Today’s U.S. employment report was a very good one. It was strong enough to suggest good economic momentum but not so strong as to alarm the Federal Reserve.

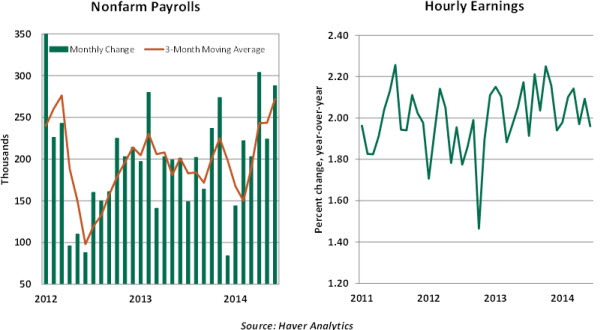

The unemployment rate dropped to 6.1% in June from 6.3% in the prior month. Payroll employment advanced 288,000. Not only do the headline numbers represent solid improvements in the labor market, but underlying details reinforce the message.

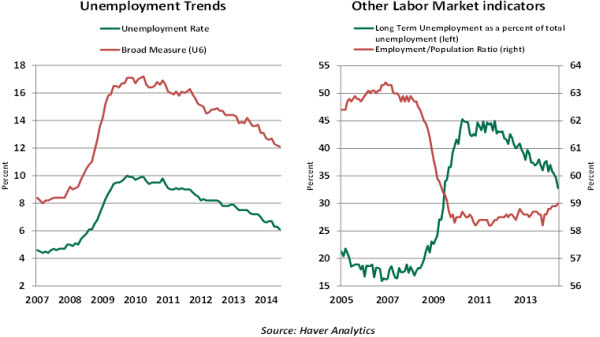

Data from the household survey, which is the source for the jobless rate, reflect firming employment conditions. An unchanged participation rate (62.8%) in June is acceptable, although an increase is the preferred option. The jobless rate is down 0.6 percentage points in the first six months of the year. The broadest measure of unemployment (U6), inclusive of official unemployment, part-time employment and those marginally attached, stands at 12.1% versus 13.1% in December 2013.

The share of long-term unemployed (32.8% versus 34.6% in May) declined sharply in June and has fallen nearly five percentage points in the last six months, the largest drop in this time span across the current expansion. The median duration of unemployment (13.1 weeks) is the lowest in a little over five years. The employment-population ratio, at 58.9%, is the highest in five years.

A similar message of strength is visible in the establishment survey data. Payrolls averaged 272,000 in the last three months, the third-best reading in the current upswing. Revisions added 29,000 more jobs during the April and May months.

There were widespread employment gains during June. In the goods-producing sector, factory employment rose 26,000 and construction jobs moved up 6,000. In the services component, private-sector employment increased 262,000 in June, reflecting an expansion of payrolls across several categories – retail establishments (+40,000), professional and business services (+67,000), leisure and hospitality (+39,000), and health care (+21,000).

Although the job news has been getting progressively better, it has yet to translate into worrisome gains in earnings. Hourly earnings increased just 2.0% from a year ago.

Some will certainly point out that unemployment has fallen far faster than the Federal Reserve expected and now stands just above the Federal Open Market Committee’s consensus estimates for the end of the year. (And joblessness is not that far from Fed estimates of the long-term unemployment rate.) Should recent trends continue, the timing of monetary tightening could certainly move forward.

Yet the absence of accelerating wage gains implies that there remains quite a bit of slack in the labor market. If wages fail to accelerate, inflation pressures are unlikely to emerge. The Fed, particularly Janet Yellen, would find conditions more troubling only if wages advanced at a higher pace than current readings.

So there is much to celebrate as we adjourn for the Independence Day weekend. We hope that you and your families enjoy the holiday.

© Northern Trust