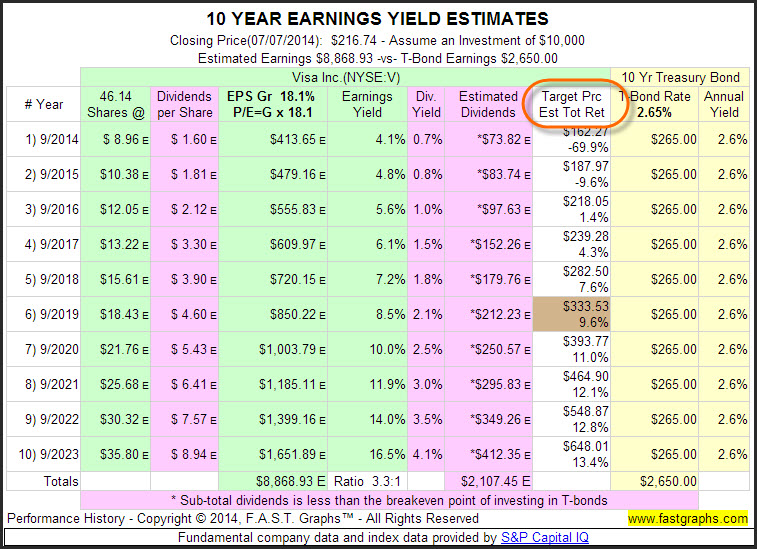

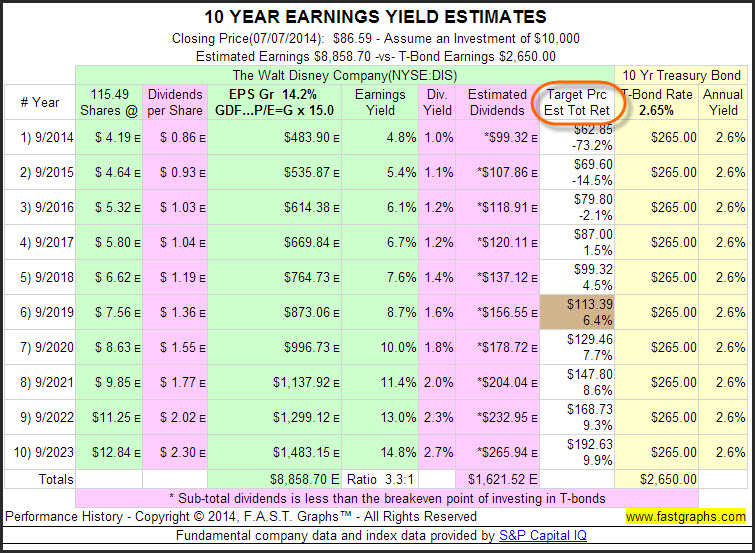

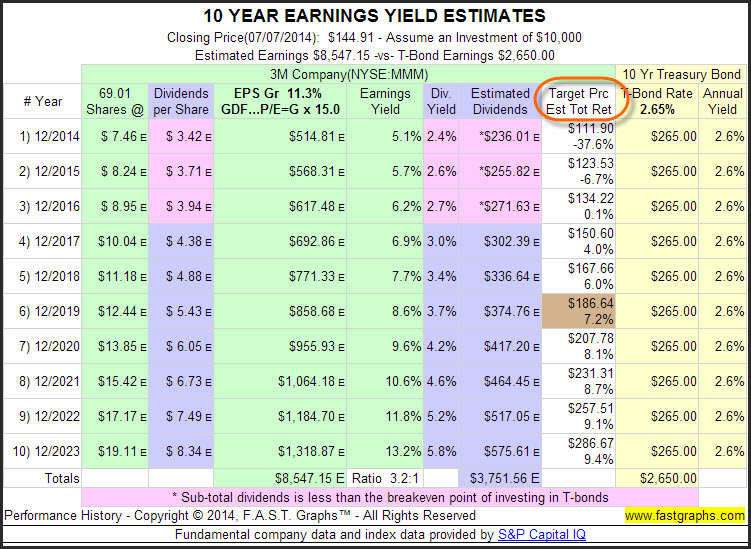

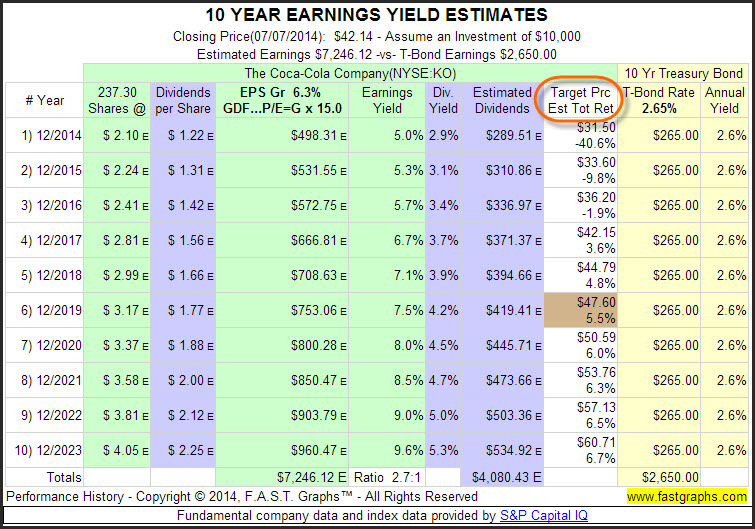

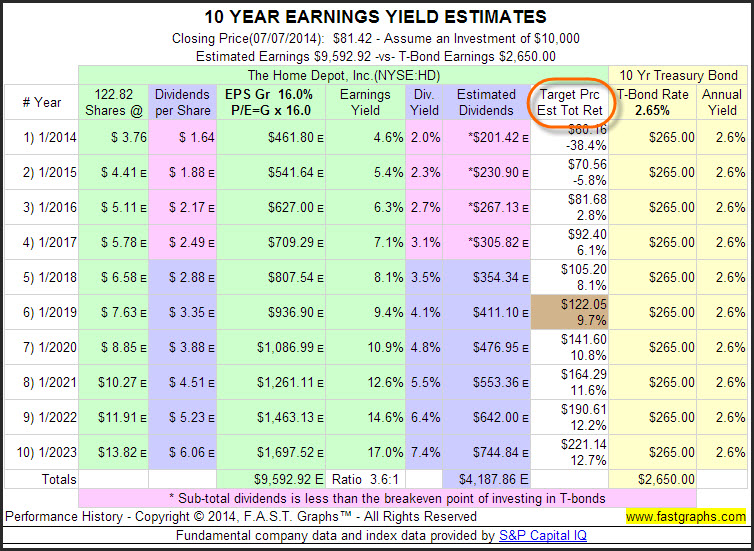

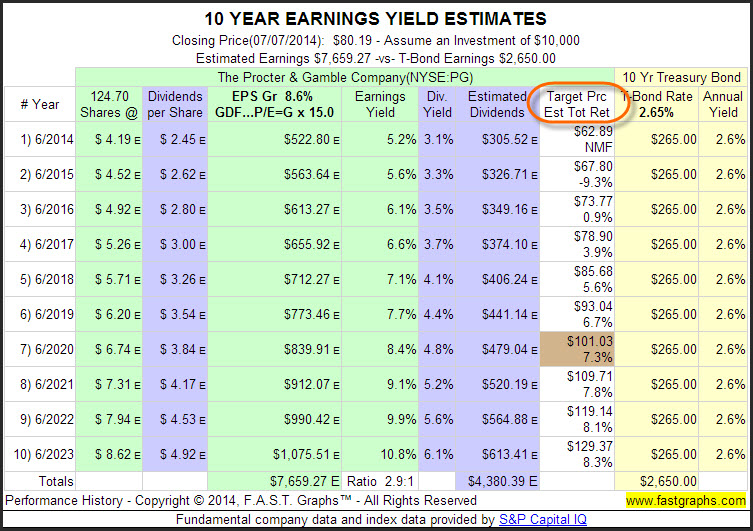

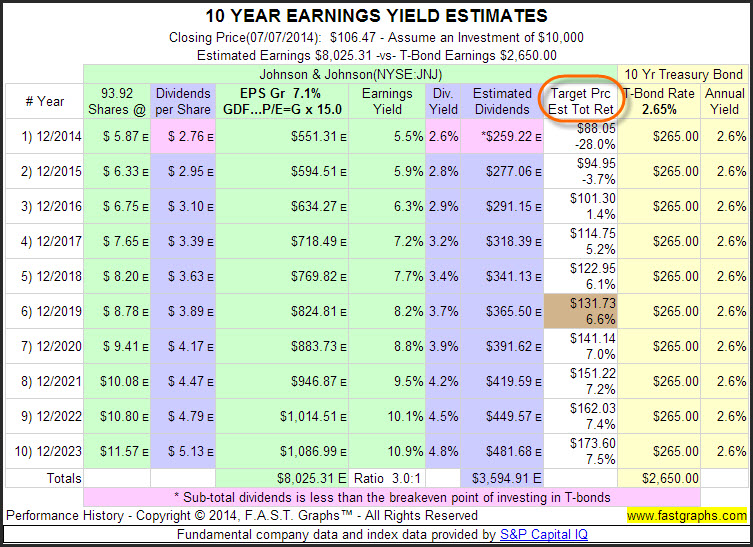

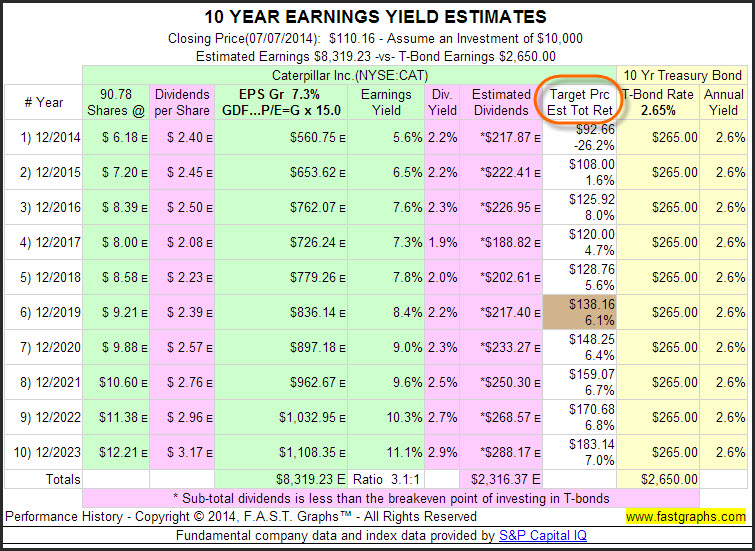

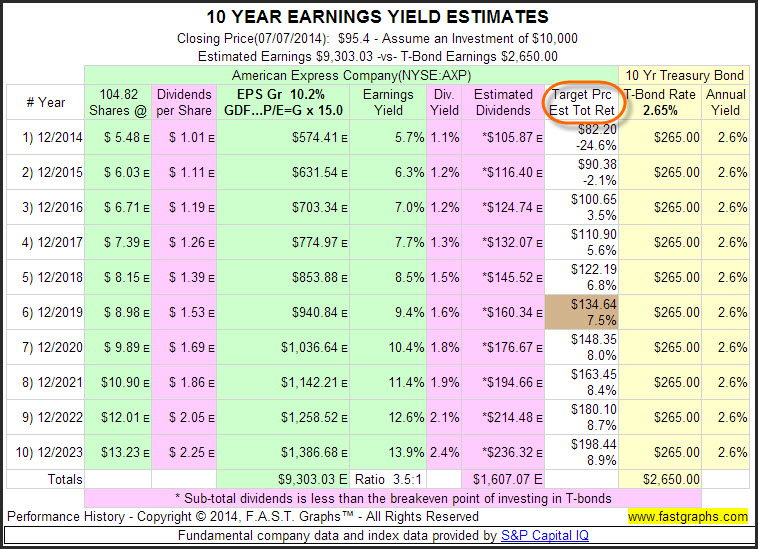

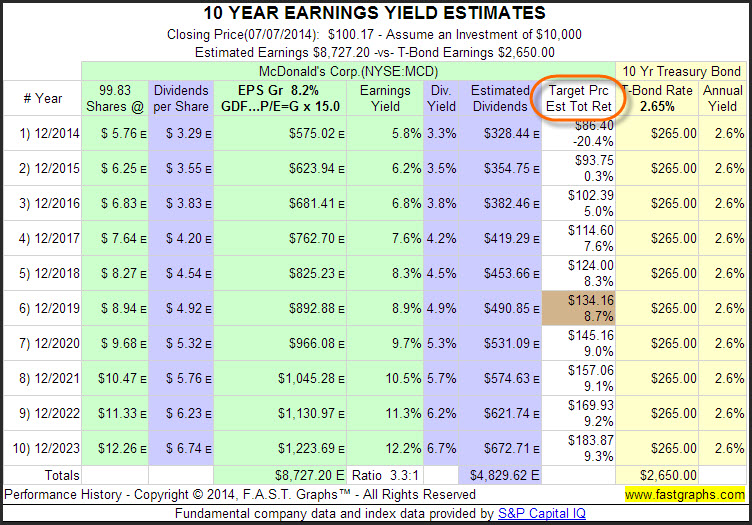

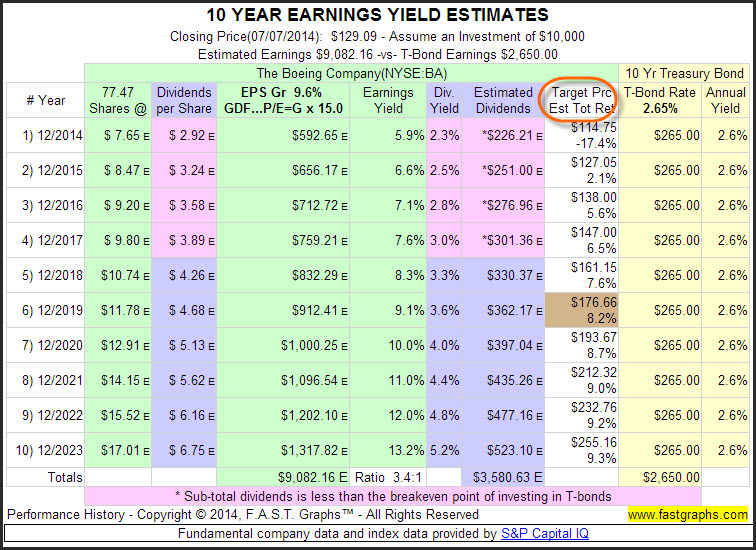

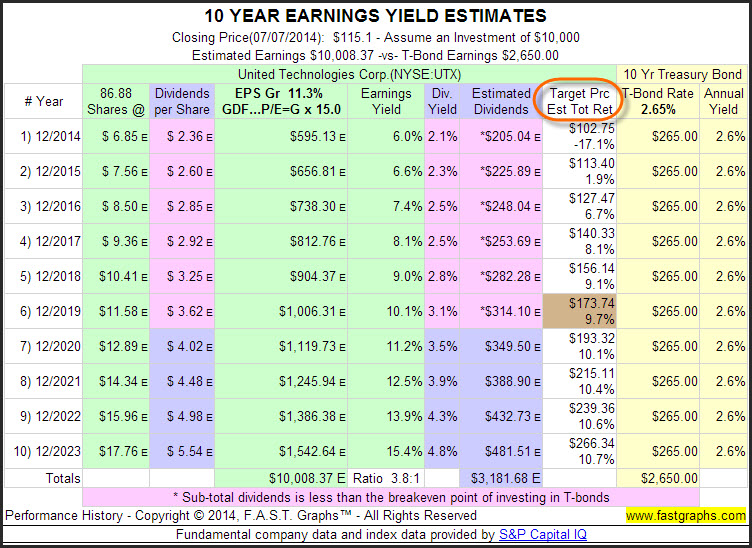

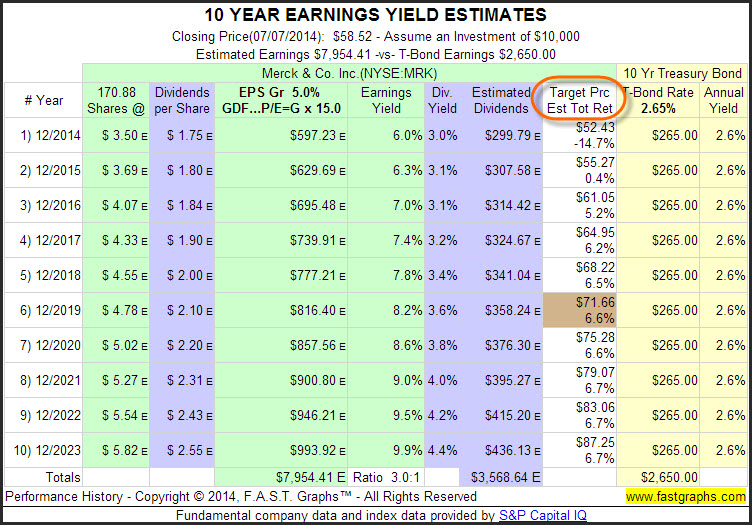

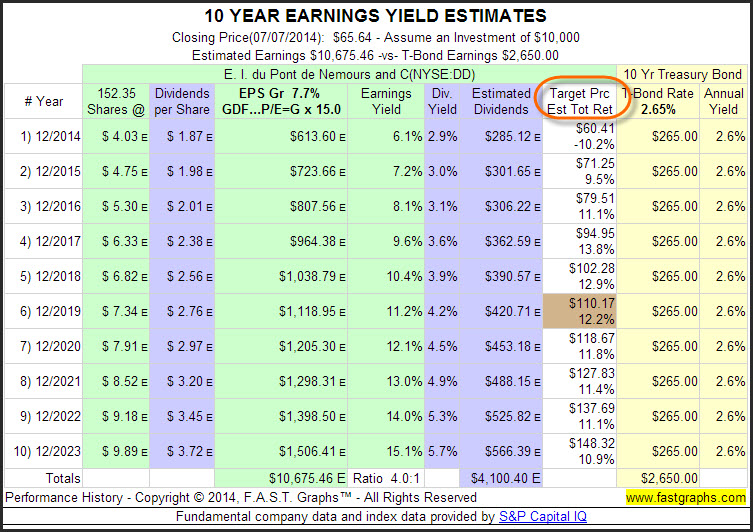

The final forecasting graph is the “10 YEAR EARNINGS YIELD ESTIMATES” table. Simply stated, this table reflects the previous graph in numerical form. For purposes of this article the most important column that the reader should focus on is the “Earnings Yield” column. This shows the current earnings yield as well as potential future growth of earnings yield based on consensus estimates.

The Travelers Companies Inc (TRV)

“The Travelers Companies, Inc., through its subsidiaries, provides a range of commercial, and personal property and casualty insurance products and services to businesses, government units, associations, and individuals.”

JP Morgan Chase & Co (JPM)

“JPMorgan Chase & Co., a financial holding company, operates as a financial services company in the United States of America. Under the J.P. Morgan and Chase brands, the company serves the U.S. and corporate, institutional and government clients worldwide.”

International Business Machine (IBM)

“International Business Machines Corporation provides integrated solutions, such as consulting, delivery and implementation services, enterprise software, systems and financing.”

The Goldman Sachs Group Inc (GS)

“The Goldman Sachs Group, Inc. operates as an investment banking, securities, and investment management company worldwide.”

Chevron Corporation (CVX)

“Chevron Corporation, through its subsidiaries, is engaged in the integrated petroleum, chemicals, mining, and power and energy services operations.”

Cisco Systems Inc (CSCO)

“Cisco Systems, Inc. designs, manufactures, and sells Internet protocol (IP) based networking and other products related to the communications and information technology (IT) industry. The company provides a line of products for transporting data, voice, and video within buildings, across campuses, and around the world.”

Exxon Mobil Corporation (XOM)

Exxon Mobil Corporation (XOM)

“Exxon Mobil Corporation manufactures and markets commodity petrochemicals, including olefins, aromatics, polyethylene and polypropylene plastics, and a variety of specialty products. The company also has interests in electric power generation facilities.

The company’s principal business is energy, involving exploration for, and production of, crude oil and natural gas, manufacture of petroleum products and transportation and sale of crude oil, natural gas and petroleum products.”

Pfizer Inc (PFE)

Pfizer Inc (PFE)

“Pfizer Inc. operates as a research-based, global biopharmaceutical company. The company’s portfolio includes medicines and vaccines, as well as consumer healthcare products. The company collaborates with healthcare providers, governments and local communities to support and expand access to affordable healthcare around the world.”

AT&T Inc (T)

AT&T Inc (T)

“AT&T Inc. provides telecommunications services in the United States and internationally. The company offers its services and products to consumers in the U.S. and services and products to businesses and other providers of telecommunications services worldwide.”

Wal-Mart Stores Inc (WMT)

Wal-Mart Stores Inc (WMT)

“Wal-Mart Stores, Inc. operates retail stores in various formats worldwide.”

UnitedHealth Group Inc (UNH)

“UnitedHealth Group Incorporated operates as a health and well-being company.”

Verizon Communications Inc (VZ)

Verizon Communications Inc (VZ)

“Verizon Communications Inc., through its subsidiaries, provides communications, information and entertainment products and services to consumers, businesses, and governmental agencies.”

Microsoft Corporation (MSFT)

“Microsoft Corporation engages in developing, licensing, and supporting a range of software products and services, by designing and selling hardware devices, and by delivering relevant online advertising to a customer audience worldwide.”

Intel Corporation (INTC)

“Intel Corporation designs, manufactures, and sells integrated digital technology platforms.”

General Electric Company (GE)

General Electric Company (GE)

“General Electric Company operates as an infrastructure and financial services company worldwide. With products and services ranging from aircraft engines, power generation, oil and gas production equipment, and household appliances to medical imaging, business and consumer financing and industrial products, the company serves customers in approximately 100 countries.”

Portfolio Review: 15 Fully Valued to Moderately Overvalued Dow Constituents

With the first portfolio review above we analyzed fairly valued Dow constituents. What follows here are a review of the 15 fully valued to moderately overvalued Dow constituents. The same analytical process for these 15 Dow components is applied. The only difference with this set of graphs is that they are presented in reverse order looking at the highest valuation to the lowest valuation in this set.

Nike Inc (NKE)

“Nike, Inc. engages in the design, development, and marketing of footwear, apparel, equipment, accessories, and services for men, women, and kids worldwide.”

Visa Inc (V)

“Visa Inc. operates as a payments technology company worldwide. The company connects consumers, businesses, financial institutions, and governments in approximately 200 countries and territories to electronic payments.”

Walt Disney Company (DIS)

“The Walt Disney Company, together with its subsidiaries, operates as an entertainment company worldwide.”

3M Company (MMM)

“3M Company operates as a technology company worldwide. The company’s segments include Industrial; Safety and Graphics; Electronics and Energy; Health Care; and Consumer Businesses.”

Coca-Cola Company (KO)

Coca-Cola Company (KO)

“The Coca-Cola Company operates as a beverage company worldwide.”

Home Depot Inc (HD)

“The Home Depot, Inc. operates as a home improvement retailer worldwide. The Home Depot stores sell an assortment of building materials, home improvement products, and lawn and garden products, as well as provide various services.”

Procter & Gamble Company (PG)

“The Procter & Gamble Company provides branded consumer packaged goods. The company’s products are sold in approximately 180 countries and territories primarily through retail operations including mass merchandisers, grocery stores, membership club stores, drug stores, department stores, salons, high-frequency stores and e-commerce. The company has on-the-ground operations in approximately 70 countries.”

Johnson & Johnson (JNJ)

“Johnson & Johnson, together with its subsidiaries, is engaged in the research and development, manufacture and sale of a range of products in the health care field. The business of the company is conducted by approximately 275 operating companies located in 60 countries, including the United States, which sell products in all countries worldwide.”

Caterpillar Inc (CAT)

“Caterpillar Inc. manufactures construction and mining equipment, diesel and natural gas engines, industrial gas turbines and diesel-electric locomotives.”

American Express Company (AXP)

American Express Company (AXP)

“American Express Company, together with its subsidiaries, provides charge and credit payment card products and travel-related services to consumers and businesses worldwide.”

McDonald’s Corp (MCD)

“McDonald’s Corporation franchises and operates McDonald’s restaurants in the restaurant industry. The company’s restaurants serve a menu at various price points in approximately 100 countries worldwide.”

The Boeing Company (BA)

“The Boeing Company, together with its subsidiaries, operates as an aerospace company worldwide.”

United Technologies Corp (UTX)

“United Technologies Corporation provides technology products and services to the building systems and aerospace industries worldwide.”

Merck & Co Inc (MRK)

Merck & Co Inc (MRK)

“Merck & Co., Inc., a health care company, offers health solutions through its prescription medicines, vaccines, biologic therapies, animal health, and consumer care products. The company’s operations are principally managed on a products basis and comprise four segments, which are as follows: Pharmaceutical, Animal Health, Consumer Care, and Alliances (which includes the company’s relationship with AstraZeneca LP).”

E.I. du Ponte (DD)

“E. I. du Pont de Nemours and Company operates as a science and technology based company worldwide. The company’s subsidiaries and affiliates conduct manufacturing, seed production or selling activities. It has operations in approximately 90 countries.”

Summary

Even though the Dow Jones Industrial Average recently broke through the 17,000 barrier representing an all-time high, it does not automatically follow that it is dangerously overvalued. 17,000 is just a number representing the sum of the component prices divided by a divisor. As such, it is, in essence, a reflection of the price of the 30 Dow components. However, in order to determine valuation, it must simultaneously be measured relative to the earnings power (fundamental value) of each component.

The 30 earnings and price correlated graphs of each of the 30 Dow constituents was presented in order to provide a clear perspective of price related to fair value based on the earnings power of each company. The objective behind this exercise was to provide the reader a more comprehensive perspective and understanding of the relative valuation of each component in order to establish a clearer point of view of the current state of the stock market as represented by the Dow Index.

Conclusions

Based on a fundamental analysis of each of the 30 Dow components, it has become clear that the Dow is not as high as it looks based on the fair value of its constituents. No less than half of the 30 Dow stocks are currently trading at reasonable valuations based on each company’s earnings power. There are a few Dow components that appear pricey today. Yet even though the index is at an all-time high, there is still an amazing amount of value to be found within the group.

Disclosure: Long TRV,IBM,CVX,CSCO,PFE,T,WMT,UNH,VZ,MSFT,INTC,GE,MCD,UTX,CAT,JNJ,PG,KO,V at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.